U.S. House Passes Crypto FIT21 Bill with Strong Democratic Backing

The U.S. House approved the FIT21 Act, marking a historic step in digital asset regulation, but its future in the Senate remains uncertain.

Miyuki

Miyuki

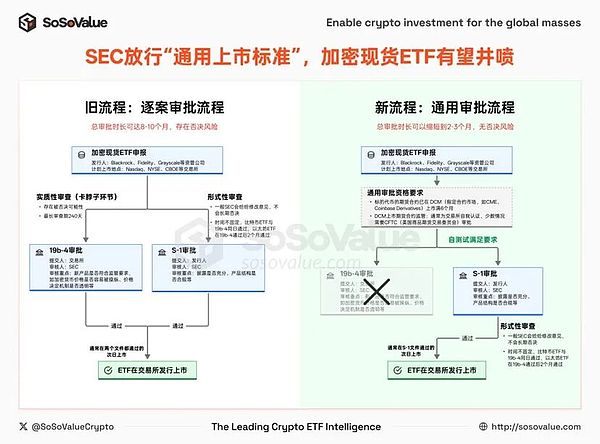

Before the release of this new regulation, crypto spot ETFs had to go through a case-by-case approval process and had to cross two approval thresholds:

1. 19b-4 rule change approval — — the exchange applies to the SEC to amend the exchange rules. This is a substantive approval and there is a possibility of being rejected by the SEC.

2. S-1 prospectus approval — — the ETF issuer submits it to the SEC for approval, disclosing details such as the fund structure, manager, and fee rates. This is more of a formal review. This dual-approval model is not only lengthy but often hampered by political wrangling and compliance disagreements. For example, Bitcoin spot ETFs saw a surge in applications in 2021, but were consistently rejected by the SEC at the 19b-4 stage from 2021 to 2022. A new batch of applications was submitted from May to July 2023, and finally, on January 10, 2024, both the 19b-4 and S-1 filings were approved simultaneously, after nearly eight months of back-and-forth. The SEC's adoption of the "Universal Listing Standard" on September 17, 2025, brought about fundamental changes. The standard clarifies that eligible commodity ETFs no longer need to submit a 19b-4 application on a case-by-case basis; instead, they only need to go through the S-1 approval process, significantly reducing approval time and costs. ETFs that meet the standard must meet one of the following three paths: 1. The underlying commodity must be traded on an ISG (Intermarket Surveillance Group) member market, such as the NYSE, Nasdaq, CME, and LME. 2. The futures contract for the underlying commodity must have been traded continuously on a Designated Contract Market (DCM) for at least six months, and a Comprehensive Sharing Surveillance Agreement (CSSA) must have been established between the exchanges. DCMs are compliant exchanges authorized by the U.S. Commodity Futures Trading Commission (CFTC), such as CME, CBOT, and Coinbase Derivatives Exchange. 3. An existing ETF must be listed on a U.S. national securities exchange, with at least 40% of its assets allocated to the underlying commodity. Because most crypto assets are considered "commodities," this rule is practically tailor-made for crypto spot ETFs. The second path is the most feasible: as long as a crypto asset has a futures contract running for at least six months on an exchange like CME or Coinbase Derivatives, it can bypass the 19b-4 approval process, potentially allowing for a rapid launch of its spot ETF.

Figure 1: New and old crypto spot ETF listing approval process (data source: SoSoValue)

Compared with the old model, the changes brought about by the new regulations are mainly reflected in two aspects:

1) Simplified approval path: 19b-4 is no longer a "roadblock". Under the old model, crypto spot ETFs required simultaneous approval of both the 19b-4 rule change and the S-1 prospectus, neither of which could be neglected. This was the case with previous Bitcoin and Ethereum ETFs: the 19b-4 review period, which stretched to 240 days, was a significant factor in slowing down the process. Under the new regulations, as long as the product meets unified standards, the exchange can proceed directly to the S-1 review process, eliminating the repetitive 19b-4 negotiations and significantly shortening the listing cycle. 2) Shift in the Center of Review Authority: The CFTC and DCM will play a more critical role. The eligibility review of futures contracts has gradually shifted from the SEC to designated contract markets (DCMs) and the CFTC (U.S. Commodity Futures Trading Commission). Under the current system, DCMs have two primary methods for listing new contracts: • Self-Certification: DCMs simply submit a self-certification to the CFTC one business day before the contract launch. If no objections are received, the contract automatically becomes effective. This typically requires the spot market to demonstrate price transparency, ample liquidity, and manageable market manipulation risks. • Voluntary Approval: If a contract is controversial, a DCM can proactively apply for CFTC approval, providing stronger legal protection. This means that as long as the spot market for a particular crypto asset is sufficiently healthy, DCMs have significant autonomy in promoting its futures listings. Meanwhile, the SEC's review of the S-1 primarily focuses on the adequacy of information disclosure and compliance with product structure regulations, representing more of a "formal review." Overall, the SEC is transitioning from a case-by-case reviewer to a rule-setter. The regulatory approach is also shifting from "whether to allow" to "how to regulate." Under this framework, the launch of crypto spot ETFs will be more efficient and standardized. Second, which cryptocurrencies are most likely to benefit? The 10 major cryptocurrencies with existing futures contracts and ETF applications will be the first to see ETFs launched. Among existing DCMs (Designated Contract Markets), Coinbase's Coinbase Derivatives Exchange boasts the most comprehensive crypto futures product line, currently covering 14 cryptocurrencies. (See Figure 2 for details.) Figure 2: List of Futures Listed on Coinbase (Data Source: SoSoValue) According to SoSoValue data, there are currently 35 crypto spot ETFs in the approval queue, covering 13 currencies. With the exception of SUI, TRX, and JitoSOL, the remaining ten coins have all had futures listed on the Coinbase Derivatives exchange for over six months, and therefore fully comply with the general requirements of the new regulations. Figure 3: 10 mainstream cryptocurrencies with existing futures contracts and ETF applications will be the first to have ETFs launched (data source: SoSoValue) This means: • About 30 spot ETFs covering 10 cryptocurrencies: LTC, SOL, XRP, DOGE, ADA, DOT, HBAR, AVAX, LINK, BCH Expected to be approved quickly in the coming weeks or months; • The market is brewing the next wave of ETF "boom." For example, although cryptocurrencies like XLM and SHIB already have futures, no one has yet submitted a spot ETF application, making them likely to become the focus of the next wave of managers. III. When the interest rate cut cycle coincides with the ETF boom, what should investors pay attention to? ETF issuance progress, macro interest rate trends, cross-asset allocation, and capital flows. In the short term, the implementation of universal standards will significantly accelerate the launch of crypto ETFs, lowering the issuance threshold and attracting more institutional funds and compliant products. Meanwhile, the Federal Reserve cut interest rates by 25 basis points as expected on Thursday, with the dot plot signaling two more rate cuts this year. This marks the beginning of a cycle of rate cuts, and expectations of a devaluation of the US dollar are growing. Global capital is searching for new asset anchors. The forces of macro liquidity and institutional reform are colliding head-on: on one hand, the massive liquidity released by the US dollar system, and on the other, the potential for a surge in crypto ETFs. This intertwined force could reshape capital allocation logic, accelerate the deep integration of traditional capital markets and crypto assets, and even mark the starting point for a reshaping of the global asset landscape over the next decade. Against this backdrop, investors need to focus on four key areas: 1. ETF Issuance Pace: For crypto spot ETFs that comply with common rules, the S-1 prospectus often undergoes multiple updates prior to final approval, supplementing details such as fee rates and initial offering size. These updates often signal a countdown to market launch. 2. Macroeconomic Environment: The Federal Reserve's interest rate path, dot plot projections, and the trend of the US dollar index will determine the direction of risk appetite shifts and serve as key clues to asset pricing. Figure 4: Expected Path of Federal Reserve Rate Cuts (Source: SoSoValue) 3. Cross-asset Allocation: During periods of dollar weakness, gold, commodities, and crypto assets often complement each other. By diversifying their exposure, investors can mitigate risk while capturing multiple yield curves. 4. Fund Flows: Compared to price fluctuations, daily net inflows into ETFs better reflect market sentiment and trends and are often more forward-looking, helping investors seize opportunities before market reversals. Figure 5: Bitcoin spot ETF single-day net inflow (data source: SoSoValue) Figure 6: Ethereum spot ETF single-day net inflow (data source: SoSoValue) In summary, the new regulations coupled with the interest rate cut cycle are paving the way for crypto ETFs. Opening the "double gates" of institutions and liquidity. For investors, this is both a new window of opportunity and a profound reshaping of asset allocation logic.

The U.S. House approved the FIT21 Act, marking a historic step in digital asset regulation, but its future in the Senate remains uncertain.

MiyukiBitcoin rebounds to challenge $70,000 again. The U.S. House of Representatives passes the "21st Century Financial Innovation and Technology Act," with Pelosi shifting to vote in favor.

MiyukiHong Kong has ruled that Worldcoin violates privacy regulations and has ordered the cessation of iris and facial image collection from its citizens.

Weiliang

WeiliangSEA has emerged as a hub for transnational criminal networks, primarily originating from China. These organisations exploit millions of victims globally through sophisticated scams like pig butchering schemes.

Kikyo

KikyoWorldcoin faces global sanctions over privacy concerns, with bans in multiple countries including France, India, Hong Kong, and Brazil. Despite its ambition to offer universal financial access, questions remain about its approach and regulatory compliance.

Joy

JoyThe SEC has approved eight spot Ether ETFs, marking a significant development following speculation that ETH might be classified as a security. This approval comes just months after the SEC granted similar approval for spot Bitcoin ETFs.

Catherine

CatherineMeta unveils Chameleon, its entry into the multimodal AI race, aiming to process text, images, and sound in one model. However, facing criticisms over misinformation and harmful ads, Meta's advertising prowess contrasts with its AI development.

Weatherly

WeatherlyA Texas judge rules that Ian Balina sold unregistered securities through Sparkster (SPRK) tokens, marking a partial victory for the SEC in its 2020 lawsuit.

Alex

AlexA Binance executive collapsed in a Nigerian court during arraignment on money laundering and tax evasion charges, leading to an adjournment for medical attention.

MiyukiLearn how the FIT 21 bill’s decentralization test defines digital commodities, crucial for protocols aiming to decentralize.

Weiliang