How many paths does Bitcoin have on its future path?

Take a look at an article by the infamous Mircea Popescu, which offers rare insight into the path Bitcoin might take in the future.

JinseFinance

JinseFinance

BitDeer (US stock code BTDR) updated its November operating figures. The A2 mining machine (Sealminer A2) that the market is concerned about has started mass production, with the first batch of 30,000 units sold to the outside world.

The first growth curve: self-developed chips, sales of mining machines, and self-operated mining farms.

Sealminer's ability to develop chips has always been the core competitiveness of mining machine manufacturers. In the past six months, Sealminer has successfully completed the first chip production of A2 mining machine chips and A3 mining machine chips.

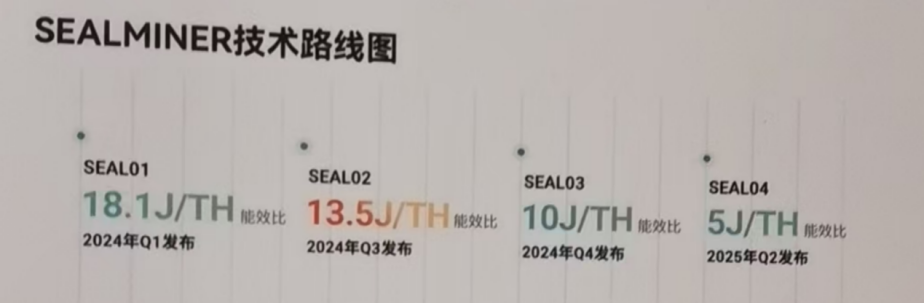

Figure 1: BitDeer Technology Roadmap

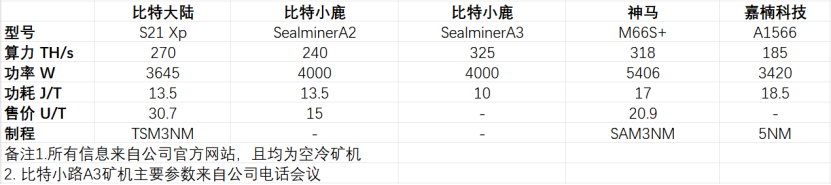

Figure 2: BitDeer Main Mining Machine Parameters Prediction

According to public information, the current operating parameters of the A2 mining machine are in a historical leading position among all the mining machines currently on sale and in operation on the market. Although the A3 has not yet been officially launched, judging from the known parameters, it will become the world's largest single hash computing power mining machine with the leading energy efficiency ratio. The possibility of this product being sold to the outside world in the short term is extremely low, and it will be used first to deploy self-operated computing power.

Figure 3: The latest mining machine companies and mining machine parameters in the world

In terms of electric fields, as of the end of November, the company has completed the deployment of 895MW of electric fields in the United States, Norway and Bhutan. There are also 1645MW projects under construction, of which 1415MW will be completed in the middle and late 2025. According to the minutes of Guosheng's conference call, the company has set up a special department dedicated to the acquisition of more power plant projects, and is still expected to add more than 1GW of power plants in 2026; the average electricity price of all self-operated power plants is less than US$0.04/kWh, which is in an absolute leading advantage compared with its peers.

Figure 4: Bit Xiaolu's built and under-construction electric fields

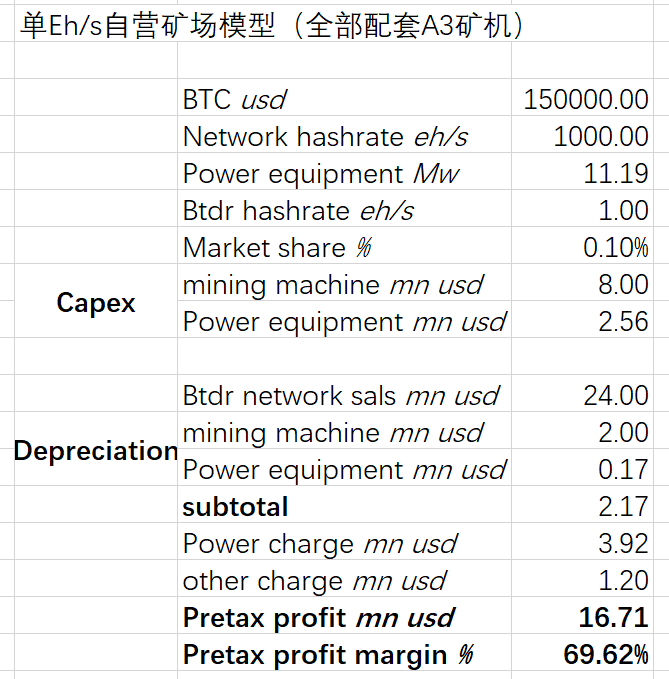

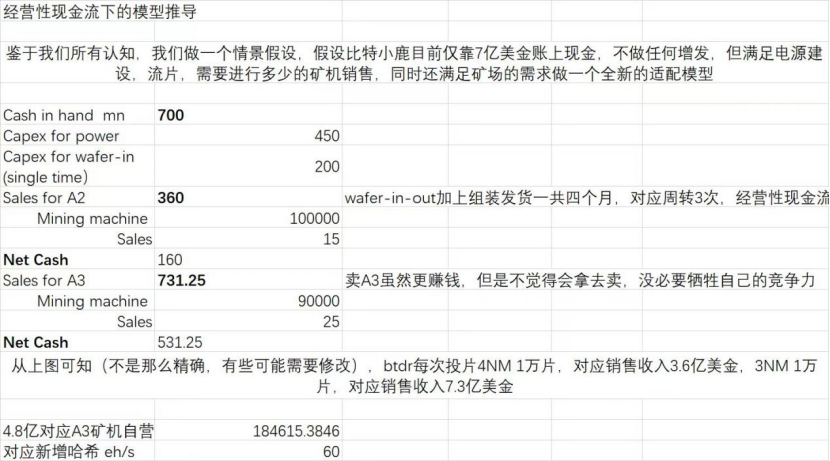

In view of the above operating figures, the Bit Xiaolu 1EH/s model is as follows:

Figure 5: Bit Xiaolu single EH/s model

The key assumptions of the model include that the mining machine depreciation period is 4 years (5 years under North American financial standards), the electric field depreciation period is 15 years (20 years under North American financial standards), and other costs (including manual operation and maintenance, etc.) account for 5% of the revenue (the company's historical operating figures are only 1-1.5%). According to the model, the shutdown price of BitDeer's self-operated mining farm is 35,000 US dollars in Bitcoin.

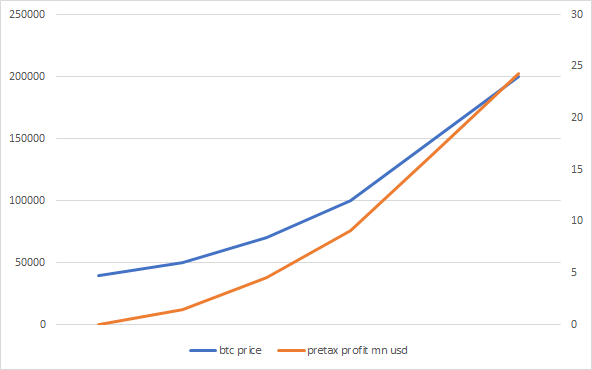

Figure 6: Relationship between the pre-tax profit margin of BitDeer’s self-operated mine and the price of Bitcoin

When the price of Bitcoin exceeds 150,000 US dollars, the pre-tax profit slope of BitDeer’s self-operated mine will exceed the rising speed of Bitcoin. If the price of Bitcoin reaches 200,000 US dollars, the pre-tax profit margin of BitDeer’s self-operated mine will be close to 80%.

For BitDeer's first growth curve, the market still has two major concerns. .

About the ratio of mining machine sales and self-use. As mentioned earlier, Xiaolu is expected to reach a power field reserve of 2.3GW by mid-2025. If all the above mines are equipped with A3 mining machines, the self-operated computing power will be close to 220EH/s. According to the linear growth of the computing power of the whole network, it will account for about 20% of the computing power of the whole network by the end of 2025. According to the company's 2024 third quarter report, the company has cash and general equivalents of US$291 million, and completed US$360 million of convertible bonds at the end of November. With the addition of US$40 million options, the company currently has cash on hand of about US$690 million. According to the company's electric field investment and self-operated needs, due to the time difference between the laying of self-operated computing power and output, it may need to raise funds again, but Xiaolu's current stock price is undervalued, and the company is not willing to issue additional shares. Therefore, based on cash flow needs, 10,000 4nm wafers can generate an annualized net cash flow of US$480 million (calculated based on 4-month mining machine turnover). If this cash flow is reinvested into self-operated computing power (all equipped with A3 mining machines), the computing power will increase by 60eh/s. After 2025, Xiaolu's overall cash flow will no longer be a problem, and the sales of mining machines plus the mining business can ensure that the bitcoins produced by Xiaolu are no longer used for sales, but for self-sustaining.

Figure 7: Operating cash flow derivation model

2. About the competitive relationship between Bitmain and Xiaolu. The core of the commercial competition relationship is still the performance of mining machines and the cost of self-operated computing power. According to public data and laboratory data, Xiaolu has sufficient competitive advantages in both the mining machines it has produced and the cost of self-operated computing power. With the development of high-end process chips, mining machines, as the downstream of the industry, will also be affected by the upstream competition pattern.

Second growth curve AI computing power

In addition to mining machine sales and self-operated mines, the company's November operating figures show that it has begun to deploy Nvidia H200 chips in the TIER3 data center of intelligent cloud services for AI computing power construction.

Mr. Wu Jihan wrote an article "The Beauty of Computing Power" in 2018: Computing power may be an effective means for humans to reach a higher civilization, and it is also the most effective way to fight against entropy increase.

The original intention remains.

According to the Tianfeng Research Report, the current power deployment plan of major North American Bitcoin mining companies exceeds 1GW, 3471MW has been powered on, and 5969MW is expected to be completed by 2028. The above power deployment will meet 56% of the electricity demand of North American data centers. In the Tianfeng conference call on December 6, BitDeer said that it will deploy Nvidia's high-end chips with at least 200MW of electricity in the short term, and start serving customers such as MEGA 7 for cloud calls, following the COREWEAVE model.

Investment advice and valuation

The right time, right place and right people are the best explanation for BitDeer's investment at the current point in time. The company has accumulated a lot of experience, and the first growth curve and the second growth curve are expected to rise simultaneously, forming a synergy. It is the most cost-effective target among the current US mining stocks.

However, how to value the company and how to define the company's value in the profit model are challenging. Neither the profit valuation generated by the sale of a single mining machine nor the valuation of the self-operated mining farm is sufficient to cover the actual operating conditions of Xiaolu. Therefore, two types of business models are fitted as follows:

Figure 8: Bit Xiaolu mining machine sales model calculation

Figure 9: Bit Xiaolu self-operated mining farm prediction model

The current valuation of mainstream North American mining companies at an average of $170 million/EHs is closest to the market consensus. It is reasonable to believe that in the next two years, Xiaolu's actual self-operated mines will reach between 120-220EH/s, with a market value of approximately US$20.4 billion to US$37.4 billion, 4.8-9.7 times the current share price.

Figure 10: Valuations of major North American mining companies

Investment risks:

1. Bitcoin price fluctuation risk;

2. TSMC wafer risk caused by sanctions.

Take a look at an article by the infamous Mircea Popescu, which offers rare insight into the path Bitcoin might take in the future.

JinseFinanceSince its creation in 2009, Bitcoin has undergone multiple forks, resulting in new cryptocurrencies and variations of the original protocol. As of May 2024, there have been over 100 Bitcoin forks, with varying degrees of adoption and success.

JinseFinance前赴后继的创业者们并未止步不前,他们不断探索新的解决方案和应用场景。

JinseFinanceOMNI, Cycle Network, chain abstraction, detailed explanation of the four little dragons of chain abstraction: Omni Network, Cycle Network, Initia, Polymer Golden Finance, chain abstraction has become a life-saving straw for cross-chain bridges to find a way out.

JinseFinanceLooking far ahead, there is only one winding and rugged road ahead for BTC (Bitcoin), and that is upward.

JinseFinanceThe mining difficulty and currency price of the entire Bitcoin network are the same and uncontrollable for all miners. Miners can only increase their income by expanding their own computing power.

JinseFinanceCameron and Tyler Winklevoss filed to launch a spot Bitcoin ETF on July 1, 2013. BlackRock has revealed it intends to launch a product in 10 years.

JinseFinanceDogecoin founder Bill Markus comments on Bitcoin's recent price fluctuations, highlighting the uncertain future of the cryptocurrency amid varying market sentiments.

EdmundJinseFinanceJinseFinance

EdmundJinseFinanceJinseFinance