Microsoft Renames Bing Chat to Copilot in Direct Challenge to ChatGPT

Microsoft has unveiled plans to transition from Bing Chat to Microsoft Copilot, signalling a strategic move aimed at entering the competitive arena with ChatGPT.

Catherine

Catherine

Competitive Landscape and Market Share (Exchange)

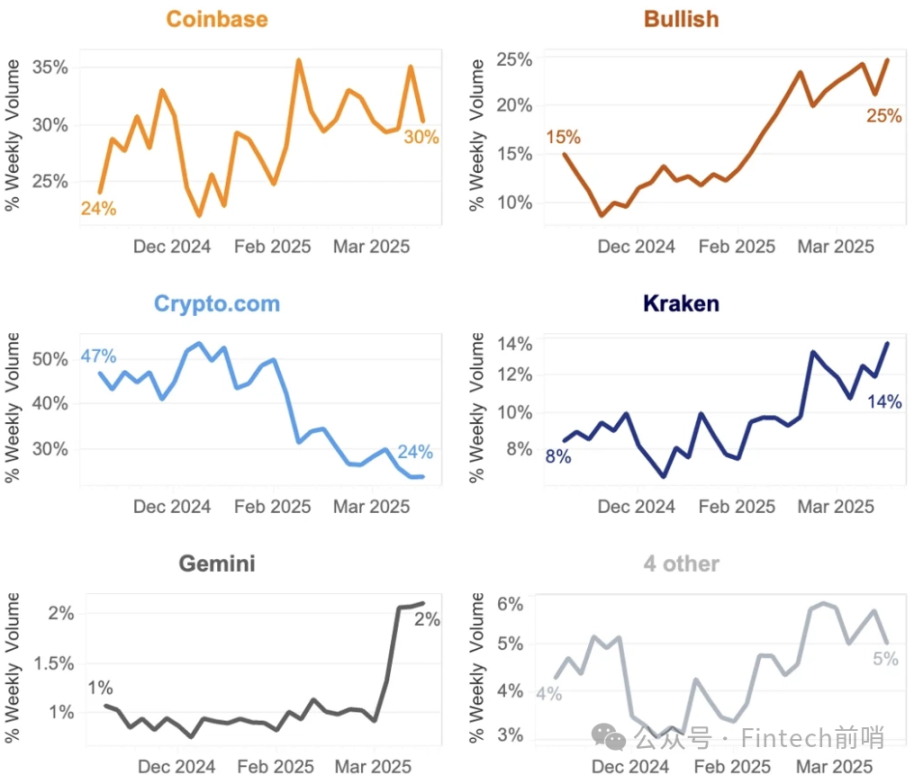

In the landscape of compliant spot exchanges, Gemini is in the "leading tier, but not the first tier." According to Kaiko's comprehensive ranking, its spot market share rose from approximately 1% to 2% in the spring of 2025, demonstrating a resilient "two steps forward, one step back" pattern. This period of growth was followed by a partial reversal, reflecting a coexistence of upward momentum and volatility in the compliant market. Coinbase remains the leading US stock market, with clear advantages in its integrated retail and institutional operations. Its synergy with derivatives businesses like options creates greater economies of scale and brand premium. Kraken, a long-established compliant US exchange, has a long history in the EU market and a more solid regional presence. Regarding retail entry, Robinhood's acquisition of Bitstamp (announced in 2024, closing in 2025) strengthens its institutional and global capabilities, further increasing competitive pressure on retail entry points in the US compliant market. On the primary market, Bullish's successful 2025 IPO has heightened the capital market's risk appetite and valuation for assets on compliant exchanges, providing valuable insights for Gemini's potential future offering window. Within this landscape, we believe Gemini's market share and ranking are not among the top tier, and its exchange products and services are poorly differentiated. While focused on compliance, Gemini's scale is too small and lacks a significant edge compared to its US competitors. User Reputation and Product Variety: In terms of user reputation and product coverage, Gemini's listing and availability align with mainstream compliant platforms: it currently supports over 70 crypto assets and covers over 60 countries (Source: S-1/Reuters). Third-party reviews show a 4.8/5 rating on the App Store and a 4.3/5 on Google Play, indicating generally good mobile experience and stability. However, reviews on Trustpilot are quite mixed, with negative feedback primarily focused on areas like risk control triggering and customer service response, suggesting room for improvement in user communication and process experience within its compliance module. In terms of product diversity, Gemini offers a broad and comprehensive product line: it offers both institutional custody and trading stacks, as well as simultaneous developments in derivatives, credit cards, stablecoins, and the NFT ecosystem, forming a relatively complete business matrix. However, there remains a noticeable gap in depth and activity (such as order book thickness and institutional market-making coverage) compared to first-tier platforms. This not only impacts fee negotiation power but also directly impacts unit economics. Given that the S-1 currently provides inadequate breakdown of key operating metrics, further monitoring is needed to assess the company's progress in liquidity acquisition, institutional partnerships, and fee structure improvements. 02 History and Business Status Founding and Positioning Gemini was founded in 2014 by Cameron and Tyler Winklevoss in New York as Gemini Trust Company, LLC. On October 5, 2015, the New York Department of Financial Services (NYDFS) granted it a Limited Purpose Trust license under the New York Banking Law, establishing its foundational approach of prioritizing safety and compliance. In terms of compliance and auditing, Gemini completed SOC 2 Type 1, conducted by Deloitte, in 2018, and passed both SOC 1 Type 2 and SOC 2 Type 2 (covering the exchange and Gemini Custody) on January 19, 2021. Early on, Gemini differentiated itself from its peers by positioning itself as a "compliance template."

In terms of related parties and business cooperation, the company has signed service agreements with entities jointly held by WCF (such as Elysian, Salient, and WCM) to obtain key operational support such as equipment leasing, cloud services, data centers, and management consulting; for the C-end and payment ecosystem, it has in-depth cooperation with multiple parties: first, it has linked its business with Ripple to expand Ripple USD (RLUSD) as the base currency for all spot trading pairs on the platform, and jointly launched an XRP reward credit card; second, it has cooperated with WebBank, and it has launched an XRP co-branded credit card as the issuing bank, expanding the application scenarios of encrypted payment and customer acquisition touchpoints under a compliance framework.

Platform size (as of 2025-06-30)

Lifetime trading volume ≈ $285bn;

Assets on our platform (AUC) > $18bn;

Monthly trading users (MTUs) ≈ 523k; Institutional clients ≈ 10k;

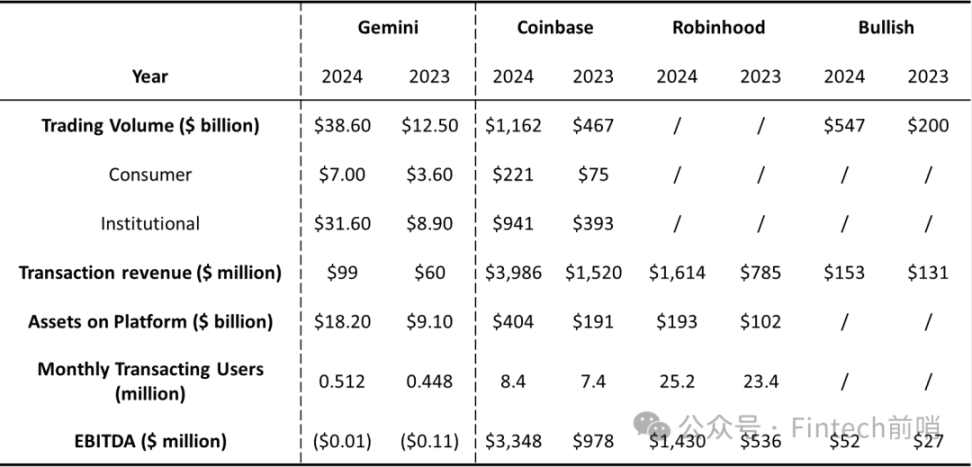

Cumulative processed transfer amount > $800bn. The above information is available from multiple authoritative secondary sources reporting on S-1 extracts/database pages: Investopedia, Renaissance Capital/IPO-Scoop, Investing.com, etc. Product Coverage Supplement (S-1/DRS Extract): Supports over 80 trading assets, Custody covers over 130 assets (as of June 30, 2025). S-1/A Filing Index (for original verification): SEC EDGAR CIK: 0002055592 (latest S-1/A index page). 03 Financial Analysis: Financial Analysis: Growth Fails to Overshadow Losses, Severe Dependence on External Funding. Performance Overview: Significant Losses. 2024 Operating Data: Demonstrated Growth, Achieving 512,000 Monthly Trading Users, Annual Trading Volume of US$38.6 Billion, and Platform Custody Assets of US$18.2 Billion. Continuous Significant Losses: Growth is offset by significant losses. A net loss of US$159 million was recorded for the 2024 period. Losses worsened in the first half of 2025: The company achieved revenue of $68.6 million and processed $24.8 billion in spot trading volume, but suffered a net loss of $282.5 million during the same period. Balance Sheet and Cash Flow Status: Operating cash flow remains negative: The company's core business has yet to achieve self-sustaining profitability. Operating cash flow was -$109 million in 2024 and -$207 million in 2023, primarily due to adjustments for non-cash items and changes in working capital. Cash Reserves (as of December 31, 2024): $42.8 million in cash and equivalents, $28.4 million in restricted cash. Client Fund Segregation: $575.6 million in client funds are held in segregated custody, dedicated to client interests, demonstrating the company's commitment to asset security and compliance. Survival Mode: Reliance on External Funding. High-Risk Financial and Asset Strategies: Bitcoin "Treasury Asset" Strategy: The company uses BTC as a core reserve asset and prefers to finance its holdings through US dollar debt rather than directly selling BTC. This can alleviate cash pressure during bull markets, but it also amplifies cyclical risks during downturns. Clearing Historical Risks ("Earn Incident"): Following regulatory requirements from the NYDFS, Gemini has returned over $2 billion worth of crypto assets to Earn users and paid a $37 million fine. While costly, this move has substantially resolved the historical issue, repaired some of its reputation, and reduced contingent liability risks.

Source of funds: Credit support from multiple parties to maintain operations:

Core support comes from Founders Fund (WCF): As of the end of 2024, the company's survival is heavily dependent on the continued "blood transfusion" from WCF, including:

1. Outstanding cryptocurrency loans: 5,054 BTC, 26,629 ETH

2. Outstanding US dollar principal: US$116.5 million

3. WCF also holds all convertible bonds issued by the company.

External credit supplemented: Received a $75 million credit line from its strategic partner Ripple as additional liquidity.

Future Plans: IPO Focused on Debt Repayment

Proceeds from this IPO will be primarily used to repay third-party debt, optimize capital structure, and reduce leverage.

Summary

Gemini's financial condition is precarious, with significant net losses largely driven by non-cash or highly volatile items, such as fair value adjustments on related-party convertible bonds, interest on borrowings, and changes in the fair value of its crypto holdings. The company has long relied on external funding from the two founding brothers. The purpose of the IPO financing is to prioritize the repayment of third-party debts, but the US$400 million financing amount still cannot fully cover all the company's debts, and the company's operating cash flow outflows an average of 100-200 million yuan per year. The funds raised from the IPO can only support the company's operations for 2 years.

Analysis of Gemini's Own Operational Status

Operational Data: Gemini achieved relatively modest growth in both user numbers and trading volume in 2024. The number of monthly trading users increased from 448,000 in 2023 to 512,000 in 2024, and the total trading volume increased from US$12.5 billion to US$38.6 billion. Platform assets also saw significant growth, increasing from $9.1 billion to $18.2 billion. Profitability: However, despite improved operating figures, Gemini's profitability remains a significant challenge. While EBITDA has improved slightly, from negative $110,000 in 2023 to negative $13,000 in 2024, it remains negative. This means Gemini's revenue cannot cover its operating costs, including employee salaries. Its path to profitability remains uncertain, raising concerns about profitability. Comparison with Peers' Operating Data: Trading Volume: Gemini's trading volume is significantly lower than that of Coinbase and Bullish. Coinbase's trading volume in 2024 is projected to reach $1.162 trillion, Bullish's $547 billion, and Gemini's just $38.6 billion. Gemini's primary revenue comes from retail investors. Despite a significant increase in institutional trading, its total trading volume lags far behind Coinbase's. User size: Gemini's user base is significantly smaller than both Coinbase and Robinhood. Coinbase's monthly trading users in 2024 will be 8.4 million, Robinhood's will be 25.2 million, and Gemini's will be just 512,000. This represents a significant gap in user numbers compared to Coinbase and Robinhood. Profitability: Coinbase and Robinhood are expected to be profitable (with positive EBITDA) in 2024, while Gemini's EBITDA remains negative. Coinbase demonstrates a clear advantage in profitability. Platform Assets: Coinbase and Robinhood have significantly higher platform assets than Gemini. Coinbase's platform assets in 2024 are expected to be $404 billion, Robinhood's $193 billion, and Gemini's $18.2 billion.

Summary

In summary, despite its growth, Gemini still lags significantly behind its main competitors in terms of market share, user base, and profitability, requiring further improvement in profitability and market competitiveness. Therefore, the company's core competitiveness lies not in market share but in its differentiated compliance strategy.

Founders and Background

Key Figures: The company was founded and led by twin brothers Cameron and Tyler Winklevoss. They are widely known for their early legal dispute with Mark Zuckerberg over Facebook's founding rights. They used the settlement funds to become early investors in Bitcoin and staunch advocates of cryptocurrencies.

Serial Entrepreneurship and Investment: Prior to founding Gemini, they established Winklevoss Capital in 2012 as their family office and venture capital vehicle. Through the firm, they actively invested in numerous cryptocurrency and technology startups, building a broad network within the industry ecosystem.

Political Involvement and Policy Lobbying

Open Support for the Trump Campaign: The Winklevoss brothers are the most prominent supporters of Donald Trump in the crypto industry. In 2024, the two each donated $1 million worth of Bitcoin to Trump's campaign and publicly criticized the Biden administration's "war on crypto," arguing that its regulatory policies are stifling innovation. Systematic Political Donations and Lobbying: Their donations are not isolated acts, but part of a broader $190 million wave of political contributions from the crypto industry. According to reports from the Financial Times and other media outlets, the Winklevoss twins, along with key figures from companies like Coinbase, Ripple, and a16z, have invested vast sums of money through Super PACs, aiming to systematically influence the American political landscape. 05 Summary: Investment Value Ranks Bottom Among Verticals Despite Gemini's foray into compliance and its diligent efforts to build a diversified product portfolio encompassing spot trading, derivatives, stablecoins, and payments, a deeper analysis of its financials, operational data, and competitive landscape reveals that its investment value is near the bottom of the regulated crypto exchange market. 1. Weakening Differentiation: Its "compliant" label no longer provides a sufficiently wide moat against similarly licensed giants like Coinbase and Kraken. The exchange's products and services are poorly differentiated, and Gemini's small scale hinders its ability to generate strong network effects and cost advantages. Its "compliant" selling point has failed to translate into sustained market share leadership or profitability. 2. Dire Financial Condition: Sustained and growing losses, perennially negative operating cash flow, and heavy reliance on funding from the founders' fund reveal the fundamental fragility of its business model. The IPO's primary purpose is clearly to repay third-party debt, making it more of a survival measure to maintain operations than a strategic expansion to drive future growth. The funds raised will only cover approximately two years of the company's cash burn, leaving the path to profitability distant and uncertain. 3. Significant operational data gap: Gemini's operational data reveals a comprehensive gap with the industry leaders. Whether in terms of trading volume, monthly trading users, platform asset size, or profitability, Gemini lags far behind competitors like Coinbase and Robinhood. With Robinhood's acquisition of Bitstamp, market competition will intensify, further squeezing the space left for second-tier players like Gemini. Therefore, for investors seeking compliant cryptocurrency trading platforms, Gemini is not an ideal investment. Allocating capital to industry leaders with solid market share, resilient business models, and demonstrated profitability, such as Coinbase, Kraken, and Robinhood, is undoubtedly a more prudent and wise choice.

Microsoft has unveiled plans to transition from Bing Chat to Microsoft Copilot, signalling a strategic move aimed at entering the competitive arena with ChatGPT.

CatherineCircle, a prominent stablecoin issuer, has made a strategic investment in Sei Network, a layer-1 blockchain

Aaron

AaronGoogle and the Malaysian government team up to transform the digital landscape, focusing on skilling and AI innovation, promising a brighter future for the workforce.

Hui Xin

Hui XinMuch like the others that have acquired the MPI license in Singapore before it, such as GSR, Coinbase, and Ripple, this approval allows StraitsX to operate as a licensed provider for digital payment token services.

Davin

DavinAnimoca Brands Japan unveils limited edition 'Liar, Liar' E-Figurine NFTs, merging digital and physical collectibles in San FranTokyo's Weebox. March 2024 release offers fans a unique 'phygital' experience, immortalizing beloved anime characters in exclusive runs of 1,000 NFTs per character.

Jixu

JixuCoinbase is contesting the US Treasury's sanction on Tornado Cash, a decentralized project, sparking a legal clash between crypto and regulators. The dispute centres on Tornado Cash's privacy-focused Ethereum platform, challenging government oversight in regulating decentralized applications and highlighting the broader conflict between regulatory control and individual privacy rights in the bitcoin industry.

JixuHex Trust obtains regulatory approval for cryptocurrency custody services in Dubai, advancing its Middle East expansion in line with the emirate's progressive regulations.

Hui XinRavi Menon, Managing Director of the Monetary Authority of Singapore (MAS), asserted that cryptocurrencies have fallen short as digital money, lacking stability as a medium of exchange or store of value.

AaronU.S. lawmakers, led by McHenry and Torres, challenge proposed digital-assets taxation, citing concerns over the broad 'Broker' definition impacting the digital asset community.

Hui XinThis surge in network activity resulted in a spike in transaction costs, soaring to over 7,000 Gwei (up from 100 Gwei the previous day) before stabilising around at the lowest point at 400 Gwei, according to Polygonscan.

Davin