Author:James Butterfill,Translator:Aki Wu said blockchain

Gold and Bitcoin are often compared as scarce non-sovereign assets. Although there has been a lot of discussion about their investment cases as value stores, few people have compared them at the production level. Both assets rely on mining — one is physical, the other is digital — to introduce new supply. The industrial characteristics of both are defined by cyclical economics, capital intensiveness, and deep connections to energy markets.

However, the mechanisms and incentives of Bitcoin mining differ from those of gold mining in subtle ways, and these differences ultimately have important implications for the economic structure and strategic layout of industry participants. This report will take you through some of their similarities, but more valuable, the substantial differences between them.

Asset scarcity stems from physical and computational mining

Gold mining is a centuries-old process that involves extracting and refining metals from the ground, which requires finding suitable deposits, obtaining permits and land rights, and using heavy machinery to extract the ore from the ground, and then chemically processing it to separate the metals for subsequent distribution.

In contrast, Bitcoin mining requires repeated computational processes to solve batches of Bitcoin transactions in a race to earn newly issued Bitcoins and transaction fees. This process, called Proof of Work, requires the procurement of rack space, electricity, and specialized hardware (ASICs) to efficiently run the calculations, and then broadcast the results to the Bitcoin network via an internet connection.

In both systems, mining is an unavoidable, high-cost process that underpins the scarcity of each asset: Bitcoin’s scarcity is maintained by code and competition; gold’s scarcity is determined by physical and geological location. Yet how scarcity is extracted, the economics of producers, and how they evolve over time bear few similarities.

Bitcoin Mining Economics: Competition, Technological Advancement, and Diversified Revenue Streams

The economics of gold mining are relatively predictable. Companies can generally forecast reserves, ore grades, and mining schedules with reasonable accuracy, although early forecasts can be wildly off: about one in five gold mining projects are profitable over their lifetimes. Major costs — labor, energy, equipment, compliance, and remediation — can be predicted with some accuracy in advance. Depreciation is primarily the normal wear and tear of equipment or depletion of reserves. The main uncertainty in the short to medium term is generally the stability of the gold market price, which is less volatile. Moreover, almost all of these input costs can be hedged effectively.

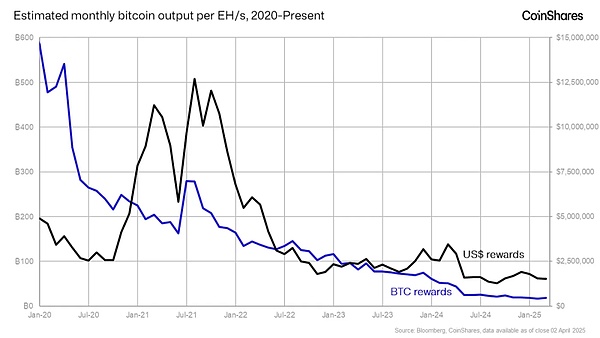

By contrast, Bitcoin mining is much more dynamic and unpredictable. Company revenues depend not only on the relative volatility of the Bitcoin market price, but also on its share of the global hash rate (ie: global competition). If other miners expand their operations more aggressively, your relative output may decline even if your mining operation remains the same. This is a variable that miners need to consider continuously during their operations.

So, our first difference is that unlike the relatively stable production forecasts of gold mining, Bitcoin miners face the challenge of production uncertainty, which comes from the entry and exit of other industry players and their changes in strategy.

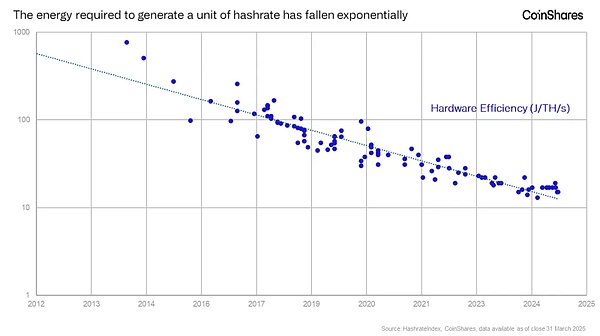

One of the most significant costs for Bitcoin mining companies is depreciation, particularly on ASIC equipment. The chips in these Bitcoin mining machines continue to improve in efficiency at a rapid pace, forcing companies to upgrade before the equipment naturally wears out in order to remain competitive. This means that depreciation occurs on the timeline of technological advancement rather than the physical wear and tear of the equipment. It is a major expense — — albeit a non-cash expense — — and stands in stark contrast to gold mining, where mining equipment has a longer lifespan because the equipment has already experienced most efficiency improvements.

The combination of changes in Bitcoin production, competition in the industry, and short-term depreciation cycles has resulted in miners facing constant pressure to reinvest in new hardware to maintain production levels — — what professionals often refer to as the “ASIC hamster wheel.”

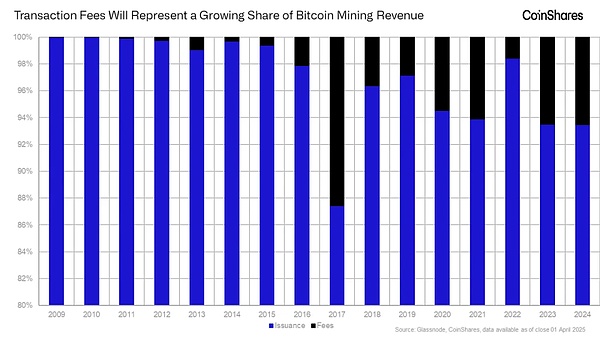

But again, Bitcoin has a fundamental difference that favors it over gold in terms of revenue structure. Gold miners profit only by extracting and selling the unreleased supply in reserves. However, Bitcoin miners profit both by extracting the unreleased supply and from transaction fees. Transaction fees provide miners with a revenue stream for the released supply that fluctuates based on demand for Bitcoin transfers. As Bitcoin approaches its 21 million supply cap, transaction fees will become an increasingly important source of revenue — — a dynamic that gold miners do not have.

Note: The y-axis portion shows the bottom range at 80%.

Finally, a major long-term advantage of Bitcoin mining is the ability to reuse a byproduct of operations — heat. When electricity passes through mining machines, large amounts of heat are generated, which can be captured and redirected for other uses such as industrial processes, greenhouse agriculture, or residential and district heating. This opens up entirely new revenue streams for miners. As mining machines become commoditized and their depreciation cycles extend, the impact of reusing heat is likely to grow further. Similarly, gold miners can benefit from selling byproducts such as silver or zinc, which are often identified in project planning and used as an element to offset the cost of gold production.

Bitcoin Mining Has a Brighter Environmental Future Than Gold Mining

Gold mining is known to be resource-extractive in nature and leaves a lasting physical footprint: deforestation, water pollution, waste ponds, and damage to ecosystems. In many regions, it also raises concerns about land rights and worker safety.

Bitcoin mining, on the other hand, involves no physical extraction and relies entirely on electricity. This provides an opportunity for integration with local infrastructure — not conflict. Because miners are mobile and interruptible, they can act as grid stabilizers and monetize otherwise wasted or isolated energy resources, such as flared gas, excess hydropower, or constrained wind and solar power.

What many people don’t realize is that Bitcoin mining also shows potential as a clean energy subsidy and can be used as a way to justify grid connection. By co-locating with renewable or nuclear power generation facilities, miners can improve the economics of their projects before grid connection — without relying on public funding subsidies.

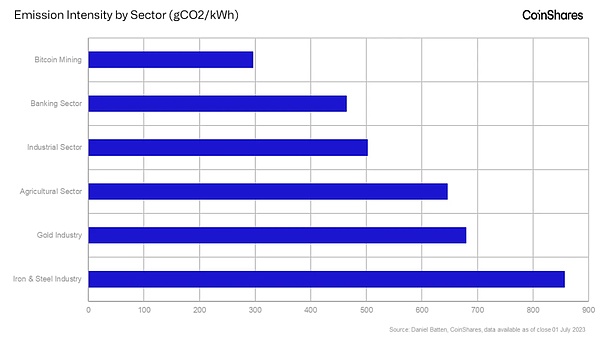

Finally, while this has been well documented, it’s worth noting that Bitcoin’s carbon emissions are lower on average and more transparent than those of traditional industries. Arguably, Bitcoin is even necessary in smoothing the transition to a grid dominated by renewable energy.

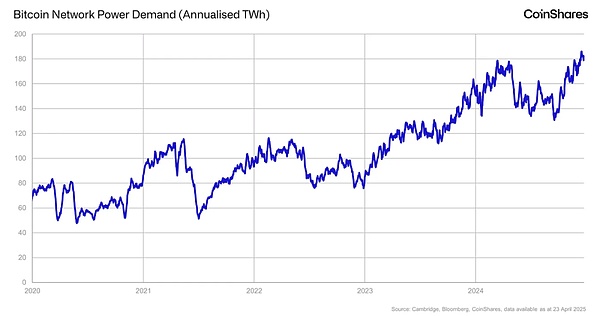

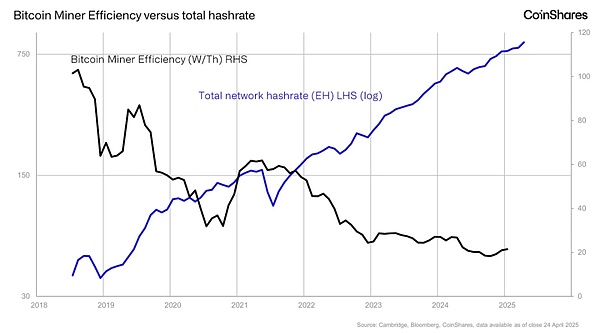

Since the peak of energy consumption in 2024, we have seen almost no increase in energy consumption, which is attributed to the continuous improvement of the efficiency of new mining hardware, and the current average power consumption is only 20 watts/terahash (W/Th), which is five times more efficient than in 2018.

Investment Characteristics of Bitcoin Mining: Fast Cycles and Technology Driven

Both industries are cyclical and sensitive to the prices of their production assets. But unlike gold miners, who typically operate on multi-year timelines, bitcoin miners can scale up or down operations more quickly based on market conditions. This makes bitcoin mining more flexible, but also more volatile.

Publicly traded bitcoin mining companies tend to trade like high-beta tech stocks, reflecting their sensitivity to bitcoin prices and broader risk sentiment. In fact, some market data providers classify publicly traded bitcoin miners as part of the tech sector, rather than the traditional energy or materials sectors.

Gold mining companies, however, are older and typically hedge future production, which can reduce sensitivity to gold price fluctuations. They are often classified as part of the materials sector and valued like traditional commodity producers.

Capital formation also differs. Gold miners typically raise capital based on reserve estimates and long-term mine plans. In contrast, Bitcoin miners tend to be more opportunistic, often raising capital in recent years through direct or convertible equity offerings to support rapid hardware upgrades or data center expansions. As a result, Bitcoin miners are more dependent on market sentiment and cycle timing, and typically operate with shorter reinvestment cycles.

Bitcoin Mining: Investment Opportunities in Energy, Computing, and Future Financial Networks

Gold and Bitcoin may tend to play similar macroeconomic roles in the long run, but their production ecosystems are structurally different. Gold mining is slower, physical, environmentally harmful, and resource-intensive. Bitcoin mining, on the other hand, is more rapid, modular, and may be increasingly integrated with modern energy systems.

For investors, this means that Bitcoin miners are an imperfect digital analog for gold miners. Instead, they represent a new class of capital-intensive infrastructure that merges investment opportunities in commodity cycles, energy markets, and technological disruption. Investors with a long-term investment horizon should view it as a distinct, emerging asset class with unique fundamentals, particularly in the context of growing transaction fees and evolving energy partnerships.

In our view, understanding these nuances is necessary to make informed investment decisions in an environment that is increasingly moving toward a distributed financial system.

As an investment, Bitcoin miners offer not only an investment opportunity in scarcity, but also in data center infrastructure, the growth of energy markets, and the monetization of computing power — a convergence that is not possible with traditional mining.

Bitcoin Mining Outlook

Overall, we believe that most potential macroeconomic scenarios post-Liberation Day remain favorable for Bitcoin. The introduction of reciprocal tariffs could drive higher inflation in the United States and its trading partners. The United States’ trading partners could face rising inflation while also dealing with growth headwinds. This dynamic could force them to adopt looser fiscal and monetary policies — measures that would typically lead to currency debasement, thus enhancing Bitcoin’s appeal as a non-sovereign, inflation-resistant asset.

In the United States, the outlook is more ambiguous. Both Trump and Bessant have expressed a preference for lower long-term yields, particularly on the 10-year Treasury. While the motivations behind this can be speculated — such as reducing the debt service burden or boosting asset markets — such a stance would typically favor interest-rate sensitive assets such as Bitcoin. However, the current situation is the opposite. The U.S. 10-year Treasury yield has fallen below 4%, but has since risen back to 4.5% and is now around 4.3%, due to suspicions about the unwinding of underlying trades, the damage to the U.S. reputation, and the increasingly precarious status of the dollar as the global reserve currency, while Trump’s insistence on an uncompromising tariff policy could further push inflation higher. However, this crisis is artificial and could soon be reversed through tariff concessions and agreements.

However, these signals could also reflect a decline in stock market expectations for future earnings, raising concerns about an impending economic slowdown. This presents a key risk for the broader market — namely Bitcoin — in the case of Bitcoin. If investors still view Bitcoin as a high-beta, risk-on asset, such sentiment could cause Bitcoin to trade in lockstep with stock markets during a global economic downturn, despite its narrative as a long-term store of value.

Nevertheless, Bitcoin has performed relatively well relative to stock markets since “Liberation Day.” This resilience highlights Bitcoin’s unique characteristics: it is a globally tradable, government-neutral asset with a fixed supply that is accessible 24/7/365. As a result, market participants are increasingly recognizing Bitcoin as a trusted, long-term store of value.

Miyuki

Miyuki