Coin Metrics: World Crypto Trading Map

Explore the “Kimchi Premium,” regional trading activity, and crypto market seasonality.

JinseFinance

JinseFinance

Speculative activity is heating up

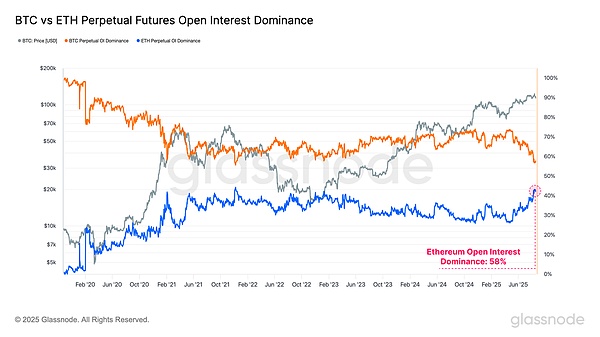

Ethereum has historically been viewed as a bellwether asset, and its outperformance cycles are often associated with "altcoin seasons" in the digital asset market.

Changes in the ratio of open interest in Bitcoin and Ethereum can be used to observe shifts in market participants' risk appetite. Current data is as follows: Bitcoin Open Interest: 56.7% Ethereum Open Interest: 43.3% Ethereum's recent rapid rise in share indicates a shift in market attention to the outside of the risk curve. Its open interest reached its fourth-highest level on record, confirming a significant increase in speculative activity. It's important to note that as the second-largest digital asset, Ethereum is one of the few assets capable of attracting institutional funding.

This trend is even more pronounced from the perspective of trading volume:

Ethereum perpetual swaps' share of trading volume soared to a record high of 67%, marking the most dramatic structural shift on record.

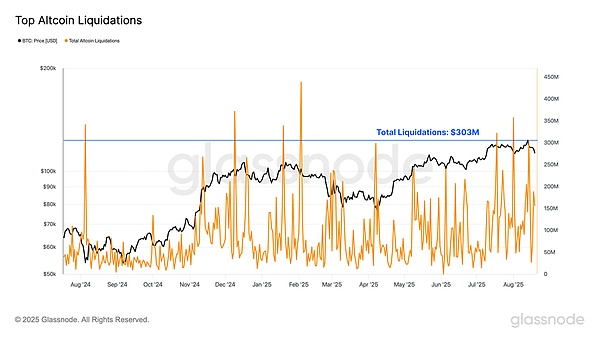

This significant shift in trading activity has intensified investors' focus on the altcoin sector, indicating an accelerated increase in risk appetite in the current market cycle. The Debate over Cycle Inflection Points: Measuring Bitcoin's performance from the lows of each cycle shows that in both the 2015-2018 and 2018-2022 cycles, the previous historical highs occurred 2-3 months after the corresponding points in the current cycle. While the existence of only two semi-mature cycles is insufficient evidence, this timing synchronization, combined with the wave of on-chain profit-taking over the past two years and the current high level of speculation in the derivatives market, is worthy of attention. Further supporting evidence: The duration of Bitcoin's circulating supply above the +1 standard deviation range in the current cycle has extended to 273 days, making it the second-longest cycle on record, second only to the 335 days in the 2015-2018 cycle. This suggests that the duration of the current cycle is comparable to historical cycles, measured from the perspective of "the vast majority of supply is in a profitable state." The cumulative profits (in BTC) realized by long-term holders (LTH) from the pre-cycle high to the final peak have surpassed all previous cycles except 2016-2017. This phenomenon is consistent with the aforementioned indicators and, from the perspective of selling pressure, further confirms that the current cycle has entered its late historical stage. However, each cycle is unique, and market behavior does not necessarily follow a fixed time pattern. These dynamics raise a key question: Is the traditional four-year cycle still valid? Are we witnessing this evolution? The coming months will reveal the answer. Conclusion: Bitcoin inflows are showing signs of weakness, with demand weakening even after the price hit a record high of $124,400. This slowdown in momentum coincided with a surge in speculative positions: Open interest in major altcoins briefly hit a record high of $60 billion before falling back by $2.5 billion.

Ethereum, as the bellwether of the "alt season," once again leads this round of rotation:

its open interest reached its fourth highest level on record, and the share of perpetual swap volume soared to a record high of 67%, marking the most dramatic structural shift to date.

From a cyclical perspective, Bitcoin's price trend also echoes historical patterns:

In both the 2015-2018 and 2018-2022 cycles, the previous highs occurred 2-3 months after the current point in the cycle low.

The scale of profit-taking by long-term holders is comparable to historical frenzy phases, reinforcing the market's late-cycle characteristics.

In summary, signals such as high leverage, profit-taking, and intense speculation are consistent with the characteristics of a historically mature market. However, each cycle is unique, and Bitcoin and the broader market do not necessarily follow a fixed timeline.

Explore the “Kimchi Premium,” regional trading activity, and crypto market seasonality.

JinseFinanceMoney never sleeps, new stories are on the way, and I hope you can win this time.

JinseFinanceBEFE challenges SHIB in meme coin space with explosive growth potential, Solana blockchain advantage, and active community support. Investors should consider BEFE's innovation and growth prospects against SHIB's tokenomics challenges and slower growth.

Xu Lin

Xu LinShiba Inu faces a 12% overnight plunge, prompting investors to shift towards Binance Coin and Everlodge amid mysterious market dynamics. While Shiba Inu struggles, Binance Coin surges past $300, and Everlodge's disruptive DeFi approach to holiday property ownership gains traction with potential high returns.

Joy

JoyCoinbase is attempting to change the narrative around cryptocurrencies as part of an upcoming television advertisement campaign.

Others

OthersMetaverse is still very much important as the days of the internet are taking a new shape with the migration of different projects into Web3.

Nulltx

NulltxThe creation of Bitcoin paved the way for a new age of finance and a surge of new cryptocurrency projects ...

Bitcoinist

BitcoinistINTERNET CITY, DUBAI, Jul. 20, 2022 – LBank Exchange, a global digital asset trading platform, has listed CRYPTOKKI COIN (TOKKI) ...

BitcoinistINTERNET CITY, DUBAI, Jul. 20, 2022 – LBank Exchange, a global digital asset trading platform, has listed Crazy Internet Coin ...

BitcoinistNulltx