Coin swap/coin duality: a huge turbine revolution

Token swap is by no means just a new way to solve the liquidity problem of NFT.

JinseFinance

JinseFinance

This article aims to outline Hyperliquid's current situation and challenges facing competition, analyzing liquidity dynamics, giants' strategies, and market principles. It also explores how Hyperliquid maintains its leadership and resilience amidst volatility and uncertainty. It serves as a reminder to investors that market success is never permanent; only by understanding probabilities and returning to fundamentals can one discern opportunities amidst turbulence.

Hyperliquid faces fierce competition from a new generation of perpetual contract DEXs—Aster, Lighter, EdgeX, and others.

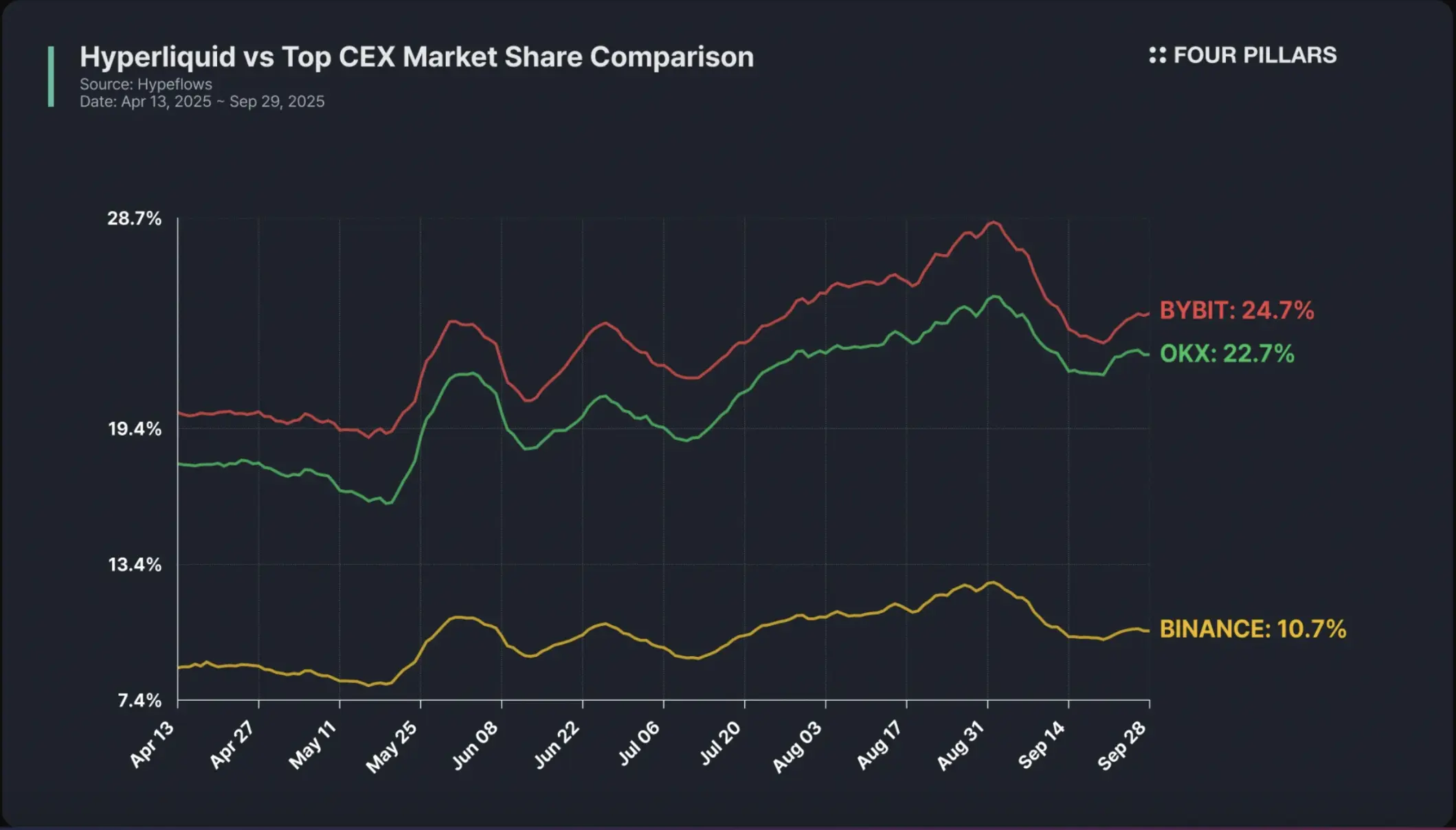

Liquidity is heavily dependent on incentives, and short-term funds and trading volume are rapidly flowing to new platforms. However, Hyperliquiquit maintains its lead in open interest and active users. The perpetual DEX market is likely to consolidate, ultimately leaving a few winners. Hyperliquid, with its infrastructure, ecosystem, and HyperEVM, is poised to maintain its core position. Success in the market isn't permanent. Whenever a company demonstrates an attractive business model, competitors flock in—either by imitating it, attracting users with more lucrative incentives, or introducing their own innovations. This pattern recurs across industries: no advantage can remain unchallenged for long. This principle is as old as capitalism, and now it's playing out in the emerging field of perpetual DEXs. Hyperliquid is under siege. After successfully demonstrating the secure and efficient operation of its proprietary blockchain-based CLOB model (centralized order book), it quickly attracted users and liquidity, becoming a recognized industry leader. However, recent developments have reaffirmed that leadership inevitably invites challengers. A wave of new perpetual DEX projects (such as Aster, Lighter, EdgeX, Pacifica, and Avantis) have emerged, each employing a nearly identical core strategy: point-based mining, aggressive airdrop promises, and attractively high incentives. 1. Competition Arrives On a single day in late September, Aster and Lighter reached $42.8 billion and $5.7 billion in daily trading volume, respectively, surpassing Hyperliquid's approximately $4.6 billion. Other newcomers, such as EdgeX, followed closely behind, with a turnover of $3.3 billion. To outside observers, this seemed to dethrone Hyperliquid. Just a few months ago, it controlled over 70% of the on-chain perpetual swap market, but now its ranking has fallen to second or even third place. But context is important. In that same month alone, Hyperliquid's trading volume approached $300 billion, a scale that no new entrant has been able to consistently reach. In terms of active users and open interest (a better indicator of capital investment than daily trading volume), Hyperliquid remains far ahead. 2. The Nature of Liquidity Liquidity is inherently transferable. Traders seek not only optimal execution efficiency but also optimal incentive returns. In the crypto market, token incentives often far exceed transaction fees, leading to a mercenary nature for capital—flowing to the current most profitable venues. However, this doesn't mean all liquidity is created equal. Some liquidity is opportunistic, entering for yield and quickly departing; other liquidity is more "sticky," driven by trust in a platform's infrastructure, reputation, and long-term value. For Hyperliquid, the key question is: how much of its liquidity is mercenary and how much is durable? Conventional wisdom holds that once incentives diminish, "farmers" will exit the market, and established platforms will eventually reclaim their share. However, this also raises a new question: what if "nomadic liquidity"—constantly circulating between pre-coin offering platforms—becomes the new market norm? In such an environment, platforms that have already launched tokens may face a paradox—their original advantages may become a burden. 3. The Role of Giants Hyperliquid faces challenges not only from emerging competitors but also from strategic rivals with deep resources—the most representative of which are Binance and its founder, CZ. Binance is well known for its aggressive competitive style. Many believe that its strategy contributed to the collapse of FTX. Today, Hyperliquid's trading volume has consistently reached over 10% of Binance's, and it's natural for CZ to take note. His first move was to launch the $JELLYJELLY perpetual contract at the height of the situation—a move the market viewed as an attempt to exacerbate volatility and put pressure on Hyperliquid's liquidity pool (HLP) by increasing margin requirements and liquidation risk. Subsequently, CZ further supported Aster, the BNB Chain decentralized exchange in which he had invested. However, Aster's success may have been a secondary objective. A more plausible speculation is that CZ's true intention was to disrupt Hyperliquid's growth momentum and force market capital and attention to be dispersed among multiple competitors. Even if Aster couldn't reach Hyperliquid's scale, as long as it could serve as a distraction, the strategic goal would have been achieved. From Binance's perspective, this strategy was perfectly rational: a decentralized competitive landscape prevented any one on-chain competitor from accumulating too much power. "Divide and conquer" has always been a classic tactic in commercial warfare.

The Bene Gesserit order’s precept is: “I must not fear. Fear is the soul-killer. Fear is the little death that brings utter destruction.”

The market often confirms this wisdom—the damage caused by fear is often deeper than the fundamentals. Today, Hyperliquid's greatest risk may not be a specific competitor, but rather a growing perception that loyalty no longer pays off. If traders begin to believe they must constantly chase the next airdrop, Hyperliquid's long-term community cohesion will be weakened. In this situation, the real enemy isn't competitors, but FOMO (fear of missing out). For investors, it's more important than ever to distinguish short-term disruptions from long-term erosion. The wise approach isn't to deny fear, but to acknowledge it, let it flow, and then return to fundamentals. 5. Emerging Markets That said, it's worth remembering that this market is still young. Today's perpetual swap decentralized exchanges (Perp DEXs) are likely similar to the centralized exchanges (CEXs) of late 2010 to early 2020, when Binance, Huobi, Gate.io, BitMEX, Bybit, and OKX were still vying for market dominance. Over time, we're likely to see a similar consolidation among decentralized exchanges, with a handful emerging as giants. The current incentive wars aren't the end of the industry, but rather part of its growing pains. DEXs are entering a period of competition all their own. 6. Probability, Not Certainty The battle for liquidity is far from over. Hyperliquid faces stiff competition from opportunistic rivals and entrenched giants. However, several factors suggest the odds remain in its favor: Superior Infrastructure and Development Ecosystem: Hyperliquid is a complete Layer 1 chain with a leading CLOB engine and a strong developer community built on the HyperEVM. This foundation is difficult for competitors operating solely as standalone DEXs to replicate. Trendsetting Initiatives: From HIP-3 to its native stablecoin, Hyperliquid has consistently set the pace for the industry. The USDH token auction was one of the most hotly contested events in crypto, attracting all major players, and the local market ultimately prevailed. 50% of USDH revenue is allocated for buybacks and AF, making Hyperliquid unique in the L1 ecosystem, allowing it to both earn stablecoin returns and collect protocol fees on multiple frontends via HIP-3. Stickier liquidity: Despite daily trading volume fluctuations, Hyperliquid maintains a dominant position in open interest and active users, demonstrating the continued engagement of a loyal core group of traders. Season 3 Points Program (speculative): Updates to the points page indicate the upcoming launch of a new Season 3 program. Incentive allocation has always been a strength of Hyperliquid, with 38.8% of the $HYPE token supply reserved for community rewards, currently valued at approximately $5.8 billion. No competitor can match this incentive pool. HyperEVM TGE: Upcoming HyperEVM tokens (such as UNIT, Kinetiq, and Felix) will inject liquidity back into the ecosystem and deepen the role of $HYPE. This evolution from a pure DEX to a broader L1 platform could present a significant revaluation opportunity. As with all investing, we discuss probabilities, not certainties. Our hope for Hyperliquid is that after today's turmoil subsides, it will emerge stronger and wiser as a market leader. As emphasized in the original article: success in the market is not sustainable. Even industry leaders like Hyperliquid face challenges from innovative competitors. Investors need to understand that any platform is susceptible to disruption. The key is to assess the probability and timing; and to prioritize fundamentals such as technical strength, user engagement, and profitability, which are more important than short-term trading volume. This competition among perpetual contract trading platforms essentially reflects the entire cryptocurrency industry's shift from "unbridled growth" to "refined operations." While Hyperliquid faces challenges, its technological expertise and user base remain significant advantages. For investors, the key lies in understanding competitive dynamics and identifying opportunities amidst change, rather than relying on single judgments. Ultimately, as has been the case throughout the internet industry, only platforms that truly create value for users and have sustainable business models will stand out in this fierce competition.

Token swap is by no means just a new way to solve the liquidity problem of NFT.

JinseFinanceOvernight, $21 million was taken from multi-chain DEX Transit Swap.

Others

OthersINTERNET CITY, DUBAI, Jul. 20, 2022 – LBank Exchange, a global digital asset trading platform, has listed CRYPTOKKI COIN (TOKKI) ...

Bitcoinist

BitcoinistINTERNET CITY, DUBAI, Jul. 25, 2022 – LBank Exchange, a global digital asset trading platform, has listed Energy Empire (E2COIN) ...

BitcoinistINTERNET CITY, DUBAI, Jul. 20, 2022 – LBank Exchange, a global digital asset trading platform, has listed Crazy Internet Coin ...

BitcoinistINTERNET CITY, DUBAI, Jul. 5, 2022 – LBank Exchange, a global digital asset trading platform, has listed Pollux Coin (POX) ...

BitcoinistINTERNET CITY, DUBAI, Jun. 28, 2022 – LBank Exchange, a global digital asset trading platform, has listed Bible Coin (BIBL) ...

BitcoinistINTERNET CITY, DUBAI, Jun. 22, 2022 – LBank Exchange, a global digital asset trading platform, has listed Galaxy Block Coin ...

BitcoinistINTERNET CITY, DUBAI, Jun. 15, 2022 – LBank Exchange, a global digital asset trading platform, has listed Gulf Coin (GULF) ...

BitcoinistINTERNET CITY, DUBAI, May. 13, 2022 – LBank Exchange, a global digital asset trading platform, will list Elia Coin (ELC) ...

Bitcoinist