Translated by: Liu Jiaolian

The overnight crypto market was under pressure as Mt.Gox distribution continued to advance. Affected by this, the market was unable to attack. BTC temporarily retreated to 66k on standby. Today, Jiaolian will talk to you about the track of the new public chain.

As early as the end of last year, in response to Messari's research report that was bearish on ETH and bullish on SOL, Jiaolian pointed out that this was one of the self-rescue actions of Wall Street capital after FTX was buried in 2022. Why? Because these institutions were fooled into a trap by SBF (founder of FTX), who had white skin and naturally attracted their trust, and heavily invested in Solana. As a result, FTX (the exchange founded by SBF) was taken away by CZ (Changpeng Zhao of Binance) during the 2022 bear market, which directly led to the loss of many assets of the "FTX system"!

Take Solana, one of the many trapped assets, from its peak of nearly $260 in October 2021, it went straight to less than $8 in December 2022! The maximum decline was as high as 97%!

This made the American institutional capital that was trapped intolerable. They immediately came up with two countermeasures:

First, launch retaliatory actions. Using the system of American capital influencing politics, promote the joint law enforcement of the Ministry of Justice, CFTC, and the Ministry of Finance, "invite" CZ to the United States, fine and sentence him. CZ was forced to leave Binance, which he founded. Binance is regulated by the US Treasury Department. This happened in November last year (2023). The revenge was taken in less than a year, which deeply reflects the "advancedness" of the capitalist system - once the boss (capital) speaks, the employees (US government) are really good at execution! This section of the rivers and lakes grudges will not be mentioned for the time being.

Second, launch a self-help action. How to save yourself? Of course, it is to jointly sit in the bank, concoct good news, and raise the price of the currency. The strategy concocted by Wall Street capital is to crown Solana with the crown of the king of public chains on Ethereum. By March this year (2024), taking advantage of that wave of copycats, SOL has successfully soared to $210, compared with less than $8 in December 2022, an increase of 25 times. During the same period, ETH only rose from $1070 at the end of 2022 to $4090 in March 2024, an increase of only about 4 times.

You may wish to recall why few people on the Internet suddenly talk about Solana not being a decentralized blockchain at all, because it needs a centralized sequencer at its core to work? Why did Rune Christensen, the founder of Maker, challenge Vitalik Buterin, the founder of Ethereum, last year, saying that Solana is better than Ethereum? Why did the head crypto investment research institution Messari openly sing the bad news about Ethereum (ETH) and sing the good news about SOL in its research report last year? Why is the saying "Solana flips ETH" becoming popular on platforms such as Twitter?

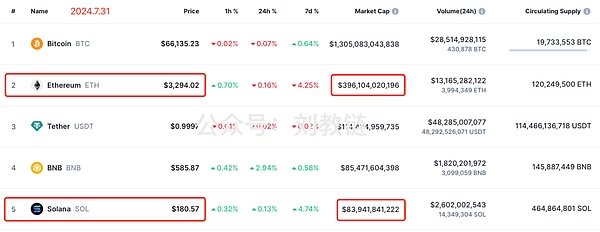

Today, on the last day of July 2024, Solana has ranked among the top 5 crypto market capitalizations, with a market capitalization of nearly $84 billion. Ethereum's market capitalization is over $396 billion. Although there is still an order of magnitude gap in size, there are already many people and many voices in the market who are encouraging the ignorant leeks to believe in stories like "Solana is the next Ethereum" and "Solana will definitely surpass Ethereum."

Remember, in the financial market, what you see is often what others want you to see. The falsity of the appearance is often proportional to the loudness of the optimistic voice. Does Solana really have the potential to surpass Ethereum, and is it possible to become the next king of the public chain? Or on the contrary, is Solana's prosperity an artificial illusion, is it the emperor's new clothes?

Below, I compiled Flip Research's research report "SOL - The Emperor's New Clothes" and shared it with you for inspiration.

Recently, my Twitter timeline has been filled with SOL bullish posts, interspersed with memecoin scams. I began to believe that the memecoin super cycle is real and that Solana will surpass Ethereum and become the main L1 (layer chain). But then I started digging into the data, and the results were worrying to say the least... In this post, I present my findings and why Solana may be a "house of cards" (referring to the game of capital and power).

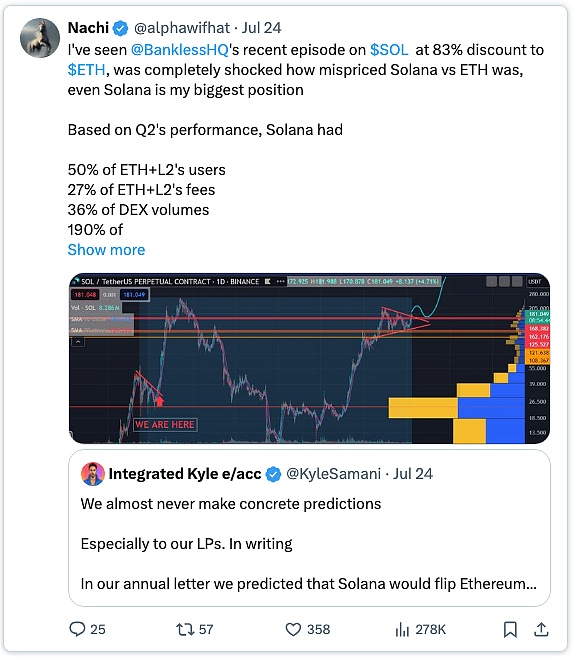

First, let’s look at the concise and succinct view of netizen Nachi on SOL:

【Note from the Teaching Chain: Netizen Nachi’s comments on SOL are mainly as follows:

I saw @BanklessHQ’s recent report on $SOL being 83% off $ETH, and was completely shocked by the pricing mismatch between Solana and ETH. Even Solana is my largest position.

Based on Q2 performance, Solana has

50% of ETH+L2 users

27% of ETH+L2 fees

36% of DEX trading volume

Accounting for 190% of ETH+L2 stablecoin trading volume.

Today, SOL’s DEX trading volume exceeds ETH’s trading volume. Even taking ETH+L2 into account, it has gone from 36% to 57% in just a few weeks.

SOL’s DEX volume will sooner or later flip ETH+L2s and memecoins, which are the best PMFs in this cycle, among other indicators.

However, SOL’s market cap is still only 20% of ETH’s, and it’s still growing rapidly, which is completely idiotic in traditional valuations, coupled with catalysts like Firedancer and possible ETF approval early next year…】

There are four different dimensions for comparing ETH+L2 indicators: 1. High proportion of user base

2. Proportionately higher fees

3. Large DEX trading volume

4. The proportion of stablecoin trading volume is significantly higher

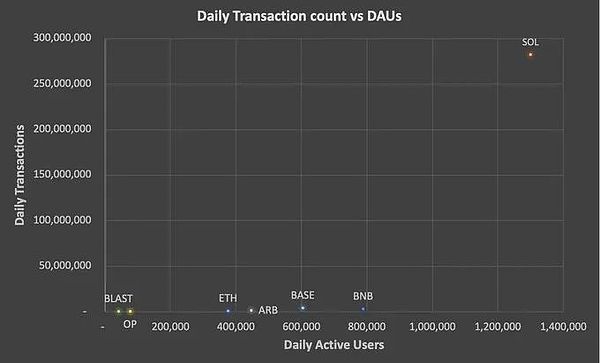

1. User base comparison:

The following is a comparison between the ETH mainnet and SOL (only the mainnet is compared, because the vast majority of fees come from the mainnet after Dencun, source: @tokenterminal):

ETH user base + on-chain transactions (tx)

SOL user base + on-chain transactions (tx)

On the surface, SOL's data is good, with more than 1.3 million daily active users (DAU) compared to 376,300 for ETH. However, when we add tx counts to the mix, I find something strange.

For example, on Friday, July 26, ETH had 1.1 million transactions and a DAU of 376,300, about 2.92 transactions per user per day. SOL, on the other hand, has 282.2M transactions and 1.3M DAU, which is a whopping 217 transactions per user per day.

I thought this could be due to the low fees allowing more transactions, more frequent compounding of positions, more arbitrage bot activity, etc. So I compared it to another popular chain, Arbitrum. However, Arb only had 4.46 user visits on the same day. Looking at other chains, the results are similar:

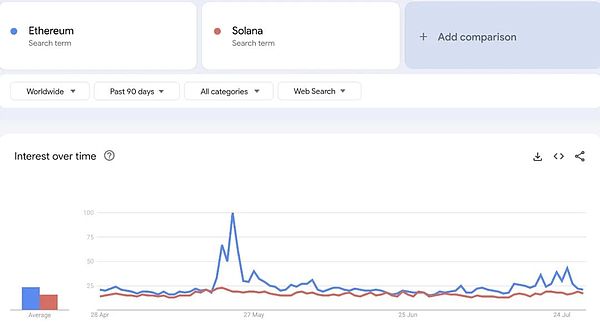

Given the higher user count than ETH, I checked against Google Trends, which should be fairly irrelevant to the per-user value:

ETH has been on par or ahead of SOL. Given the difference in DAU, plus all the hype around the SOL meme coin trend, this is not what I expected. What is going on?

Subtitle in the picture: The secret to getting rich is written in the Criminal Law.

2. DEX transaction volume analysis

To understand the difference in transaction volume, it will be inspiring to look at Raydium's LPs. Even at first glance, it’s clear something’s not right:

At first, I thought it was just low-liquidity wash trading on honeypot LPs to attract the odd memecoin degen, but looking at the charts, it’s much worse:

Each of these low-liquidity pools is a project that has pulled a rug in the last 24 hours alone. In the case of MBGA, there were 46,000 trades on Raydium in the last 24 hours, $10.8 million in volume, buys/sells from 2,845 different wallets, and over $28,000 in fees. (Note that $MEW, a similarly sized legitimate LP, only generated 11,200 trades).

Looking at the wallets involved, the vast majority appear to be bots in the same network, with tens of thousands of transactions. They independently generate fake volume, randomly generating SOL amounts and transaction times until a project has problems, then moving on to the next project.

In the past 24 hours, there were over 50 projects with >$2.5M in volume on Raydium’s standard LP, generating a total of over $200M in volume and over $500K in fees. Volume on Orca and Meteora appears to be much lower, and I’m having a hard time finding any meaningful volume on Uniswap (ETH) for these runaway projects.

It’s clear that there are huge issues with project runaways on Solana, with a variety of repercussions:

Given the abnormally high transaction-to-user ratio, and the number of wash trades/wash on-chain, it seems like the vast majority of transactions are unnatural. On the main Ethereum L2, the highest daily transaction-to-user ratio is 15.0x that on Blast (which also has low fees and users are all on Blast S2). As a rough comparison, if we assume the true SOL transaction-to-user ratio is similar to Blast, this would mean that over 93% of transactions (and by extension, fees) on Solana are unnatural.

The only reason these scams are running is because they are profitable. Therefore, the amount of money users are losing must be at least equal to the fees + transaction costs incurred, which is millions of dollars per day.

Once deploying these scams becomes unprofitable (i.e. actual users get tired of losing money), you'll see that most trading volume and fee revenue declines.

From this it seems that users, true fees, and DEX trading volume are all grossly inflated.

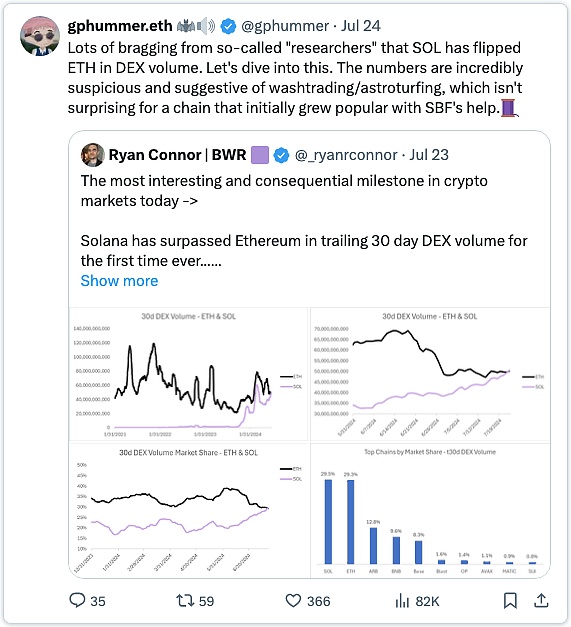

I’m not the only one to come to these conclusions, @gphummer recently posted something similar:

【Jiaolian Note: Netizen ghpummer said: Many so-called "researchers" are boasting that SOL has surpassed ETH in DEX trading volume. Let’s take a deeper look. These numbers are incredibly suspicious and suggest wash trading/marketing deception, which is not surprising for a chain that initially became popular with the help of SBF. 】

3. MEV on Solana

MEV (miner extracted value) on Solana is in a unique position. Unlike Ethereum, it does not have a built-in memory pool; instead, players like @jitoo_sol created (now abandoned) extra-protocol infrastructure to simulate memory pool functionality, thus providing opportunities for MEV, such as front-running, sandwich attacks, etc. Helius Labs has a detailed introduction to MEV here: https://www.helius.dev/blog/solana-mev-an-introduction The problem with Solana is that the vast majority of tokens traded are ultra-volatile, low-liquidity meme coins, and traders often have to set slippages greater than 10% to successfully execute trades. This provides a lucrative attack surface for MEV to capture value:

【Note from Teaching Chain: What netizen Ben said is: In the past 1-2 months, the infamous sandwich robot arsc on Solana has earned more than 30 million US dollars?! 】

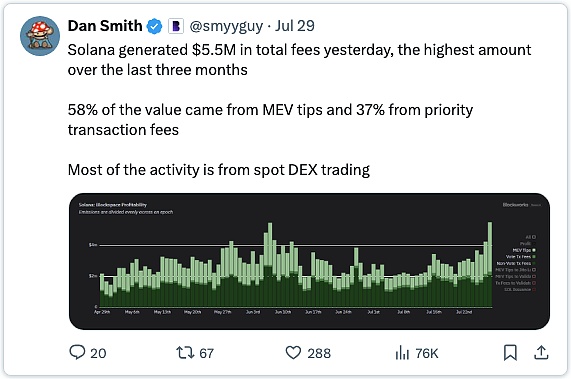

If we look at the profitability of the block space, we can see that most of the value now comes from MEV oil and water:

【Jiaolian Note: Netizen Dan Smith said: Solana generated a total of $5.5 million in fees yesterday, the highest in the past three months. 58% of the value came from MEV prompts, 37% from priority transaction fees, and most of the activity came from spot DEX transactions】

While this is strictly "real" value, MEV will only be carried out when it is profitable, that is, as long as retail investors continue to "all-in" memecoins (and make a net loss), MEV will be carried out. Once memecoins start to cool, MEV fee income will also collapse.

I see many SOL posts talking about how they will eventually turn to infrastructure investments such as $JUP, $JTO, etc. This is very likely, but it is worth noting that these tokens, with their lower volatility and higher liquidity, simply do not offer the same MEV opportunities.

Sophisticated players are motivated to build the best infrastructure to take advantage of this situation. During my investigation, some sources mentioned rumors that these players invested in controlling memory pool space and then sold the rights to third parties. But I was unable to confirm this information.

There are some clearly perverse incentive mechanisms here - by moving as much memecoin activity as possible to SOL, it allows sophisticated players to continue to profit from MEV, the memecoin insider trading mentioned above, and the price appreciation of SOL.

Fourth, stablecoins

Speaking of stablecoin transaction volume + TVL (total locked amount), there is another strange phenomenon. The transaction volume is significantly higher than ETH, but when we look at @DefiLlama's stablecoin data, ETH has $80 billion in stable TVL, while SOL only has $3.2 billion.

I think stablecoin (and more broadly) TVL is a less scalable metric than volume/fees on low-fee platforms, and it shows how many players are in the game.

The volume dynamics of stablecoins highlight this - @WazzCrypto points out that once the CFTC announced they were investigating Jump, volume suddenly dropped:

【Note from the Teaching Chain: What netizen Wazz said is: Since Jump was investigated by the US Commodity Futures Trading Commission (CFTC), the chart of Solana stablecoin trading volume has become a literal horizontal line. It's a big mystery what caused this...】

V. Leek Value Extraction

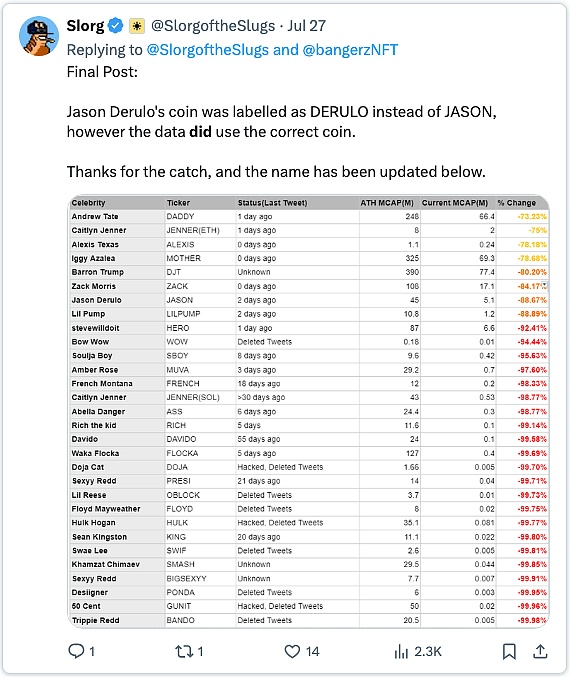

Apart from running away and MEV, the outlook for retail investors remains bleak. Celebrities chose Solana as their preferred chain, and the results are not optimistic:

【Teaching Chain Note: This table shows the amazing decline of "celebrity coins" issued on Solana】

Andrew Tate's "DADDY" is the best performing celebrity coin with a return of -73%.

A quick search on Twitter reveals evidence of rampant insider trading and developers dumping tokens on buyers:

Some people may ask: But my Twitter timeline is full of people who made millions trading meme coins on Solana. What does this have to do with what you are saying?

I simply don't believe that posts by KOLs on Twitter are representative of the broader user base. It’s easy for them to fall into a niche in the current frenzy, promote their token, profit from their followers, and repeat over and over again. There’s definitely survivorship bias at work here — the winners are far louder than the losers, creating a distorted perception of reality.

Objectively speaking, retail investors are being ripped off by scammers, developers, insiders, MEVs, KOLs every day, and that’s not even taking into account that most of what they’re trading on Solana is memecoins that aren’t backed by anything real. It’s hard to argue with the fact that most memecoins will eventually go the same way as $boden (ie: to zero).

VI. Additional Considerations

Markets are fickle, and when sentiment changes, factors that were once blind to buyers come into focus:

Poor chain stability and frequent outages

High transaction failure rate

Unreadable block explorer

High development barrier, Rust is far less user-friendly than Solidity

Poor interoperability compared to EVM. I believe it is healthier to have multiple interoperable chains competing with each other rather than being constrained by a single (fairly centralized) chain.

The likelihood of an ETF is low from both a regulatory and demand perspective. This post itself highlights why institutional demand will be low in Solana’s current state. @malekanoms also highlighted some points that I think are relevant to traditional finance (plus @0xmert's rebuttal):

【Note from the Teaching Chain: What netizen Omid Malekan said is: ETH is a high-quality liquid asset (HQLA) in cryptocurrencies

In anticipation of the launch of the ETH ETF, I wrote a small paper explaining what HQLA is, why we need a digital native HQLA, and why ETH is the most likely candidate asset. My analysis compares it to BTC and SOL.

Here is the summary:

Why HQLA?

HQLA is a concept from traditional finance, used in banking supervision. It refers to assets that have almost universally recognized value and deep liquidity - assets that banks can safely hold and sell in a pinch without affecting the market. I apply this concept loosely to cryptocurrencies, because this asset is what we can use to build a whole new decentralized financial system.

Native digital HQLA means better decentralized stablecoins, safer credit, and more trusted derivatives. My analysis explains why this can't be a dApp token, a centrally issued stablecoin/RWA, or an L2 token. The best candidate is the native coin of L1.

Why not Bitcoin?

BTC is the most valuable and liquid asset in crypto, but you can't do a lot with it. There are no native DeFi or alternative assets on the chain, such as stablecoins. The only way to use it as collateral is to custody it or bridge it to another chain, both of which introduce new risks and somewhat defeat the purpose.

Perhaps with the introduction of new contracts or L2s, this will change, but I doubt it. The soul of BTC lies in fulfilling another purpose, which is to be the HQLA of traditional finance.

ETH vs. SOL

The Solana network has many attractive features. But it is not the same thing as SOL (the asset). From an economic perspective, SOL has weak fundamentals and is therefore a medium-quality asset.

First, SOL ownership is concentrated, thanks to its youth, multiple rounds of venture capital, grants to labs and foundations, and the fact that it is launched on a staking basis (i.e. PoS). Concentration reduces liquidity. ETH had a modest funding round a few years ago, only gave the foundation and founders a small amount of money (by current standards), and had many years of PoW (proof of work, i.e. computing power mining) before the merger.

Second, SOL has a relatively high inflation rate of over 5%. The inflation rate will eventually decrease, but the supply will grow by 25% before the inflation rate stabilizes at 1.5%. In the meantime, SOL will have a high cost of capital in DeFi.

DeFi will always favor native assets — LST (liquidity staking tokens) carry their own risks — but using native SOL in DeFi means giving up high staking yields. For DeFi to attract capital, it must compete with staking.

This means that SOL’s nominal interest rate is high. ETH, on the other hand, is close to deflation, with a nominal interest rate close to zero. You can already see this in action: it currently costs almost three times as much to borrow SOL on Kamino as it does to borrow ETH on AAVE.

Third, high nominal interest rates lead to more staking. To avoid dilution, SOL owners would be silly not to stake, but this would hinder liquidity. Solana’s staking participation rate is more than double that of Ethereum. Ethereum holders don’t miss out on much by not staking. This means there is always more ETH floating freely in the market than SOL.

To make matters worse, Solana’s LST ecosystem is fragmented. Liquid staking tokens are not as sexy as HQLAs, but people do use them, and there is a large amount of Lido stETH in Ethereum DeFi. Concentration in a single LST may be bad for the security of the chain, but it is good for DeFi. This means more liquidity for assets that may be considered "too big to fail".

Fourth, perhaps counterintuitively, Solana has low transaction fees. This may be good for users, but it is bad for SOL fundamentals - fees are a cost to users, but they are also income for stakers. Low fees mean that most of the returns paid to stakers must come from new coin issuance, which is depreciation.

The interaction between issuance and fees determines the effective interest rate of a crypto asset (MEV also plays a role, but is not included in my analysis).

ETH has low issuance and high fees, and almost all of the fees go to stakers. This means that its effective yield is positive. In this regard, it is even better than Bitcoin. Bitcoin also has very low issuance and high fees, but both go to miners, not holders.

SOL has an almost negative real yield. Except during peak activity, almost all of the yield comes from increasing the money supply.

ETH also has a burn mechanism. This increases its positive real yield while also returning value to non-stakers, which reduces the incentive to stake, reduces staking participation, and leads to more liquidity. Solana used to have a burn mechanism, but later decided to remove it.

Finally, Ethereum's high fees mean that ETH has a higher convenience yield: users will want to always hold some ETH (without staking) to pay for future on-chain gas fees, thereby increasing the available supply of ETH.

ETH has better monetary properties than SOL, and monetary properties are very important to being HQLA.

This is a complex argument with many moving parts, but SOL's lack of importance in Solana's success hinders its qualification as the ultimate asset built on it.

You can even see this in Solana culture. Even @aeyakovenko thinks that security in the crypto economy is just a meme. But if that’s true, then the foundation of the chain’s token is a meme, too.

The circular logic of security->coin->security is the ultimate source of value for any cryptocurrency. This was Satoshi’s greatest insight.

This doesn’t mean that SOL can’t appreciate, or even outperform ETH, because memes and momentum are more important than fundamentals in crypto right now.

But these dynamics reduce the importance of SOL in a financial system that is being rebuilt on the basis of entirely new assets.

ETH is the HQLA of crypto

As the market slowly realizes this, it may grow at a disproportionate rate as a DeFi coin to SOL, and could potentially surpass Bitcoin in value and status one day. The winner-take-all bias in finance is very strong.

This analysis is at the forefront of thought, so all comments, questions, and rebuttals are welcome. Here is the full analysis:

https://omid-malekan.medium.com/eth-is-the-high-quality-liquid-asset-of-crypto-4d27ee77c127 】

Up to 67,000 SOL/day ($12.4 million)

FTX Legacy still has 41 million SOL ($7.6 billion) locked in it. 7.5 million SOL ($1.4 billion) will be unlocked in March 2025, and an additional 60,900 SOL ($113 million) will be unlocked each month until 2028. Most tokens appear to have been purchased at around $64 per token.

VII. Conclusion

As usual, pickaxe and shovel sellers have profited from the Solana memecoin boom, while speculators have been robbed, often unwittingly.

I believe that the commonly quoted metrics for SOL are grossly overstated. Furthermore, the vast majority of organic user funds on-chain are rapidly draining. We are currently in a mania phase, and retail inflows still outweigh the outflows of these sophisticated players, creating a positive perception. Once users become fatigued by the continued losses, many metrics will quickly collapse.

As mentioned above, SOL also faces some fundamental headwinds that will become prominent once sentiment turns. Any price increase will exacerbate inflationary pressures/unlocks.

Ultimately, I believe that SOL is overvalued from a fundamental perspective, and while existing sentiment and momentum will likely drive prices higher in the short term, the long-term picture is more uncertain.

JinseFinance

JinseFinance