Tether Amplifies Digital Currency Space with New USDT Token Influx

Tether generates 1 billion USDT, strategically enhancing liquidity and market readiness.

Brian

Brian

We have to say that Tether CEO Paolo Ardoino is very humble as the king of the stablecoin world, but he has ambitious plans for Tether's continued development and dominance. In this new digital era, we have just witnessed the landmark stablecoin bill in the United States just passed the Senate. In the coming months, it will be sent to Trump's desk and signed.

Amid the Circle IPO boom, we have been thinking about where the next stage of the stablecoin battlefield is?

Especially the definition of "payment stablecoin" in the Genius Stablecoin Act will pull the battlefield from the crypto market to the real world payment settlement scenario.

Bankless launched an interview program with Tether CEO Paolo Ardoino in a timely manner, revealing to us the understanding of the king of stablecoins Tether USDT, which is of great reference value. Here are the facts that we are covered by the Circle IPO boom, and the national will to expand the dollar on the chain. Paolo's analysis of the stablecoin business model, the target market promotion strategy, and Tether's investment logic are blind spots that are not covered by the current popular science research reports on stablecoins, and are also what we Web3 payment practitioners need to really care about.

Stablecoins have completely different application scenarios in the United States and other parts of the world, and the current stablecoin business model in the US market seems to be difficult to work.

The United States is one of the markets with the highest efficiency of capital flow in the world, and the efficiency of its financial channels can reach 90%. The introduction of stablecoins can perhaps increase efficiency from 90% to 95%, and the premium space is very limited. In contrast, in other parts of the world, the introduction of stablecoins can provide 30%-40% financial efficiency. Therefore, for these countries, stablecoins are more significant.

For example, there are still 3 billion people in the world who do not have bank accounts, and Tether currently covers 450 million users. The opportunities here are huge and there is still a lot to do. Therefore, Paolo emphasized that it is crucial to distinguish between these two different products and application scenarios.

Go deep into Asia, Africa and Latin America, invest in infrastructure, this innovative distribution channel and deep penetration into emerging markets are the key to Tether's leading position in the stablecoin field. Tether is not only technologically advanced, but also has established an unprecedented US dollar distribution network worldwide, which is one of Tether's least known advantages.

Less than 40% of Tether's market value is related to the cryptocurrency market. In other words, more than 60% of the market value growth actually comes from the grassroots use of USDT in emerging markets. The next driving force for the growth of USDT's market value may come from the trade of commodities.

Users are not interested in the blockchain itself. They only care about one thing - the fee should be low, almost zero.

User: I understand Bitcoin, but I still prefer to use USDT.

The U.S. Senate has just passed the Genius Stablecoin Act, and U.S. President Trump couldn’t wait to tweet: "Hurry up and send the bill to our table, ASAP, we will win comprehensive advantages in the digital asset market!"

1.1 Stablecoin Act for Tether

The bill is undoubtedly a great boon to the onshore stablecoin issuer Circle, but the offshore stablecoin issuer Tether How do you view the Genius Act?

Paolo said that Tether, as a pioneer in the stablecoin industry, has been committed to promoting the development of this field since its birth in 2014. This concept was almost ignored in the first ten years. This process is not easy. We are building a brand new industry from scratch, which will naturally cause friction with the traditional financial system and encounter many obstacles, especially from the banking system. But our team has never backed down and has always believed in providing dollars to people who are excluded from mainstream finance.

For Paolo personally, this is also the first time to really set foot in the United States-the first time at the age of 40. In the past few years, regulatory actions like "Chokepoint 2.0" have been very unfavorable to Tether, but in recent exchanges on Capitol Hill and administrative agencies, I can feel that attitudes are beginning to improve.

Today, the Tether team is honored and encouraged to see the most powerful countries and governments in the world begin to pay attention to and legislate to regulate stablecoin technology. The GENIUS Act is an important step in the right direction. Although the bill still needs to be passed by the House of Representatives, it currently seems to have good momentum. Tether and looks forward to seeing its final version so that it can continue to advance its possible stablecoin plans in the United States.

The Genius Act builds a strong framework for onshore stablecoins in the United States, as well as offshore stablecoins like USDT, enabling them to meet regulatory requirements through corresponding systems. Paolo believes that as an offshore stablecoin issuer, USDT is already in a good position in terms of compliance.

The GENIUS Act sets a high compliance threshold, which Paolo believes is very fair and commendable, especially in terms of anti-money laundering and compliance. Tether has been actively cooperating with law enforcement agencies around the world. At present, they have established cooperative relationships with more than 250 law enforcement agencies from more than 55 different countries, which is far more than other financial institutions. At the same time, Tether can effectively identify secondary market activities in the blockchain ecosystem through its own monitoring technology and notify law enforcement agencies in a timely manner.

Bankless previously communicated with Senator Bill Hagerty, a co-drafter of the GENIUS Act, and specifically asked questions about Tether. Senator Bill Hagerty said that if offshore issuers like Tether want to enter the US market, the bill allows the Treasury Department to conduct comparability testing. If the rules of the country where Tether is located are consistent with those of the United States, then Tether can continue to operate. Otherwise, Tether needs to set up a subsidiary in the United States, which must meet the same reserve and disclosure standards as other companies. Senator Bill Hagerty also mentioned that Tether can start complying with these regulations immediately.

Paolo believes that Senator Bill Hagerty is correct that the GENIUS Act provides a way for offshore issuers to achieve mutual benefits by establishing similar management systems. He pointed out that countries must establish corresponding systems, and the GENIUS Act will set an example for other countries. Once the United States passes the GENIUS Act, other countries will follow suit, which will pave the way for the development of the global stablecoin industry.

1.2 Tether's response

Bankless hopes to learn more from Paolo about Tether's plans after the passage of the GENIUS Act, as Tether currently seems to be facing multiple development directions, whether it is offshore/onshore operations or issuing new stablecoins onshore.

A. Strong profitability

In response, Paolo said that Tether is confident in meeting the requirements of the GENIUS Act, especially for USDT. He pointed out that Tether achieved a profit of $13.7 billion last year and is expected to exceed this figure this year. He stressed that even if Tether only holds $155 billion in assets, it can bring Tether about $7.5 billion in revenue at current interest rates. In addition, Tether is making other investments, including gold and Bitcoin, which are expected to further increase its returns.

B. Huge U.S. Treasury reserves

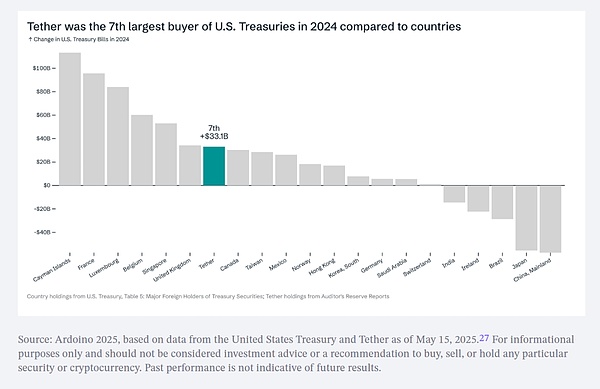

Paolo questioned those who believe that Tether cannot meet the requirements of the bill. He pointed out that Tether is not only profitable, but also outstanding in purchasing U.S. Treasury bonds. He revealed that Tether was the fifth largest buyer of U.S. Treasury bonds last year, and among all non-state entities, Tether was the 18th largest holder.

He believes that the power of stablecoins lies in their support for the U.S. economy, and the president is well aware of this.

( Stablecoins Could Become One Of The US Government’s Most Resilient Financial Allies)

Tether’s funds are deposited in the United States’ “Counterfeit Gerald”, which is the leading financial institution in the United States. Tether holds more than $120 billion in U.S. Treasury bonds in this institution, which shows that Tether does not hide its funds, but conducts transparent financial operations in the United States. Paolo emphasized that this way of depositing funds is consistent with the spirit of the GENIUS Act. Because these institutions have direct links with the Federal Reserve, Tether also conducts overnight reverse repurchase and repurchase operations. This means that even if faced with tens of billions of dollars in redemptions, Tether will be able to cope with it easily and meet these demands without any problems.

Paolo believes that the beauty of this fund storage and operation model is that it ensures that Tether can still operate stably when facing huge redemption pressure. He believes that this government and the GENIUS Act will help make the entire industry more solid and provide a clearer and safer operating environment for Tether and other stablecoin issuers.

In addition, he emphasized that the most powerful point of USDT compared to anything else is that USDT focuses on the overseas market of the United States, which means that after overseas users buy USDT, Tether uses these funds to buy US Treasuries, thereby diversifying the ownership of US debt and reducing the risk of single-point selling. He believes that it is more ideal for US Treasuries to be held by overseas people, otherwise it may lead to disastrous consequences.

C. Strong Balance Sheet

Tether is confident in the various compliance requirements set forth in the GENIUS Act because they believe they are able to do better than other institutions in this regard. Tether is well aware of the importance of having a strong balance sheet to avoid a recurrence of events similar to Terra-Luna. Tether currently holds more than $125 billion in Treasury bonds, and this number continues to grow, to ensure the stability of the value of the stablecoin.

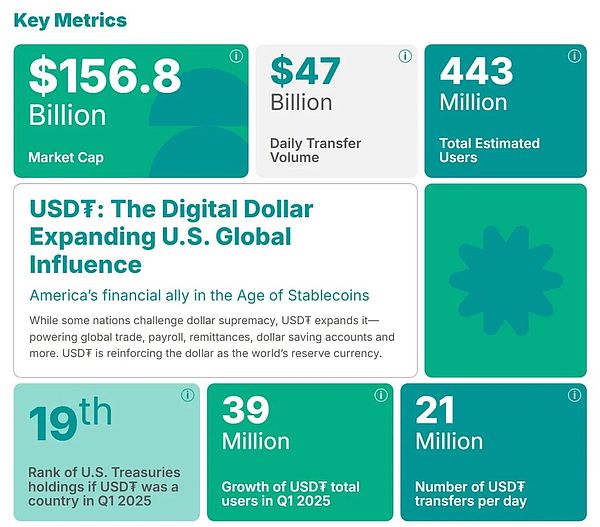

From an equity perspective, the Tether Group currently has approximately $176 billion in assets, while the market value of its stablecoin is $155 billion. They strictly maintain a single reserve of stablecoins, that is, on the basis of 100% reserves of USDT stablecoins, they retain an additional approximately $6 billion. In contrast, the traditional banking system usually adopts a fractional reserve system, retaining only about 10% of liquid assets. Tether has approximately 105% of liquid assets as reserves for stablecoins, supplemented by $15 billion in group equity. This strong reserve model is unprecedented in the industry.

1.3 After the Stablecoin Act is passed

Paolo believes that if the Genius Act is passed in its current form, it will bring many opportunities to Tether and the entire industry. He pointed out that in the past four years, the industry has faced the "Operation Chop Point 2.0" action, and government departments such as the U.S. Office of the Comptroller of the Currency (OCC) have been opposed to cryptocurrencies, which has limited the development of crypto-friendly banks. This is also one of the reasons why Silicon Valley Bank and Silvergate Signature collapsed and almost killed Tether's competitor Circle.

However, the Trump administration is now building a framework to support crypto-friendly banks, which will enhance the security of the entire industry, and Tether is looking forward to it. Federal Reserve Chairman Powell recently said: Banks can provide banking services to the cryptocurrency industry and conduct related businesses, provided that the security and soundness of the financial system are ensured.

Numerous banking consortiums, such as JP Morgan or companies like Amazon and Walmart have announced their intention to create stablecoins. In Paolo's view, the more competition, the better, as this will drive technological progress, improve efficiency, and reduce costs.

For markets outside the United States, Paolo hopes to see more countries adopt legislative frameworks similar to the GENIUS Act. Paolo pointed out that Europe's MICA compliance requires that at least 60% of the assets of stablecoin issuers be held in banks in the form of uninsured cash deposits. This is in stark contrast to the US GENIUS Act, which requires that the reserve assets of stablecoins must be US dollars or US Treasuries. Paolo believes that this requirement is more robust in the United States, where deposit insurance is $250,000, while in Europe it is 100,000 euros. He mentioned that if a stablecoin company has 60% uninsured cash deposits, it will be a huge risk, especially in the event of a bank bankruptcy.

In addition to the United States and Europe, other regions are also actively promoting the legislation of stablecoins. For example, Hong Kong has passed the Stablecoin Act. Singapore also released a stablecoin regulatory framework in 2023. These legislative developments show that a consensus is gradually forming on the regulation of stablecoins worldwide, and the GENIUS Act may become a reference template for legislation in other countries.

Paolo believes that the GENIUS Act provides a clear regulatory framework for the stablecoin market, especially in terms of more robust requirements for reserve assets. He hopes that Europe can learn from the experience of the United States and adjust its legislative requirements to promote the healthy development of stablecoins. At the same time, he also expects other countries to adopt similar legislative frameworks to promote the unification and standardization of the global stablecoin market.

1.4 Europe's attitude towards Euro stablecoins and CBDC

Bankless asked Paolo whether Europe would prefer to develop a digital currency led by the EU Central Bank rather than letting private companies launch stablecoins like the United States. Paolo believes that Europe may fully implement CBDC, but he has reservations about this.

Paolo pointed out that Europe is concerned about the popularity of US dollar stablecoins and is worried that the US dollar will replace the international status of the euro. He mentioned that if people are randomly asked outside of Europe whether they prefer their national currency or the US dollar, most people will choose the US dollar. In contrast, the euro has a lower profile and acceptance outside of Europe. Therefore, Europe tries to maintain the status of its own currency through protectionist measures.

Paolo expressed concerns about CBDC, especially about privacy and freedom. He pointed out that currently in credit and debit card transactions, banks act as intermediaries, providing a layer of isolation between individuals and the state, protecting the privacy of individuals. The state cannot track you or geolocate every transaction you make. For example, if you spend digital euros in a bar in Milan, the central bank will know. I think this is too much. We sometimes see Europe go crazy and decide that free speech is no longer an option and should be reduced, etc.

However, with CBDC, the central bank will be able to track every transaction, which may lead to excessive infringement of personal privacy. He emphasized that this excessive surveillance may be used to restrict freedom of speech and other fundamental rights. If you control people's money, you may eventually use this power to seek people's obedience.

Paolo believes that Europe's motivation for promoting CBDC is partly to counter the popularity of US dollar stablecoins and protect the international status of the euro. However, he is concerned that this approach may sacrifice personal privacy and freedom. He hopes that Europe will be more open to innovation in the private sector rather than over-relying on central bank digital currencies to achieve its goals.

1.5 About Circle IPO

Bankless mentioned Circle's stock price performance after its initial public offering (IPO), which rose from an issue price of $31 to $300. He saw some analysis on Twitter that if Tether received a similar valuation, its valuation would reach about $3 trillion. He asked Paolo what he thought of Circle's stock price performance.

Paolo responded that Tether currently has no plans to go public. He explained that there are usually two main reasons why companies choose to go public: one is that they need funds, but Tether's profitability is very strong and does not need external financial support; the other is to provide shareholders with an exit mechanism, but Tether does not need to consider the issue of shareholder exit at present. He emphasized that Tether's profitability not only supports the company's own operations, but also enables them to make large-scale investments. In the past two years, Tether has invested more than $5 billion in the United States, a fact that is often overlooked but is crucial to the company. They are committed to giving back to the United States, the country that created the great currency of the US dollar.

Paolo also mentioned that going public is usually to obtain cheap capital or to meet the exit needs of shareholders, and Tether does not need either. He himself has no intention of leaving the company because the company still has too much development potential and things to prove. There are many different verticals and industries that can be explored under the concept of USDT, and they are committed to serving the interests of the people in a disruptive way, rather than just for the interests of a few companies.

Although Tether currently has no plans to go public, Paolo admits that Circle's stock price performance is indeed impressive from a valuation perspective. He believes that if Tether's valuation can reach a similar level, it will be a very good result. However, he also said that They will pay attention to the sustainability of this valuation level, but in any case, this is a positive signal for Tether.

Although we can see the Circle IPO boom and many large companies are preparing to issue their own stablecoins, Paolo believes that stablecoins have completely different application scenarios in the United States and other parts of the world, which may be a controversial point of view.

2.1 Business models in different scenarios

He pointed out thatthe current stablecoin business model in the US market seems difficult to work. Although Circle's IPO has attracted a lot of attention in the United States, the fact is that it is almost impossible to make money through stablecoins in the United States. All these competitors will focus on the US market where profits are easier to obtain because it is low-hanging fruit for them. But in his opinion, the stablecoin market in the United States is caught in a race to the bottom.

A. Fee competition compresses profitability

Paolo reviewed the development of cryptocurrency exchanges. Around 2010, exchanges began to emerge, and Bitfinex charged 20 basis points for each transaction. However, today as a taker, the transaction fee is only one basis point, which is a significant drop compared to ten or twelve years ago, which reflects the fierce competition in the market and the decline in profitability.

B. Improved capital efficiency

The United States is one of the most efficient markets for capital flows in the world, with an efficiency of 90% in its financial channels. If stablecoins are introduced in the United States, the efficiency may be increased from 90% to 95%, but the premium space brought by this increase is very limited.In contrast, in other parts of the world, such as Nigeria, Argentina or Turkey, the efficiency of financial channels may be only around 10%-20%. After the introduction of stablecoins, the efficiency is expected to increase to 50%, which means an efficiency increase of 30%-40%. So for these countries, stablecoins are more significant. In emerging markets, people are more willing to accept lower interest rates because the daily volatility of their own currencies is much higher than the 4% yield that Tether can offer each year.

To some extent, the red ocean competition in the global north may be beneficial to Tether's profitability, but from the perspective of industry development and end users, this is not a good thing. Because in theory there should be more competitors in the market to further improve efficiency and reduce costs. At the same time, Paolo also pointed out thatThere are many opportunities in the world. For example, there are still 3 billion people in the world who do not have bank accounts, and Tether currently covers 450 million users. The opportunities here are huge and there is still a lot to do.

Regulatory regulations should also take this into account and provide appropriate safeguards for overseas issuers like USDT. USDT is a foreign stablecoin to the United States, but its importance is no less important, and it is even more important for maintaining the global status of the dollar and purchasing US Treasury bonds.

(USDT.network)

Therefore, Paolo emphasized that it is crucial to distinguish between these two different products and application scenarios. In the United States, stablecoins may evolve into tokenized money market funds, similar to the JPMD he mentioned. Other stablecoins will also develop in this direction, and the returns will be mainly returned to users.

For Tether, the onshore US dollar stablecoin they plan to create needs to compete on different levels, especially in programmability and services, rather than competing with USDT's business model, because USDT is a stablecoin designed for foreign markets.

2.2 Competitive Advantages of Tether

Bankless said that the domestic stablecoin market in the United States will be very competitive in the future. At present, there are more and more discussions about the issuers of stablecoins in the United States, including Amazon, Walmart, and even Meta, Twitter and other companies have reported that they will launch stablecoins. In addition, large banks such as JPMorgan Chase, Citi, and Wells Fargo are also exploring alliance stablecoins. If large banks in the United States can mint tokenized deposits and settle with the Federal Reserve's assets, then after this situation becomes common in the country, he wonders what competitive advantages (moats) Tether will have left in five years.

Paolo responded that Tether's distribution partners and its own distribution network still have great potential. He also pointed out that banks usually only sell their stablecoins to their own customers, and will not actively promote stablecoins on the streets like Tether does, educating ordinary people, especially those with low and middle incomes.

He emphasized that when Tether enters a new country, it will not directly cooperate with the largest local bank like its competitors. Instead, they will go deep into the streets to carry out grassroots education and promotion. They will visit door to door, looking for local partners who share their ideas, starting from the grassroots, and promote their products. This bottom-up promotion method has always been their method.

Although the United States has an advanced financial infrastructure, Paolo mentioned that he has seen reports that many people even have difficulty maintaining bank accounts. Therefore, he believes that more and more people in the United States will benefit from Tether's products because Tether's products take a more direct and close-to-the-people approach to communicating with people, rather than being high up and thinking that the world is the same as it was 20 years ago.

As we told us in the previous article, Arthur Hayes told us about Bitfinex and Tether's joint creation of USDT products,-People need to bypass the banking system to create a digital dollar that can flow freely, for free, and 24/7.

In this crypto-native world, Tether has already won in the first phase of this stablecoin.

With the advancement of the GENIUS Act, the stablecoin industry is about to enter the second phase, in which the key to stablecoins lies in distribution. As a pioneer in the industry, Tether has established a strong crypto-native distribution channel. Bbakless asked Paolo how Tether will continue to win the second phase of stablecoins in the face of these new competitors?

3.1 Distribution Network from an Investment Perspective

Paolo responded that, first of all, based on his understanding of the GENIUS Act, it may be difficult for large technology companies like Meta to launch their own stablecoins, because there seems to be some kind of ban in the bill that restricts companies that are not in the main financial industry from issuing stablecoins. He believes that these large technology companies may need to work with existing stablecoin providers or small banks to support other stablecoins and obtain revenue sharing. Paolo emphasized that although companies such as Meta have a large user base, they may face restrictions in the issuance of stablecoins.

Secondly, in terms of distribution channels, Paolo pointed out that Tether has invested in more than 100 companies, and these investments were made with Tether's own funds, rather than with reserves, which has brought profitability to Tether and established a wide range of distribution channels. Tether has established strong physical touchpoints in places such as Africa, Central and South America, covering millions of entities, which is one of the key factors in their success.

Paolo detailed Tether's innovative projects in Africa, where they are building kiosks with solar panels and rechargeable batteries to solve local power shortages. These kiosks offer subscription services at a price of 3 USDT per month, and currently have about 500,000 users and 10 million battery replacements. By the end of 2026, Tether plans to have 10,000 kiosks, and by the end of 2030, this number will increase to 100,000, covering approximately 30 million households, covering an average of 120 million people in Africa. This initiative not only provides electricity to local residents, but also enables them to use USDT for daily transactions.

Paolo believes that this innovative distribution channel and deep penetration into emerging markets are the key to Tether's leading position in the stablecoin field .

He emphasized that Tether is not only technologically advanced, but has also established an unprecedented dollar distribution network worldwide, which is one of Tether's least known advantages .

3.2 Acceleration boosted by the epidemic

Bankless found when browsing Tether's statistics (USDT.network) that the total estimated number of Tether users reached 440 million, and these users are actually using US dollars for transactions. They believe that the entire United States has ignored this use case. They curiously asked Paolo how the first phase of market expansion and distribution happened, which could not be achieved solely through the narrative of emerging markets. Paolo responded that, unfortunately, the success of USDT was not because of how well we did, but because the economies of many countries were too bad. Take Turkey as an example, with annual inflation as high as 50%, and the local currency has depreciated by 80% against the US dollar in the past few years; Argentina is even worse, with the local currency depreciating by almost 90% and defaulting on many occasions. USDT provides a safe haven for these countries. It was the global pandemic that largely changed the trajectory of Tether's user growth. He mentioned that Tether's market value was only $4.7 billion in 2020, and Tether did not actually form a marketing team until 2022. Therefore, the growth from 2020 to 2022 was bottom-up and was the result of natural growth of users.

Paolo explained that emerging markets in developing countries have three common characteristics:

These countries are relatively poor;

Inflation rates are high, much higher than in wealthy countries;

These countries have a high penetration of smartphones, a high level of digitization, and a young population structure.

From 2017 to 2020, it was these young people who were the first to come into contact with and understand cryptocurrencies. When the epidemic broke out in 2020, the situation changed. The epidemic accelerated the rise in unemployment rates around the world, especially in emerging markets, and the rise in unemployment rates exacerbated inflation.

During the epidemic, people became increasingly afraid and took to the streets to buy US dollar cash. For example, in Argentina, when the epidemic began, the Argentine peso began to depreciate, and people were afraid of losing their jobs and being unable to work, so they took to the streets and bought US dollar cash on the black market. However, in 2020, these young people saw their parents going out and taking risks to buy US dollars during the epidemic. Children ask their parents why they risk going to the black market to buy dollars when they already have them in their cryptocurrency wallets. This phenomenon has become particularly evident during the pandemic.

Paolo stressed that This phenomenon is particularly prominent in emerging markets, where the economic situation is relatively fragile. In Europe and the United States, although there are also problems, they are generally better than emerging markets. When people face economic difficulties and their families are at risk, they will do everything they can to protect their families. That's why people have found ways to hold and obtain dollars through local exchanges, platforms such as Binance.

And these young people, who are familiar with cryptocurrencies and willing to try new things, have become the key force driving this trend. Through word of mouth, one parent told another parent that they were buying dollars on this app, etc., and this phenomenon gradually spread.

3.3 The next driver of growth

Bankless asked Paolo if there was any correlation between Tether's market value and the total market value of the entire cryptocurrency market. He pointed out that before 2022, Tether's market value experienced a massive acceleration in growth, and then the market experienced a decline.

Paolo responded that according to their statistical analysis,

less than 40% of Tether's market value is related to the cryptocurrency market. In other words, more than 60% of the market value growth actually comes from the grassroots use of USDT in emerging markets. He emphasized that the application of USDT in these markets occurred naturally, rather than through the direct promotion of Tether. Paolo further pointed out that the next driving force for the growth of USDT's market value may come from the trade of commodities. He mentioned that almost all the largest commodity traders are contacting Tether because USDT is a very attractive solution for them. In international trade, the slow process of relying on banks leads to capital inefficiency, while USDT can significantly improve transaction efficiency.For commodity traders, USDT provides a fast and efficient payment method. Since commodities often come from emerging markets, traders need to ensure that sellers can receive payments as quickly as possible so that they can move on to the next transaction. Therefore, USDT is an ideal choice for both buyers and sellers.

Paolo also mentioned a specific example, where stores in Santa Cruz and other towns in Bolivia have begun to mark USDT on price tags. He emphasized that all this happened naturally and Tether did not conduct any promotional activities in Bolivia. This shows that the acceptance and use of USDT in emerging markets is growing naturally, which will provide continued momentum for Tether's market value growth.

3.4 The expansion of the US dollar under geopolitics

So how do we understand Tether’s role in the current geopolitical landscape, especially the expansion of “Western values”?

Paolo:

In my opinion, money is the ultimate social network,and the changes driven by Tether have a triple impact.First, Tether is doing more effective financial inclusion than many international organizations, NGOs, and even charities. This is shocking to me - if a small company can do what they haven't done for decades, it means they really need to reflect. We are truly bringing financial services to hundreds of millions of people around the world who are still excluded.

Second, Tether is expanding the global use of the dollar and promoting dollar hegemony. This is not an exaggeration. We have established millions of offline touchpoints in emerging markets, from convenience store networks, phone recharge points, and newsstands in Central America to rural markets in Africa, where we engage directly with them. These distribution channels can also be used for financial education and even to sell other products.

Third, Tether is building its own energy and financial infrastructure in Africa. In this continent with extremely low electricity coverage—600 million of the 1.4 billion people have no electricity at home—we have built solar-powered financial service kiosks. In these small villages, Tether's kiosks provide rechargeable batteries for only 3 USDT per month. Residents use these kiosks to learn how to open USDT and Bitcoin wallets, save and transfer money. We have deployed 500 such kiosks in Africa, with 500,000 users and 10 million battery replacement records. It is expected to expand to 10,000 kiosks by 2026 and 100,000 by 2030, covering about 30 million African households. This is not only financial distribution, but also light distribution. We want to light up the center of the African continent, and then this distribution network will be visible from space.

3.5 What do users really care about?

Paolo: Users are not interested in the blockchain itself. They only care about one thing - the fees should be low, almost zero.

We have recommended some partners' digital wallets to users and encouraged them to deposit USDT into these wallets. However, we have noticed a phenomenon: many wallets are promoting various fancy features to users, such as investing USDT in other currencies, participating in staking or purchasing NFTs. Although these features seem rich, they may put users into unnecessary risks and are extremely detrimental to family savings.

Given this, Tether has decided to take matters into its own hands and build a wallet that is truly savings-centric, tailored for these markets. We are developing an open source SDK, called the Wallet Development Kit (WDK), which will allow anyone to build a wallet based on it. The interface of this wallet is extremely simple, with only two accounts: a USDT daily account for users' daily payment needs, and a savings account where users can deposit Bitcoin and connect to decentralized yield protocols to earn returns. While we provide developers with the flexibility to add new features, the default version will be a minimal version designed for African users, aiming to provide the most basic and practical functions.

In terms of cooperation, we maintain a close cooperation with Opera's MiniPay team, and are actively looking for more partners to jointly promote the development of this project.

Tether has been actively engaged in Bitcoin education around the world. However, in these markets, we often hear feedback like this:"I understand Bitcoin, but I still prefer to use USDT." This is not because people are ignorant, but because they do not have enough time or resources to deeply understand Bitcoin.Many "Bitcoin maximalists" often ignore this point. They mistakenly believe that people all over the world have the time and ability to study cryptocurrency, but in fact, this is not the case.

Therefore, we decided to start with USDT, which users are familiar with and trust, to build a trust relationship first, and then gradually guide them to Bitcoin. Education is a long-term battle that cannot be achieved through verbal propaganda alone, but through practical actions. Tether is investing a lot of money and resources on the ground to actively promote this education process, and is committed to enabling more people to use digital assets for savings safely and stably.

Tether has made about $20 billion in the past two or three years. Less than 5% of it has been distributed to shareholders. Our idea is that most of the funds should be kept in Tether's investment department. As you mentioned, part of the excess reserves are used for over-collateralization of stablecoins, but the remaining approximately $14 billion or more is now invested in different ways.

Tether Ventures has made investments in many different fields, including Layer 1 chains designed specifically for Tether (such as Plasma and Stable), mobile networks, telecommunications networks, energy startups, media technology companies, and even an Italian football team. Bankless asked Paolo about Tether Ventures' investment strategy.

4.1 Tether's investment layout

Paolo responded that Tether's investment portfolio is very broad and covers different verticals. He explained that a good investment portfolio should include conservative and stable assets, and Tether is no exception. In addition to buying traditional assets such as Bitcoin (the Tether Group currently holds more than 100,000 Bitcoins) and gold (the Tether Group currently holds 80 tons of gold), Tether has also begun investing in land and agricultural companies. For example, Tether has invested in Adecoagro, a company that owns a large amount of land in South America, and its main businesses include dairy, bioethanol, rice and livestock products. Paolo pointed out that land is a scarce and safe asset that has historically appreciated slowly. In addition, agriculture is closely related to commodity trading, and Tether's stablecoin USDT has potential application value in commodity trading.

What I said about commodity trading and USDT can also be applied to agricultural products. Therefore, USDT and stablecoins in general will also accelerate agricultural companies to become more efficient in terms of access to capital,while also speeding up the payment of the goods they produce. So it's a very interesting marriage between the two. And then there's another area where Tether is, which is new technologies. Artificial intelligence is one of them.

Paolo also mentioned Tether's investments in new technologies, especially artificial intelligence. Tether is building its own peer-to-peer artificial intelligence platform, QVAC, which aims to bring artificial intelligence closer to people, able to run on a variety of devices, from low-end smartphones to high-end servers. In addition, Tether has invested in Blackrock Neurotech, a brain-computer interface technology company, which Paolo believes is crucial for humans to maintain their advantage in the competition with artificial intelligence and robots.

Tether has also invested in Northern Data, a leading AI infrastructure company with more than 24,000 H100 GPUs and its own AI R&D team. We are also developing a P2P reasoning and federated learning platform called "CUAC", which is inspired by Isaac Asimov's short story "The Last Question", which raises the ultimate question: "Can entropy be reversed?" The philosophy behind this is that if we want AI to answer this question one day in the future, it must be part of the structure of the universe, not a data center system controlled by a centralized company.

Regarding Tether's investment in the Italian football team Juventus, Paolo said that although this investment accounts for a small proportion of Tether's portfolio, as Juventus fans, they see the potential for global promotion through the football club. Juventus fans are all over the world, which provides Tether with a unique distribution channel. Tether can also help Juventus achieve its goals in football. We have a global digital and physical distribution network that can promote Juventus' brand to the world. In addition, many of the technology companies we invest in can also help Juventus.

In general, Tether Ventures' investment strategy is diversified, aiming to achieve long-term growth and stability through different verticals. These investments include not only traditional financial assets, but also emerging technologies and global market promotion opportunities.

4.2 The core logic of investment

Bankless: When evaluating potential investments, is distribution the primary consideration, and is distribution at the core of every investment?

Paolo answered affirmatively that distribution is indeed a key factor when they evaluate investments.

For example, Tether invests in digital distribution networks, such as Rumble. It is a video platform with 70 million users. An interesting thing is that the creators of Rumble sold $850 million of gold between 2023 and 2024. Imagine how big the opportunities would be if Rumble launched a wallet that supports Bitcoin and Tether Gold? So we hope to combine this digital infrastructure and asset distribution.

He further explained that even in the field of artificial intelligence (AI), they see huge potential. He predicts that in the next 15 years, there may be a trillion AI agents, and each AI agent should have a non-custodial wallet. He doubts that these AI agents will open accounts at traditional financial institutions such as the Federal Reserve or JPMorgan Chase, so Tether is developing a wallet development kit called WDK (Wallet Development Kit). This kit will be completely open source, allowing anyone to build a complete non-custodial wallet, Tether will not hold any keys, users are free to create any model they want, and Tether will support all different blockchains.

Paolo went on to elaborate on their vision, where he hopes to create a seamless user experience with their AI platform. He used the example of a smart refrigerator that displays a QR code that connects to a non-custodial wallet. The user can top up the refrigerator with, say, $50, and the refrigerator will automatically buy groceries. He emphasized that he doesn’t want the money in the refrigerator to be stored on a third-party payment platform like PayPal because that’s not the user experience he expects.

He also looked to the future, imagining that in 20 years or more, even devices like light bulbs may be equipped with very small AI that can automatically adjust the optimal amount of power and lighting based on the environment. He believes that achieving such a future goal requires the support of local AI, rather than having each device connect to a central server like ChatGPT, which would cause server overload and high latency. Therefore, it is very important to provide wallet support for local AI, and it would be even more ideal if stablecoins were added to this wallet.

Bankless: Some of Tether's investments happened to catch up with the trend in the cryptocurrency field, especially Layer 1 blockchains such as Plasma and Stable, which are trying to become Layer 1s based entirely on Tether. They asked Paolo whether any of these Tether-specific high-throughput blockchains would become the "Tether chain" and how Tether views its investments in these blockchains.

Paolo responded that he did not think there would be a "Tether chain" and did not think there would be one in the future. He stressed that despite this, there are great opportunities in these blockchain projects and there are great teams that can build great ecosystems. He foresees that the fees of certain blockchains will vary over time, sometimes high and sometimes low.

Tether may launch a wallet that supports all networks by the end of the year, which will be built using the WDK (Wallet Development Kit) with the goal of allowing everyone to build similar wallets. Paolo stressed that Tether does not want to make money from the wallet, but wants to ensure that there is a good product on the market.

He envisions a future where users' wallets can automatically transfer USDT to chains with lower fees based on cross-chain swap tools, thereby incentivizing blockchains to keep fees low. He believes that this user experience is the best for the end user because it allows for fair competition between different chains and lets users decide for themselves which chain is best for them.

Bankless further asked Paolo how to describe Tether's relationship with Bitcoin and whether Tether considers Bitcoin to be special or it is just another chain. They mentioned that Tether was originally issued on Omni Network (a Bitcoin sidechain), then exploded on Ethereum, and now Tether is investing in and incubating blockchains that support Tether, including the Bitcoin sidechain Plasma. They wanted to know what Paolo thinks of Bitcoin.

Paolo expressed his love for Bitcoin, mentioning that the way Bitcoin was born is poetic and that it is a simple chain that has accomplished its mission. He especially likes Bitcoin because it works even in the worst cases. Although Bitcoin’s 10-minute block time is considered slow, Paolo believes that this is justified. He mentioned that Layer 2 solutions such as Lightning Network, Light Spark, etc., as well as Plasma, offer more opportunities.

He believes that Layer 1 should not be used for payments, and even Ethereum has realized that there will be bottlenecks in making payments on Layer 1. Therefore, there needs to be a scalability layer, and this is the right way to go. Paolo also mentioned that Bitcoin’s block size and block time make it possible for people to download the Bitcoin blockchain even in remote villages in Africa. If the block time is faster, like Solana, then almost no one can run a node in countries with underdeveloped networks. Therefore, Bitcoin is very special to him because it is the ultimate inclusiveness and can work even in the worst case scenario, even in World War III. He emphasized that other blockchains have different use cases, but it is very important to distinguish between different use cases. For example, Plasma is compatible with EVM, and Blockstream Liquid is another great Bitcoin sidechain that is working on a contract system similar to Turing complete. Paolo said that he likes innovations outside of Bitcoin, but Bitcoin is their love and is very consistent with their philosophy.

He also mentioned that as Bitcoin block rewards gradually decrease, the fees on the chain may rise sharply. He believes that the Bitcoin main chain will become the settlement layer for Lightning Network-style channels, or the bottom layer of some very important contracts. In this case, a user may open a Bitcoin transaction on the first layer, then make countless transactions on the second layer, and finally return to the first layer for settlement. If the fee for each settlement is $500, but it is actually the sum of 1 billion transactions, then the average cost per transaction becomes very low. Paolo believes that this dynamic is one of the most beautiful parts of the Bitcoin network, and as more and more new layers or new applications emerge on Bitcoin, they will all be anchored to Bitcoin, making Bitcoin the security layer that anchors everything.

There has been a lot of negative news about Tether in the past, and Tether has experienced many ups and downs with the US government, but Bankless feels that 2025 is almost Tether's year of redemption. Now there is no more negative news, and even US lawmakers recognize what Tether is, how big it is, and the value it brings to the US Treasury market.

Paolo believes that Tether has many benefits for the United States.

First, Tether is bringing financial inclusion to hundreds of millions of people through the dollar. There have been charities and NGOs that have raised a lot of money from all over the world trying to solve the problem of financial inclusion. A company like Tether is able to bring financial inclusion to nearly 500 million people, and Tether is doing it with the dollar.

Second, Tether is spreading through the dollar. When other BRICS countries are trying to replace the dollar's international position, Tether is helping. In fact, Tether is one of the companies that helps the United States the most. When Tether is in Africa and Central and South America, you don't see the United States, but you see the BRICS. They are trying to replace the dollar's position, and Tether's presence is associated with millions of touch points. Tether is trying to fight back and is making the dollar the preferred currency and the most used currency in these countries.

Third, Tether is one of the largest buyers of US Treasuries and US debt. Three years ago, China held $2 trillion of US debt, and now it's less than $700 billion. This could be used as a weapon against the United States. As I said, you want to diversify the ownership of US debt, and Tether is helping the United States do that.

Fourth, Tether invests in the United States. Tether reinvests most of its profits in the United States, supporting very good American companies. Everything Tether does is closely related to the United States. Tether stores Treasuries in the United States, not in some random European bank.

When it comes to crypto, it's interesting because there is indeed a lot of FUD (Fear, Uncertainty, and Doubt), but if you pull up the chart, you can see that FUD is one thing, but FUC (Fundamental Underlying Conditions) is another. The chart is almost always growing. Tether's stability and transparency have provided a solid foundation for the cryptocurrency market and helped drive the growth of the entire industry.

Tether generates 1 billion USDT, strategically enhancing liquidity and market readiness.

BrianSolana aggregator Jupiter plans a system upgrade focused on reliability and user feedback, aiming to enhance performance and maintain its lead in the evolving blockchain market.

Alex

AlexBinance introduces Sleepless AI gaming on Launchpool, offering AI token staking and trading starting December 28, 2023, with various rewards and mandatory KYC for participants.

Kikyo

KikyoNaver's cutting-edge AI robots, fuelled by a 5G cloud, might reshape crypto trading, but concerns linger over global infrastructure readiness and regulatory hurdles.

Hui Xin

Hui XinBounce Brand's AMMX token launch, involving oversubscribed AUCTION and DAII pools, signifies robust interest and growth in decentralized finance.

BrianDOJ reveals an $80 million 'Pig Butchering' crypto scam hitting Americans, intertwined with global human trafficking networks. UK joins the fight, imposing sanctions on individuals linked to the scheme, shedding light on a dark nexus of financial fraud and exploitation.

Joy

JoyAfter enduring a ten-year wait, Mt. Gox creditors are now witnessing the long-awaited arrival of payments, marking a significant development in the aftermath of the exchange's collapse.

Hui XinOn Christmas Day, cryptocurrency scammers managed to siphon off a staggering $3 million from unsuspecting victims. Employing a tactic using Google Ads to direct users to fake websites equipped with wallet-draining software, these scammers continue to plague the cryptocurrency landscape with their malicious schemes.

JoyThe analoS Airdrop is making waves in the cryptocurrency world, offering a massive giveaway of $ANALOS tokens. With its distinctive philosophy and ambitious ecosystem incentives, analoS is challenging established memecoins and attracting a wide range of crypto enthusiasts. This event is not just a token distribution but a signal of an evolving crypto landscape where innovation and community engagement are key to success.

AlexManta Pacific introduces Manta New Paradigm, a Layer 2 platform offering enhanced yields and a significant $MANTA token airdrop, backed by major firms and led by industry experts.

Kikyo