Article Author: VannaCharmer Article Compilation:Block unicorn

In the token market, Perception is everything. As in Plato's allegory of the cave, many investors are trapped in the shadows - misled by the distorted illusion of value by malicious actors. This article will reveal how VC-funded projects systematically manipulate token prices, including: Maintaining the "false float" (FALSE Float) of tokens as much as possible. Compressing the "real float" (REAL Float, for easy manipulation) as much as possible. Using the fact that the real float is extremely low to drive up the price of their tokens.

From the "Low Circulation / High FDV" Model to the "Fake Circulation / High FDV" Model

No, I'm nota low circulation / high FDV token! I'm "Community First"

Earlier this year, the surge in Meme coins caused VC tokens, which were called "low circulation / high FDV" tokens, to fall out of favor. With the rise of platforms like Hyperliquid, many VC tokens have become uninvestable. However, rather than fix the flaws in their token economics or focus on developing actual products, these projects have doubled down on artificially controlling the supply while claiming otherwise.

Lowering the supply is extremely beneficial to the project because it makes price manipulation easy. For example, a foundation can cash out locked tokens through behind-the-scenes transactions and then buy them back on the open market, which is very capital efficient. At the same time, extremely low true supply makes the token price extremely easy to manipulate, exposing short sellers and leveraged traders to extreme risks.

Here are a few typical cases (not a complete list):

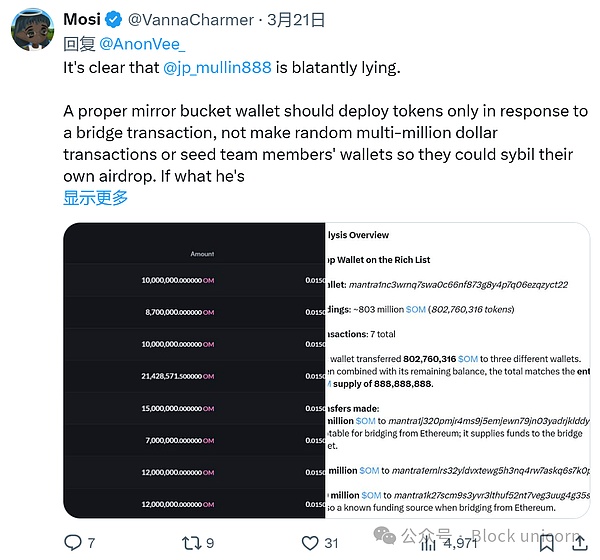

1. MANTRA Chain

This is the most blatant case. A project with a TVL of only $4 million and a FDV of more than $10 billion? The answer is simple: they control the vast majority of $OM in circulation. The Mantra team stored 792M OM (90% of total) in a single wallet and didn’t even bother to disguise their holdings. When I questioned @jp_mullin888, he argued that it was a “mirror storage wallet” which is bullshit.

So how to calculate the real circulation of Mantra?

We can calculate it in the following way:

980 million (declared circulation) - 792 million (the part controlled by the team) = 188 million OM

This 188 million OM number may not be accurate either. The team still holds a significant portion of OM, and they also manipulated airdrops through Sybil attacks, further reducing the actual circulation. They used about 100 million OM to fake airdrops, which also needs to be deducted.

The final actual circulation is only 88 million OM (assuming that the team does not control more, but this assumption is likely wrong). Based on this calculation, this makes Mantra's actual circulation market value only $526 million, which is a far cry from the $6.3 billion shown on CoinMarketCap.

The extremely low real circulation allows the team to easily manipulate the OM price and blow up short positions. The team controls most of the circulation and can raise and lower the price at will. Retail investors shorting OM is like betting against @DWFLabs on Dogecoin. I suspect that Tritaurian Capital, the $1.5 million company loaned to @SOMA_finance (@jp_mullin888 is the co-founder of SOMA, Tritaurian is owned by JPM's boss at trade io, Jim Preissler), as well as some funds and market makers in the Middle East, may be behind the current price action. This further tightens the true circulation and makes it more difficult to calculate.

2. Movement Labs

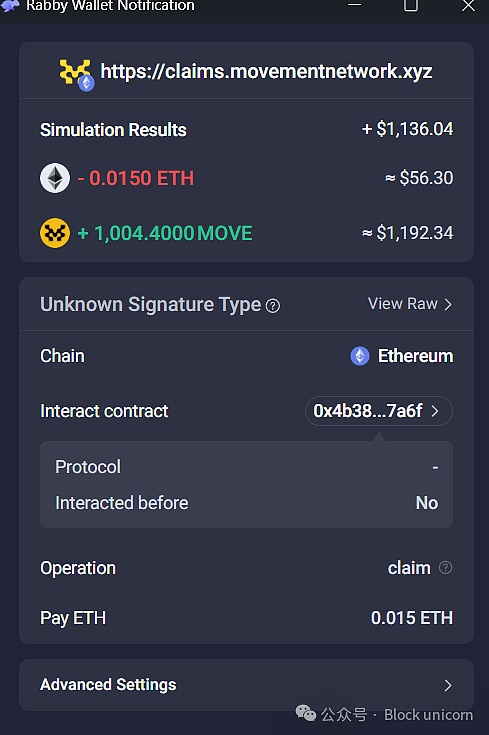

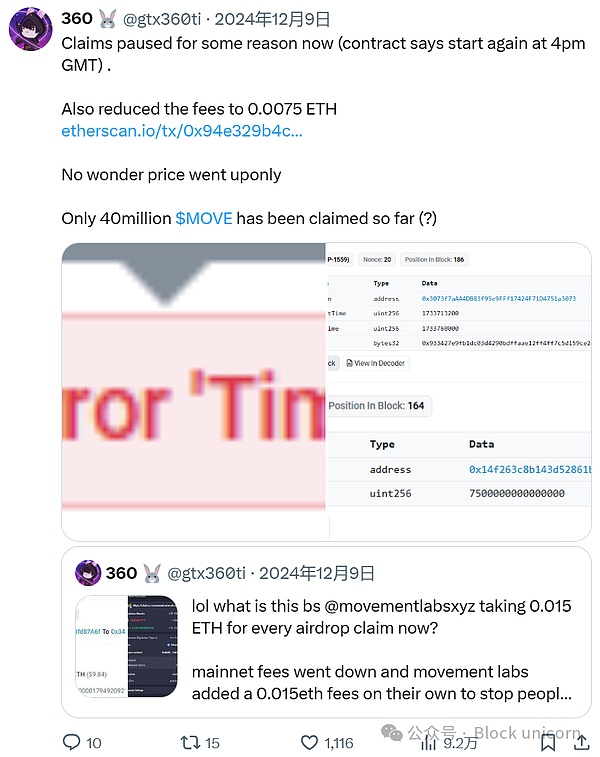

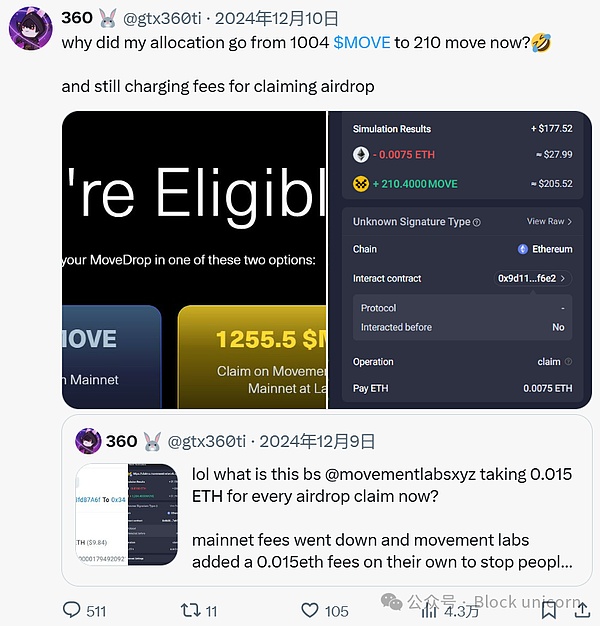

The project's airdrop offers two options: claim the airdrop on the ETH mainnet, or claim it on its unlisted chain (with a small reward). However, a few hours after receiving the tokens, the team suddenly:

Added a high fee of 0.015 ETH (about 56 USD) (excluding gas fees) to ETH mainnet recipients, forcing small testnet users to give up.

Cut the ETH mainnet allocation by more than 80%, but retain the high fee.

Suspend the token collection.

Set a very short deadline for the token collection.

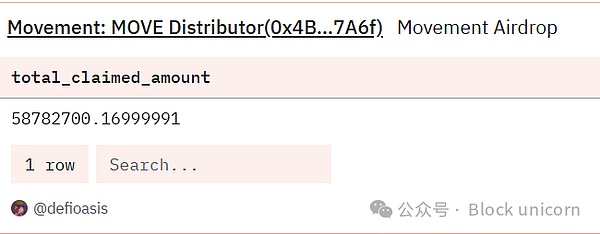

The result is obvious: only 58.7 million MOVE were claimed, accounting for 5% of the planned airdrop (1 billion).

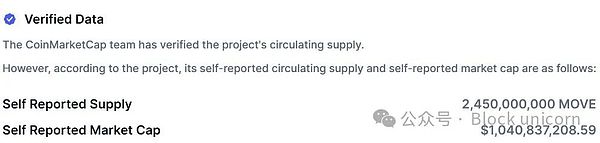

According to CoinMarketCap data, MOVE claims to have a circulation of 2.45 billion.

However, according to Move's pie chart, the tokens in circulation after the airdrop should only be 2 billion (base + initial airdrop), so the suspicious shenanigans start here, because 450 million MOVE are missing. 245 million MOVE (claimed circulation) - 1 billion MOVE (foundation allocation) - 941 million MOVE (unclaimed portion) = 509 million MOVE or $203 million in real circulation. The real circulation is only 20% of the claimed circulation! Moreover, it is hard for me to believe that all 509 million MOVE are in the hands of retail investors, but let's assume that this is the real circulation.

What did Movement Labs do during this period of extremely low real circulation?

Payed WLFI (market maker) to buy their own tokens

Payed REX-Osprey to apply for an ETF for MOVE (purely a gimmick)

Rushi (a member of the project) went to the NYSE to make a show

Colluded with funds and market makers to privately sell locked tokens in exchange for cash to let them pump the market

The team deposited 150 million MOVE at the high point of Bybit and may start selling it later (the token price has been falling since then)

Payed 70 per month to a Chinese KOL company before and after the TGE (Token Generation Event) $10,000 so that they can list on Binance and get more exit liquidity in Asia

In the words of Rushi: “We are just playing a game.”

3. Kaito AI

Kaito is the only project mentioned in this article that has an actual product, but their current airdrop distribution method also has similar problems.

As CBB pointed out, only a few people received Kaito's airdrop, which also affected the actual circulation. Let's do the math: According to Coinmarketcap, Kaito has a circulation of 241 million, or $314 million. I assume this number includes: Binance holders, liquidity incentives, foundation allocations, and initial community and airdrops.

Let's split it up and see what the real circulation is:

Real circulation = 241 million KAITO-68 million (unclaimed part) + 100 million (foundation holdings) = 73 million KAITO

The real circulation market value is only 94.9 million US dollars, which is much lower than CMC data.

Kaito is the only one of the three projects in this article that deserves partial trust, because they at least have profitable products, and as far as I know, their operations are not as bad as Movement and Mantra.

Solutions and Conclusion

CoinMarketCap and CoinGecko should show the real circulation of tokens, not the data made up by the project.

Exchanges such as Binance should take measures to punish such behavior. The current listing mechanism is broken - like Movement, paying KOL companies to fake data and cheat listing in Asia.

Traders please stay away from these tokens because the project can manipulate the price at will. They control all the circulation and thus the trend of the token (not financial advice).

Miyuki

Miyuki