There has never been a lack of legendary stories in the history of Wall Street, but the strategic transformation of MicroStrategy Bitcoin Treasury Company is destined to become a new and unique legend.

A Bitcoin strategy that has attracted global attention

In 2020, the COVID-19 pandemic triggered a global liquidity crisis, and countries adopted loose monetary policies to stimulate the economy, leading to currency depreciation and increased inflation risks.

Michael Saylor re-evaluated the value of Bitcoin during the COVID-19 pandemic. He believes that when the money supply grows at a rate of 15% per year, people need a safe-haven asset that is not linked to legal cash flow. Therefore, he chose the Bitcoin strategy for MicroStrategy.

Compared with the BTC ETF or other Spot Bitcoin ETPs launched by companies such as BlackRock, MicroStrategy's Bitcoin strategy is more radical. It purchases Bitcoin through the company's idle funds, convertible bonds, additional shares and other financing methods. The company itself obtains the potential benefits of Bitcoin's rise and bears the potential risks of Bitcoin's decline, while ETF/ETPs focus more on price tracking.

MicroStrategy's funding sources and Bitcoin purchase process

MicroStrategy mainly raises funds to purchase Bitcoin through four channels.

1. Use own funds to purchase

For the first three investments, MicroStrategy used idle funds on its books to purchase. In August 2020, MicroStrategy spent $250 million to purchase 21,400 bitcoins; in September, it invested $175 million to purchase 16,796 bitcoins; and in December, it invested $50 million to purchase 2,574 bitcoins.

2. Issuance of Convertible Senior Notes

In order to buy more Bitcoin, MicroStrategy began to use the issuance of convertible bonds to finance the purchase of coins.

Convertible senior notes are a financial instrument that allows investors to convert bonds into company stocks under certain conditions. This type of bond is characterized by a low interest rate, even zero, and a conversion price that is higher than the current stock price. Investors are willing to buy such bonds mainly because they provide downside protection (that is, the principal and interest can be recovered when the bond matures) and potential gains when the stock price rises. The interest rates of several convertible bonds issued by MicroStrategy are mostly between 0% and 0.75%, indicating that investors are actually confident in the rise of MSTR's stock price and hope to earn more income by converting bonds into stocks.

3. Issuance of Senior Secured Notes

In addition to convertible senior bonds, MicroStrategy has also issued a $489 million senior secured bond with an interest rate of 6.125% due in 2028.

Senior secured bonds are a type of secured bond with lower risk than convertible senior bonds, but this type of bond only has fixed interest income. This batch of senior secured bonds issued by MicroStrategy has chosen to be repaid in advance.

4. At-the-Market Equity Offerings

As MicroStrategy's Bitcoin strategy has begun to bear fruit and MSTR's stock price has continued to rise, MicroStrategy has adopted more at-the-market equity offerings to raise funds. Funds obtained in this way are less risky because it is not a debt, there is no repayment pressure, and there is no foreseeable repayment date.

MicroStrategy has signed open market sales agreements with agency structures such as Jefferies, Cowen and Company LLC and BTIG LLC. Under these agreements, MicroStrategy can issue and sell Class A common stock through these agencies from time to time. This is what the industry calls ATM.

Market-priced stock issuance is more flexible, and MicroStrategy can choose the time to sell new shares based on the secondary market conditions. Since the issuance of stocks dilutes the equity of existing shareholders, the correlation with the price of Bitcoin and the increase in the amount of coins per share of MSTR have led to a complex market reaction to this move, and the overall volatility of MSTR's stock price has been high.

MicroStrategy's process of purchasing Bitcoin through the above four methods is as follows:

Produced by: IOBC Capital

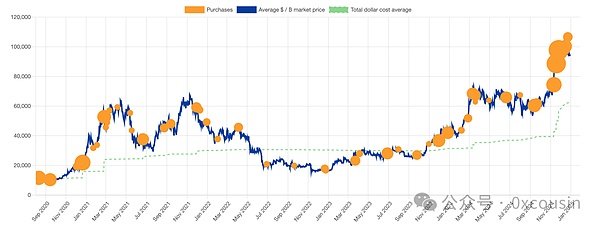

Corresponding to the BTC price trend chart, MicroStrategy's specific purchase history is as follows:

Source: bitcointreasuries.net

As of December 30, 2024, MicroStrategy has invested a total of approximately US$27.7 billion to purchase 444,262 bitcoins, with an average holding price of US$62,257 per bitcoin.

Several key issues regarding MicroStrategy's "Intelligent Leverage" purchase of Bitcoin

There is much controversy in the market about MicroStrategy's "Intelligent Leverage" strategy to purchase Bitcoin. Regarding several key issues hotly debated in the market, I would like to share my thoughts:

1. Is MSTR's leverage risk high?

First, the conclusion is that it is not very high.

According to the information disclosed by MSTR in the Q3 2024 earnings conference call, MSTR's total assets were approximately US$8.344 billion at the time, because the carrying value of Bitcoin in this financial report was only US$6.85 billion (there were only 252,220 coins at the time, calculated at a price of US$27,160). The total debt was approximately US$4.57 billion, so the corresponding debt-to-equity ratio was 1.21.

We will not discuss this accounting standard, but only consider the data at the time of actual sale, which reflects the latest market price. If calculated based on the latest market price of Bitcoin on September 30, 2024 (US$63,560), the actual market value of Bitcoin held by MSTR is US$16.03 billion, and the corresponding MSTR debt-equity ratio is only 0.35.

Let's look at the data as of December 30, 2024.

As of December 30, 2024, MicroStrategy's total outstanding liabilities were US$7,273.85 million, as follows:

Produced by: IOBC Capital

As of December 30, 2024, MicroStrategy held 444,262 bitcoins, valued at US$42.25 billion. Assuming that the assets of other parts of MicroStrategy remain unchanged (i.e., $1.49 billion), then MSTR's total assets are $43.74 billion and its liabilities are $7.27385 billion, then MSTR's debt-to-equity ratio is only 0.208.

Let's take a look at the debt-to-equity ratios of the top listed companies in the U.S. stock market: Alphabet 0.05, Titter 0.7, Meta 0.1, The Goldman Sachs Group 2.5, JPMorgan Chase & Co. 1.5.

MicroStrategy is a company that has transformed from the software industry to the financial industry, and this debt-to-equity ratio is still healthy.

Second, under what circumstances will these convertible bonds become an unbearable burden in the future?

First, let me talk about the conclusion. If MicroStrategy does not continue to issue convertible bonds, then Bitcoin will fall below $16,364 for a long time, and the value of the 444,262 Bitcoins held by MicroStrategy will be lower than the total amount of its convertible bonds of $7.27 billion. If MicroStrategy only uses ATM financing and idle funds to buy coins in the future, as the number of MicroStrategy Bitcoin holdings increases, this "insolvency" price line can become even lower.

If MicroStrategy continues to issue convertible bonds to buy Bitcoin when Bitcoin is high, and Bitcoin enters a bear market, the decline in Bitcoin prices will cause the value of Bitcoin held by MicroStrategy to be lower than the total amount of its convertible bonds, which will also cause MSTR's stock price to fall, thereby affecting its refinancing and debt repayment capabilities, and then the convertible bonds will become an unbearable burden.

For MicroStrategy's convertible bonds, bondholders have the right to convert their bonds into MSTR shares, and there are two stages: 1. Initial stage - if the trading price of the bond falls by >2%, the creditor can exercise the right to convert the bond into MSTR shares and sell it back to the original price; if the trading price of the bond is normal or even rises, the creditor can resell the bond in the secondary market at any time to recover the original price. 2. Late stage - When the bond is about to mature, the 2% rule does not apply. Bondholders can take back the cash and leave, or directly convert the bonds into MSTR shares.

Since the convertible bonds issued by MicroStrategy are low-interest or even zero-interest bonds, it is obvious that creditors actually want the conversion premium. If the MSTR stock price has a certain increase compared to the price at the time of financing on the repayment date, then the creditors are more likely to consider debt-to-equity conversion. If the MSTR stock price has a certain decline compared to the price at the time of financing, then the creditors will consider asking for principal and interest.

If the creditors do not choose to convert into MSTR shares, and MicroStrategy eventually needs to repay the creditors, it also has multiple options:

Continue to issue new shares to obtain funds for repayment;

Continue to issue new bonds and use new bonds to repay old debts; (This has already been done in September 2024)

Sell some Bitcoin to repay the loan.

Therefore, at present, it is unlikely that MicroStrategy will fall into a "liability-insolvent" situation.

Third, why do investors begin to care about the amount of coins per share of MSTR?

First, the conclusion is that the amount of coins per share will determine the net assets per share of MSTR.

Whether issuing convertible bonds or ATMs, financing is achieved by diluting equity. The purpose of financing is to increase Bitcoin reserves. For MSTR's shareholders, diluting equity is a negative, and in the traditional sense, it is not a good thing. The story that MicroStrategy's management told MSTR shareholders was BTC Yield KPI.

Essentially, as long as MSTR's market value is higher than the total value of BTC it holds, that is, there is a market value premium rate, then diluting MSTR's equity to buy BTC can increase the amount of money in each MSTR share. The increase in the amount of money in MSTR means that MSTR's net assets per share are growing, so for shareholders, diluting equity to achieve financing to buy Bitcoin is still a worthwhile thing to do.

Currently, MicroStrategy holds 444,262 BTC, with a total holding value of approximately US$42.256 billion. With the current market value of MSTR at US$80.37 billion, MSTR's market value is 1.902 times the value of its Bitcoin holdings, that is, the current premium rate is 90.2%. The current total share capital of MSTR is 244 million shares, and the corresponding BTC holdings per share are about 0.0018.

This is the core of the so-called "smart leverage", which converts the difference between the market value of its own enterprise and the market value of its Bitcoin holdings into a capital operation advantage.

Fourth, why has MicroStrategy bought Bitcoin more aggressively in the past two months?

First, the conclusion may be that MSTR's stock price is very high.

MicroStrategy has significantly increased the scale of financing to buy coins in the past two months. In November and December 2024, MicroStrategy invested a total of $17.69 billion (63.8% of the total investment) through ATMs and convertible bonds, and purchased 192,042 bitcoins (43.2% of the total purchases). Only $3 billion of these were convertible bonds, and the remaining $14.69 billion were financed through ATMs.

Overall, the entire process of MicroStrategy's strategic allocation of Bitcoin has the characteristics of fixed investment in terms of time dimension; but in terms of quantity and amount, it seems that it is bought more aggressively in a bull market than in a bear market.

I can't understand this feature, and can only boldly guess that it may be because MSTR's stock price rose higher in a bull market. In August 2024, MSTR's stock price rose 3 times after the high dividend and transfer, and the stock price rose more than 4 times throughout the year, while Bitcoin rose only 2.2 times this year.

MicroStrategy's CEO talked about a beautiful "42B plan" in the Q3 2024 earnings conference call.

British writer Douglas Adams said in "The Hitchhiker's Guide to the Galaxy" that the supercomputer "pondered" the "ultimate answer to life, the universe, and all problems", and the result was 42.

MicroStrategy believes this is a magical number, so it proposed a 42B financing plan. 21 is also a magical number. The maximum total amount of Bitcoin is 21M. Therefore, MicroStrategy plans to issue 21B ATM + 21B Fixed Income in the next three years to continue to increase its holdings of Bitcoin.

Assuming that MicroStrategy eventually raises $42 billion through additional share issuance, assuming that the additional issuance is based on a share price of $330, the total share capital after the additional issuance will become 371.3 million shares. Assuming that MicroStrategy buys Bitcoin at an average price of 10wU, the company can increase 420,000 Bitcoins, bringing MicroStrategy's total holdings to 864,262 Bitcoins. At that time, the coin content per share will increase to 0.00233, an increase of about 29.4%. At this time, MSTR's total market value is $122.53 billion, and the total value of BTC held is 86.4 billion. In this case, the market value premium rate still exists.

5. After MicroStrategy, what other driving forces are there for Bitcoin to rise?

First, let me say the conclusion. In addition to the listed companies that bought Bitcoin driven by MicroStrategy, we can only think of more national strategic reserves, but we don’t have too much expectation in this bull market.

The main reasons for the rise of Bitcoin in this cycle are the following major buying forces:

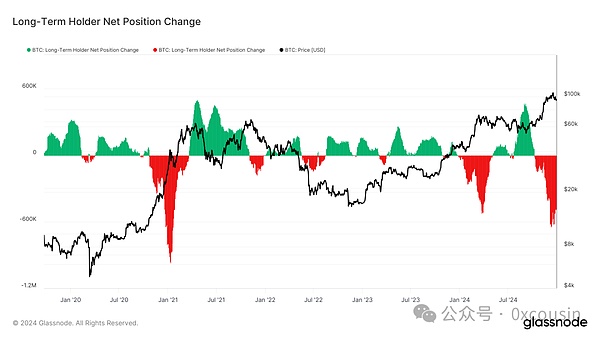

1. Long Term Holders who have a strong consensus on Bitcoin

There is no need for a reason for the long-term rise of Bitcoin, for BTCers, this is as natural as monkeys climbing trees and mice digging holes, because it is digital gold.

After Bitcoin fell below $16,000, the most mainstream Antminer S17 full series of mining machines were near the shutdown price, and Shenma M30S, Hippo H2, Antminer T19 and other mining machines have also fallen into the shutdown price range. In this price range, even if nothing happens, this rebound will happen. The bull-bear transition is like a basketball falling freely from a high altitude. After hitting the ground, there will be multiple rebounds that weaken in sequence.

Source: glassnode

As can be seen from the above figure, at the end of 2022, Long Term Holders continued to increase their positions.

After more than ten years of development, the Bitcoin consensus has become strong enough, and on-site existing investors and Long Term Holders have a consensus on the shutdown price of mainstream mining machines.

2. ETF brings incremental funds to the traditional financial market

Since the approval of BTC ETF, a total net inflow of 528,600 BTC has been recorded. In this round of bull market, ETF has brought nearly 36B incremental buying orders to Bitcoin and 2.6B incremental buying orders to ETH.

Source: coinglass.com

In addition, the passage of BTC ETF (and ETH ETF) will also have a driving effect, and more traditional financial institutions will begin to pay attention to and deploy in the field of Crypto.

3. MicroStrategy continues to buy, and many listed companies follow suit, Davis double-clicks

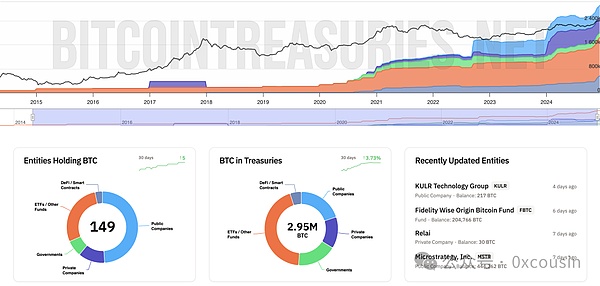

According to Bitcointreasuries data, as of December 30, 2024, 149 entities held a total of more than 2.95 million bitcoins. And this data is still growing rapidly in the near future.

Source: bitcointreauries.net

Of these entities holding Bitcoin, 73 are listed companies, 18 are private companies, 11 countries, 42 ETFs or Funds, and 5 DeFi protocols.

MicroStrategy is the first listed company to adopt the "Bitcoin Treasury Company" strategy, but it is not the only one. Marathon Digital Holdings, Riot Platforms, Boyaa Interactive International Limited and other listed companies have also implemented this strategy. But MicroStrategy still has the greatest impact.

4. National Strategic Reserves

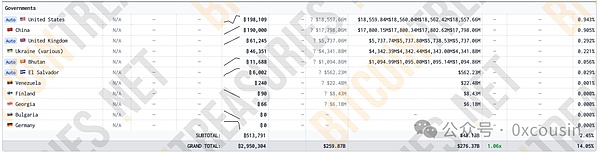

Currently, some governments already hold Bitcoin. The details are as follows:

Among these countries, I am afraid that only El Salvador is a real BTC Holder. El Salvador has been buying Bitcoin since 2021, buying 1 per day. So far, it has held 6,002 BTC, with a market value of over $560 million.

If there is any better driving force for the rise of Bitcoin after MicroStrategy, the first choice is to promote the US government's strategic reserve of Bitcoin after Trump takes office, and then drive more countries to strategically reserve Bitcoin.

MicroStrategy's Bitcoin strategy is not only a business experiment of corporate transformation, but also a major innovation in financial history. Through sophisticated capital operations, intelligent leverage, and deep insights into the value of Bitcoin, it has not only won a brilliant growth in its market value, but also pushed Bitcoin deeper into the vision of traditional finance, breaking the barriers between crypto assets and mainstream capital markets.

MicroStrategy's bold attempt may be just the prelude to the Bitcoin legend, or just a small step in the real rise of Bitcoin, but it may be a big step in the new era of finance.

Miyuki

Miyuki