Author: @13300RPM, @FourPillarsFP Researcher; Translator: Block Rhythm Xiao DeepEditor's Note: Ethena maintains a $5 billion market value stablecoin USDe with a team of 26 people. It hedges the volatility of assets such as ETH and BTC through delta neutral strategies, maintains a $1 anchor, and provides double-digit annualized returns. Its automated risk management and multi-platform hedging have built a moat and successfully responded to market shocks and the Bybit hacking incident. Ethena plans to push the circulation of USDe to 25 billion through iUSDe, Converge chain and Telegram applications, and become a financial hub connecting DeFi, CeFi and TradFi.

The following is the original content (the original content has been reorganized for easier reading and understanding):

Have you ever tried to eat hot noodles while riding a roller coaster? It sounds outrageous, but this is the best metaphor for what @ethena_labs does every day: it maintains a stablecoin (USDe) with a market value of $5 billion, always keeping the peg at $1, despite the volatility of the crypto market. And all this is achieved by a team of 26 people led by founder @gdog97_. This article will deeply analyze Ethena's unique secrets, reveal why it is difficult to replicate, and explain how Ethena plans to push the circulation of USDe to $25 billion.

Hedge against billions of fluctuations

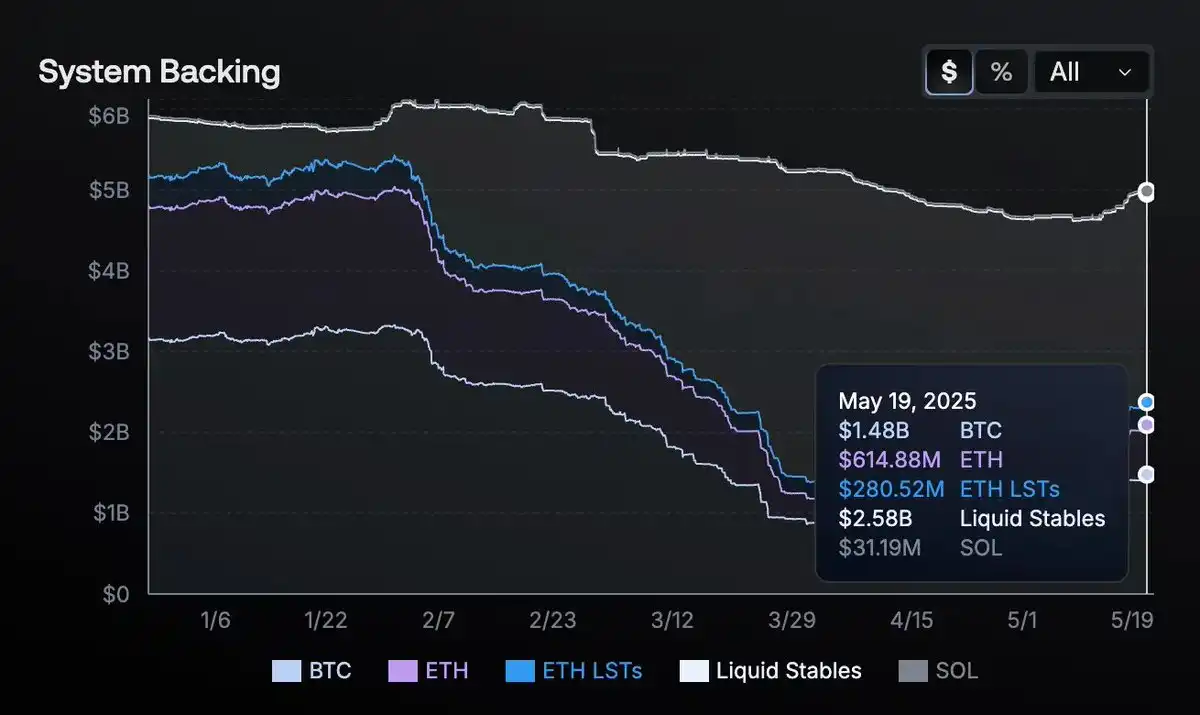

Stablecoins look boring on the surface: $1 is $1, right? But dig into the internal mechanism of Ethena and you will find that it is not simple at all. Instead of using dollars in banks as the backing for stablecoins, Ethena uses a strong portfolio of assets, including ETH, BTC, SOL, ETH LSTs (liquidity pledge tokens), and $1.44 billion worth of USDtb (a stable asset backed by U.S. Treasuries). These assets are continuously shorted in major derivatives markets to ensure that any fluctuations in the collateral price can be offset by the corresponding gains and losses of the short positions.

Source: Ethena Transparency Dashboard

If ETH goes up 5% and your hedge ratio is skewed, it could result in tens of millions of dollars in exposure. If the market crashes at 3 a.m., the risk engine must immediately rebalance collateral or close positions. There is very little room for error. Yet, Ethena managed billions in daily hedges in the roller-coaster market of 2023-2024 without a single crash (no decoupling, no margin call, no funding shortage).

During the Bybit hack, Ethena remained solvent without any collateral loss. Traditional hedge funds might need a whole floor of analysts and traders to deal with this volatility, but Ethena did it with just a lean team and zero mistakes.

Within months of its launch, Ethena became the largest counterparty to several centralized exchanges. Its hedging transactions even affected liquidity and order book depth, but few people noticed because stablecoins "just work."

About high yields: Ethena offers double-digit annualized returns when the market is bullish. At first, this is reminiscent of Terra/LUNA and its 20% Anchor fiasco. But the difference is that Ethena's returns come from real market inefficiencies (staking rewards plus positive perpetual contract funding rates, etc.), not minting tokens or unsustainable subsidies.

How Ethena's Delta Neutral Magic Works

When a user deposits $1,000 in ETH, they can mint about $1,000 in USDe. The protocol automatically opens a short futures position. If the ETH price falls, the short position makes a profit, offsetting the loss of collateral; if ETH rises, the short position loses money, but the collateral increases in value. The end result is that the net USD value remains stable. At the same time, when the perpetual contract market is over-leveraged in the long direction, Ethena (holding shorts) can collect funding fees, thereby providing double-digit APYs for USDe in bullish conditions without fiscal subsidies.

Ethena disperses these hedges across Binance, Bybit, OKX, and even some decentralized perpetual contract protocols to avoid the risks and margin restrictions of a single exchange. A recent governance proposal showed that Ethena plans to include Hyperliquid in the hedging portfolio and conduct short trades in the most liquid markets. By dispersing short positions, Ethena reduces its dependence on a single platform and further enhances stability.

Source: Ethena Transparency Dashboard

To cope with constant adjustments, Ethena deploys automated robots that work in conjunction with the trading team (similar to high-frequency trading systems) to continuously rebalance the entire multi-platform ledger. This is why USDe can remain anchored no matter how volatile the market is.

Finally, the protocol is overcollateralized to handle extreme drawdowns and can pause minting in unsafe conditions. Custody integrations (Copper, Fireblocks) allow Ethena to control assets in real time rather than leaving them in an exchange’s hot wallet. If an exchange goes bankrupt, Ethena can quickly withdraw collateral, protecting users from a single point of failure.

Solid Moat

Ethena’s approach seems replicable on paper (hedge a few crypto assets, collect funding fees, profit), but in practice, the protocol has built a strong moat that deters copycats.

A key barrier is trust and credit lines: Ethena hedges billions through institutional trading with custodians and major exchanges (Binance Ceffu, OKX). Most small projects don’t have easy access to these institutions, and negotiating minimum on-exchange collateralization requirements for multi-million dollar short positions requires institutional-grade rigor in legal, compliance, and operations.

Equally important is multi-platform risk management. Splitting large hedges across multiple exchanges requires real-time analytical capabilities that rival those of Wall Street’s quantitative trading teams. Yes, anyone can replicate delta hedging at a small scale, but scaling to $5 billion (and rebalancing huge amounts of collateral 24/7 across multiple platforms) is another level. The complexity of the required analytics, automation, and credit relationships grows exponentially with scale, and new entrants can hardly catch up to Ethena’s scale overnight.

At the same time, Ethena does not rely on perpetual free returns. If perpetual contract funding rates turn negative, it will reduce short positions and rely on staking or stablecoin returns. Reserve funds can buffer against long-term negative funding rate periods, while many high-yield DeFi protocols collapsed when the music stopped.

Ethena further reduces counterparty risk by not holding all collateral directly on a single exchange; instead, assets are stored at custodians. If a trading platform becomes unstable, Ethena can quickly close positions and move collateral off-exchange, ensuring minimal risk of catastrophic failure.

Finally, Ethena’s performance during extreme volatility strengthens its moat. USDe has not experienced a single decoupling or crash during months of intense market volatility. This reliability has driven new user adoption, listings, and top brokerage deals (from Securitize to BlackRock and Franklin Templeton), creating a trust snowball effect that cannot be replicated. The gap between talking about delta hedging and delivering 24/7 at billion scale is what makes Ethena stand out.

The Road to 25 Billion

Ethena’s growth strategy relies on a self-reinforcing ecosystem where the currency (USDe), network (“Converge” chain), and exchange/liquidity aggregation evolve in parallel. USDe was launched first, driven by crypto-native demand from DeFi (Aave, Pendle, Morpho) and CeFi (Bybit, OKX). The next phase involves iUSDe, a compliant version suitable for banks, funds, and corporate treasuries. Even if only a small portion of the huge bond market in traditional finance (TradFi) flows into USDe, it could push the circulation of stablecoins to 25 billion or more.

What drives this growth is the arbitrage between on-chain funding rates and traditional interest rates. As long as there is a significant yield gap, funds will flow from low-interest rate markets to high-interest rate markets until equilibrium is reached. As a result, USDe becomes a hub connecting crypto returns to macro benchmarks.

Source: Ethena 2025: Convergence

At the same time, Ethena is developing a Telegram-based application to bring high-yield US dollar savings to ordinary users through a user-friendly interface, introducing hundreds of millions of users to sUSDe. On the infrastructure side, Converge Chain weaves together DeFi and CeFi tracks, and each new integration will bring cyclical growth to USDe's liquidity and utility.

It is worth noting that sUSDe's returns are negatively correlated with real interest rates, and when the Federal Reserve cut interest rates by 75 basis points in the fourth quarter of 2024, the funding yield jumped from about 8% to over 20%, highlighting how falling macro interest rates can fuel Ethena's yield potential.

This is not a slow, phased advancement, but a cyclical expansion: wider adoption enhances USDe's liquidity and yield potential, which in turn attracts larger institutions, driving further supply growth and a more solid anchor.

Looking Ahead

Ethena is not the first stablecoin to promise high returns or position itself as an innovative approach. The difference is that it has delivered on its promise, keeping USDe firmly anchored at $1 during the most violent market shocks. Behind the scenes, it operates like a high-level institution, shorting perpetual futures and managing pledged collateral. However, what ordinary holders experience is a stable, yielding dollar that is simple and easy to use.

Scaling from 5 billion to 25 billion is not easy. Greater scrutiny from regulators, greater counterparty exposure, and potential liquidity crunches may bring new risks. However, Ethena's multi-asset collateral (including $1.44 billion in USDtb), powerful automation, and robust risk management show that it is better equipped to cope than most projects.

Ultimately, Ethena demonstrates a way to navigate crypto market volatility with a delta-neutral strategy at an astonishing scale. It outlines a future vision: USDe will be at the heart of every financial sector, from the permissionless frontier of DeFi, the trading desk of CeFi, to the massive bond market of TradFi.

Catherine

Catherine