Author: Despread; Compiler: Shenchao TechFlow

1. Introduction

From Since the second half of 2023, the approval of the highly anticipated Bitcoin spot ETF has become a reality, resulting in a large influx of institutional funds. As a result, Bitcoin prices are back at four-year highs for the first time since November 2021. During this period, trading volume on centralized exchanges like Binance and Upbit exceeded $1 trillion, and the popularity of CEX mobile apps increased, indicating increased market participation among individual investors.

In addition, there has been an increase in investors withdrawing assets from CEX to use them to earn interest on digital assets in decentralized finance or receive airdrops. . This has resulted in the total value locked (TVL) in the DeFi space doubling compared to the second half of last year.

Amid these developments, the TVL of EigenLayer, which is based on the Ethereum network, has increased approximately tenfold from the beginning of 2024 to the present, quickly rising to the top of the total TVL ranking of DeFi protocols. the third. The significant growth of TVL has had a profound impact on the rise of TVL in the DeFi field.

EigenLayer shares security with other protocols by proposing a re-staking feature that leverages ETH staked for Ethereum network verification while providing additional benefits to protocol participants. Interest. Thanks to its proposal, which aims to maximize the efficiency of Ethereum network capital and security, EigenLayer attracted approximately $160 million in investment from crypto VCs including a16z.

In addition, through the effective use of various point systems, which has become an important part of airdrops, it also increases investor expectations. EigenLayer’s TVL has been on a straight-line upward trend year-to-date through various derivative protocols that take the points system to its extreme.

This article will cover the overall aspects of EigenLayer, while focusing on the synergies created by the various derivative protocols and EigenLayer.

2. What is EigenLayer

In the Ethereum network from Proof of Work (PoW) After the consensus mechanism was converted to Proof of Stake (PoS), approximately 980,000 Ethereum verification nodes pledged 32 ETH each on the beacon chain to participate in network verification. In PoS, the value staked in the network is directly tied to the security of the network, meaning approximately 31 million ETH are ensuring the reliability of the Ethereum network. Ethereum’s decentralized applications (Dapps) can deploy smart contracts on the Ethereum network, thereby sharing its trust and security.

However, protocols known as Active Validation Services (AVS), such as bridges, orderers, and oracles, face problems when using only the functionality of the Ethereum network major challenges. This is because they act as intermediaries between chains or require faster synchronization times than the Ethereum network can provide. Therefore, these AVS are faced with the task of establishing their own trust network in a decentralized manner and need to have their own consensus mechanism in the process.

AVS, which is eager to establish its own trust network through a PoS structure similar to the Ethereum consensus mechanism, encountered several problems in the process of launching the network:

Lack of ways to promote the project and attract stakers

- < p style="text-align: left;">Stakers usually need to purchase the native tokens of the AVS network. These tokens are often volatile and difficult to obtain, resulting in reduced accessibility compared to ETH

AVS must provide an annualized yield (APY) higher than ETH to attract stakers, because stakers give up other asset management opportunities to participate in network verification, Thus bearing a higher cost of capital

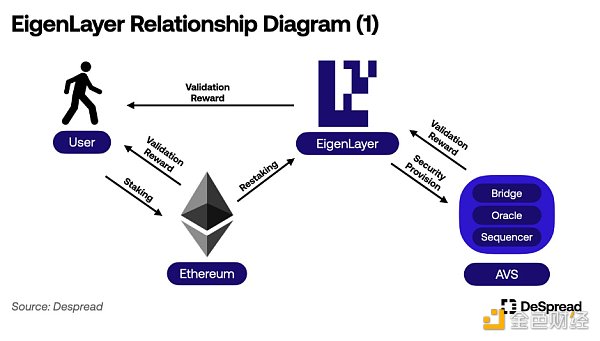

EigenLayer solves these problems with a feature called re-pledge, which allows The ETH pledged on the Ethereum beacon chain is again used to participate in AVS verification. Re-staking offers re-stakers the opportunity to participate in AVS network validation and earn additional validation rewards without purchasing other network tokens, using ETH or LST. For AVS, EigenLayer aims to provide an environment where they can promote their projects and build a network of trust based on the liquidity of re-stakeholders recruited through EigenLayer.

2.1. Exploiting the security of Ethereum through re-staking

Currently, if a validator on the Ethereum network takes actions that endanger network security, they may be Cut 16 ETH out of 32 ETH staked. If their staked ETH falls below 16 ETH, they will lose validator status. This means that if there was a way to use pledged liquidity as collateral, it would be possible to leverage up to 16 ETH pledged elsewhere and continue to participate in Ethereum network validation as long as the pledge balance remains above 16 ETH.

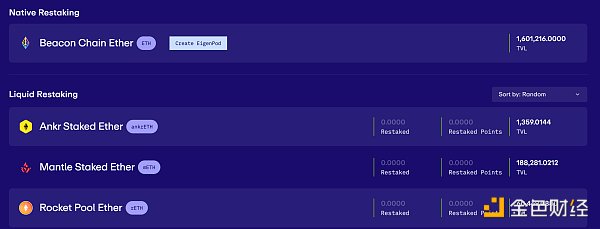

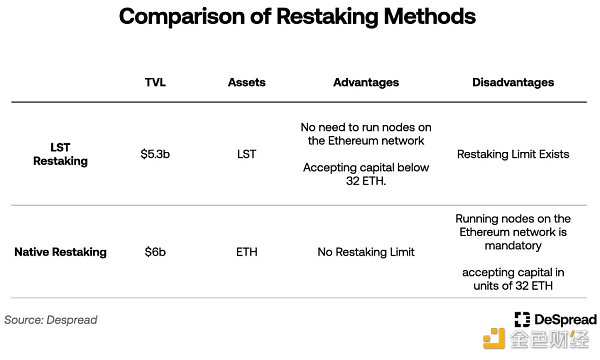

Re-staking in EigenLayer refers to utilizing validators to pledge the idle portion of ETH as collateral by exposing it to the slashing criteria of AVS using the PoS consensus algorithm , and utilize it for verification to provide security. Currently, EigenLayer supports two re-staking methods: LST (Liquidity Staking Token) re-staking and local re-staking.

LST re-staking: Although it is called liquid re-staking in EigenLayer, this article will refer to it as LST re-staking to reduce confusion with the concepts introduced later.

2.1.1. LST repledge

LST (Liquid Staking Token) is a deposit certificate issued by the LSP (Liquid Staking Protocol) that connects depositors of ETH with entities operating Ethereum nodes on their behalf. LSP addresses certain limitations of staking on the Ethereum network, such as:

Allows users to use less Participate in Ethereum network verification with a capital of 32 ETH and receive verification rewards.

Allows the use of LST in DeFi protocols to generate additional income, or by selling LST on the market without waiting for the unstaking period, effective Land provides the same benefits as unstaking.

A well-known LSP, Lido Finance, currently has approximately 10 million ETH deposits. Many DeFi protocols have begun to adopt the LST issued by Lido Finance, stETH, as an asset that can be used in their protocols, making it an infrastructure within the Ethereum ecosystem.

EigenLayer provides a re-pledge function that involves depositing the Ethereum network deposit certificate LST into the EigenLayer smart contract and participating in AVS verification and exposing it to Penalty standards for the AVS network. This method is called LST re-staking.

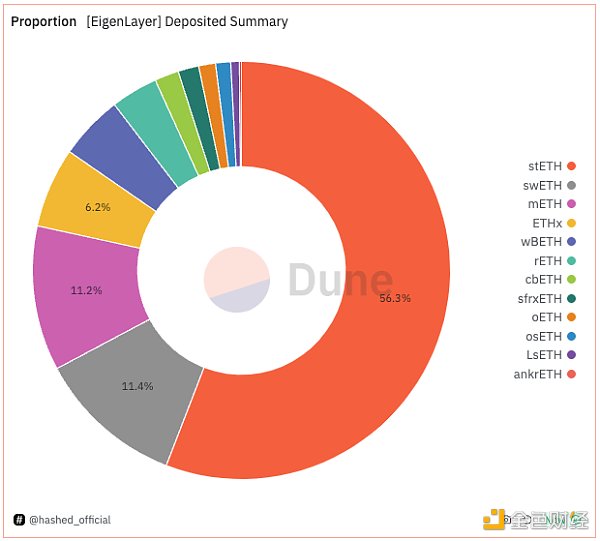

With its mainnet launch in June 2023, EigenLayer began to support re-staking of stETH, rETH and cbETH, and currently supports a total of 12 types of LST Pledge again.

The EigenLayer development team works hard to ensure the decentralization and neutrality of the protocol, achieving these measures by setting limits for each LST. These include only accepting LST re-pledge deposits during a specific time period, or limiting the incentive and governance participation rights that a single LST receives from EigenLayer to a maximum of 33%. EigenLayer’s LST restaking limit has been increased five times to date, with no further plans to increase deposit limits announced as of this writing.

2.1.2. Local re-stakingPledge

While LST re-staking involves using LST as collateral to participate in AVS verification, local re-staking is a more direct method in which Ethereum PoS node validators connect their ETH staked in the network to EigenLayer.

Ethereum node validators can participate in AVS verification by using their staked ETH as collateral. They accomplished this by setting the address that receives unstaking ETH to their own wallet address rather than the address of a contract called EigenPod, which was created through EigenLayer.

In other words, Ethereum network validators give up the right to directly receive their deposited ETH and participate in local re-staking to participate in AVS verification. This leaves their staked assets exposed not only to the Ethereum network’s penalty standards, but also to those of AVS, albeit with the potential for additional rewards.

Performing local re-staking requires staking 32 ETH and directly managing an Ethereum node, which provides a higher entry barrier compared to LST re-staking. However, it is not subject to LST re-staking restrictions.

2.2. Operator

After re-staking in EigenLayer, the re-stakeholder has two options: either run the AVS verification node directly, or convert it The re-pledged share is entrusted to the operator. Operators participate in AVS verification on behalf of re-stakers and receive additional verification rewards.

Operators grant penalty rights to the collateral they hold or entrust to AVS, install the software required for AVS verification, and then participate in the verification process. In return, they can collect a self-set fee from re-hypothecaters.

However, the process of sharing security with AVS is currently only running on the testnet. Therefore, at this moment, there are no operators or AVS in EigenLayer and restakers will not receive any additional verification rewards. Recently, EigenLayer mentioned that it has entered the final stage of preparations to launch the first AVS, EigenDA, on the mainnet and activate AVS verification in Phase 2.

To summarize, the relationship diagram of EigenLayer is as follows:

2.3. EigenLayer points

EigenLayer awards one EigenLayer point per hour for each ETH deposited by a re-stakeholder as a measure of contribution. Although the team has yet to clearly specify the purpose of the points or announce any details about the launch of the EigenLayer token, many users are re-staking in anticipation of a points-based airdrop when the token is eventually launched.

As of the time of writing, approximately 2.6 billion EigenLayer points have been distributed to all re-stakeholders, while on the OTC market, every EigenLayer point has been traded The price is $0.18.

This allows the market to estimate the expected value of the EigenLayer token airdrop to be approximately $440 million, which compares to Celestia’s value based on the price on the day of the airdrop, which is $1.2 billion, showing considerable market anticipation and interest in airdrops.

However, users who re-stake for the purpose of airdrop points face some inconveniences:

There are restrictions on LST re-staking, which prevents users from depositing the funds they want at will.

Local re-staking requires a capital of 32 ETH and involves running an Ethereum network node directly.

Re-staking freezes EigenLayer’s liquidity, forcing users to give up other opportunities to generate additional income.

Canceling and re-staking in EigenLayer to obtain bound liquidity requires waiting for a 7-day custody period.

To alleviate these disadvantages and make re-staking more efficient, the LRP (Liquid Redemption Protocol) emerged. Utilizing LRP for EigenLayer points has become a more attractive investment option for users.

3.LRP (Liquid RePledgeProtocol)

LRP accepts users’ ETH or LST deposits and re-pledges on EigenLayer on behalf of users. In addition, LRP issues LRT (Liquid Re-staking Tokens) as proof of deposited assets, allowing users to generate additional income by leveraging these LRTs in DeFi protocols, or sell them on the market, thereby bypassing the escrow period waiting for EigenLayer to cancel the re-staking to restore their deposits. LRP is structurally similar to LSP except that the assets are deposited into EigenLayer.

LSP (Liquid Pledge Protocol): a protocol used to replace Ethereum network verification

p>LST (Liquid Staking Token): issued by LSP to depositors as proof of principal amount

LRP (Liquid Redemption Protocol): a protocol used to replace re-staking on EigenLayer

LRT (Liquid Re-pledged Token): a certificate issued by LRP to depositors as a principal amount

In addition, most LRPs provide their own protocol points to depositors in addition to issuing EigenLayer points. Therefore, utilizing LRP offers several advantages over re-staking directly through EigenLayer, such as:

Create added value through the use of LRT.

Close the re-pledge position by selling LRT

Earn additional airdrops through protocol points

However, the EigenLayer points generated by re-staking through LRP are not The wallet address of the user who deposited the assets, but the ownership address of the LRP. As such, LRP promises to distribute any EigenLayer token airdrops it receives to its depositors and provide users with a dashboard to check the EigenLayer points they have accumulated through LRP.

In the next few sections, we will classify LRP based on two criteria and continue to explain in detail.

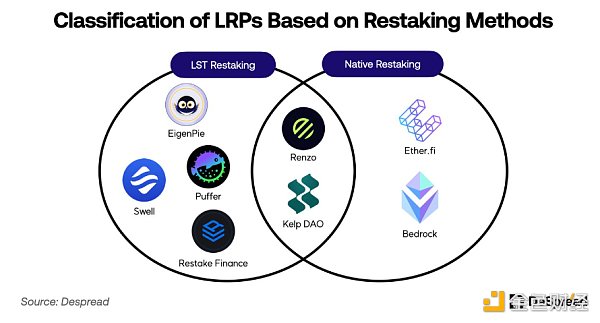

3.1. Classification of LRP based on re-pledge method

As discussed earlier, EigenLayer There are two re-staking methods: LST re-staking and local re-staking. These methods differ in the types of assets accepted for deposit and whether they involve operating an Ethereum network node.

LRP using the LST re-staking method can build its protocol through a relatively simple mechanism. They accept users’ LST, deposit it into the EigenLayer contract, and then issue equivalent value of LRT to depositors. However, they are directly affected by LST re-staking restrictions. Therefore, unless EigenLayer reopens LST for re-staking, the LST deposited during the restriction period will remain within the LRP protocol, and depositors will not accumulate EigenLayer points until their assets are re-staking.

On the other hand, LRPs that adopt the local re-staking method must directly manage and operate Ethereum network nodes because they accept ETH from users. This requires more work to build, operate and manage the protocol than LRP using the LST re-staking method. However, unlike the restrictions in the LST restaking method, there are no restrictions on local restaking, allowing depositors to start earning EigenLayer points immediately after depositing funds.

Based on these characteristics, LRP provides re-staking methods that fit their protocol concepts, and they do not necessarily need to adhere to one re-staking method. For example, Kelp DAO initially supported LST re-staking to quickly aggregate TVL after the launch of EigenLayer, and subsequently adopted a strategy of providing native re-staking functionality.

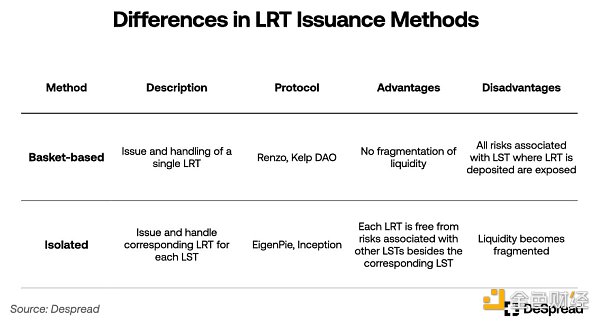

3.2. LRP classification based on LRT issuance method

In LRP that accepts various LST types or replaces a single asset with ETH and performs reinvestment, issuance LRT methods can be divided into basket-based and stand-alone methods.

The basket approach deals with a single type of LRT, with one LRT issued and paid regardless of the type of LST the user deposits into the LRP. Since it only handles one type of LRT, it is intuitive and easy to understand for users, and has the advantage of not distracting LRT liquidity. However, one drawback is that the entire LRP is exposed to the individual risks of deposited LST, and the LST deposit ratio within the LRP needs to be adjusted to protect against these risks.

On the other hand, the stand-alone method issues and pays for different LRTs corresponding to each LST processed by the LRP. This means that while it has the disadvantage of diversifying LRT liquidity, the risks associated with each LST are also isolated, eliminating the need to adjust deposit ratios.

Most LRPs adopt a basket approach, although a stand-alone approach carries less risk and is relatively easier to set up and operate. This approach is simpler for users and promotes cooperation with DeFi protocols.

In addition to these basic features, LRP also highlights its unique features and market entry strategies through various examples to attract users. Let's examine these aspects in more detail with some examples.

3.3. Explore noteworthy LRPs

3.3.1. Ether.fi

Ether.fi started out as an LSP with the concept of allowing stakers to have full control over their deposited ETH, and was the first LRP to support local re-staking following the launch of EigenLayer. This enables Ether.fi to provide its depositors with EigenLayer points farms through local re-staking, allowing them to continuously increase their TVL even during periods of restricted re-staking.

Ether.fi issues two types of LRT: eETH and weETH. eETH is the basic LRT obtained after depositing ETH to Ether.fi. It adopts a buy-back mechanism and the interest is reflected in the number of tokens. Repurchasing tokens adjusts the token balance in the holder's wallet when interest is paid, maintaining a 1:1 value ratio with the underlying assets. However, some DeFi protocols do not support this token mechanism. To enhance compatibility between LRT and DeFi protocols, Ether.fi offers the ability to wrap eETH into weETH, a reward-based token that reflects interest.

Ether.fi rewards LRT holders with EigenLayer points and its proprietary protocol points, ether.fi loyalty points. In order to reduce the selling pressure of LRT and expand its use, Ether.fi cooperates with various DeFi protocols to allow users to deposit LRT into DeFi protocols and continue to accumulate EigenLayer points. Ether.fi also hosts events to increase ether.fi loyalty points for users who use its LRT at DeFi events.

Users can use eETH or weETH to participate in various DeFi activities, such as:

In Decentralized exchanges such as Curve and Balancer provide liquidity to the weETH/WETH pool.

Provide weETH as collateral in lending protocols such as Morpho Blue and Silo.

Use weETH as collateral to issue over-collateralized stablecoins in protocols such as Gravita.

Use weETH in derivative protocols such as Pendle and Gearbox.

Through these activities, users can earn interest from DeFi protocols or use tokens obtained as LRT collateral. Earn EigenLayer and ether.fi loyalty points simultaneously. Ether.fi recently supported the bridging of LRT on Ethereum L2 Arbitrum and Mode Network, providing users with lower gas fees for using LRT in DeFi.

On March 18, Ether.fi announced the TGE of its governance token $ETHFI and a 6% of the total supply based on ether.fi loyalty points airdrop. The second quarter airdrop is scheduled to take place on June 30, and 5% of the total ETHFI supply will be allocated.

Currently, Ether.fi has the highest TVL among LRPs at approximately $3 billion, accounting for approximately a quarter of EigenLayer’s total re-pledge liquidity.

3.3.2. Kelp DAO

Kelp The DAO was originally a basket-based LRP that provided LST re-hypothecation for two assets, Lido Finance’s stETH and Stader Labs’ ETHx, and issued a single LRT, rsETH.

Initially, as the EigenLayer LST re-staking limit increased, a large number of users quickly filled the limit, but faced the inconvenience caused by high gas fees and time zone differences. In response, Kelp DAO proposed a solution where users can deposit their LST into the protocol and Kelp DAO will handle re-staking once the deposit limit is reached. Depositors will receive Kelp DAO’s proprietary protocol points, Kelp Miles, which has attracted a large user base. Like other LRPs, it designed its system to boost Kelp Miles when users use their LRT to participate in specific DeFi protocols, encouraging re-staking and LRT usage.

Kelp DAO has now added native restaking to its offering, offering depositors unlimited EigenLayer points earning activities. Similar to Ether.fi, it focuses on enhancing user convenience by offering restaking on the Arbitrum network, making it easier for users to hold and use their LRT in DeFi.

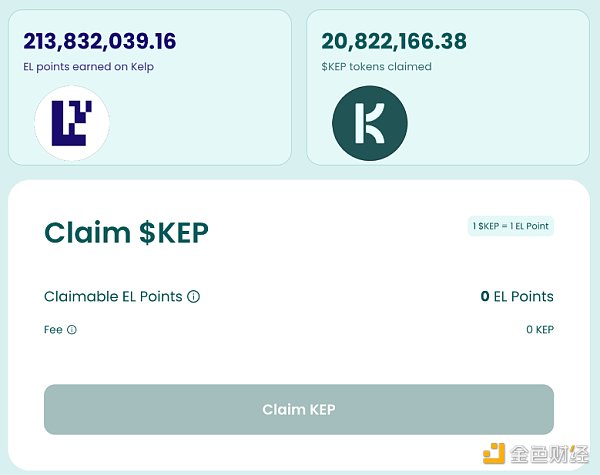

Additionally, Kelp DAO differentiates itself from other LRPs by enabling users to redeem their farm’s EigenLayer points for a token called $KEP .

Users can convert their accumulated EigenLayer points into $KEP tokens by paying a 0.5% fee. They can then sell these tokens on the market, monetize their EigenLayer points or provide liquidity on decentralized exchanges such as Balancer, thereby generating additional revenue and earning Kelp Miles. In addition, users who have not deposited assets with Kelp DAO can also purchase $KEP on the market, effectively receiving the same benefits as accumulating EigenLayer points through Kelp DAO.

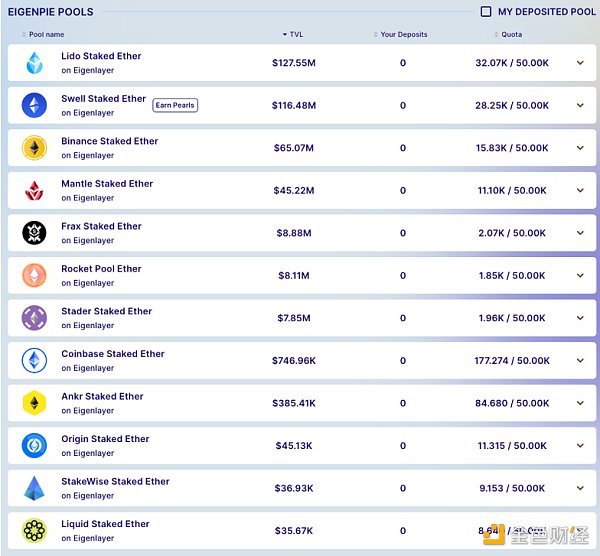

3.3.3. EigenPie

EigenPie is a sub-DAO launched by the MagPie ecosystem to aggregate governance currency, which has an important impact on DeFi protocol decisions, especially for EigenLayer. It supports the re-staking of all LST supported by EigenLayer and adopts an independent method to issue and distribute different LRT for each deposited LST.

Isolating the pools of each LST makes it easier for EigenPie to establish partnerships and carry out activities with specific LST protocols. For example, before launching its native re-staking feature, LSP Swell Network collaborated with EigenPie on a campaign to reward users who deposited its native LST, swETH, in EigenPie with Swell Network’s proprietary points.

EigenPie depositors can accumulate EigenLayer points and EigenPie points at the same time. Officials have announced that users who earn these points will have the opportunity to participate in the airdrop and IDO of its upcoming governance token $EGP.

However, EigenPie does not support local re-staking, making it limited to EigenLayer’s LST re-staking limit. In addition, since twelve types of LRT are issued, its liquidity is more fragmented compared to other LRPs, resulting in relatively less cooperation with DeFi protocols.

4. Leverage Points

LRP acts as an intermediary for re-pledge and provides LRT, Provide users with easy access to EigenLayer points. Additionally, by introducing their proprietary protocol points system and working with DeFi protocols to increase these points through events, they have attracted a large number of airdrop enthusiasts to the EigenLayer ecosystem.

However, when LRP first appeared, there was a lack of lending protocols that could cooperate with LRP to use LRT as a pledged asset. Therefore, users participating in protocol point enhancement activities can only farm EigenLayer points honestly based on the amount of LRT they hold.

Gravita is an over-collateralized stablecoin issuance protocol that allows users to issue stablecoins using Ether.fi’s weETH as collateral. Users can then leverage their positions through a so-called looping process – using stablecoins collateralized by LRT to buy and deposit more LRT, thereby earning more EigenLayer points. However, the Ethereum network’s high gas fees and Gravita’s minimum usage requirements (at least 2,000 stablecoins issued) create significant barriers to entry for many users trying to cycle.

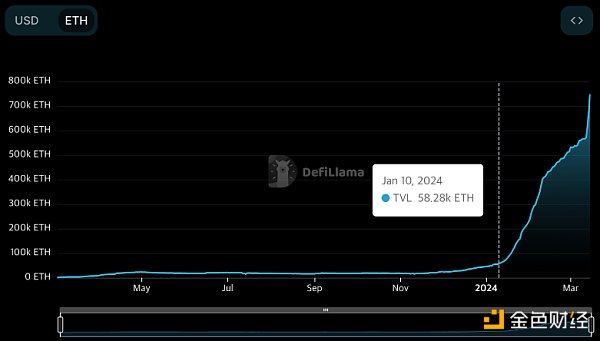

Things changed on January 10, 2024, when Pendle Finance began supporting Ether.fi’s eETH, allowing users to leverage points farms with a small amount of capital . This development has generated considerable interest among airdroppers who use Pendle Finance for EigenLayer points farming. As a result, EigenLayer and LRP saw significant growth in TVL.

4.1. Pendle Finance

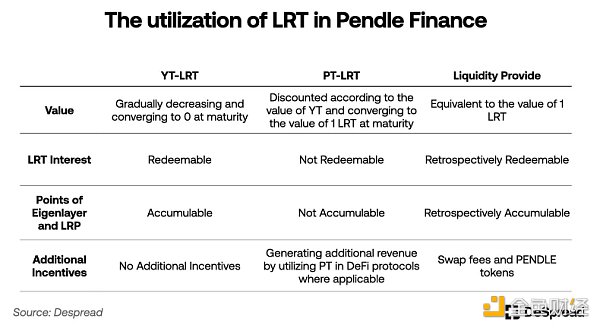

Pendle Finance is a DeFi protocol that allows trading of tokens with yields, such as LST and LRT, by setting a specific maturity date and splitting them into a principal token (PT) and a yield token (YT).

The total value of YT and PT is always equal to the value of the underlying assets, and YT holders have the right to claim accumulated interest from the beginning of holding to maturity. Therefore, as the expiration date approaches, the value of YT will tend to zero, while the market value of PT will discount proportionally as the demand for YT tokens increases.

Pendle Finance has partnered with Ether.fi to launch Ether.fi’s eETH as the first LRT available on its platform. Ether.fi has designed a system to distribute EigenLayer points and Ether.fi loyalty points to users who hold eETH’s YT token (YT-eETH). This enables users to purchase YT-eETH that is approaching expiration (which is getting cheaper) and accumulate interest and points up to that date.

The following is an example:

The above picture is based on the status of Pendle Finance eETH products as of the time of writing. The details are as follows:

The product expires on June 27, 2024, approximately 103 days from the date of writing.

eETH's 7-day average annualized return is 3.13%, and its current price is $3,872.

The price of YT-eETH is $196. If purchased at this value, the annual interest yield is -99.8%.

The price of PT-eETH is $3,676. If purchased at this value, the annual interest rate will be 20.02%.

As of the date of writing, the exchange ratio between eETH and YT-eETH is approximately 1:20. Ether.fi is running a campaign offering double Ether.fi loyalty points to users holding YT-eETH. Therefore, if a user exchanges one eETH for YT-eETH and holds it until maturity, he will receive the following interest and points:

Interest for holding 20 eETH

EigenLayer points for holding 20 eETH

EigenLayer points for holding 20 eETH

p>Ether.fi loyalty points equivalent to holding 40 eETH

However, since the value of YT-eETH will gradually drop to zero, all the holder can actually recover is the basic interest generated from 20 eETH. At current prices, this is approximately $640, approximately one-sixth of the $3,872 worth of one eETH, indicating that users are willing to bear this loss and participate in point farming activities by purchasing cheaper YT-eETH.

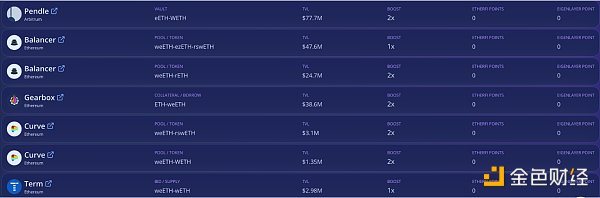

As the value of YT-eETH for points farming is highly valued, discounted PT-eETH has also become an attractive investment option, with an increased discount rate. Additionally, there has been an increase in demand to contribute LP to Pendle Finance’s eETH product trading pool as users seek to earn incentives. Currently, approximately one-third of all LRT issued on Ethereum is used by Pendle Finance.

Following its collaboration with Ether.fi, Pendle Finance continues similar collaborations with other LRPs, increasing the number of supported LRTs and adding support for EigenLayer via the Arbitrum network and LRT provide leveraged points farming. Recently, derivatives utilizing the undervalued PT-eETH as collateral appeared in Silo Finance, allowing Pendle Finance to benefit from the EigenLayer ecosystem, with TVL increasing approximately tenfold since the beginning of the year.

4.2. Gearbox

Gearbox is a leveraged income protocol that is different from traditional lending protocols such as Pendle Finance. Attract users' attention in different ways.

In Gearbox, borrowers must create a smart contract called a credit account before borrowing assets. They can then leverage their positions by depositing their pledged assets and borrowed assets from the protocol in a credit account. Borrowers can then conduct margin trading with leveraged spot assets through a credit account, powered by Gearbox, or participate in various DeFi yield farming opportunities such as Convex and Yearn Finance.

With this structure, Gearbox launched a leverage points strategy through cooperation with the LRP protocol. Gearbox allows EigenLayer points and LRP local points to be accumulated in credit accounts and sent to the borrower's wallet, providing users with up to 9x leverage points.

Gearbox Leverage Points Farm, Source: Gearbox

Gearbox provides a more intuitive UI/UX compared to Pendle Finance. Even users who are unfamiliar with DeFi can easily access the leverage points farm. In just three weeks since the launch of the leveraged points farm feature, Gearbox was able to increase TVL by approximately 5x.

5.Risks

Many people using the Ethereum network The deposited ETH is connected to each other as pledged protocols, forming a huge ecosystem. Currently, derivative protocols using LRP, LRT, and EigenLayer points are emerging, and there is much discussion about the growth potential of the EigenLayer ecosystem. However, many voices have expressed concerns about the potential risks of EigenLayer.

In the EigenLayer white paper, the basic risks associated with EigenLayer are outlined: collusion among operators providing AVS security to misappropriate AVS funds in this way ; Penalties due to unexpected vulnerabilities such as AVS programming errors. Improvements against operator collusion include implementing systems to monitor the possibility of collusion and diversifying operators by incentivizing them to focus on smaller AVS. Improvements to address unexpected penalties include a thorough AVS security audit and community veto power over penalties.

Even if the above risks are mitigated, there are still unobserved risks due to the delegation of staking to EigenLayer operators and the functionality that mainly provides AVS security. risk. In addition, when using LRT and its derivative protocols, there are additional risks that vulnerabilities in each protocol contract and oracle may be attacked. Furthermore, even a minor penalty from EigenLayer could lead to a significant chain of liquidations for over-borrowing LRT through derivative protocols.

Vitalik Buterin, the founder of Ethereum, also expressed concerns about EigenLayer by publishing an article titled "Don't Overload Ethereum's Consensus", implying that the verifier passed EigenLayer staked a social consensus attack on the possibility of a hard fork on the Ethereum network for its own benefit.

6.The future of EigenLayer

In the short term, EigenLayer is preparing to launch its first AVS, EigenDA, with a second phase update coming soon, which will allow secure sharing and re-earning on AVS.

Created by EigenLabs, the team behind EigenLayer, EigenDA is an AVS (Availability Security Sublayer) that leverages the security of EigenLayer to provide a data availability layer, not available here Independent consensus algorithm. Currently, several second-layer chains including Celo, Mantle, and Fluents have mentioned EigenDA as their data availability layer.

In addition, after the launch of the second phase of the mainnet, a third phase of testing is planned, which will allow security to be shared with other AVS besides EigenDA. Many well-known projects such as Ethos, Hyperlane, and Espresso are preparing to receive AVS security from EigenLayer after the launch of the third phase of the mainnet.

In this journey, whether EigenLayer will launch a token, and if so, what role the token will play in EigenLayer, and how many points will be accumulated What incentives will be offered to users is still uncertain. However, if EigenLayer continues with token airdrops, let us judge the mid- to long-term future of EigenLayer based on the author’s opinion.

6.1. EigenLayer’s token economics

Assets stored in EigenLayer are used to AVS security. Therefore, EigenLayer’s TVL indicator not only indicates how many assets are stored in EigenLayer, but can also be interpreted as the overall security index of AVS. However, after the airdrop, EigenLayer's TVL may be reduced as the airdroppers withdraw their re-staking liquidity.

Therefore, if EigenLayer were to announce plans for tokenomics, it would be possible to design tokenomics centered around maintaining the liquidity that has been re-staking so far, Attract more AVS based on this liquidity and encourage more re-staking to strengthen the network effect.

Especially at initial launch, it is expected that tokens will be offered as an additional incentive to diversify operations. In addition, when multiple AVS are registered with EigenLayer to receive security, EigenLayer tokens are expected to be distributed to operators and re-stakeholders who provide security for AVS as an additional incentive for risk diversification.

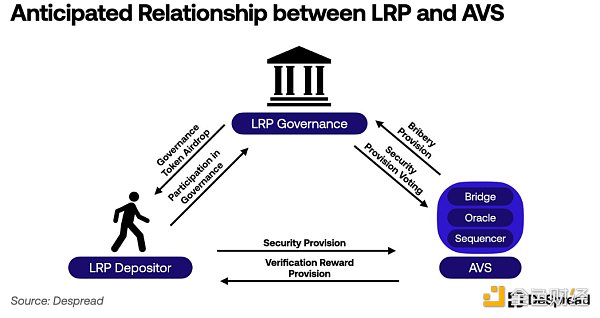

6.2. The relationship between LRP and AVS

< p style="text-align: left;">AVS may airdrop its own tokens to re-stakeholders to attract more security. AltLayer, the RaaS (Rollup as a Service) protocol that will become AVS on EigenLayer, has issued its own token $ALT and airdropped part of it to EigenLayer re-stakeholders.

In January 2024, protocols such as Dymension and SAGA announced the adoption of Celestia as their data availability layer and revealed plans to airdrop their native tokens to their investors $TIA, which results in doubling the number of $TIA in the network. Similarly, airdrops targeting restakers of AVS like AltLayer have the potential to drive restaking as a dominant narrative in the market after the EigenLayer token is launched.

Also, from an AVS perspective, promoting their AVS through LRPs, where re-hypothecaters and security options are numerous, can achieve greater results at a lower cost of capital, rather than committing to an unspecified majority Airdrop and carry out unilateral promotion. Therefore, expect an increase in various collaboration announcements between LRP and AVS. For example, Omni Network, which supports rollup inter-network messaging, has announced a partnership with Ether.fi and revealed that it has received approximately $600 million in staking support from Ether.fi. The announcement sparked anticipation for the Omni Network token airdrop among Ether.fi stakers.

In addition, LRPs are expected to attempt to systematize their interoperability with AVS through token economics. For example, the LRP might distribute governance tokens to re-stakeholders, allowing them to choose AVS that provide security. By using these governance tokens, users who vote on AVS may receive rewards in the form of AVS’s native token. This structure will strengthen incentive alignment between LRP re-pledgers, LRP governance token holders and AVS.

6.3. Evolution of LRT’s utility

Currently, most re-pledgers use LRT in DeFi protocols such as Pendle Finance to maximize point leverage, thereby Optimize their points farm in EigenLayer. However, the sustainability of the points system after the EigenLayer token is issued remains uncertain. However, as the expected value of EigenLayer points among re-stakeholders decreases, it may result in a decrease in the TVL that facilitates the leveraged points protocol.

However, LRT holds the potential to offer the highest interest rates after providing AVS security, and these rates may be higher than tokens pegged to the value of ETH. Therefore, DeFi protocols that previously used ETH or LST can provide users with higher returns by integrating LRT.

Currently, lending protocols like Morpho Blue and Silo Finance, as well as Gravita’s platform for over-collateralized stablecoin issuance, allow the use of LRT as collateral. Additionally, platforms like Whales Market facilitate OTC trading with weETH (Ether.fi’s LRT) as collateral. LRT’s utility is expanding, as evidenced by Ether.fi’s recent launch of Liquid functionality, which enables Ether.fi’s LRT to generate yield across various DeFi protocols.

LRP like Ether.fi and Renzo officially support LRT bridging and native re-staking on second layer networks such as Arbitrum, Mode Network and Blast, allowing DeFi protocols Adopt LRT as an asset on the second layer network. Additionally, Mitosis, a project that aims to become a liquidity hub for modular rollup networks, is working with Ether.fi to expand LRT’s interoperability on different chains.

6.4. Super Liquidity ReStaking

Going back to the re-staking area discussed earlier, the EigenLayer white paper introduces a method called super-liquidity re-staking, which exists in parallel with local re-staking and LST re-staking.

Super-liquidity re-staking involves providing liquidity to AMM DEX pools containing ETH and LST, such as Uniswap and Curve, and re-staking the obtained LP tokens to EigenLayer. This approach allows investors to both receive restaking rewards and earn interest from fees generated by the pool.

Although the possibility of EigenLayer supporting super-liquidity re-staking has not been officially mentioned in the white paper, this possibility is still open. If EigenLayer adopts this feature in the future, it could pave the way for various derivative protocols to emerge, creating another aspect of the ecosystem.

Vector Reserve is a protocol designed with super-liquidity re-pledge as its design concept. It provides various LRT and LST as liquidity to the DEX pool and issues To obtain the index token vETH backed by the value of LP tokens. Vector Reserve plans to enhance EigenLayer’s functionality after it starts supporting super-liquid re-staking.

7.Conclusion

EigenLayer has evolved from a simple The concept of sharing the security of the Ethereum network and generating additional revenue evolved to expand its ecosystem and meet the needs of infrastructure builders and investors, launching numerous spin-off projects. AVS like bridges and sequencers leverage Ethereum’s security to build their own network security, while investors see the potential to maximize ETH’s capital efficiency by leveraging LRT beyond LST.

Despite the high risk since EigenLayer-based AVS is not operational yet, many users still participate in re-staking to obtain points with no clear purpose. In addition, user interest in EigenLayer points has been accelerated through LRP and derivative protocols, allowing the capital in EigenLayer-supported LRT to be used to build a huge empire at this stage.

EigenLayer has certainly sparked interest and expectations in the infrastructure industry and crypto market, and as its mainnet launch becomes fully operational, it will be necessary to closely monitor whether EigenLayer It will bring a new DeFi Summer to Ethereum that some people are looking forward to, or as some people worry, it will increase the complexity of Ethereum and may lead to a chain collapse.

JinseFinance

JinseFinance