The tokenization of real-world assets (RWA) is no longer a futuristic narrative in the blockchain circle, but a financial reality that is happening. In particular, with the entry of financial technology giants such as Kraken and Robinhood, the structural change driven by blockchain technology has already begun. For the first time, global investors have the opportunity to trade "digital stocks" of companies such as Apple and Tesla 24 hours a day in a nearly frictionless way. However, under the hustle and bustle of the market, deeper questions need to be answered. Continuing from the previous article "From Retail Paradise to Financial Disruptor: In-depth Analysis of Robinhood's Business Landscape and Future Chess Game" Aiying Aiying's report aims to penetrate the surface of market hotspots and deeply analyze the internal logic of current mainstream stock tokenization products. We will no longer stay at the level of "what is it", but focus on "how to achieve it" and "what are the risks", providing our customers, investors, developers and regulators with a reference map that has both depth and practical value.

Aiying will conduct an in-depth comparative analysis with two typical cases - xStocks (issued by Backed Finance and traded on exchanges such as Kraken) representing the "open DeFi" path, and Robinhood representing the "compliant walled garden" path, supplemented by the practices of key industry players such as Hashnote and Securitize, to jointly explore a core question:

I. Core Analysis (I): The "Tightening Curse" and "Amulet" of Compliance - The Underlying Logic of the Two Mainstream Models

The primary challenge of stock tokenization is not technology, but compliance. Any attempt to "move" traditional securities onto the blockchain must face the complex global financial regulations. In the long-term game with regulators, the market has quietly differentiated into two completely different compliance paths: 1:1 asset-backed security tokens and derivative contract tokens. The underlying legal structure and operating logic of these two models are very different, which determines their product forms, user rights and risk characteristics. Let's disassemble them one by one.

Mode 1: xStocks - Embracing the open road of DeFi

Core definition:The tokens held by users (for example, TSLAX representing Tesla stocks) legally directly or indirectly represent the ownership or interest in real stocks (TSLA). This is an on-chain mapping of "real" stocks, pursuing the authenticity and transparency of assets.

Legal Framework and Market Performance

Aiying believes that xStocks' compliance design is ingenious. Its core lies in embracing the openness of blockchain while minimizing legal risks through multi-layered legal entities and a clear regulatory framework.

Currently, xStocks has supported 61 stocks and ETFs, 10 of which have been traded on the chain, showing initial market vitality. After being supported by Bybit and Kraken, its trading volume has experienced explosive growth. As of July 1, its daily trading volume has reached 6.641 million US dollars, with more than 6,500 trading users and more than 17,800 transactions.

Issuing Entity and Regulatory Framework:

xStocks is issued by a Swiss company, Backed Finance, and its operations comply with the Swiss DLT (Distributed Ledger Technology) Act. Switzerland was chosen as the legal base because the country provides a relatively clear and friendly regulatory environment for digital assets and blockchain innovation.

Special Purpose Vehicle (SPV):

This is the cornerstone of the entire architecture. Backed Finance established a special purpose vehicle (SPV) in Liechtenstein, which has a stable legal and tax environment. This SPV is like an "asset safe" whose only function is to hold real stocks. This design achieves keyrisk isolation: Even if the platform where the user trades (such as Kraken or Bybit) or the issuer has operational problems, the underlying assets held in the SPV are still safe and independent.

Asset Backing and Liquidity Strategy

In order to ensure the value and credibility of the tokens on the chain, xStocks has established a transparent asset backing and dual-track liquidity system.

1:1 Anchoring (1 coin = 1 share):

Each xStock token circulating on the chain strictly corresponds to a real share of stock held in a third-party custodian. This 1:1 anchoring relationship is the core of its value proposition. Currently, the total number of stock tokens of NVIDIA, Circle and Tesla has exceeded 10,000.

Issuance process:

Professional qualified investors can apply for a Backed Account and purchase stocks through Backed. Backed plays the role of a primary investor and purchases stocks from a brokerage firm, which are then held in custody by a third-party institution. Finally, xStocks mints the corresponding number of tokens based on the number of stocks purchased and returns them to the primary investors. These primary investors can issue and redeem stock tokens at any time.

Proof of Reserve:

Transparency is the cornerstone of trust. xStocks is integrated with the industry-leading oracle network Chainlink PoR. This means that anyone can query and verify Backed Finance's reserve vault in real time and autonomously on the chain, ensuring that the number of real shares it holds is sufficient to support all issued tokens.

Dual-track liquidity strategy:

Centralized Exchange (CEX) Market Makers:

On mainstream exchanges such as Kraken and Bybit, professional market makers are responsible for providing liquidity, ensuring that users can buy and sell xStocks as easily as trading ordinary cryptocurrencies.

Decentralized Finance (DeFi) Protocols:

xStocks' tokens are open, and users can deposit them into DeFi protocols on the Solana chain (such as lending platforms, DEX liquidity pools), provide liquidity themselves and earn returns. Currently, xStocks has cooperated with DEX aggregator Jupiter and lending protocol Kamino to make full use of the composability of DeFi and create additional value for assets. For example, the SP500 (SPY) token with the highest trading volume has reached US$1 million in USDC-based liquidity on the chain.

xStocks' ecosystem is composed of the issuer Backed, trading platforms Bybit and Kraken, and the underlying blockchain Solana.

Model 2: Robinhood - a "walled garden" with compliance priority

Core definition: Completely different from xStocks, users on Robinhood The stock tokens purchased on the platform are not legally stock ownership, but a financial derivative contract signed between the user and Robinhood Europe to track the price of a specific stock. Its legal essence is an over-the-counter (OTC) derivative, and the tokens on the chain are merely digital certificates of this contractual right. 1. Legal framework and technical implementation The Aiying team found that Robinhood's model is a very pragmatic "regulatory arbitrage", which cleverly packages the product into an existing financial instrument with a clear regulatory framework and deploys it quickly at a very low cost.

Issuing Entity and Regulatory Framework:

These tokens are issued by Robinhood Europe UAB, an investment firm registered in Lithuania and regulated by its central bank. Its products are regulated under the EU's MiFID II (Markets in Financial Instruments Directive II) framework. Under MiFID II, these tokens are classified as derivatives, thus circumventing more complex securities issuance regulations.

Low-cost and fast deployment:

Robinhood deployed 213 stock tokens on the Arbitrum chain at a total cost of only $5.35 (on-chain gas fees), demonstrating the extremely high efficiency of utilizing Layer 2 technology. Of these, 79 tokens have metadata set up, ready for subsequent trading.

Pioneering:

Robinhood boldly tried the first tokenization of private company stocks, launching OpenAI and SpaceX tokens, intending to seize the initiative in the high-value field of private equity. Currently, Robinhood has minted 2,309 OpenAI (o) tokens. (OpenAI tokens will provide investors with the opportunity to invest in OpenAI indirectly through Robinhood's ownership in the SPV, and then the price of OpenAI tokens will be linked to the value of OpenAI shares held by the SPV) 2. "Walled Garden" technology and compliance design Robinhood's technology implementation is closely linked to its compliance strategy, together building a closed but compliant ecosystem.

On-chain KYC and whitelist:

Through reverse analysis of the Robinhood stock token smart contract, community developers discovered that strict permission controls were embedded in its contract. Every token transfer operation triggers a check to verify whether the recipient's address is in the "approved wallet" registry maintained by Robinhood. This means that only EU users who have passed Robinhood KYC/AML can hold and trade these tokens, forming a "Walled Garden".

Limited DeFi composability:

A direct consequence of this “walled garden” model is that its stock tokens can hardly interact with the vast, permissionless DeFi protocols. The on-chain value of the assets is firmly locked inside the Robinhood ecosystem.

Future Plan (Robinhood Chain):

In order to better serve its RWA strategy, Robinhood plans to develop its own Layer 2 network, Robinhood Chain, based on the Arbitrum technology stack, showing its ambition to control the underlying technology.

Although Robinhood's model has found a compliance path under the EU framework, it has also caused considerable controversy and potential risks.

“Fake equity” storm:

The most representative events are the OpenAI and SpaceX tokens it launched. Soon after, OpenAI officially made a public statement denying its cooperation with Robinhood and clearly pointed out that these tokens do not represent company equity. This incident exposed the huge risks of the derivatives model in information disclosure and user cognition.

Centralization risk:

Users' asset security and transaction execution are completely dependent on the operating conditions and credit of Robinhood Europe. If there is a problem with the platform, users will face counterparty risk.

3. Comparison and summary of the two models

Through the above analysis, we can clearly see the fundamental differences between the two models. The xStocks model is closer to the open spirit of Crypto Native and DeFi, while the Robinhood model is a "shortcut" found within the existing regulatory framework.

Key Points

xStocks' path is"asset chain-in", which attempts to map the value of traditional assets to the blockchain world truly and transparently and embrace open finance. Robinhood's path is to "put business on the chain". It uses blockchain as a technical tool to package and deliver its traditional derivatives business. Aiying understands that this is essentially more like a blockchain upgrade of "CeFi" (centralized finance). 2. Core Analysis (II): The "Song of Ice and Fire" of Technical Architecture - Open DeFi and Walled Gardens Under the compliance framework, the technical architecture is the skeleton for realizing the product vision. Aiying believes that the differences between xStocks and Robinhood in technology selection and component design also reflect their two different philosophies of "open" and "closed".

1. Choice of underlying public chain: a triangular game of performance, ecology and security

Choosing which public chain to use as the "soil" for asset issuance is a strategic decision related to performance, cost, security and ecology.

xStocks chooses Solana:

Its core motivation is the pursuit of extreme performance. Solana is known for its high throughput (theoretical TPS is as high as tens of thousands), low transaction costs (usually less than $0.01), and sub-second transaction confirmation speeds. This is critical for stock tokens that need to support high-frequency trading and interact with complex DeFi protocols in real time. However, several network outages in history have also exposed its challenges in stability, which is a risk that must be taken when choosing Solana.

Robinhood chooses Arbitrum:

Arbitrum is Ethereum's Layer 2 expansion solution, and the logic behind its choice is "standing on the shoulders of giants." By adopting Arbitrum, Robinhood not only achieved higher performance and lower fees than the Ethereum mainnet, but more importantly, inherited Ethereum's unparalleled security, a large developer community, and mature infrastructure. In addition, Robinhood also announced plans to migrate to its own Layer 2 network based on Arbitrum technology in the future, which is specially optimized for RWA, which shows its ambition for long-term layout. Comparative analysis: This is not a simple question of "who is better", but a manifestation of a strategic path. Solana is a single chain that pursues "integrated high performance", while Arbitrum represents the path of "modularization" and inheriting Ethereum security. The former is more radical, and the latter is more robust.

2. Analysis of core technical components

In addition to the underlying public chain, several key technical components together constitute the core functions of stock tokenization products.

Smart Contract Design:

xStocks (SPL Token):

As the standard token (SPL) on Solana, its smart contract is designed to be freely transferable, similar to ERC-20 on Ethereum. This open design is the technical basis for its seamless integration with DeFi protocols (such as collateral on the Kamino lending platform).

Robinhood (Permissioned Token):

As mentioned earlier, its contract has transfer restriction logic embedded in it. Every transaction calls an internal whitelist registry for verification, which is the technical core of its "walled garden" model and the fundamental reason for its isolation from the open DeFi protocol.

The key role of Oracle (taking Chainlink as an example):

Price information:

The value of stock tokens needs to be synchronized with the stock price in the real world. Oracles (such as Chainlink Price Feeds) play the role of a data bridge, feeding stock prices from multiple reliable data sources to smart contracts in a secure and decentralized manner, which is the lifeline for maintaining price anchoring, executing transactions, and performing liquidations.

Proof of Reserves (PoR):

is crucial for 1:1 anchored products such as xStocks. Through Chainlink PoR, smart contracts can automatically and regularly prove to the outside world the adequacy of their off-chain reserve assets, solving the trust problem at the code level, which is far more timely and convincing than traditional audit reports.

Cross-chain interoperability (taking Chainlink CCIP as an example):

Value:

With the formation of a multi-chain landscape, the cross-chain capability of assets has become crucial. The Cross-Chain Interoperability Protocol (CCIP) allows assets such as xStocks to be securely transferred between different blockchains (such as from Solana to Ethereum). This can break the silos between chains, greatly expand the liquidity pool and application scenarios of assets, and is a key technology to realize the vision of "one token, universal for all chains". Backed Finance has mentioned the use of Chainlink CCIP in its products to achieve cross-chain bridging.

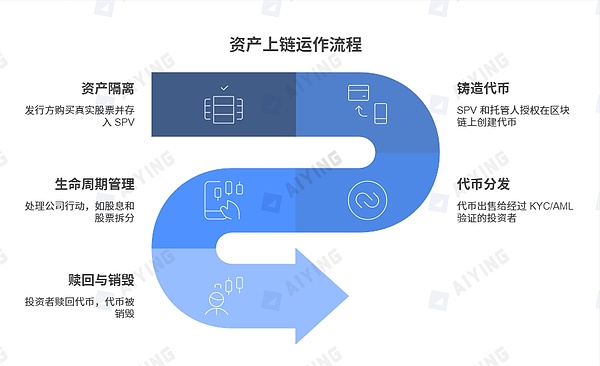

3. Detailed explanation of asset on-chain and SPV operation

For asset-backed tokens, SPV is the key hub connecting real-world assets and the blockchain world. Its rigorous and interlocking operating procedures ensure the security and compliance of assets.

Asset Isolation:

The issuer (such as Backed Finance) first purchases real stocks in a compliant financial market (such as the New York Stock Exchange). These stocks will not be placed on the issuer's own balance sheet, but will be deposited in an independent, regulated special purpose vehicle (SPV) and kept by a third-party licensed custodian (such as a bank).

Token Minting:

After the SPV and the custodian confirm that the real assets are in the warehouse, they will send a verified instruction to the smart contract on the chain, authorizing the minting of an equal amount of tokens on the target blockchain (such as Solana) (for example, if 100 shares of TSLA are deposited, 100 TSLAX tokens will be minted).

Token Distribution:

The minted tokens are sold through compliant exchanges (such as Kraken) or directly to qualified investors who have passed KYC/AML audits.

Lifecycle Management:

During the life of the token, the issuer needs to handle corporate actions through smart contracts and oracles. For example, when Tesla pays dividends, the SPV receives the dividends and triggers the smart contract to distribute the equivalent stablecoins or tokens to the on-chain holders. In the case of a stock split, the smart contract automatically adjusts the number of tokens for all holders.

Redemption & Burning:

When qualified investors wish to redeem, they send the on-chain tokens to the designated burn address. After verification by the smart contract, the SPV is notified. The SPV then sells the corresponding number of real shares in the traditional market and returns the cash received to the investors. At the same time, the on-chain tokens are permanently destroyed to ensure that the on-chain circulation and off-chain reserves always maintain a 1:1 balance.

III. Core Analysis (III): Business Model and Risk Assessment - The "Reef" Behind Opportunities

Behind the complex compliance and technical architecture is a clear business logic. The stock tokenization platform has not only created unprecedented value for users, but also opened up new profit channels for itself. However, opportunities and risks always go hand in hand.

1. Business model and profit source

Although all platforms provide stock token transactions, the profit models of different platforms have different focuses.

Robinhood's revenue sources:

Clear income:

According to its official description, Robinhood mainly charges a 0.1% foreign exchange (FX) conversion fee on transactions by non-Eurozone users. This fee is incurred when users use euros to buy dollar-denominated tokens.

Potential income:

Although it currently focuses on "zero commission" to attract users, its business model is scalable. In the future, it may introduce profit methods similar to its traditional US stock business, such as payment for order flow (PFOF, although it is strictly restricted in the EU), member value-added services for high-frequency traders, or income from the underlying assets held.

Exploring the private equity market:

By issuing tokens of non-listed companies such as OpenAI and SpaceX, Robinhood has expanded high-value asset categories. This is not only a powerful user acquisition strategy, but may also make profits in the future by charging for related value-added services (such as information and transaction matching).

xStocks (Kraken & Backed Finance)'s income sources:

Transaction fees:

As one of the core trading platforms, Kraken will charge a certain percentage of transaction fees to both buyers and sellers of xStocks. This is the most traditional profit model of the exchange.

Minting/Redemption Fees:

Backed Finance, as an issuer, mainly serves institutional clients. It may charge a certain service fee for large-scale minting and redemption operations performed by institutional users to cover the cost of purchasing, custody and managing the underlying assets.

B2B Services:

Backed Finance's core business model is to provide a one-stop asset tokenization (Tokenization-as-a-Service) solution for other financial institutions. xStocks is both its product and a demonstration of its technical strength.

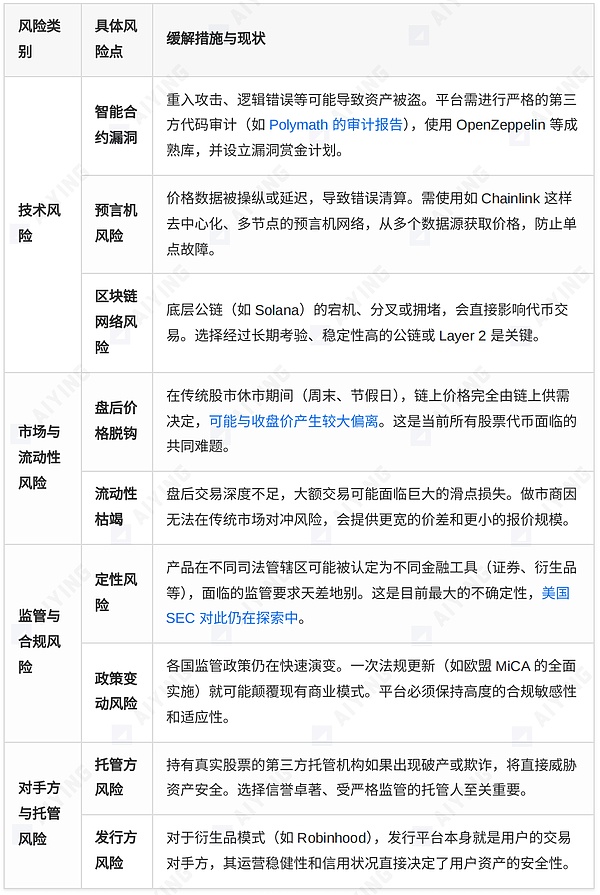

2. Comprehensive risk assessment matrix

While enjoying the convenience brought by stock tokenization, investors must be aware of the various risks hidden behind it.

3. Market structure and future prospects: Who will dominate the next generation of financial markets?

Major platforms in the asset tokenization track are competing for the market with different strategic positioning. Understanding their differences will help us gain insight into the future direction of the industry.

1. Comparison of the main player matrix

The RWA tokenization track has emerged in large numbers, and they have formed a distinctive competitive landscape based on different strategic considerations. We divide the main players into three camps for in-depth comparison.

2. Market trends and evolution paths

Looking to the future, stock tokenization and even the entire RWA track are showing several clear trends:

2. Market trends and evolution paths

Looking to the future, stock tokenization and even the entire RWA track are showing several clear trends:

list-paddingleft-2">

From isolation to integration:

Early tokenization projects were mostly isolated attempts within a single platform. Today, the trend is turning to deep integration with mainstream financial institutions (such as BlackRock, Franklin Templeton) and the vast DeFi ecosystem. Tokenized assets are becoming a bridge connecting TradFi and DeFi.

Regulation-driven innovation:

Regulatory clarification is the strongest catalyst for market development. The EU's MiCA Act, Switzerland's DLT Act, and the Monetary Authority of Singapore's "Guardian Plan" are all providing the market with clearer rules, which in turn encourages more compliance innovation. Compliance capabilities are becoming the core competitiveness of the platform.

Institutional entry and product diversification:

As BlackRock brings the trillion-dollar money market to the blockchain through its BUIDL fund, institutional participation will inject unprecedented liquidity and trust into the market. Product types will also expand from single stocks and bonds to more complex structured products, private equity and alternative assets.

Private equity tokenization has become a new blue ocean:

Platforms represented by Robinhood have begun to explore the tokenization of non-listed company stocks, which has opened a window for the private equity market that is usually limited to institutions and high-net-worth individuals. Although it faces huge challenges in valuation, information disclosure and law, it is undoubtedly a new direction with great potential.

Future Outlook and Thinking

The wave of stock tokenization is unstoppable, but the road ahead is not smooth. Several core issues will determine its final form:

Open vs. Closed Battle:

Will the future market be dominated by an open, composable model like xStocks, or will it be won by a compliant, but closed "walled garden" model like Robinhood? More likely, the two will coexist for a long time, serving user groups with different risk preferences and needs. Crypto Native users will embrace the open world of DeFi, while traditional investors may prefer to try it in a familiar, regulated "garden".

The race between technology and law:

Cross-chain technology (such as CCIP), Layer 2 solutions, and privacy computing (such as ZK-proofs) will continue to evolve to solve the current technical bottlenecks in scalability, interoperability, and privacy protection. At the same time, whether the global legal framework can keep up with the pace of technological innovation and provide certainty for these innovations will determine the development speed and ceiling of the entire industry.

Stock tokenization is far more than a simple "on-chain" of financial assets. It is fundamentally reshaping the issuance, trading, settlement, and ownership paradigms of assets. It promises a more efficient, transparent, and inclusive global financial market. Although this road is full of technical, market and regulatory "reefs", the future direction it points to is undoubtedly irreversible. For all market participants, whether investors, builders or regulators, the top priority is to actively and prudently embrace this coming financial revolution based on a deep understanding of its underlying logic and potential risks.

Preview

Gain a broader understanding of the crypto industry through informative reports, and engage in in-depth discussions with other like-minded authors and readers. You are welcome to join us in our growing Coinlive community:https://t.me/CoinliveSG

Aaron

Aaron

Jasper

Jasper Davin

Davin Hui Xin

Hui Xin Clement

Clement Brian

Brian Catherine

Catherine