Source: 10K Ventures

Since 2025, the blockchain industry has continued to face the challenges of low overall market sentiment and tight liquidity since Trump/Melania/Libra's coin issuance drained market liquidity, but we believe that the market's quantitative tightening has gradually entered the bottoming stage. Potential quantitative easing in the second half of this year may bring stronger liquidity to the market. We are particularly concerned about some high-quality altcoin projects with real application scenarios and revenue. We believe that these projects will be the first to highlight their value during the market recovery process, and it is worth continuing to maintain patience and confidence. At the same time, 10K FundⅠ 10 million US dollars of mixed strategy fund fundraising has been successfully completed and will be officially launched soon.

The transaction volume of the entire network in March was about 1.5T, which is half of the transaction volume in December. It is almost close to the transaction volume when the market was not good in the middle of last year, indicating that market sentiment has begun to be pessimistic and deeply bearish. The market rally brought about by the Trump trading atmosphere lasted only three months. The future growth of altcoins and mainstream coins still depends on interest rate cuts and quantitative easing.

Now we have summarized the industries in the blockchain industry that still have highly healthy cash flow:

Exchange

We will not elaborate on centralized exchanges, as everyone knows that this is a profitable industry. Although the competitive landscape of spot exchanges is basically finalized, there are still opportunities in the contract exchange market. This is because as a "private domain" industry, a considerable number of traders follow KOLs to follow orders. The KOL market is highly fragmented, and each community leader has his own private domain traffic. This leads to a situation where after a small perp cex/dex has secured a lot of KOLs in a small country, the exchange is still highly profitable, but the ceiling is relatively low and the profit is highly long-tailed.

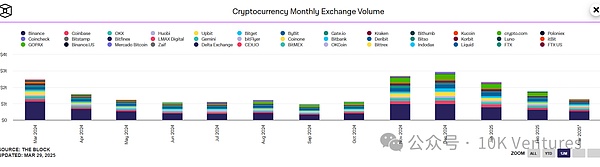

In the first quarter of this year, the market share of Binance and Bitget has increased significantly, while the market share of Bybit and Upbit has declined. This is also highly related to the business operations of the company - Binance was active in the first quarter. In addition to frequent Launchpool, Binance Alpha+Pancake IDO+Cex can use funds to buy dex tokens and other operations, which has brought Binance's market share back from the lowest point of 42% to 50%; the wealth effect of BG's launchpool+launchx still exists.

Due to the fact that Bybit’s 1.5 billion was hacked by a North Korean hacker group this year and South Korea’s Upbit was suspected of corruption and had its coin listing suspended, the market share of Bybit and Upbit dropped significantly in Q1 - Bybit’s market share dropped to 7%, less than half of last year’s high; Upbit’s market share was 7.36%, a drop of about 30%.

Broker

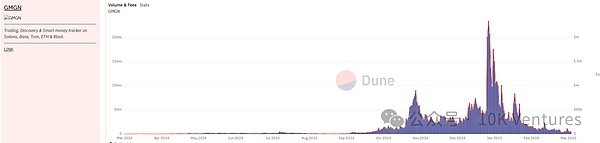

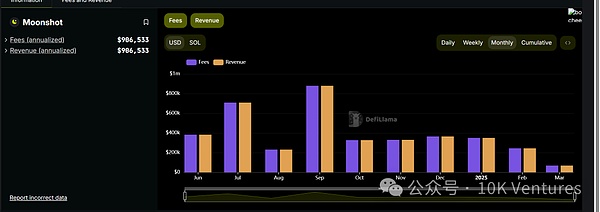

The brokers here are more like trading tools such as Moonshot and Gmgn. They combine token recommendation + trading bots, and do not do maker liquidity themselves, but only taker liquidity. The company's business model is more similar to the commission model of brokerage firms. Users are usually meme traders. They don't care about the 1% transaction fee, but they care more about the transaction speed and whether they can grab the token with wealth effect earlier. Benefiting from Trump's coin issuance craze, the first software for many new users is no longer Binance or Bybit, but Moonshot, because Moonshot has better meme trading and fiat currency deposit and withdrawal functions. Users can smoothly transfer US dollars to U, then trade gas-free, and then smoothly withdraw funds through OTC. The experience is highly similar to Futu and others.

Asset management

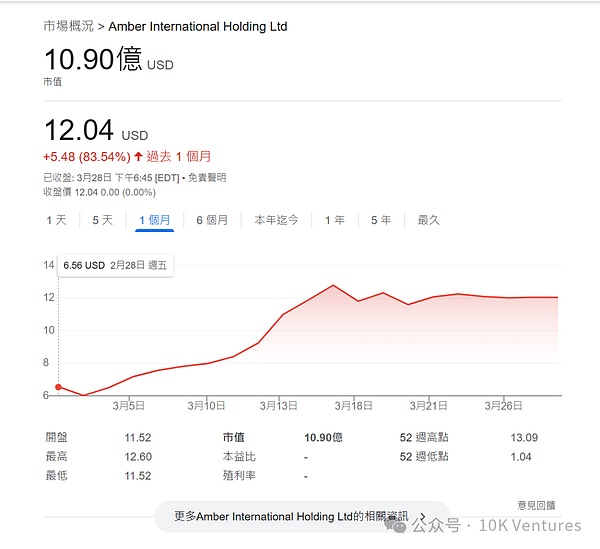

We will not elaborate on centralized asset management. But it is worth mentioning that Amber was listed on NASDAQ through SPEC, with a current market value of 1.1 billion US dollars, which is a significant adjustment compared to the last round of 3 billion US dollars at the beginning of 22 years; Matrixport's current AUM has reached 10 billion, making it the largest asset management company in Asia.

Stablecoin

Upstream and downstream payment + deposit and withdrawal

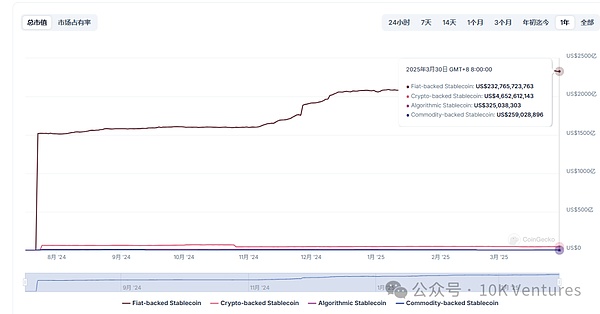

Stablecoin is nothing more than the hottest topic in 24-25 years. Show a set of data-the market size of the 25-year legal currency-collateralized stablecoin has reached 230 billion US dollars, an increase of 15% in the first quarter of this year. Even in a very bad market environment, stablecoin companies still maintain high growth.

In the traditional financial industry, the ceiling of payment is much greater than that of exchanges. For example, Visa's net profit in 24 years was 19.7 billion US dollars, more than 10 times that of Nasdaq or Hong Kong Stock Exchange. In 24 years, Binance's net profit is about 1 billion US dollars; Tether's net profit in 24 years is about 13 billion US dollars, of which Q4's net profit is 6 billion US dollars - in fact, it is easier to understand that most of the money in the world is used for payment, a medium amount of money is used for investment, and a small part of the money is used for gambling.

If Tether Circle does not make mistakes in the future and the supervision is friendly, then Tether's net profit will not be a big problem in the next one or two years.

The upstream and downstream of stablecoins mainly include deposit and withdrawal companies + payment companies, etc.

Among the deposit and withdrawal companies, the main leading players include moonpay and others. Moonopay is a deposit and withdrawal company founded in 2019. Its last round of financing was valued at US$3.5 billion. Its net profit in 2014 increased by 112% year-on-year, and its cash flow began to turn positive. The deposit and withdrawal track is the eternal theme of blockchain. As stablecoins become more and more compliant, the downstream deposit and withdrawal/OTC distributors of stablecoin issuers have begun to grow rapidly.

In addition to deposit and withdrawal companies, we are currently also looking at the growth potential of payment companies. Payment companies can be divided into B2B and B2C. The application scenarios of B2B mainly include helping cross-border/overseas companies to handle payments and collections and cross-border entity funds sorting; the application scenarios of B2C are mainly similar to U card payment and financial management.

web3 payment companies will be similar to web2 payment companies, with highly fragmented competition. It is easy for players to gain a certain share in the market, but it is difficult to have a monopoly on the market due to factors such as localization and compliance. This will cause certain difficulties for investment, but for business. The pure stable currency payment scenario is a low-profit, highly competitive track. But now it is in the early stages of the race to grab land. Finding customers + improving automation + using customer retained funds for asset management are the key competition points at present.

BSCEcosystem

Meme

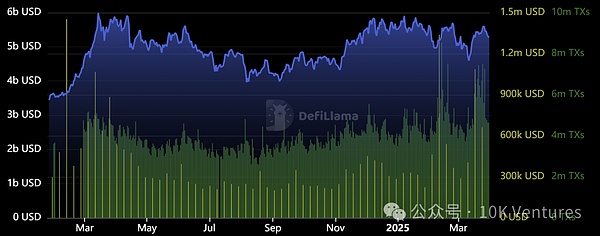

BSC ecology has taken over the outflow of funds from the Solana and Base ecology meme tracks. Although the overall TVL has not produced a substantial breakthrough, it is still high. Both the handling fee and on-chain transaction income have continued to increase in the short and medium term, with handling fee income and the number of transactions exceeding 1.2MUSD and 8M TXs respectively.

Blue is TVL, yellow is Revenue, and green is the number of transactions; Data source: DefiLlama

From the perspective of tracing back to the source, the main ecological projects that contribute to the entire BNB Chain are Pancake (DEX) and Venus (Lending).

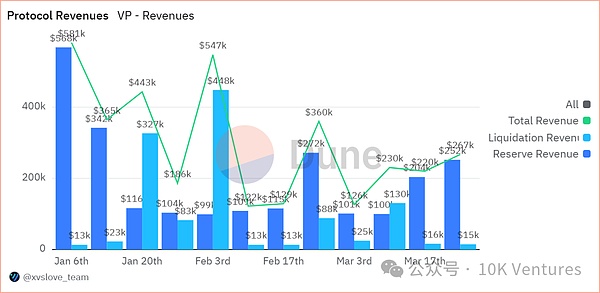

As the hub of the on-chain ecosystem, Pancake contributes of fees and income to the entire BNB Chain; the positive growth of Venus has become the second growth pole of BNB Chain, mainly due to the short-term lending demand caused by IDO.

The main boost to the BNB ecosystem comes from the founder's direct support for meme and the frequent launch of IDO on the Pancake chain. Solana and Base ecosystems have been hit hard by the celebrity coin effect, and users have lost confidence in the Solana ecosystem. BSC has become the center for taking over the lost traffic of meme. But BSC still has some shortcomings. The highest ceiling of the top token in the BSC meme season is about 180 million, which is much lower than the ceiling of 3-4 billion in the Solana meme season during the same period. Therefore, looking for on-chain Alpha in the BSC ecosystem is risky and has low returns. Choosing a suitable beta token is a relatively safe choice.

CAKE

In addition to BNB, the platform token CAKE of DEX Pancake is both relevant and cost-effective.

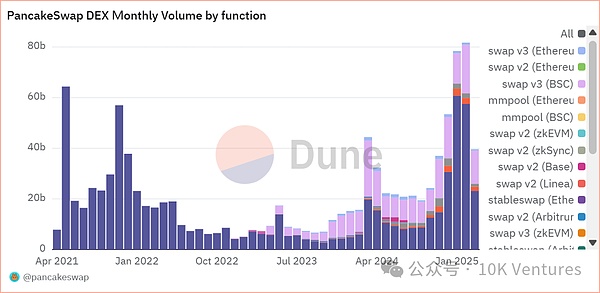

At present, the meme market of the BNB ecosystem is still in its early stages. It is still in the early stage of hype, with pure meme hype such as dogs, cats, and avatars as the main focus, and CZ/Yi He shouting orders as the main line. Similar to the Ethereum mainnet meme market in 23-24 when Musk changed his avatar and shouted orders. What can be expected in the future is the meme phenomenon of natural market trends (similar to Solana's Bome), which will transform from the founder's shouting to the market's spontaneous pmup, and then to AI and other on-chain products, which will reach a climax when mass entrepreneurship returns to ICO. It can be said that the market trend of the BNB ecosystem is a macro-reproduction of Solana's market trend, and a concrete reflection of the market's pursuit of certain opportunities. According to Raydium's highest market value of 2 billion, the market value of Pancake still has the potential to hit the previous high. The average monthly fee of Pancake AMM V3 is about 10 million. The transaction fee of Pancake Stable Swap has been close to zero since the last bull market, and the average monthly fee is 200K (up to 160 million at its peak)

In terms of token economics, according to bscscan, 1.685 billion CAKE have been destroyed, with a total release of about 2.058 billion, and about 290 million CAKE are currently in circulation. In its proposal in December 23, Pancake controlled the total supply to 450 million, ending the previous unlimited supply.

The other reason why CAKE is worth bullish is that CAKE has a strong shovel attribute. The market has released news that Pancake can use its own platform token to replace BNB to achieve on-chain IDO.

Name | FDV | TVL | Fees 7d | Revenue 7d | Volume 7d | FDV/Fees 7d |

PancakeSwap | $0.831b | $1.651b | $26.21m | $618m | $12.339b | 31 |

Uniswap | $6.13b | $3.988b | $11.89m | $0 | $9.524b | 515 |

Raydium AMM | $0.990b | $1.127b | $4.57m | $278,623 | $2.777b | 216 |

All DEXs are "leverage" of the ecosystem. Among the "leverage" packages, PancakeSwap has the highest cost-effectiveness. Among them, Uniswap and Raydium represent the Ethereum and Solana ecosystems respectively. They are both DEX "leverage" of the ecosystem, but both are expensive. Among them, the FDV/fees 7d of UNI and RAY are 17 times and 7 times that of CAKE respectively. In the case that the BSC ecosystem still has the potential to continue to grow, CAKE is the most "cheap" DEX platform coin.

How to find certainty in the uncertain encryption industry

In order to meet the needs of the market

In terms of the amount of financing, the market in March has increased significantly compared with the previous year; but in terms of the number of financing companies, it is a new low within a year - this is because there were many large mergers and acquisitions in this month and Binance was invested by MGX. Before there is a big innovation in the entire crypto market, the market will linger in "junk time". Mergers and acquisitions will be frequent, and companies with sufficient cash flow will continue to improve their business landscape. The biggest certainty comes from exchanges, securities companies, asset management, stablecoins and other markets with established application scenarios. Everyone needs to accept the fact that the business cycle of the crypto market is close to that of traditional industries and realize PMF and revenue as soon as possible.

Win with surprise

The best time to start a business is 2025, when the positive financing cycle of the primary market is broken, and the copycat bear market caused by the excessive supply of junk assets is in the brutal process of clearing out. The whole process may last until 26 years. When the negative cycle reaches the extreme, we will have the opportunity to see high-multiple primary opportunities, and high-quality start-up project opportunities will also be born. We can see that many high-quality entrepreneurs in this cycle have entered the market during this period and faced the wind and rain. We hope to always admire and support such entrepreneurs to the best of our ability. When consensus is no longer unified, opportunities emerge from the gaps.

Everyone is asking how to find certainty in the uncertain crypto industry. 10K's answer is to find and accompany those who have already started moving forward.

Weatherly

Weatherly