When it comes to the values of the crypto world, the concept of decentralization is the most well-known one. Tracing back to the source, the emergence of cryptocurrency was shortly after the bankruptcy of Lehman Brothers. Against the backdrop of the global turmoil caused by the currency crisis, Satoshi Nakamoto proposed the concept of decentralized currency, and Bitcoin was born, laying the foundation for the value belief of the crypto world. In the following not-so-long decade, the crypto ecosystem continued to expand and grow around decentralization, and the value belief and technical belief went from controversy to unification, and from unification to dispersion, and developed in the theory of value and price. But no matter how controversial it is, Bitcoin is the strongest value pillar in the crypto world. From miners to mines, from capital to institutions, despite the constant changes in the so-called "bankers" surrounding Bitcoin, the market firmly believes that no one can own more than 51% of Bitcoin, and recognizes it as a successful demonstration of decentralized currency. But in recent years, decentralized currency seems to have returned to the context of centralization. Since 2020, Wall Street institutions and listed companies have started a Bitcoin buying craze. Last year, the Bitcoin spot ETF was listed. Now, with the establishment of the US Bitcoin strategic reserve, it can be seen that institutional investors, listed companies, and even countries have begun to hold a large number of Bitcoins. This move has both advantages and disadvantages. The advantage is the high price. The injection of liquidity has successfully pushed Bitcoin to $100,000, which not only left a strong and colorful mark in the history of encryption, but also truly gave glory to Diamond Hand. Compliance has made the threshold for holders higher. Cryptocurrency has entered the mainstream for the first time. Speculators hiding in the dark have also turned gorgeously into value investors, and by the way, they have been labeled as emerging asset holders.

But the disadvantages are also obvious. Miners have gone behind the scenes, the linkage between the encryption market and the US stock market has become increasingly close, and independent market conditions are difficult to find. Any disturbance in the macro economy has stimulated the fragile nerves of the market. The current market is a good interpretation of this point. People's focus is either on the tariff war, the discussion of the US interest rate cut, or the list researchETF inflows and outflows, and the priority of technological progress is constantly recursively backwards. Compliance and regulation have not made the crypto market sunny. Instead, the president took the opportunity to reap the first harvest. Family MEME is in constant turmoil, and Defi and blockchain games also need to be caught up.

Combined with the above, the question is also emerging, who holds the most Bitcoin? Is the growing number of institutional investors a good thing for Bitcoin? As more and more BTC is locked in cold wallets, treasury bonds and ETFs, is the on-chain data losing reliability? In response to this issue, Matt Crosby, a reporter for Bitcoin Magazine, also conducted research, and his report is translated here for explanation, to explore whether Bitcoin's decentralized spirit is really at risk or just evolving.

New Whale

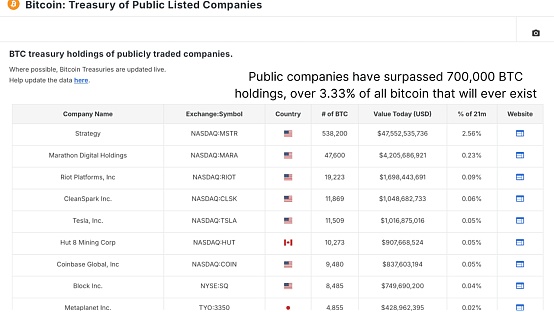

Start with the financial data of listed companies. In terms of data, large listed companies including Strategy and MetaPlanet have accumulated more than 700,000 BTC in total. Strategy is the undisputed leader among them. As of April 21, 2025, Strategy holds 538,200 bitcoins, with a total purchase cost of approximately US$36.47 billion and an average price of approximately US$67,766. In the past six months, it has acquired 379,800 BTC. Considering that the total supply of Bitcoin is capped at 21 million, this accounts for approximately 3.33% of the total future supply of BTC. Although this supply cap cannot be reached in the lifetime of current holders, the phenomenon it reflects is obvious: listed companies are making long-term bets.

Figure 1: Listed companies have the highest BTC holdings

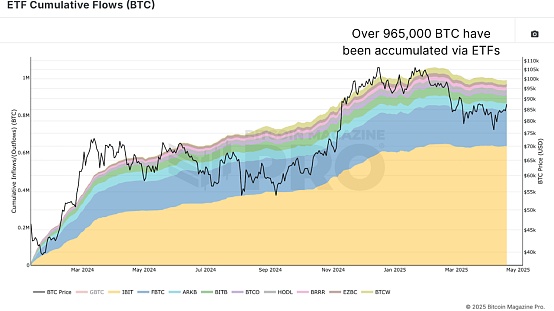

In addition to the Bitcoin directly held by enterprises,

throughEFT cumulative flow (BTC)It can be seen from the chart thatIfcorporate treasuries andETF holdings are combined, the number will climb to more than 1.67 million BTC, accounting for about 8% of the theoretical total supply, but this data is still more than that.

Figure 2: ETFs have stimulated institutional interest in BTC

In addition to Wall Street and Silicon Valley,in some regions and countriesgovernments are now

Extensivelyactive in the Bitcoin field. Through sovereign purchases and strategic Bitcoin reserves and other initiatives,regions andcountries hold a total of approximately542,000 Bitcoins. Combined with the previous institutional holdings, it can be concluded that the number of bitcoins held by institutions, ETFs and governments exceeds 2.2 million. On the surface, this accounts for about 10.14% of the total supply of 21 million bitcoins. The ForgottenSatoshi Nakamotoand Lost Supply

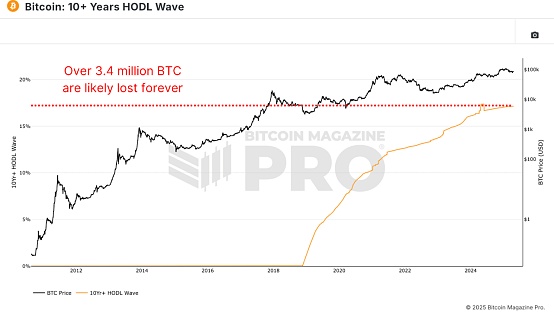

In fact, not all21 million BTCcan be accessed. According to the 10+ Year HODL Wave data, which measures coins that have not moved in a decade, more than 3.4 million BTC may have been lost forever, including Satoshi Nakamoto’s wallet, coins from early mining, and coins mined during the Cold War. leaf="">forged currencies, forgotten passwords, and even USB flash drives found in landfills.

Figure 3: It is conceivable that the number of lost BTC exceeds 3.4 million

There are currently about 19.8 million BTC in circulation, and it is estimated that about 17.15% have been lost, so the actual supply is close to 16.45 million. This completely changes the current balance, and the proportion of BTC held by institutions has risen to about 13.44% in terms of more actual supply. This means that about 1 in every 7.4 BTC on the market has been locked up by institutions, ETFs or sovereign states.

In this context, are institutions sufficientto control Bitcoin?

Fortunately, from the data, there is no such trend yet.

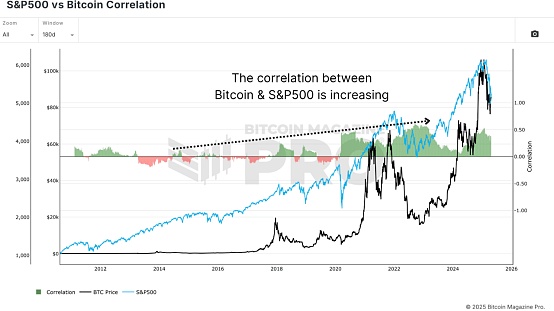

But it does indicate its growing influence, especially in terms of price action. Looking at the S&P 500 correlation chart with Bitcoin, the correlation between Bitcoin and traditional stock indices such as the S&P 500 or Nasdaq is clearly increasing. As these large entities enter the market, BTC is increasingly viewed as a “risk-on” asset, meaning its price tends to fluctuate with changes in investor sentiment in traditional markets.

Figure4: The correlation between Bitcoin and the S&P 500 index continues to strengthen

This will be relatively beneficial in a bull market,

leaf="">When global liquidity expands and risk assets perform well, Bitcoin is now poised to attract larger inflows than ever before, especially as pensions, hedge funds and sovereign wealth funds begin to allocate even a small portion of their portfolios. But there is also a trade-off. As institutional adoption deepens, Bitcoin's sensitivity to macroeconomic conditions will increase. Central bank policy, bond yields and stock volatility all begin to matter more than before. Despite these changes, more than85% of Bitcoin has not yet entered the hands of institutional investors. Retail investors still hold the vast majority of Bitcoin supply. ETFs and corporate vaults may have hoarded a large amount of Bitcoin in cold wallets, but the market remains highly fragmented.

In response, some industry critics

believe that the usefulness of on-chain data is waning. After all, if so muchBTC is locked in ETFs or idle wallets, can we still draw accurate conclusions from wallet activity? This concern is not groundless, but it is not new either. NewAdapt

Historically, the majority of Bitcoin’s trading activity has occurred off-chain, particularly on centralized exchanges like Coinbase, Binance, and

formerly FTX. These transactions rarely appear on-chain in a meaningful way, but still influence price and market structure. Today, markets face a similar situation, only with better tools. ETF flows, company filings, and even state purchases are subject to disclosure regulations. Unlike opaque exchanges, these institutional players typically must disclose their holdings, which provides analysts with a wealth of data to track. Moreover, on-chain analytics are not static. Tools like the MVRV-Z score are evolving. By narrowing the focus to the 2-year rolling average of the MVRV Z-score rather than the full historical data, it is possible to better capture current market dynamics without the impact of long-term lost tokens or inactive supply.

Figure 5: A more targeted 2-year rolling MVRV Z-score can better capture market dynamics

Conclusion

In summary, institutional investors' interest in Bitcoin is at an all-time high. Between ETFs, corporate bonds, and sovereign entities, there are more than 2.2 million bitcoins held and growing. This influx of money has undoubtedly had a stabilizing effect on prices during periods of market weakness. However, this stability has also brought some entanglements. Bitcoin's growing ties to the traditional financial system have also increased its correlation with stocks and broader economic sentiment. This does not mean the end of the era of Bitcoin decentralization or on-chain analysis. In fact, as more and more Bitcoins are held by identifiable institutions, the ability to track the flow of funds will become more precise. Retail investors still dominate, and on-chain and off-chain analysis tools are becoming smarter and more responsive to market changes. The spirit of Bitcoin's decentralization is not threatened, it is just maturing. As long as the analysis framework and Bitcoin can keep pace with the times and develop together, they will certainly be able to cope with the corresponding challenges in the future.

Catherine

Catherine