朝韩冲突升级引发市场担忧,亚洲“黑天鹅”将至?比特币或面临剧烈波动

朝鲜半岛紧张局势持续升级,韩军对军事分界线南侧进行警告射击,朝鲜则炸毁了连接两国的通路。币圈担忧,若战争爆发,韩国作为主要的加密货币市场,恐慌情绪可能引发比特币价格剧烈波动。

Alex

Alex

According to the report by a court-appointed examiner for its bankruptcy proceedings, the collapsed cryptocurrency lending platform Celsius Network had cheated customers since its foundation as a public company in the United States, which it allegedly created to avoid regulation in the United Kingdom.

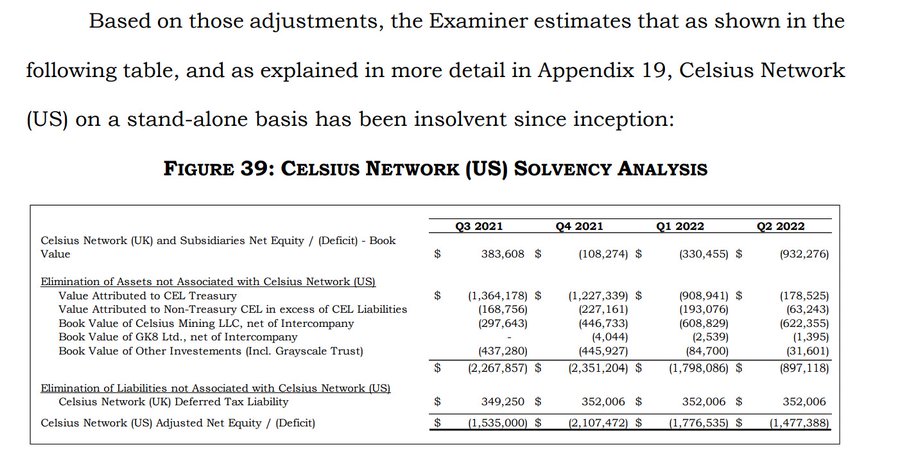

Indeed, Celsius U.S. “on a stand-alone basis has been insolvent since inception,” according to the solvency analysis by the U.S. examiner, shared in a Twitter thread by the speaker and writer on economics, finance, and monetary policy, Frances Coppola, on February 1.

Celsius U.S. solvency analysis. Source: Frances ‘Cassandra’ Coppola

Furthermore, the report found that the Celsius U.S. entity was founded in August 2021, after the U.K.’s financial watchdog Financial Conduct Authority (FCA) denied Celsius Network U.K. a license and ordered it to cease selling to retail customers in the country.

Complicated connections

The examiner also drew attention to the intercompany accounting between the two entities, which Coppola said was “convoluted to say the least, and includes bizarre ‘loans’ and equity transfers rather similar to those in the Celsius-AMV (Equities First) arrangement” that she discussed earlier.

What AMV and Celsius actually did was write off their claims on each other arising from the incomplete ICO. But for some reason that I do not understand, both sides recorded these write-offs as secured loans.

— Frances 'Cassandra' Coppola (@Frances_Coppola) February 1, 2023

As the economist explained, Celsius U.S. was created to circumvent U.K. regulation, as internal accounting never distinguished between the two entities, instead viewing them on a consolidated basis, adding that she didn’t think “they ever had the slightest intention of creating a standalone US entity.”

According to the above table from the examiner’s report that Coppola shared, “significant parts of Celsius’s business, including its Treasury (and all its retained CEL tokens), its mining business and GK8, remained with the U.K. entity,” she stressed.

No accounts filed in two years

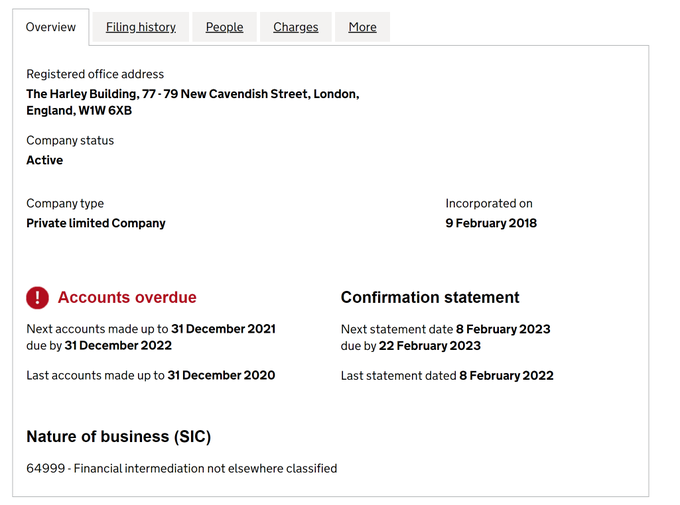

On top of that, Celsius’s U.K. branch showed no accounts filed since December 2020 on the website of Companies House, the executive agency sponsored by the Department for Business, Energy & Industrial Strategy, which registers information about companies in the U.K. and makes it available to the public.

Information on Celsius U.K. Source: Companies House

As it happens, the Companies House webpage for Celsius Network U.K. indicates that its accounts were significantly overdue, considering that it was supposed to file its 2021 full-year accounts by December 31, 2022, as Coppola observed.

Meanwhile, Celsius faced scam allegations from the crypto community after it unveiled a plan to exit the bankruptcy by rebranding itself into a publicly traded recovery corporation, which also involves giving creditors with locked assets above a certain threshold a token called Asset Share Token (AST) reflecting the value of their assets.

Notably, in September 2022, Finbold reported on regulators accusing Celsius’s company executives of misleading investors before the high-profile collapse and making questionable transactions, such as by the wife of former Celsius CEO Alex Manshinsky, who had reportedly cashed out $2 million in crypto before the bankruptcy announcement.

朝鲜半岛紧张局势持续升级,韩军对军事分界线南侧进行警告射击,朝鲜则炸毁了连接两国的通路。币圈担忧,若战争爆发,韩国作为主要的加密货币市场,恐慌情绪可能引发比特币价格剧烈波动。

AlexCanary Capital Group向美国证监会提交莱特币现货ETF申请,莱特币价格迅速上涨逾7%。同时,香港胜利证券宣布允许投资者使用USDT认购基金,稳定币恢复了美元锚定。

Miyuki

Miyuki比特币在萨尔瓦多推行三年,但民众接受度依然低迷

Weiliang

Weiliang根据美国联邦选举委员会最新披露,特斯拉CEO马斯克在过去三个月内向他为川普设立的政治行动委员会 America PAC 捐赠了7500万美元。与此同时,为了提升川普在关键摇摆州宾夕法尼亚的支持率,马斯克宣布将连续六天在宾州展开助选演讲活动。

AlexGoogle has begun rolling out Android 15, introducing new security features like Theft Detection Lock and Remote Lock, which help users secure their devices against theft. However, a promised Mobile Network Security feature is missing, leaving users disappointed, while enhancements like satellite messaging and predictive back gestures improve overall usability.

Weatherly

Weatherly特朗普家族的World Liberty Financial(WLFI)项目在周二推出代币公开发售,但仅售出4%的代币,筹资金额约1245万美元,远低于预期的3亿美元募资目标。

AlexFracture Labs has sued Jump Trading, accusing it of running a "pump and dump" scheme with DIO tokens, allegedly manipulating the token's price for profit during FractureLabs' fundraising.

Catherine

CatherineWeb3 projects are increasingly integrating Telegram into their user engagement strategies, as seen with the success of games like Hamster Kombat attracting over 300 million users. Robby Yung, CEO of Animoca Brands, predicts that having a Telegram strategy will become essential for onboarding users and expanding reach in the Web3 ecosystem.

Anais

AnaisSiam Commercial Bank has introduced Thailand's first stablecoin remittance solution, enabling 24/7 cross-border payments with enhanced security and efficiency. This initiative sets a new standard for financial transactions in the region.

Kikyo

KikyoDonald Trump has raised approximately $7.5 million in cryptocurrency donations for his 2024 presidential campaign, with major contributions coming from Bitcoin, Ether, and XRP. The influx of crypto donations reflects his shift from a critic to a pro-crypto candidate, gaining support from key figures in the industry.

Anais