ETF Buying Three Times More Bitcoin Supply than New Bitcoin Supply – Here’s What You Must Know

Bitcoin approaches $69,000 with traders optimistic about continued gains, supported by favorable economic policies and strong ETF inflows.

Miyuki

Miyuki

Source: Wall Street News

The private equity industry on Wall Street is currently facing a perfect storm, trapped in asset lock-ups, continued transaction deadlocks, valuation crises, and liquidity depletion.

As the conflict between Trump and universities becomes increasingly intense, the investment of Ivy League’s huge endowment funds has become the “eye of the storm”, and the latter’s investment decisions are usually regarded as the vane of the private equity market.

Now that Ivy League universities in the United States have started selling private equity, is a “new subprime mortgage” crisis slowly unfolding?

On Sunday, according to media reports citing people familiar with the matter, facing pressure from the Trump administration and threats to its tax-exempt status, Yale University is seeking to sell its private equity portfolio on a large scale, with the transaction size possibly reaching $6 billion, equivalent to 15% of its $41.4 billion endowment fund. This is Yale’s first sale in the secondary market.

Not only Yale, but some analysts say that if its tax-exempt status is still cancelled, it is only a matter of time before Harvard University starts selling liquid assets (such as stocks), and perhaps even issuing more debt.

In the current situation where risks in the private equity industry are accumulating, the psychological signal transmitted by this is crucial. This storm is likely to trigger a bigger crisis - a new "subprime crisis", and may trigger a chain reaction: hedge funds preemptively trade, private equity discount revaluation, and even spread to venture capital departments supported by endowment funds.

Some analysts further pointed out that the core of the problem is not only the high exposure, but also that endowment funds were originally a model of "long-term investment": lack of liquidity, tax benefits, and freedom from political interference.

Now this isolation is breaking down. Once Harvard sells under pressure, it will not only make headlines, but also become a signal flare, marking the beginning of a new stage of defensive rotation, risk disintermediation, and a confidence crisis in private equity valuations.

According to CCTV News, the US federal government recently threatened to freeze federal funding and demanded that many universities "rectify", and Harvard University, a famous private institution in the United States, chose to "harden".

Harvard University in the United States rejected the Trump administration's request for major reforms to its management structure, recruitment and admissions policies on the 14th, and the US government immediately announced the freezing of the school's federal funding totaling about 2.26 billion US dollars.

On the 15th, Trump threatened again to cancel Harvard University's tax-exempt status and demanded an apology from the school.

On April 16, local time, US Secretary of Homeland Security Kristi Noem announced the cancellation of two grants totaling more than 2.7 million US dollars provided by the Department of Homeland Security to Harvard University.

Faced with severe financial challenges, it is reported that Yale has been forced to sell a private equity portfolio of up to $6 billion. As of June 2024, the fund's endowment fund size is $41.4 billion, and the shares sold account for about 15% of the total endowment fund.

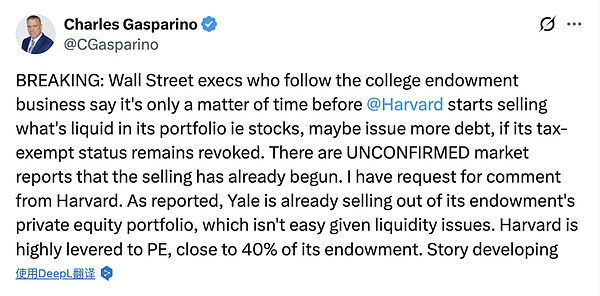

FOX's senior business reporter said on X:

Wall Street executives who pay attention to the university's endowment business said that if its tax-exempt status is still cancelled, it's only a matter of time before Harvard starts selling liquidity (i.e. stocks) in its portfolio, and perhaps issuing more debt.

There are unconfirmed market reports that the sell-off has begun. Harvard's investment in private equity is quite high, close to nearly 40% of the endowment fund.

Some analysts said that such a large-scale sale is extremely rare in the history of education endowment funds, indicating that the Ivy League is facing unprecedented financial pressure.

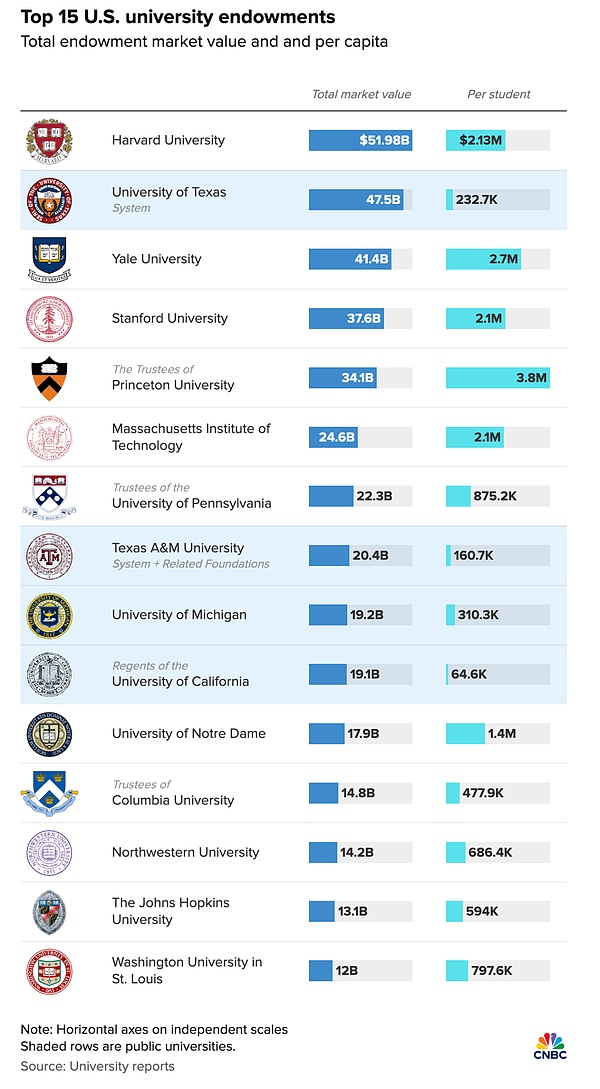

It is worth mentioning that elite universities such as Harvard are "rich enough to rival a country". The total amount of Harvard University's endowment fund is close to 52 billion US dollars, which is larger than the GDP of many countries. These universities are more willing to invest their huge wealth in riskier assets, but this model also comes with risks.

Historically, university endowment funds have traditionally invested very conservatively, but in the early 1950s, Harvard University adjusted its allocation to 60% stocks and 40% bonds, taking on more risk and creating more opportunities for upside.

Other universities soon followed suit, with Yale University pioneering the "Yale Model" in the 1990s, which is centered on diversified investment and allocates a large amount of funds to alternative assets, especially private equity.

Yale University ranks 27th among private equity investors in the world, with more than $20 billion invested in this asset class.

According to Harvard's annual report, the majority of the endowment fund's funds are allocated to private equity (39%), and Harvard has made significant adjustments to its portfolio allocation over the past seven years. Harvard Management Company has reduced the proportion of the endowment fund's investment in real estate and natural resources from 25% in 2018 to 6%. These cuts have allowed it to increase private equity investments.

In addition, Harvard will issue $750 million in taxable bonds, due in September 2035, and in February the school issued $244 million in tax-free bonds. Many universities, including Princeton and Colgate, also issued bonds this spring.

Moody's has not yet updated Harvard's AAA rating on its bonds. However, for higher education as a whole, the rating agency is not so optimistic, downgrading its outlook to negative in March.

"New Bond King" Jeffrey Gundlach previously said in an interview that

Harvard originally operated on the cash flow of annual donations, which allowed them to invest the principal, but they ended up having to go to the bond market to raise billions of dollars to pay salaries and electricity bills. They have no liquidity at all, and their money is locked up in a place where they can't move at all.

For the private equity industry, the Ivy League has always been one of the most important investors. They not only provide a lot of funds, but also their investment decisions are often regarded as market vanes.

The forced withdrawal of these university funds will change the industry's capital flow pattern and may lead to a valuation reset.

In particular, the current private equity industry on Wall Street is facing a perfect storm, trapped in asset lock-ups, continued transaction deadlocks, valuation crises, and liquidity depletion.

The stock prices of private equity giants such as Apollo, Blackstone and KKR have plummeted by more than 20% this year, far exceeding the decline of the S&P 500 index. As the transaction deadlock continues, it is becoming increasingly difficult for these companies to return funds to clients such as pension funds and endowment funds.

"New Bond King" Gundlach once warned that the United States may be facing a new "subprime crisis" and the risks of the private equity market are seriously underestimated.

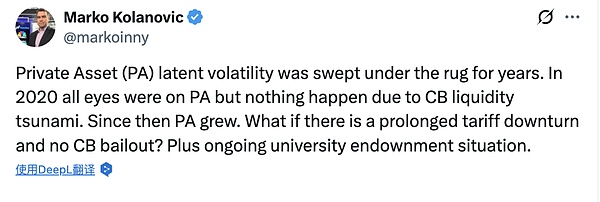

Analyst Marko Kolanovic said on X:

The potential volatility of private equity assets has been concealed for many years. Private equity assets were in the spotlight in 2020, but no problems arose in the end due to the release of a large amount of liquidity by central banks.

Since then, the scale of private equity assets has continued to grow. However, what will happen if there is a long-term downward tariff cycle and no central bank rescue? Add to that the current situation of university endowment funds.

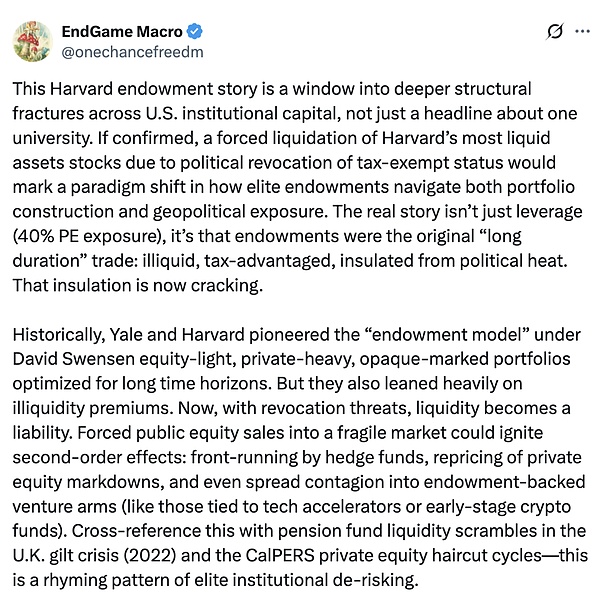

EndGame Macro analyzes the deeper impact:

The Harvard endowment fund incident reflects the deeper structural cracks in American institutional capital, and is not just a news headline about a certain university. If true, the revocation of tax-free status due to political factors forces Harvard to liquidate its most liquid asset - stocks, which will mark a paradigm shift in the way elite endowment funds deal with portfolio construction and geopolitical risk exposure.

The core of the problem is not only leverage (40% private equity exposure), but also that endowments were once the epitome of "long-term investment": illiquid, tax-advantaged, and free from political interference. Now, this insulation is breaking down.

Historically, Yale and Harvard, led by David Swensen, pioneered the "endowment model", which is to reduce public market equity allocation, focus on private equity, and have a professional and opaque portfolio, optimized for a long-term investment horizon. However, this model also relies heavily on a liquidity premium.

Now, with the threat of revoking tax benefits looming, liquidity has become a burden. Being forced to sell public market equities in a fragile market environment could trigger second-order effects: hedge fund front-running, revaluation of private equity discounts, and even spillover to venture capital arms backed by endowments (such as those connected to tech incubators or early-stage cryptocurrency funds).

Looking back at the pension fund liquidity scramble during the gilts crisis in the UK in 2022 and the CalPERS private equity write-down cycle, this series of events shows a similar pattern of elite institutional de-risking.

A possible mistake in the analysis is to assume that Harvard’s entire portfolio is at risk. In fact, Harvard may have hedged political risk through prudent asset reallocation over the past year. However, the psychological signal sent to other institutions (such as MIT, Princeton University, and even corporate foundations) is critical. Liquidity defensive postures will have a silent tightening effect through capital markets, cascading down.

This event marks the beginning of an era of reputational risk for institutional allocators. Politics are now part of portfolio risk, and the myth of “permanent capital” has been shattered. Harvard’s sale of shares under pressure will not only make headlines, but will also serve as a signal flare, marking the beginning of a new phase of defensive rotation, risk disintermediation, and a crisis of confidence in model-based private equity valuations.

Next, closed-end fund and private equity secondary market auctions may stall, which is worth paying close attention to.

Bitcoin approaches $69,000 with traders optimistic about continued gains, supported by favorable economic policies and strong ETF inflows.

MiyukiThe individual identified by Pump.Fun as the former employee responsible for the recent $1.9 million exploit, has been apprehended and subsequently released on bail in London.

Kikyo

KikyoAndrew Tate plans to ditch fiat for Bitcoin, investing $100 million in the cryptocurrency due to frustrations with traditional banking and inflation concerns. El Salvador's bold adoption of Bitcoin as legal tender, coupled with its innovative mining methods using volcanic power, showcases a growing trend towards digital currencies and renewable energy in the global financial landscape.

Anais

AnaisRumors suggest that the SEC might make a 180-degree turn on approving a spot Ethereum ETF. In response, Ethereum surged over 15%, and Bitcoin broke the $70,000 mark.

Alex

AlexEther surged close to 20% within 24 hours, driven by fresh speculation from analysts. Despite months of prevailing pessimism, it was suggested that spot Ether ETFs might receive approval this week.

Catherine

CatherineMajor tech giants like OpenAI, Google, Apple, Microsoft, and ByteDance are fiercely competing in the AI race, investing heavily in developing advanced AI models and integrating AI into their products. As AI technology advances, ensuring security measures are in place to prevent exploitation and combat misinformation becomes increasingly crucial for fostering safe and responsible AI innovation.

Joy

JoyRussian President Putin accuses the US of attempting to block Russia's payments to China and other countries. Putin claims: "This is truly stupid and a huge mistake by the American political elite because they are causing themselves enormous harm."

MiyukiA 16-year-old genius from China bought Bitcoin for $10 in 2010 and later established a well-known trading platform. However, due to three hacker attacks, a staggering $7.2 billion worth of Bitcoin was lost.

Weiliang

WeiliangOpenAI has suspended the ChatGPT voice model ‘Sky’ due to its uncanny resemblance to Scarlett Johansson, emphasizing that AI-generated voices should not intentionally imitate those of celebrities.

KikyoNeuralink gains FDA approval for second brain chip implant, aiming to expand trials with plans to target ten participants. While facing criticism for transparency and safety concerns, the company's progress offers hope for individuals like Noland Arbaugh, demonstrating potential life-changing improvements in quality of life.

Weatherly

Weatherly