Coinbase's Layer-2 Blockchain, Base, Faces Challenges Amidst Ethereum Network Surge

Coinbase's Base blockchain faces challenges amid Ethereum's network surge, exacerbated by the meme coin craze, causing transaction disruptions and rising fees.

Alex

Alex

In essence, moving RWA assets such as US stocks and gold to the chain only completes the "digital packaging" of the assets, solving the problems of asset issuance and cross-regional circulation, but is far from releasing their true potential.

Imagine that a tokenized asset, if it can only be circulated statically in a wallet and cannot be used in combination, will lose the composability advantage of the blockchain. After all, in theory, the introduction of RWA can greatly improve asset liquidity and release new value through DeFi operations such as lending and staking. Therefore, it should have injected high-quality assets with real returns into DeFi, strengthening the value foundation of the entire crypto market. This is a bit like ETH before the DeFi Summer. At that time, it could not be loaned, used as collateral, or participated in DeFi. It was not until protocols like Aave gave it functions like "collateralized lending" that it released hundreds of billions of dollars in liquidity. For US stock tokens to break through this dilemma, they must replicate this logic and make the deposited tokens "live assets that can be mortgaged, traded, and combined."

For example, users can use TSLA.M to short BTC and use AMZNX to bet on the trend of ETH. Then these deposited assets are no longer just "token shells", but margin assets that are used. Liquidity will naturally grow from these real trading needs.

This is exactly what the move from RWA to RWAFi means. However, the real release of value requires far more than a single technological breakthrough, but a systematic solution, covering:

Infrastructure layer: secure asset custody, efficient cross-chain settlement and on-chain liquidation;

Protocol layer: standardized tools that facilitate rapid integration between developers and asset parties;

Ecosystem layer: in-depth linkage and cooperation of various DeFi protocols such as liquidity, derivatives, lending, and stablecoins;

So where is it stuck now?

The biggest problem in the current RWA token market is no longer the "lack of underlying assets" but the "lack of liquidity structure."

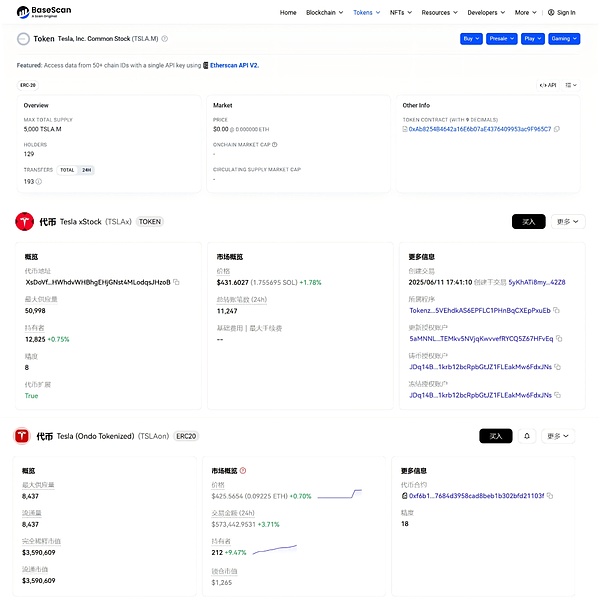

First, there is the lack of financial composability. In the traditional US stock market, abundant liquidity stems not from the spot market itself but from the trading depth fostered by derivatives like options and futures. These tools support price discovery, risk management, and leverage, fostering long-short speculation and diversified strategies, attracting continued institutional investment, and ultimately creating a virtuous cycle of "active trading → deeper market → more users." However, the problem is that the current US stock tokenization market lacks this crucial structural element: The TSLA and AAPL tokens purchased by users can mostly only be "held" but not truly "used." They cannot be used as collateral to borrow stablecoins on Aave, nor as margin to trade other assets on dYdX, let alone construct cross-market arbitrage strategies based on them.

Therefore, although these RWA assets have come to the chain, they are not yet "alive" in a financial sense. Their capital efficiency is far from being released, and the road to the vast DeFi world is blocked.

Note: They are TSLA.M of MyStonks, TSLAx of xStocks, and TSLAon of Ondo Finance.

Secondly, there is the fragmentation and fragmentation of liquidity. This presents a more thorny issue: different issuers, based on the same underlying asset (e.g., Tesla stock), have launched independent, incompatible token versions, such as MyStonks' TSLA.M, xStocks' TSLAx, and Ondo Finance's TSLAon. This "multiple token issuance" situation is reminiscent of the early difficulties of the Ethereum Layer 2 ecosystem—liquidity was fragmented into isolated islands, unable to converge into a single ocean. This not only significantly diluted market depth but also created significant obstacles for user and protocol integration, severely hindering the scalability of the RWA ecosystem. 03 How to Complete the Missing Pieces? How to resolve the above dilemma? The answer lies in building a unified and open RWAFi ecosystem, transforming RWA from a "static asset" into a composable and derivative "dynamic Lego brick." Therefore, Nasdaq's latest move is particularly worthy of attention. Once top traditional institutions like Nasdaq enter the market and issue official stock tokens, it will fundamentally resolve the trust issue at the source of assets. Then, within the RWAFi framework, a unified RWA asset can be "financialized" in various ways - through operations such as mortgage, lending, staking, and income aggregation, it not only generates cash flow but also introduces real-world value anchoring to the chain.

Importantly,this kind of financialization is not limited to highly liquid assets such as U.S. stocks and U.S. bonds. Even fixed assets with extremely poor liquidity and composability in the real world can be "activated."

We can imagine its potential through an example. Take real estate, an asset with extremely poor liquidity in the real world. Once it is standardized and introduced into the RWAFi framework, it is no longer "real estate" but becomes a highly dynamic financial component:

Participate in lending: Use it as high-quality collateral to obtain low-interest financing on the chain and activate dormant capital;

Automate income: Through smart contracts, monthly rental income is automatically and transparently distributed to each token holder in the form of stablecoins;

Build structured products: Separating a property's "value-added rights" from its "rental income rights" and packaging them into two distinct financial products caters to investors with varying risk appetites. This "dynamic empowerment" breaks the inherent limitations of RWAs and infuses them with the higher-dimensional composability inherent in DeFi. Therefore, Nasdaq's stock tokenization is just the first domino to fall. Once they find success with US stock tokens, all kinds of assets, from real estate to commodities, will usher in a wave of on-chain integration. Therefore, the real explosion point in the future will not be these assets themselves, but the derivative ecosystem built around them—collateralization, lending, structuring, options, ETFs, stablecoins, income certificates… All of these familiar DeFi modules will be recombined and nested on standardized RWA to form a brand new "Real Return Finance (RWAFi)" system. If the DeFi Summer of 2020 was a "currency Lego" experiment centered around crypto-native assets like ETH and WBTC, then the next wave of innovation initiated by RWAFi will be a larger and more imaginative "asset Lego" game based on the entire real-world value. When RWA is no longer just an asset on the chain, but becomes the underlying building block of on-chain finance, a new round of DeFi Summer may also begin.

Coinbase's Base blockchain faces challenges amid Ethereum's network surge, exacerbated by the meme coin craze, causing transaction disruptions and rising fees.

AlexCCData's report highlights stablecoin market growth, with USDT surpassing $100 billion and Ethena's USDe emerging as a significant player.

Miyuki

MiyukiAcademics have uncovered a severe vulnerability in Apple's M-series chips, allowing hackers to access encryption keys. This "unpatchable" flaw poses a significant challenge to Apple's security infrastructure.

AlexSchwartz's cryptic tweet suggests a future XRP price of $5. SEC victories and a new trading bot add intrigue. XRP's price shows volatility.

MiyukiAIOZ Network partners with Alibaba Cloud, becoming the leading blockchain ally in their Innovation Accelerator program, aiming to revolutionize southeast Asia's blockchain landscape.

Weiliang

WeiliangA Binance executive, detained in Nigeria over a tax evasion case, reportedly escaped using a fake passport. The incident has raised questions about security and regulatory oversight in the crypto space.

AlexIndonesian student Sultan Gustaf Al Ghozali, known for earning $1M from selfie NFTs, raises $1.8M in a memecoin presale comeback.

MiyukiElon Musk questions Vitalik Buterin's departure from X, prompting discussions about Farcaster and the cultural impact on cryptocurrency platforms.

WeiliangNilam Resources, Inc. enters a strategic partnership to acquire 24,800 Bitcoin, signaling a shift towards digital assets in the financial landscape.

AlexARK Invest's Cathie Wood offloads 1.6 million HOOD shares as Robinhood surges, focusing on Roblox and Coinbase.

Miyuki