China's Progress with Digital Yuan Signals Potential for De-Dollarisation

China's Digital Yuan achieves milestone as it makes debut in landmark oil transaction.

Hui Xin

Hui Xin

Author: CryptoAmsterdam, Twitter@damskotrades; Source: SevenUp DAO

Is it true that "without quantitative easing (QE), there would be no alt season"?

Recently, my comment section has been filled with similar opinions:

"We need QE to usher in the alt season."

"Without QE, the alt season will never start."

Let's analyze it.

This is not usually my main research area, but since everyone is discussing QE, I will briefly analyze it.

(Note: I am not an expert in this field. Please correct me if I make any mistakes. In order to simplify the discussion, we will only start with the charts and not make too many guesses. Please refer to them with caution.)

1.What are QE and QT? 1. QE (Quantitative Easing): The central bank injects money into the market by creating new money. The specific operation is to increase market liquidity by purchasing assets. Increased liquidity = Favorable for risky assets (such as cryptocurrencies) 2. QT (Quantitative Tightening): The central bank reduces the money supply in the market. Methods include selling assets or letting assets mature to recover liquidity. Reduced liquidity = Unfavorable for risky assets

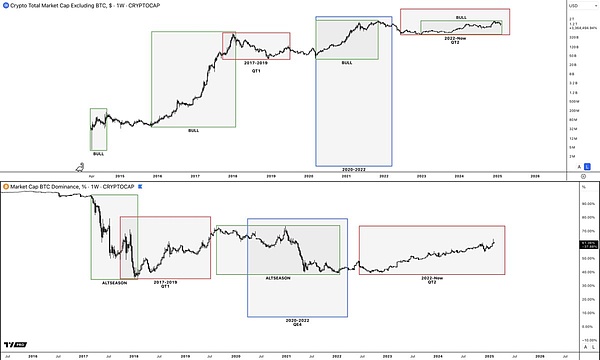

If we overlay the total market value chart of the entire altcoin market with the Bitcoin dominance chart, and mark the time periods of QE (good for the market) and QT (bad for the market), we will find that these two statements are not true.

3. There have been significant bull markets and altcoin seasons without QE

In fact, QE has only coincided with a bull market once, which was in 2021.

Summary of chart analysis:

The arrival of the altcoin season does not depend on QE.

During the QT period, the total market value of the altcoin market soared from US$400 billion to US$1.7 trillion.

While QE can boost the market, it is not a necessary condition - other factors may also trigger market growth, such as the launch of ETFs, support from government policies, SBR (which may refer to a stable currency reserve mechanism) or the increase in the value of Bitcoin.

Stopping QT would theoretically be beneficial to the market, but the market still achieved growth during QT, which shows that QT is not the decisive factor in market performance.

Second, What is Altseason?

In the cryptocurrency market, two main phases can generally be divided:

Bitcoin Season

Altcoin Season

1. Bitcoin Season:

Bitcoin Season is characterized by an increase in Bitcoin Dominance (i.e., Bitcoin's share of the total cryptocurrency market). This is because funds flow from altcoins to Bitcoin, causing the overall performance of altcoins to deteriorate compared to Bitcoin.

New funds mainly flow into Bitcoin, and the market share of altcoins therefore decreases.

2.Alt Season:

Alt Season is characterized by a decline in Bitcoin dominance as funds flow from Bitcoin into Alt.

The inflow of new funds drives up the market share of Alt, while the total market value of Alt will soar rapidly.

From historical data, the market is in Bitcoin Season most of the time, and Alt usually performs worse than Bitcoin. Here are several typical Bitcoin Season stages:

Bitcoin is in a bear market? This is Bitcoin Season.

Bitcoin bottomed out? It is still Bitcoin Season.

Bitcoin starts to rise initially? Bitcoin Season.

Bitcoin rises to the high point of the previous cycle? Bitcoin Season.

Bitcoin breaks new highs? Still Bitcoin Season.

The emergence of the alt season usually has certain rules: It often occurs after Bitcoin breaks new highs for the first time and enters a consolidation phase. Then, when Bitcoin rises again, the alt season will truly arrive, when Bitcoin dominance begins to decline and the alt market usher in an explosion.

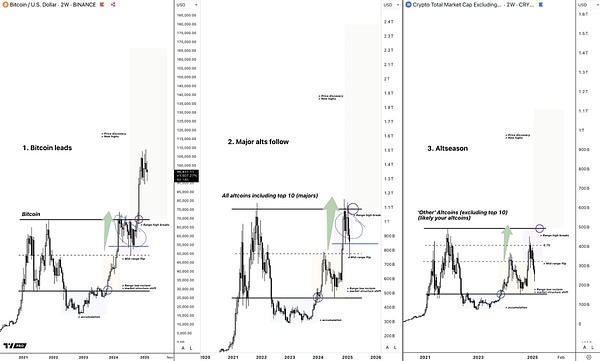

3. Triggers of the Alt Season

The Alt Season is usually triggered by the start of the Bitcoin bull market. (Note that this does not depend on quantitative easing (QE); we are currently in the quantitative tightening (QT) phase. Other possible triggers include the value and cycle of Bitcoin, the stablecoin reserve mechanism (SBR), the launch of Bitcoin ETFs, etc.)

The first step of capital flow is usually an influx of Bitcoin and major Alts.

The next result is:

The media hype attracts the attention of retail investors, who may therefore start buying Alts.

At the same time, investors who have made profits in Bitcoin will turn their funds to the altcoin market in pursuit of higher returns.

From historical data, this phenomenon usually occurs when Bitcoin breaks through a new high for the second time. This pattern can be observed from the previous chart.

The flow of funds in the crypto market has a relatively clear path:

Bitcoin → Major altcoins → High market value tokens → Medium market value tokens → Low market value tokens

For example, on January 18, 2021, Bitcoin was in a consolidation phase and tried to break through a new high (as shown by the red arrow in the figure), while Total 3 (i.e., the total market value indicator of the altcoin market) was still at an intermediate level (as shown by the red arrow in the figure).

From here, we can see that Bitcoin is usually the starting point of capital flow, followed by the total market value of the major altcoins (Total 3), and finally the other tokens (including high-cap and mid-cap tokens).

The trigger of the altcoin season does not rely on quantitative easing QE. (Of course, QE does help the market.)

The key is that a large amount of funds first flow into Bitcoin and major altcoins, and then the greed of the market will drive funds to flow further to other altcoins.

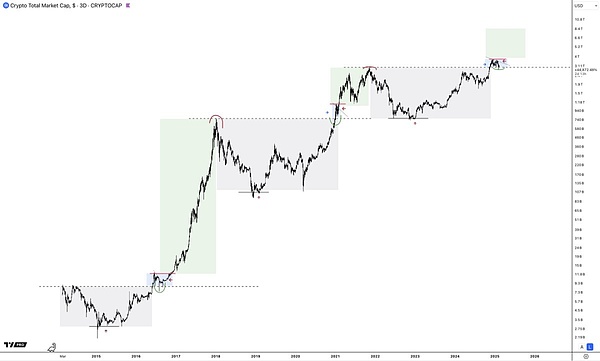

This is the trigger mechanism of the altcoin season. So far, whether it is QE, QT, or other external factors, we are on the right track. The entire cryptocurrency market (mainly composed of Bitcoin and some major alts, because the alt season has not really arrived yet) has grown from 700 billion US dollars to nearly 4 trillion US dollars.

(Think carefully, the market can still achieve such growth in the QT stage, which is undoubtedly a very optimistic signal. In the future, as the policy environment changes, this trend may become more favorable.)

China's Digital Yuan achieves milestone as it makes debut in landmark oil transaction.

Hui XinApple allocates $1B to accelerate it’s lagging AI initiatives. Amidst executive anxieties, the tech giant is fast-tracking generative AI technology for a smarter Siri and more.

YouQuan

YouQuanThe trial involved real-time transfers and swaps of synthetic USDC and EURS to wallets owned by Deutsche Bank.

Clement

ClementIn a shocking case, Dr. James Wan used Bitcoin to orchestrate a dark web murder-for-hire plot to kill his girlfriend.

Jixu

JixuBTC experienced a notable upswing, briefly reaching $35K, reflecting a surge in enthusiasm stemming from recent advancements in the Bitcoin ETF landscape.

Jasper

JasperThe new governor Pan Gongsheng stressed the importance of seeking progress while maintaining stability.

Alex

AlexU.S. contemplates clampdown on Chinese access to cloud technology amid escalating geopolitical tensions.

Hui XinUnder current federal legislation, providing such services remains tightly regulated, effectively excluding many businesses, particularly small independent operators, from the benefits of conventional banking.

Brian

BrianAstar Network and Startale Labs, both Singapore-based entities, have entered into an agreement with KDDI Corporation, a Japanese telecommunications company, to explore collaboration in the Web3 domain.

Joy

JoyAmidst a backdrop of rising optimism for Bitcoin ETFs and regulatory shifts, Lyn Alden argues that the anonymity of Bitcoin's creator, Satoshi Nakamoto, fortifies the cryptocurrency's foundational tenets of decentralization. Alden's perspective adds another layer to the evolving narrative of crypto legitimacy.

YouQuan