RMB internationalization is a long-term task, but the progress of internationalization is still slow compared with the improvement of China's economic status in the world. This article explores the possibility of accelerating the process of RMB internationalization and analyzes the pros and cons brought about by it. Marx once wrote in "Capital": The process from commodity to currency is a thrilling leap. So, will it also be a thrilling leap for RMB to change from its current state to an international currency with high global recognition? This article mainly discusses the feasibility and significance of accelerating the pace of RMB internationalization from the perspective of "liquidity premium".

Key points of this article:

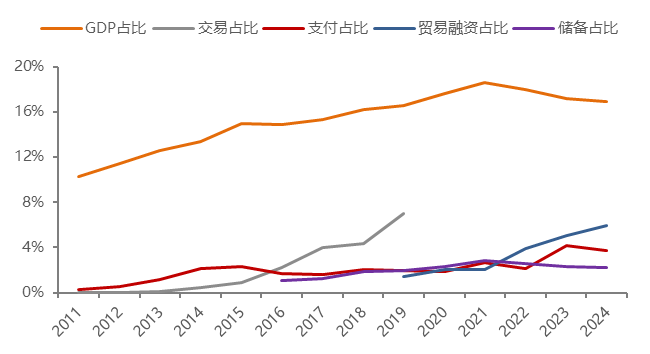

The current level of RMB internationalization does not match the size of China's economy. The international share of RMB in foreign exchange transactions, international payments, trade financing, reserve currencies, etc. is far lower than the share of economic size.

RMB payment may be underestimated in the world. The scale of currency swap agreements and CIPS usage has increased significantly. SWIFT's statistics on RMB payments are incomplete, and the actual RMB payment settlement ratio is estimated to be around 8%. However, RMB payments have a relatively narrow geographical area. International payments mainly occur in Hong Kong, accounting for more than 70%.

Historical experience shows that accelerating the internationalization of the RMB does not necessarily lead to RMB depreciation. After my country's exchange rate reform in 2005, the RMB appreciated against the US dollar for nine consecutive years.

The difference between the PPP exchange rate and the market exchange rate of an economy's currency is actually the risk premium of the currency, and the risk premium = liquidity premium + credit premium. To narrow the exchange rate difference, on the one hand, liquidity should be improved, and on the other hand, currency credit should be enhanced.

The RMB market exchange rate is underestimated compared to the purchasing power parity (PPP) exchange rate. In foreign exchange transactions, 1 US dollar can be exchanged for about 7.2 RMB, but 1 US dollar can only buy goods worth 3.5 RMB. The main reason why the RMB exchange rate is undervalued is the lack of liquidity worldwide, which leads to a high liquidity premium.

High M2 does not mean high pressure for currency depreciation. The proportion of "foreign exchange deposits" in China's M2 is relatively high because the export surplus has led to foreign exchange inflows into China, forcing the central bank to passively absorb foreign exchange and release base currency. If the circulation of RMB is expanded from domestic to global, similar to the full circulation of corporate shares in the equity split reform, the "valuation" level of RMB will be further improved.

Currently, the liquidity of the US dollar is too large (as a payment currency, the US dollar accounts for 48.46% of the world's share, and as a reserve currency, it accounts for 57.8% of the world's share). In addition, the scale of the US stablecoin anchored to the US dollar, US short-term bonds and time deposits is the largest in the world, resulting in excessive liquidity of the US dollar. After all, the US GDP accounts for 26% of the world. Therefore, if too much US dollars or US dollar assets are allocated, it is easy to be kidnapped by the credit of the US dollar. In other words, too low liquidity is likely to lead to an undervalued exchange rate, and too high liquidity leads to an overvalued exchange rate. At present, the US dollar is in an overvalued exchange rate state.

Now is a good time to accelerate the internationalization of the RMB. From the perspective of the external environment, the US dollar index fluctuates downward, the US debt pressure increases, and the safe-haven attribute of the US dollar weakens. From the perspective of its own development, enterprises going overseas have driven the RMB to "go global", and the use of RMB in cross-border business has increased significantly. The low interest rate level helps to enhance the RMB's financing currency function.

It is recommended to further expand the openness of the capital account and provide convenience for enterprises and residents to exchange foreign exchange. With the decline in the return on investment in domestic industries and overcapacity in some industries, Chinese enterprises and capital have the need to go overseas to seek high returns and allocate global high-quality resources. In particular, insurance funds and pension funds can be considered to go overseas.

Study and promote the legislation of RMB stable currency. Study the pilot RMB stable currency within a certain scope (such as offshore, free trade zones, etc.) and certain business scenarios (such as "Belt and Road" cross-border trade, RMB settlement of bulk commodities, etc.), and gradually improve the relevant regulatory system and finally raise it to law.

The moderate appreciation of the RMB will reduce the lower limit requirement for the annual GDP growth rate to a certain extent, avoid driving economic growth too much through investment in "fast variables", and help the transformation of the economic structure.

The internationalization of the RMB is conducive to the growth and strength of Chinese enterprises. It can not only attract foreign capital to flow into the A-share market, but also help enterprises to acquire key resources overseas.

Of course, the appreciation of the RMB may have a certain negative impact on exports, but generally speaking, the benefits outweigh the disadvantages. The impact of the appreciation of the RMB on exports has a lag effect. The improvement of trade quality and the advantages of the industrial chain and supply chain will help to mitigate the adverse effects of the appreciation of the RMB. The appreciation of the RMB is beneficial to some industries with a high proportion of imports.

The current level of RMB internationalization - does not match the global influence of China's economy

According to the data of the National Bureau of Statistics, China's GDP in 2024 will be 18.9 trillion US dollars, ranking second, accounting for about 18% of the global GDP. However, the international share of the RMB in foreign exchange transactions, international payments, trade financing, and reserve currencies is far lower than the share of economic size.

Figure 1 Economic size and RMB function ratio (%)

Source: BIS/SWIFT/IMF/WIND, Zhongtai Securities (6.400, -0.03, -0.47%) Research Institute

Note: The transaction ratio is the two-way ratio of foreign exchange transactions

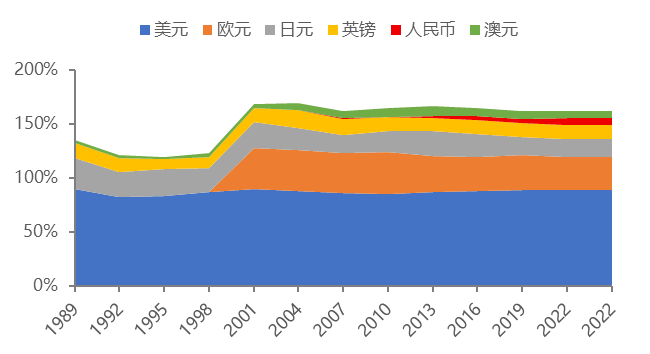

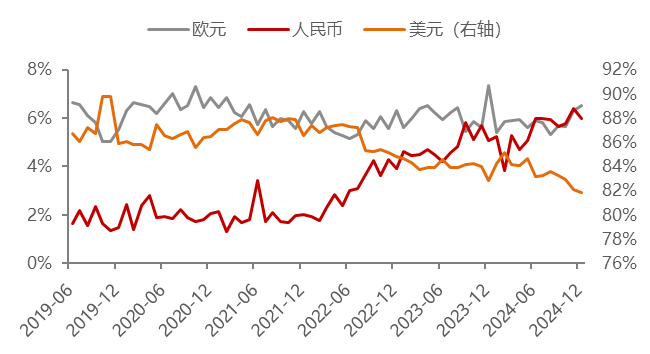

Figure 2: The proportion of major currencies in foreign exchange transactions (%)

Data source: BIS, Zhongtai Securities Research Institute

In terms of international payments, the proportion of RMB payment settlement is estimated to be around 8%. According to the data released monthly by the Society for Worldwide Interbank Financial Telecommunication (SWIFT), the proportion of RMB in international payments in May 2025 was only 2.89%, falling to the sixth largest payment currency. In recent times, the share of RMB in international payments has fluctuated, fluctuating downward from the highest point of 4.7% (July 2024), especially from March to May 2025, when it fell for three consecutive months, and its ranking also dropped from fourth to sixth, being surpassed by the Japanese yen and Canadian dollar successively.

Figure 3 The proportion of major currencies in international payments (%)

Data source: SWIFT, WIND, China Securities Research Institute

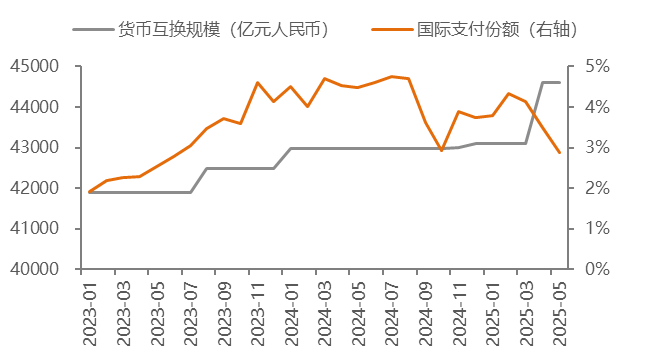

Since SWIFT only counts payments within its message system, and international payments in RMB do not necessarily go through the SWIFT system, SWIFT data may underestimate the scale of international payments in RMB. The underestimation is mainly reflected in two aspects: First, currency swap agreements; the People's Bank of China signs bilateral local currency swap agreements with foreign central banks, and foreign companies or individuals can directly complete currency payment settlement through the chain of "domestic bank-domestic central bank-People's Bank of China-Chinese bank" without relying on SWIFT. As of the end of May 2025, the People's Bank of China has signed bilateral local currency swap agreements with central banks of 32 countries (regions), with a total quota of 4.46 trillion yuan and an unexpired balance of 81.8 billion yuan.

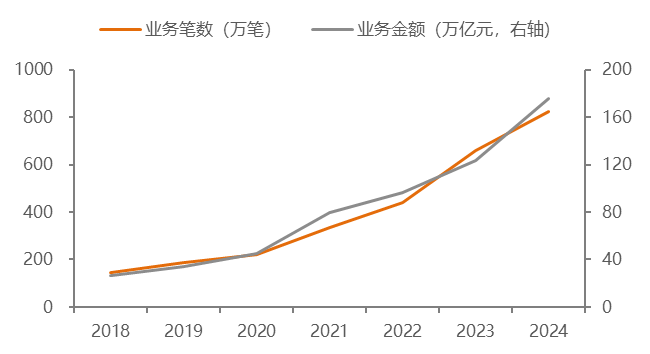

Second, the RMB Cross-Border Payment System (CIPS); SWIFT is a message system that transmits payment instructions (information flow) and does not involve the transfer of actual capital positions. CIPS has both message transmission and fund clearing functions. Its self-built message system independently processes payment instructions, and can directly complete the transfer of funds (fund flow) for cross-border RMB payments without SWIFT transit. Since CIPS went online, it has processed a total of about 600 trillion yuan in various payment businesses; as of the end of May 2025, there were 1,683 participants in the CIPS system.

Figure 4 The number and amount of CIPS business have increased significantly

Data source: WIND, China Securities Research Institute

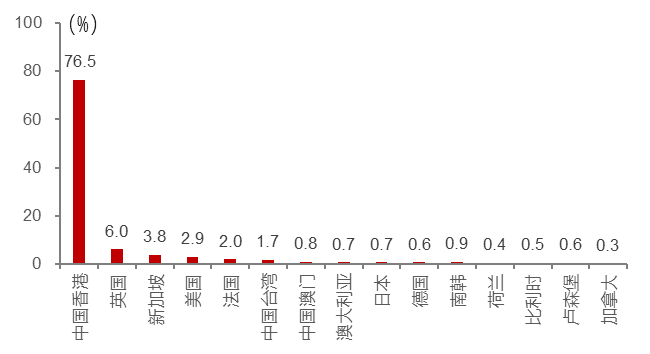

However, there is a relatively narrow geographical problem for RMB payments, that is, RMB international payments mainly occur in Hong Kong, accounting for more than 70%.

Figure 5 Regional share of RMB payments in the offshore market at the end of 24 years

Data source: WIND, China Securities Research Institute

In addition, the People's Bank of China recently launched the Cross-Border Payment Pass, which connects the mainland's online payment inter-bank clearing system with the Hong Kong fast payment system "FPS", providing real-time cross-border payment services without the need to go through the SWIFT message system. Taking into account currency swap agreements, CIPS and settlement data with local settlement systems of some countries (regions), the actual RMB payment settlement ratio is estimated to be around 8% (the Bank for International Settlements estimates that it will account for 6.8% in 2024).

Figure 6 The scale of currency swaps has steadily expanded

Data source: WIND, China Securities Research Institute

Note: The scale of currency swaps is the total upper limit of the available swap amount agreed upon in the bilateral local currency swap agreements signed between the People's Bank of China and other countries (regions).

In terms of trade financing, according to SWIFT data, by the end of 2024, the proportion of RMB in trade financing will be 5.98%, making it the third largest trade financing currency.

Figure 7 Proportion of major currencies in trade financing (%)

Data source: WIND, China Securities Research Institute

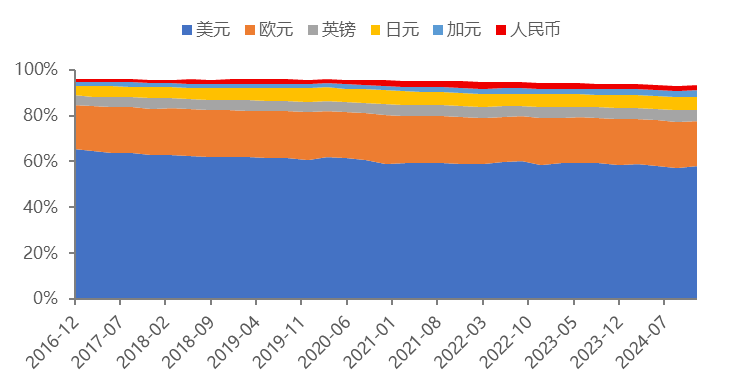

Figure 8 The proportion of major currencies in official reserves (%)

Data source: IMF, China Securities Research Institute

Through the above data analysis, it is not difficult to find that the internationalization of the RMB is indeed increasing, but it still lags behind the growth rate of my country's GDP. As the world's second largest economy, the proportion of revenue from overseas business operations of Chinese enterprises is still relatively low, and there is a lack of large multinational companies; although the global share of commodity exports has long been the first, is there any similarity with the motivation of large-scale exports in order to obtain more silver under the silver standard hundreds of years ago?

China's foreign exchange reserves are the largest in the world, and its export volume has also been the largest for a long time. The large scale of export surplus may be related to the fact that the RMB has not become a global "hard currency". What if the internationalization of the RMB can be accelerated and the RMB can become a hard currency? It may have a greater impact on corporate investment and residents' consumption behavior. However, the RMB becoming a hard currency will at least help China's economy to be more open, domestic enterprises to invest more conveniently in the world, domestic investors to have a more reasonable asset allocation portfolio, and China's economic growth quality will be higher.

The accelerated internationalization of the RMB - will it appreciate or depreciate?

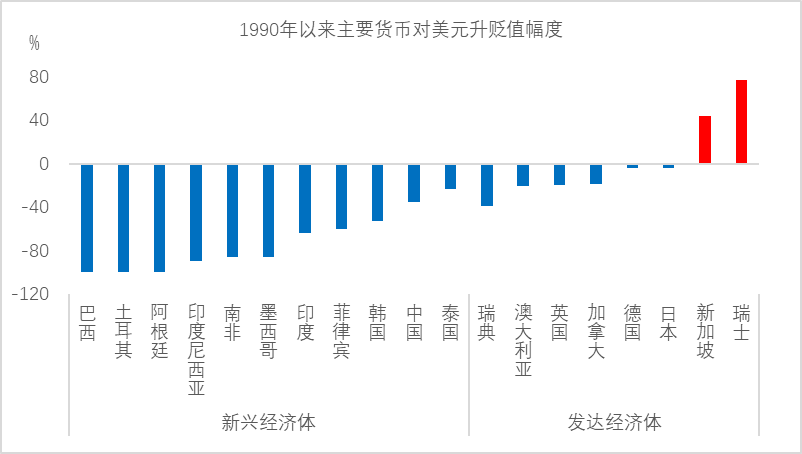

Before 2025, the market generally expects that the RMB will face depreciation pressure. But after Trump came to power, he advocated the devaluation of the US dollar, and the US dollar index continued to decline, and the RMB passively appreciated. So, is the expectation of RMB depreciation reasonable? Looking at the past 35 years, almost all developing countries' currencies have depreciated against the US dollar, and most developed economies have also depreciated against the US dollar. This easily gives people an illusion that the only way for developing countries' currencies to depreciate is to depreciate. But in fact, after my country's exchange rate reform in 2005, the RMB has appreciated against the US dollar for nine consecutive years. This shows that depreciation or appreciation is more determined by market supply and demand.

Figure 9 Since 1990, the currencies of most countries have depreciated against the US dollar

Data source: WIND, China Securities Research Institute

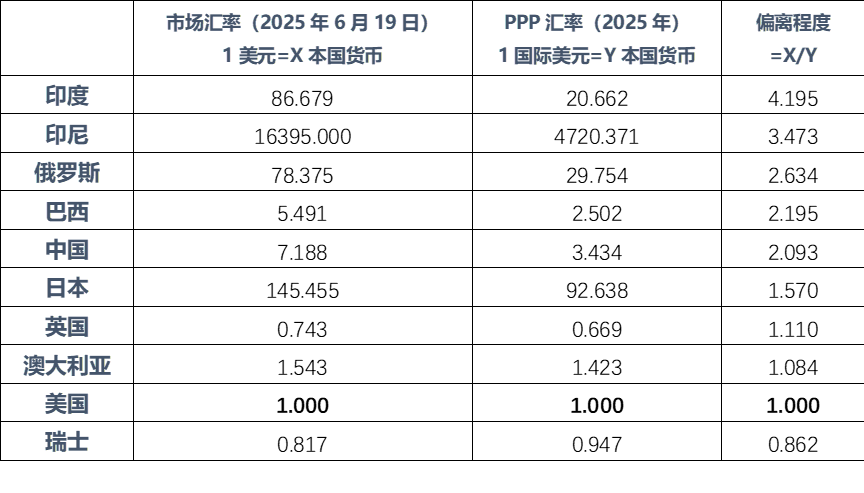

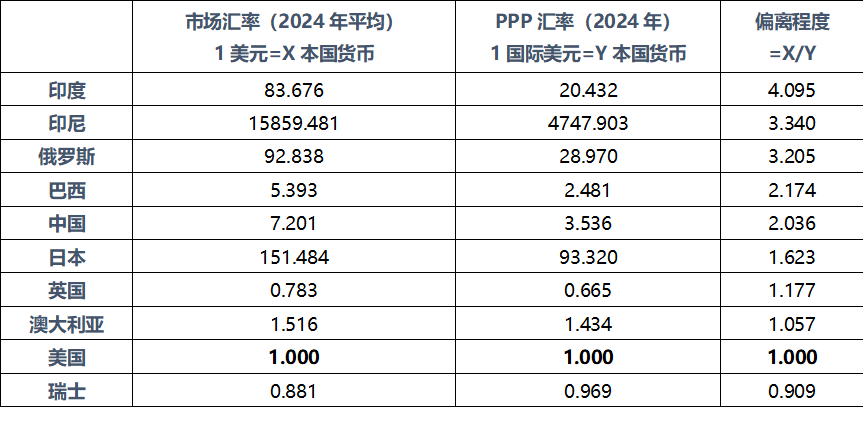

What if we compare the market exchange rate with the purchasing power parity (PPP) exchange rate? The market exchange rate is the currency exchange rate determined by the supply and demand relationship in the foreign exchange market and is easily affected by short-term currency flows; while the PPP exchange rate is a currency exchange rate calculated by comparing the price levels of the same goods and services in different countries, and aims to measure the actual purchasing power of a currency. The market exchange rate selects the bilateral exchange rate against the US dollar, and the PPP exchange rate uses data published by the IMF to compare the RMB with the currencies of major economies such as the United Kingdom, Japan, Switzerland, Australia, Russia, India, Brazil, and Indonesia (US dollar = 1). Comparing the average market exchange rate in 2024 with the PPP exchange rate in 2024, and the current market exchange rate in 2025 with the PPP exchange rate in 2025, we find that: (1) The RMB market exchange rate is undervalued. In foreign exchange transactions, 1 US dollar can be exchanged for about 7.2 RMB, but 1 US dollar can only buy goods worth 3.5 RMB. From the perspective of purchasing power, the RMB market exchange rate should appreciate. (2) In vertical comparison, the ratio of a country's market exchange rate to the PPP exchange rate has generally been at a relatively stable level from last year to this year (except for Russia, where the ratio has changed significantly due to significant fluctuations in the exchange rate last year. The ruble's closing price in 2024 fluctuated between 83.5 and 113.5, with a volatility of more than 30%). (3) In horizontal comparison, there are obvious differences in the ratio of each country's market exchange rate to the PPP exchange rate.

Table 1 Comparison of current market exchange rate and PPP exchange rate

Data source: wind, IMF, China Securities Research Institute

Table 2 Comparison of average market exchange rate and PPP exchange rate in 2024

WIND, IMF, Zhongtai Securities Research Institute

From the perspective of purchasing power parity, the RMB should appreciate. However, it is not only China that has a PPP lower than the market exchange rate. The PPP exchange rate of most developing countries is significantly lower than the market exchange rate. Should the currencies of all developing countries appreciate against the US dollar?

In addition, my country's broad money M2 is huge. As of May, it has exceeded 32.5 trillion yuan, close to the sum of the M2 of the United States, the European Union, and Japan. It is indeed suspected of "flooding". Therefore, many people are worried that once the RMB is fully internationalized, it will face pressure to depreciate significantly.

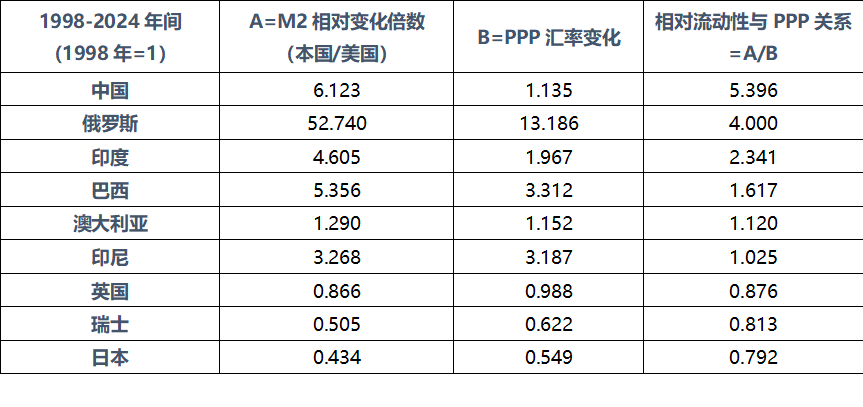

To this end, we analyze the reasons for the differences between the market exchange rate and the PPP exchange rate ratio in various countries. From the definition point of view, the difference between the market exchange rate and the PPP exchange rate is essentially the difference between the "short-term currency transaction price" and the "long-term purchasing power equilibrium", which seems to be related to the liquidity of a country's currency. Below, the two indicators A and B are compared (due to data availability, the observation period is 1998-2024, 1998=1):

A=a country's M2 in 2024 relative to its M2 in 1998/US M2 in 2024 relative to its M2 in 1998, used to measure a country's liquidity growth relative to US dollar liquidity between 1998 and 2024;

B=a country's 2024 PPP exchange rate relative to its 1998 PPP exchange rate, used to measure a country's real purchasing power growth between 1998 and 2024;

A/B=a country's liquidity growth relative to its purchasing power.

Calculation shows that China's liquidity growth is 5.4 times of its purchasing power, while Russia is 4 times, India is 2.3 times, Brazil is 1.6 times, Australia, Indonesia, the United Kingdom, Switzerland, and Japan are all around 1 or close to 1. China's broad money scale relative to purchasing power growth is significantly higher than other countries, and also significantly higher than the ratio of market exchange rate to PPP exchange rate.

Table 3: Growth of a country's monetary liquidity relative to purchasing power

Source: WIND, IMF, Zhongtai Securities Research Institute

It is not difficult to find from the above table that the A/B ratio of developing countries is generally higher, while that of developed countries is relatively low. What is the reason? Especially in China, where the currency scale is so large, the price level is so low. The author published an article "Chinese-style money creation and asset price fluctuations" 9 years ago, explaining this phenomenon. It is predicted that with the long-term decline of the real estate cycle, the growth rate of M2 will slow down and the ability to create money will also weaken. Therefore, it cannot be simply deduced that the larger the M2, the greater the pressure on currency depreciation. Just as CPI and M2 do not show a positive correlation.

Moreover, is it because the lack of international liquidity of the local currency that forces the scale of M2 to continue to expand? For example, the proportion of "foreign exchange deposits" in China's M2 is relatively high, because the export surplus leads to foreign exchange inflows into China, forcing the central bank to passively absorb foreign exchange and release base currency. Conversely, if the RMB is fully internationalized, the central bank will not need to increase foreign exchange reserves, but can reduce foreign exchange reserves, so that the total amount or growth rate of M2 will decline.

In other words, if the circulation scope of the RMB is expanded from domestic to global, then the "valuation" level of the RMB will be further improved due to the expansion of the circulation scope. For example, in 2006, the equity split reform of the A-share market achieved full circulation of legal person shares, and their stock prices all rose sharply. For example, in the planned economy era, national food coupons were more valuable than local food coupons. Although they could be exchanged for the same food, national food coupons were more convenient to exchange for food because they had a wide circulation range. Economists Menzie Chinn and Hiro Ito compiled the Chinn-Ito index in 2006 and have been continuously improving it. The index is mainly based on the IMF's Annual Report on Exchange Arrangements and Exchange Restrictions (AREAER). The principal component analysis method is used to obtain the degree of capital account openness of a country (measuring the degree of regulatory restrictions rather than the actual level of flow). The higher the score, the higher the level of free flow. At present, the index has been updated to 2022. From the perspective of capital account openness: the United States, the United Kingdom, Switzerland, Japan, Australia> Indonesia> China, Russia, India, Brazil, which can provide a basis for the explanation of the above-mentioned "undervalued exchange rates in developing countries". Since expanding the global openness and enhancing liquidity of the local currency can make the local currency appreciate, then why don't so many developing countries promote the globalization of their local currencies? This can be analyzed from the perspective of risk premium.

Risk premium = liquidity premium + credit premium

Most small and medium-sized developing countries have poor currency credit (such as political instability, economic fluctuations, etc.), and their economic size is small, so the currency liquidity is poor, which leads to high liquidity premium and credit premium of many developing countries' currencies. Therefore, the difference between the PPP exchange rate and the market exchange rate of an economy's currency is actually the risk premium. The larger the exchange rate difference, the higher the risk premium.

Therefore, the global liquidity or credit of a country's currency should match its economic size and its position in global finance and trade. There are nearly 200 countries and regions in the world, and there should be no more than 20 currencies that can become internationally influential. In other words, although the PPP exchange rate level of these countries' currencies exceeds the long-term market exchange rate level, the market exchange rate level is difficult to improve.

However, China is the world's second largest economy, with a GDP of nearly 18% of the world, exceeding the EU; its exports account for 14% of the world, which is also far ahead. However, the share of RMB as an international settlement, payment, trade financing and reserve currency is very low, which is extremely disproportionate to its status as a major economic and trade power. In addition, the leverage ratio of the Chinese central government is low, the scale of state-owned assets (including land, minerals, state-owned enterprises and other resources) is huge, and the credit of RMB is high, so there is huge room for RMB internationalization and appreciation is expected.

The current acceleration of RMB internationalization - is it a good time to "take a dangerous leap"?

From the external environment, affected by multiple factors such as reciprocal tariffs, the Beauty Act, and geopolitical conflicts, the current credit of the US dollar has weakened significantly, which brings opportunities for the RMB to accelerate its internationalization process.

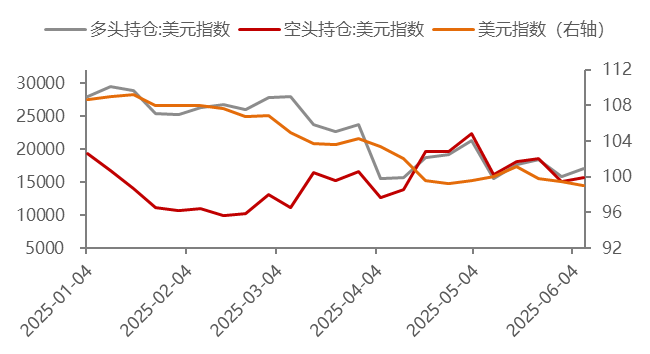

The US dollar index fluctuated downward. At the beginning of June, the US dollar index fell to 97.6, a new low since 2022, down more than 10% from the high of more than 110 at the beginning of the year. From the non-commercial positions of the Intercontinental Exchange (ICE), an indicator of the bullish/bearish sentiment of large speculators in the derivatives market, long positions decreased and short positions increased. As of June 10, 2025, the long position of the US dollar contract was 17,000 that week, a decrease of 36% from the number of positions at the end of last year. The market is not optimistic about the trend of the US dollar. According to the June Global and Asian Investment Manager Survey released by Bank of America Merrill Lynch, the current underweight ratio of the US dollar has hit a new low in nearly 20 years, and 59% of global investors expect the US dollar to weaken in the next 12 months.

Figure 10 The US dollar index fell and long positions decreased

Data source: WIND, Zhongtai Securities Research Institute

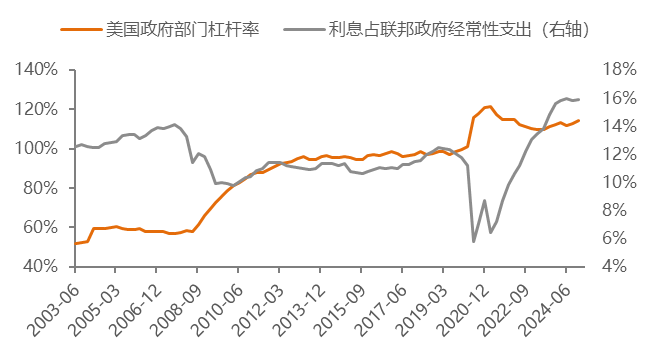

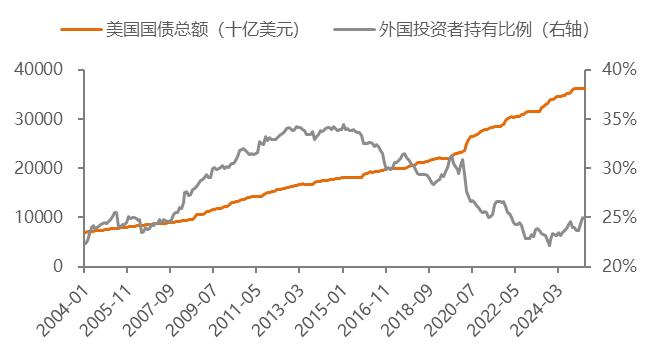

The US debt pressure is rising. At the end of 2024, the leverage ratio of the US government sector reached 114%, and the interest expenditure of the federal government accounted for as much as 16% of its recurrent expenditure. As of the end of May 2025, the size of the U.S. national debt exceeded 36.2 trillion U.S. dollars, and the pressure of maturing debt and borrowing new to repay old debts was huge. In recent years, the proportion of U.S. debt held by foreign investors has declined significantly and is currently below 25%.

Figure 11 The leverage ratio of the U.S. government has increased and the pressure of interest payments has increased

Data source: WIND, China Securities Research Institute

Figure 12 The scale of U.S. debt has increased and the proportion of foreign investors has decreased

Data source: WIND, Zhongtai Securities Research Institute

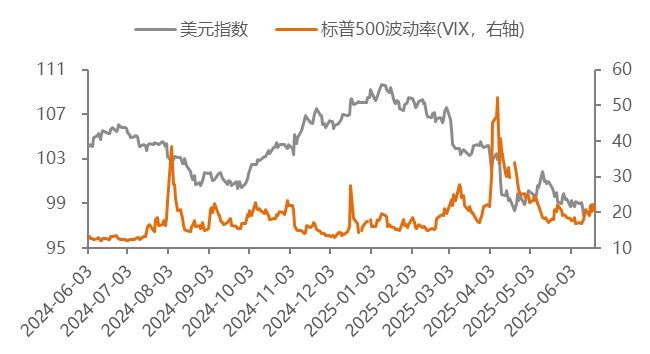

The safe-haven property of the US dollar has weakened. Historically, when the market is in panic, the S&P 500 Volatility Index (VIX) rises, and investors turn to the US dollar for risk aversion. The US dollar index rises with the VIX. The safe-haven characteristics of the US dollar were obvious during the 2008 financial crisis and the 2020 COVID-19 pandemic. However, in the past year, the US dollar index has continued to decline when the VIX rose, and the safe-haven asset attribute of the US dollar is questionable.

Figure 13 The safe-haven property of the US dollar has weakened

Data source: WIND, Zhongtai Securities Research Institute

From the perspective of its own development, the scale of Chinese companies going overseas has increased significantly, and the demand for cross-border payment and collection of RMB and RMB financing has increased significantly. The international use scenarios of RMB have become more abundant, bringing huge demand for the internationalization of RMB.

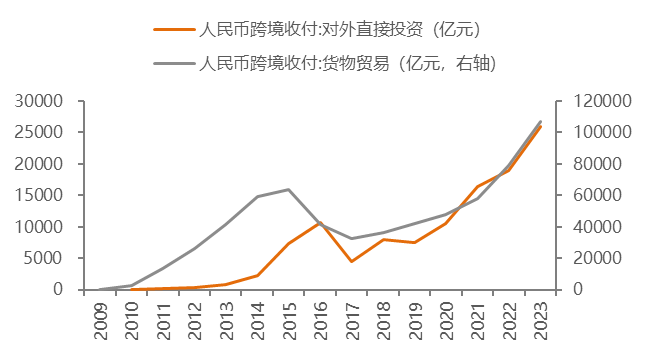

Enterprises' outbound direct investment (ODI) has driven the RMB to "go global". In 2023, the amount of cross-border RMB receipts and payments for outbound direct investment will be 2.6 trillion yuan. Although the absolute scale is not large, the growth momentum is good. Since 2017, the average annual compound growth rate has reached 33.6%, which is faster than the cross-border RMB receipts and payments for goods trade in the same period. As the chain of "outbound investment-equipment procurement-production and operation-profit remittance" of overseas enterprises is opened up, it will further drive the cross-border RMB receipts and payments of current and capital items. This is mutually confirmed by the fact that in recent years, the proportion of RMB assets in the external assets of my country's banking industry has increased significantly, from 8% at the end of 2015 to 29%, while the proportion of US dollar assets has decreased from 73% to 51%. At the end of 2024, my country's banking industry's external assets will be 1.6 trillion US dollars, of which deposits and loans account for 60%; RMB assets account for 35% of deposits and loans, which is higher than the proportion of RMB assets in the overall external assets.

Figure 14 The cross-border receipts and payments of RMB used for ODI have increased significantly

Data source: WIND, China Securities Research Institute

The use of RMB in cross-border business has increased significantly. According to the "2024 RMB Internationalization Report" released by the People's Bank of China, in 2023, the amount of cross-border RMB receipts and payments in goods trade and service trade accounted for 24.8% and 31.9% of the amount of cross-border RMB receipts and payments in the same period, respectively. From January to August 2024, the above proportions were 26.5% and 31.8% respectively; in 2023, the total amount of cross-border RMB receipts and payments in direct investment was 7.6 trillion yuan. Increasing the use of RMB in cross-border business will help domestic companies avoid exchange rate risks, reduce the impact of currency mismatches, and deepen industrial chain and supply chain cooperation with other countries.

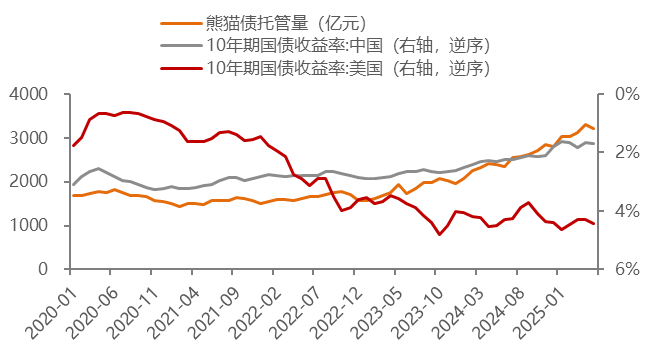

The financing cost of RMB is relatively low. As the Federal Reserve continues to postpone the pace of interest rate cuts and the People's Bank of China maintains a moderately loose monetary policy orientation, the interest rate gap between China and the United States continues to invert, the role of RMB as a financing currency has increased, and the issuance scale of panda bonds has increased significantly. In 2024, a total of 109 panda bonds will be issued with a total amount of 194.8 billion yuan, and the average issuance rate is 2.33%, a record low. As of the end of May 2025, the total amount of panda bonds held by the Shanghai Clearing House is 322.4 billion yuan.

Figure 15 The inverted interest rate differential between China and the United States increases the attractiveness of panda bonds

Data source:

WIND, Zhongtai Securities Research Institute

Currently, digital currencies are surging, and recently a wave of stable currencies has been set off around the world. Stablecoins are conducive to improving the liquidity of the corresponding currency, and the money supply will increase significantly. Therefore, under the wave of commercial institutions issuing stablecoins, the global monetary system faces the opportunity of reconstruction. my country should seize this historical opportunity and significantly increase the proportion of RMB in international payments, settlements, financing and reserves.

Framework suggestions for accelerating the pace of RMB exchange rate reform

First, further expand the openness of the capital account.

In the 2024 "Article IV Consultation Report", the IMF pointed out that "the Chinese authorities have increased the availability of RMB assets by easing capital flows and simplifying foreign investment procedures". It is recommended that, under the premise of controllable risks, the management system and access services of qualified foreign investors should be further optimized, a unified application approval framework should be established, the above-mentioned cross-border channels should be appropriately "widened" or "opened up", and pilot foreign investors should realize investment in various cross-border interconnection mechanisms through a single account to improve the efficiency of capital use.

Further promote the high-level opening of the capital market. In recent years, with the opening and optimization of interconnection channels such as the Shanghai-Hong Kong Stock Connect, Bond Connect, Swap Connect, and Cross-border Wealth Management Connect, restrictions on direct investment in the interbank market and the QFII/RQFII system have been continuously relaxed, and the "pipeline opening" and "institutional opening" of the financial market have been jointly promoted, and the channels for foreign investors to hold onshore RMB assets have become more diverse and the procedures have become more convenient.

At the same time, enrich risk management and hedging tools, and orderly relax restrictions on foreign investors' participation in derivatives markets such as options and futures. Increase the allocation ratio of global high-quality assets.

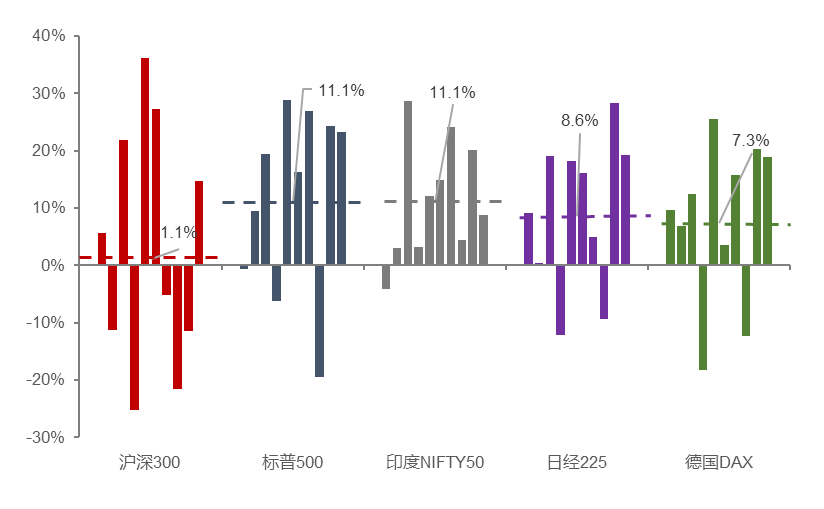

For domestic investors, it is advisable to further expand the scope of their permitted investments. Judging from the returns of major global stock indices over the past 10 years, the average annual return of the CSI 300 Index (3942.7620, 6.68, 0.17%) is 1.1%, which is significantly lower than the S&P 500 (11.1%), India's NIFTY50 (11.1%), Nikkei 225 (8.6%), and Germany's DAX (7.3%). To better preserve and increase the value of assets, funds should be allocated to places with high global investment returns. For example, the world's largest pension fund, the Government Pension Investment Fund (GPIF) of Japan, has continued to increase the proportion of overseas asset allocation in recent years. Currently, domestic stocks, foreign stocks, domestic bonds, and foreign bonds each account for 25%. As of the end of 2024, GPIF will manage assets of 258.69 trillion yen (about 1.73 trillion US dollars), of which the United States is the largest overseas asset destination, with assets allocated to the United States accounting for nearly 30%.

Compared with the situation in my country, as of the end of May, my country's QDII investment quota was only US$167.789 billion, of which insurance was only about US$40 billion; survey data from the Insurance Asset Management Association showed that by the end of 2024, the proportion of overseas investment in the insurance industry's total assets was only 1.59%. In order to further improve the investment return rate of insurance funds, it is recommended to expand the opening of capital accounts and allow insurance funds to moderately increase their allocation of overseas high-quality assets.

Figure 16 Annual changes in major stock indices over the past 10 years (%)

Source: WIND, China Securities Research Institute

Note: The dotted line is the average return rate of the index over the past 10 years

Second, provide foreign exchange convenience for enterprises and residents.

Regarding the corporate sector, we will continue to promote the upgrade, expansion and optimization of the pilot program of the integrated foreign currency and RMB fund pool business of multinational corporations. The pilot program of the integrated foreign currency and RMB fund pool business of multinational corporations aims to improve the efficiency of cross-border fund management and support the global operation of enterprises. As of June 2025, the pilot policy has been upgraded to "Version 3.0", covering more than 26 provinces and cities across the country, benefiting a large number of leading enterprises, and helping enterprises to effectively reduce their capital costs through fund collection and surplus and shortage adjustment, centralized payment and collection of current account funds, and net settlement.

It is recommended to further extend the policy dividends to the central and western regions, small and medium-sized enterprises, etc. At the same time, special regulatory areas such as free trade zones and free trade ports have launched different versions of integrated foreign currency and RMB fund pools. It is recommended to merge them appropriately according to actual conditions to reduce corporate compliance costs.

Regarding the resident sector, we will study the appropriate increase in the annual foreign exchange purchase quota limit for individuals. Appropriately relaxing the limit on foreign exchange purchases to "keep foreign exchange in the hands of the people" will help reduce the pressure on the allocation of foreign exchange reserves to U.S. Treasuries, which is consistent with the policy orientation of diversifying foreign exchange reserves.

We try to estimate the annual scale of individual foreign exchange purchases. (1) According to the data of the State Administration of Foreign Exchange, the cumulative scale of foreign exchange sales by banks on behalf of customers in 2024 is US$2,433.6 billion, which includes the foreign exchange sales business handled by banks for corporate and individual customers.

(2) Estimate the proportion of individual foreign exchange purchases. The Lanzhou Central Branch of the People's Bank of China mentioned in "The Situation, Characteristics and Regulatory Countermeasures of Individual Foreign Exchange Purchases - Taking Gansu Province as an Example" that "in 2015, the total amount of individual foreign exchange purchases in the province accounted for 17% of the total amount of foreign exchange sold by banks on behalf of customers"; the Yunnan Branch of the People's Bank of China disclosed at the press conference on the financial operation situation in the first quarter of 2024 that the amount of individual foreign exchange purchases in Yunnan Province in that quarter was US$380 million, an increase of 3.4% from US$370 million in the same period of 2019 before the epidemic. The total amount of foreign exchange sold by banks on behalf of customers in the province in that quarter was US$2.56 billion, which means that the proportion of individual foreign exchange purchases was 15%. Taking into account the economic development level and degree of openness of the region, it is estimated that the proportion of individual foreign exchange purchases in the country to bank foreign exchange sales is 20%-30%.

(3) Therefore, it is estimated that the scale of individual foreign exchange purchases in 2024 will be about US$600 billion. The current foreign exchange management regulations limit the annual foreign exchange purchase quota for individuals to the equivalent of US$50,000. It can be seen that the above amount is far less than the total quota for residents nationwide. Further relaxation of the upper limit does not seem to cause excessive exchange growth. Of course, this may involve the problem of the gap between the rich and the poor. For example, the wealthy have more willingness to exchange foreign exchange. It is necessary to comprehensively consider the "feasibility" and "completion" of foreign currency-denominated asset allocation and the "economic account" of holding currency under the expectation of RMB stability and strength.

Third, study and promote the legislation of RMB stable currency.

Recently, the US Senate passed the "GENIUS Act" and the Hong Kong Legislative Council passed the "Stablecoin Ordinance". Although the two differ in the issuer, regulatory requirements, and innovation tolerance, they also reflect the high attention paid to the development and compliance operation of stable currency. The core significance of stable currency is not to replace legal currency, but to provide a digital and efficient cross-border circulation method for legal currency. The role of stable currency is to expand the liquidity of the linked currency and help strengthen the international currency status of the linked currency.

Therefore, we can follow the international development trend and study the pilot RMB stablecoin within a certain scope (such as offshore, free trade zones, etc.) and certain business scenarios (such as "One Belt, One Road" cross-border trade, RMB settlement of commodities, etc.), and gradually improve the relevant regulatory system and gradually upgrade it to law. According to the principle of "same activities, same risks, same supervision", the quasi-currency or quasi-securities attributes of stablecoins should be clarified, and the RMB reserve asset standards should be formulated to guide the standardized development of stablecoins, protect the rights and interests of financial consumers, and prevent systemic financial risks and illegal financial activities.

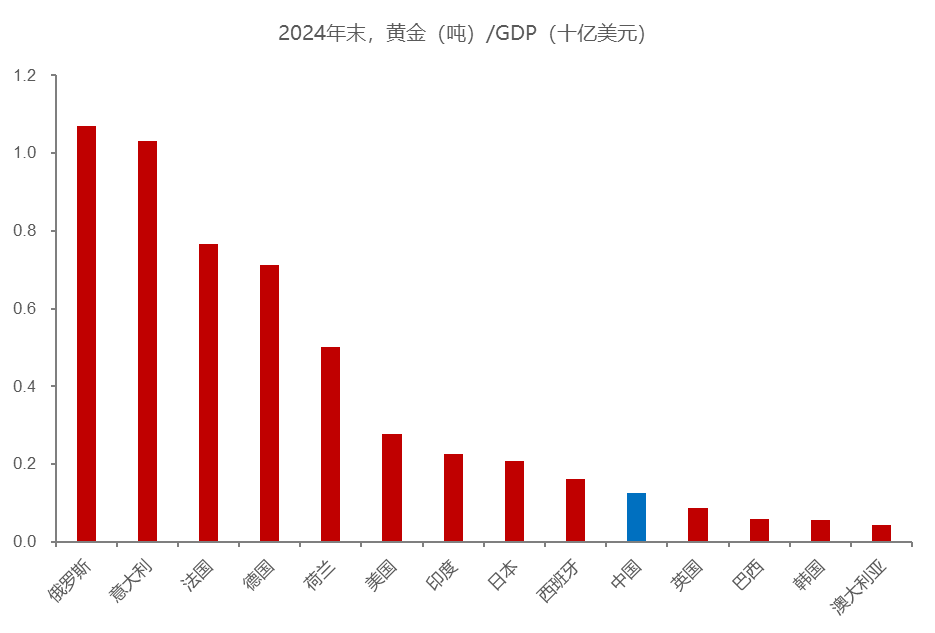

Fourth, the central bank should gradually reduce its holdings of US dollars and US dollar assets (such as US bonds), continue to increase its holdings of gold, and it is recommended to increase its holdings of low-valued high-quality equity assets globally.

Based on the overvaluation of the US dollar (excessive liquidity leads to too low liquidity premium, and the credit of the US dollar has a downward trend, such as the international rating agency Moody's recently downgraded the US sovereign credit rating), the US debt balance is too large, as the world's largest foreign exchange reserve, China should prepare for a rainy day and continue to increase its gold holdings, while considering increasing its holdings of low-valued high-quality equity assets around the world, such as the current overall valuation level of Hong Kong stocks, which is the lowest among the world's mainstream stock markets.

Moreover, increasing gold holdings is conducive to improving the credit of the RMB and reducing the credit premium. As of the end of May 2025, the current gold reserves of my country's central bank are 73.83 million ounces, while its foreign exchange reserves are as high as 3.29 trillion US dollars. In contrast, the Federal Reserve's gold reserves are as high as 262 million ounces, and its foreign exchange reserves are only 29.8 billion US dollars.

Figure 17 my country's gold reserves account for a low proportion of GDP

Source: Wind, China Securities Research Institute

It is obvious that the United States uses the privilege of the dollar to levy "seigniorage" on the world, and at the same time uses the excellent liquidity of the dollar to maintain its strong position and high valuation. But everything has its pros and cons. The high valuation of the US dollar has also led to huge fiscal deficits and trade deficits in the United States, which in turn affects the credit of US debt and the US dollar. As the world's second largest economy, the RMB does not need excessive liquidity, but only needs to increase liquidity to match the size of China's economy.

Therefore, adjusting the asset structure corresponding to foreign exchange reserves has become a top priority.

Accelerating the internationalization of the RMB -

Helps promote China's economic transformation

From a macro perspective, the internationalization of the RMB is conducive to high-quality economic growth. Against the background of RMB appreciation, the GDP growth target can be appropriately lowered in the future.

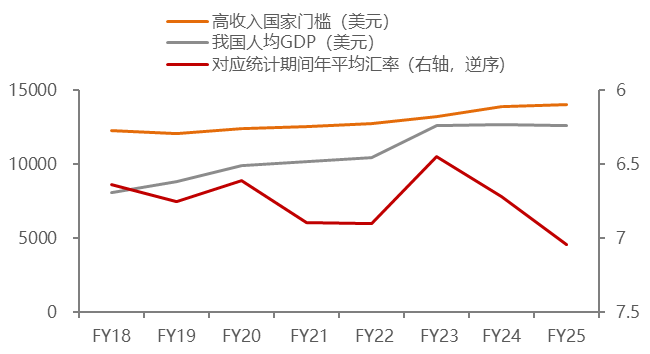

One of my country's long-term goals for 2035 is to "reach the level of per capita GDP of moderately developed countries." The World Bank divides the world's economies into four groups according to their per capita gross national income (GNI), namely low-income, lower-middle-income, upper-middle-income and high-income. The per capita gross national income is measured in US dollars. Usually, middle- and low-income countries are called developing countries, and only by entering high-income countries can they become developed countries. For example, the classification standard used from July 2024 to June 2025 is that countries with a GDP of more than US$14,005 are high-income countries. From this definition, factors such as economic growth, population growth, inflation, and exchange rates will have an impact on the realization of the 2035 vision.

Therefore, a moderate appreciation of the RMB exchange rate through the internationalization of the RMB will help achieve my country's medium- and long-term development goals; that is, if the RMB appreciates slightly, it will reduce the lower limit of the annual economic growth rate to a certain extent.

Figure 18 The depreciation of the RMB makes it difficult for my country to enter the high-income threshold

Source: World Bank, WIND, China Securities Research Institute

Joy

Joy