Author: Tanay Ved Source: Coin Metrics Translation: Shan Ouba, Golden Finance

Abstract

Wrapped assets enhance the utility and interoperability of cross-blockchain tokens, helping to maintain liquidity and promote decentralized financial (DeFi) activities.

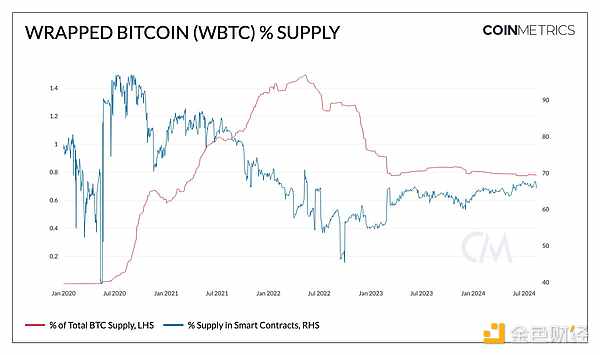

WBTC is one of the largest wrapped assets at present, with a market value of US$9 billion. Its supply is 154,000, accounting for 0.8% of BTC's current supply and 67% of Ethereum smart contract supply.

BitGo’s plan to transfer custody of WBTC to a cross-jurisdictional joint venture with BiT Global, in which Justin Sun and Tron participate, has raised some concerns, prompting the launch of DeFi risk mitigation and new solutions.

Introduction

As the potential market of the crypto ecosystem continues to expand, the demand for tokenization of various forms of value and assets on public blockchains continues to grow. Today, asset classes include not only pure digital assets such as Bitcoin (BTC), but also tokenized representations of underlying assets, ranging from cryptocurrencies (i.e. BTC, ETH) to fiat currencies such as the US dollar and now traditional financial instruments such as government securities. This has given rise to a range of areas such as wrapped assets, stablecoins, and tokenized public securities, enhancing the interoperability and utility of crypto assets.

This article explains the role of tokenized and wrapped assets in the crypto ecosystem, with a focus on Wrapped Bitcoin (WBTC), which is about to be reorganized by BitGo.

The World of Tokenized and Wrapped Assets

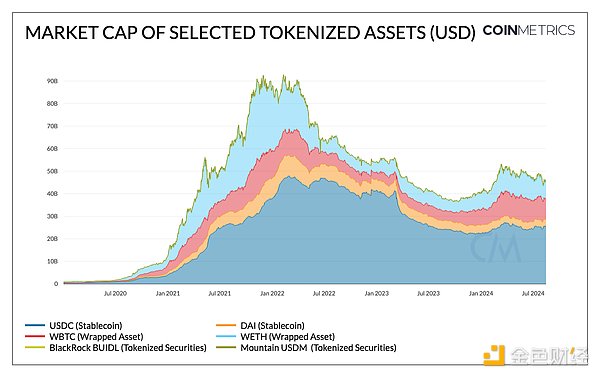

The scope of tokenized assets has expanded significantly to include wrapped assets, stablecoins, and real world assets (RWAs). Although these assets have different uses, they can be classified under the broader category of tokenized assets because they share the common feature of representing the value of different underlying assets.

Source: Coin Metrics Network Data Pro

Wrapped Assets:Wrapped assets are tokens that represent the value of another cryptocurrency, enabling interoperability across blockchain networks. For example, Wrapped Bitcoin (WBTC) is an ERC-20 token that represents Bitcoin and can be used by holders within the Ethereum ecosystem. This category also includes tokens like Wrapped Ether (WETH) (an ERC-20 representation of ETH), Wrapped Liquid Staked Ether (wstETH) (represents ETH staked via Lido), and Wrapped BNB (wBNB). WBTC and WETH are the largest wrapped assets today, with market caps of $9.1 billion and $7.6 billion, respectively.

Source: Coin Metrics Network Data Pro

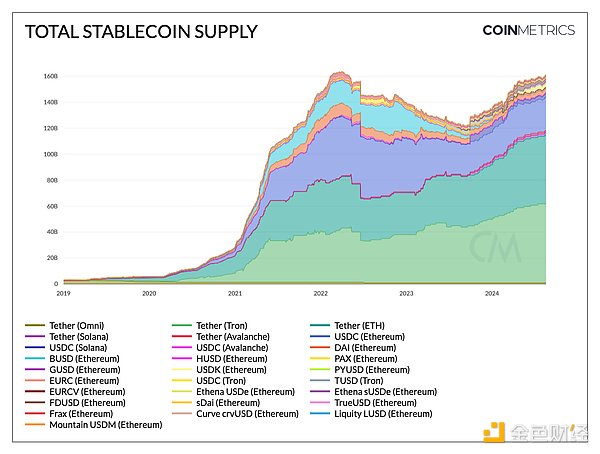

Stablecoins:Stablecoins tokenize a fiat currency like the USD or EUR, or in some cases a basket of cryptocurrencies and traditional assets. For example, USDT and USDC are pegged to the USD, and each stablecoin is backed by cash-equivalent assets held in the issuer’s reserves to maintain a 1:1 value ratio. We have seen the emergence of various categories of stablecoins, from fiat-backed to crypto-backed and more, with the combined market cap of USDT and USDC being around $148 billion.

Source: Coin Metrics Network Data Pro

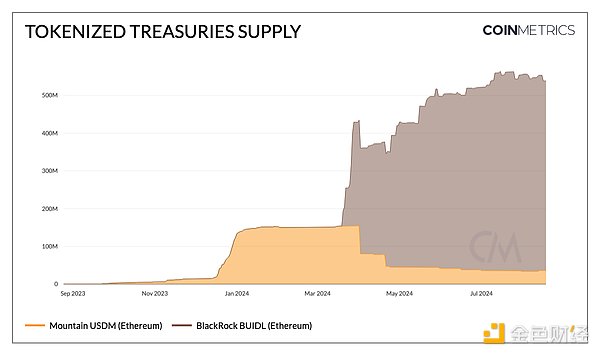

Tokenization RWAs: While tokenized assets are relatively nascent, they include a range of RWAs beyond cryptocurrencies, such as Treasuries, private credit, commodities, and more. For example, BlackRock’s recently launched USD Institutional Liquidity Fund (BUIDL) tokenizes cash, repurchase agreements, and U.S. Treasuries of various maturities to provide traditional investment opportunities to accredited investors and enhance liquidity in traditional markets. BUIDL is the largest in this category, with an estimated market cap of $517 million.

Mechanics of Wrapped Bitcoin (WBTC)

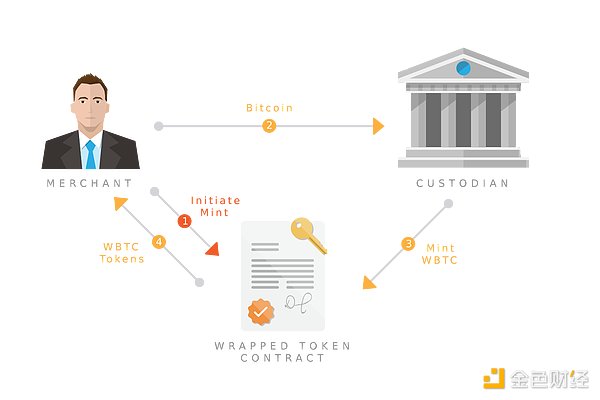

Wrapped assets are created by locking up a cryptocurrency on its native blockchain and issuing an equivalent token on another blockchain. This process spans a variety of models, from centralized approaches using custodians and merchants to relatively permissionless solutions that leverage direct smart contract interactions or a network of participants to reduce potential points of failure.

A typical example is Wrapped Bitcoin (WBTC), a joint initiative launched by REN, Kyber, and BitGo in 2019. WBTC uses a decentralized autonomous organization (DAO) to manage the addition and removal of custodians and merchants, controlled by key holders of multi-signature contracts. BitGo is the main custodian of WBTC, responsible for custody of Bitcoin as collateral for WBTC tokens, while merchants act as intermediaries to facilitate minting and destruction.

Merchants use BitGo to lock BTC and initialize the minting of WBTC, which appears in Ethereum accounts in the form of ERC-20 tokens and is backed at a 1:1 ratio. This allows Bitcoin to be used in Ethereum-based products and services such as DeFi without affecting BTC liquidity. It is also possible to redeem the original BTC by returning WBTC to the custodian's Ethereum account and then destroy it from there.

Source: wbtc.network

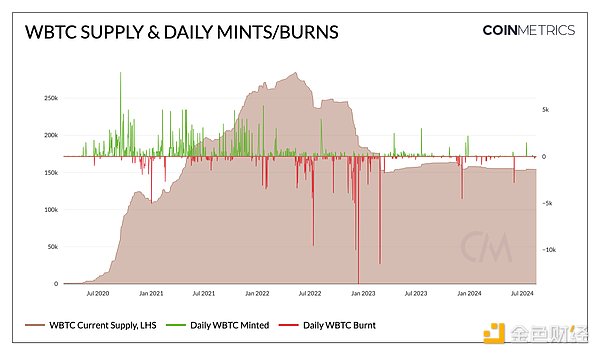

Although there are currently a variety of Bitcoin packaging solutions, each with its own advantages and disadvantages, WBTC The custody model of WBTC has become the most widely adopted model. Currently, there are 154,000 Bitcoins (worth about $9 billion) in custody, and 98,000 Ethereum addresses hold a positive balance of WBTC.

WBTC's custody transformation and BitGo's revenue model

On August 9, BitGo announced plans to restructure the management of WBTC through a joint venture with BiT Global, with a transition period of 60 days. The new structure aims to diversify custody and cold storage, covering multiple jurisdictions, expanding from the current US model to Hong Kong and Singapore. Notably, this partnership will be closely aligned with Justin Sun and the Tron ecosystem, influencing the management of WBTC by granting BiT Global access to 2 of the 3 private keys of the multi-signature contract for supervision.

Traditionally, BitGo has earned revenue by charging fees for the minting and destruction of WBTC. The fee is typically between 0.4% and 0.5%, varying depending on the size of the transaction and market conditions. These operations are transparent and auditable on WBTC's order book and block explorer. For example, in one transaction, BitGo received 52.17193124 BTC as custodian. However, the corresponding minting transaction requested by the merchant shows that only 52.08845615 BTC was minted, which means that BitGo's income is about 0.16% in fees.

Source: Coin Metrics Network Data Pro

Although this reorganization may expand BitGo Influence in Asian markets, but may also affect its revenue model. Sharing custody responsibility for WBTC with BiT Global may lead to changes in how fees are allocated and collected in the future.

WBTC in DeFi: Utility and Risk Management in Custody Changes

Wrapped assets are an essential component in the decentralized finance (DeFi) ecosystem. They enhance the liquidity, interoperability, and usability of cryptocurrencies across different blockchain networks and their applications. As a result, the average transfer size of WBTC is almost 7 times that of BTC, with a typical WBTC transfer amount of $76,000 compared to $11,000 for BTC. While WBTC accounts for about 0.8% of Bitcoin's current supply of 19.7 million, a large portion of it (about 67% of its supply) is in Ethereum-based smart contracts, which proves its use in DeFi.

Source: Coin Metrics Network Data Pro

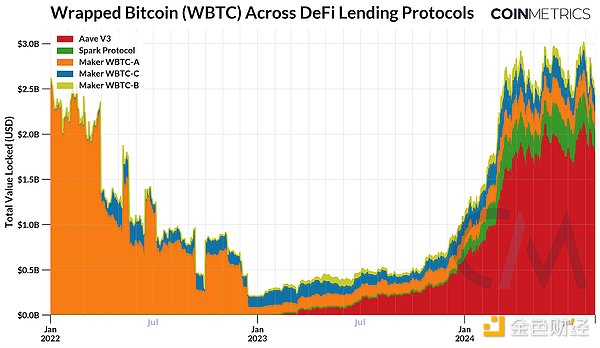

WBTC and other wrapped assets and derivative assets are widely used as DeFi Collateral on lending platforms, used to borrow other assets or earn liquidity interest, while also being traded between DEXs. Due to WBTC's debt interest, it constitutes a significant source of income for protocols such as Maker, SparkLend, and Aave v3. There are a total of about 50,000 wrapped bitcoins (currently worth about $3 billion) in lending protocols on Ethereum.

Source: Coin Metrics ATLAS

Given WBTC’s custody transition, well-known DeFi The lending platform’s governance body (DAO) has proposed various risk management strategies to reduce risk in its ecosystem. Aave DAO has decided not to make any major changes to its market at this time. The DAO has not decided to delist WBTC itself, as the total market size of Aave V3 is $14 billion, of which about 34,000 BTC (about $1.9 billion) is held, and risk manager Chaos Labs says it generates about $6 million in annual revenue for the protocol.

However, MakerDAO has taken a more decisive stance. They executed a proposal to phase out WBTC on the Maker and SparkLend platforms, aiming to reduce the risk of the Dai stablecoin. This move resulted in changes to the debt ceiling and stability fee of the WBTC vault due to the risks posed by WBTC’s new operating structure. As a result, users can no longer obtain WBTC collateral, effectively limiting its use in these protocols.

Conclusion

The reorganization of WBTC into a joint venture’s custody business, while intended to achieve geographic diversification, has also raised concerns across the crypto ecosystem. Given WBTC’s important role in the on-chain ecosystem, this shift has brought custody and operational risks to the forefront, spurring interest in permissionless alternatives such as Threshold BTC (tBTC) and new entrants such as Coinbase’s cbBTC. As the impact of this change unfolds, DeFi protocols and other stakeholders are likely to implement risk mitigation measures - especially as more tokenized assets enter the interconnected on-chain ecosystem.

Preview

Gain a broader understanding of the crypto industry through informative reports, and engage in in-depth discussions with other like-minded authors and readers. You are welcome to join us in our growing Coinlive community:https://t.me/CoinliveSG

Cheng Yuan

Cheng Yuan