Author: David Han Source: DAOSquare

Key Takeaways

While USD momentum has stalled, we believe the upcoming PPI and CPI data on May 14 and 15 will likely determine the next major direction for the USD. We believe the Fed will continue to prioritize fighting inflation over early signs of a cooling labor market.

Grayscale Bitcoin Trust (GBTC) saw inflows in its first two days since transitioning to an open-end fund, marking an important completion of a structural capital rotation for the asset.

Aave recently revealed plans for the fourth iteration (V4) of its protocol as part of the Aave 2030 long-term vision, with a focus on supporting their GHO stablecoin, which is scheduled to launch in Q2 2025.

Market View

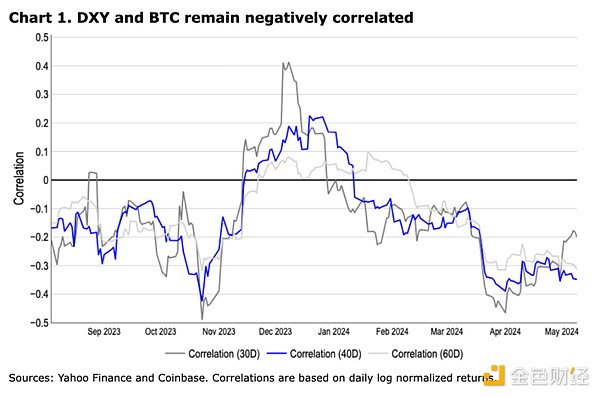

The continued lack of clear macro direction has led to Bitcoin's continued decline in recent times. Altcoins have also shown a similar situation, with correlations within the crypto asset class remaining close to their highest point since the beginning of the year. The current uncertainty in macro factors proves our thesis in our April Outlook that macroeconomic conditions will continue to dominate BTC performance (with altcoins following closely behind), and the market is beginning to look for other catalysts besides the Bitcoin halving as US spot ETF inflows taper off. Although the ECB and other central banks have reiterated plans to cut interest rates in the summer, higher-than-expected US inflation data has raised market concerns about the Fed delaying rate cuts. Expectations of a prolonged US rate cut have led to a stronger US dollar, which in turn has weighed on the broader crypto market due to its key role as the quote currency on most crypto exchanges.

However, the momentum of the dollar’s strength has stalled following a more dovish-than-expected Fed meeting, with market expectations (based on Fed Funds futures) for the first rate cut shifting from November to September 2024 following the weaker-than-expected non-farm payrolls data on May 3. The higher-than-expected initial jobless claims on May 9 further added to the drive for faster rate cuts, as the Fed has a dual mandate to not only fight inflation but also keep unemployment low.

Nevertheless, we do not believe that changes in the US unemployment rate (currently at 3.9%) will be a focus for the Fed in the near term, as it remains close to historic lows. Indeed, we continue to believe that the US economy will be supported by technological progress and government spending, and is not on the verge of entering a contraction. At the next Federal Open Market Committee (FOMC) meeting, we believe the Fed's attention and rhetoric will remain focused on inflation indicators, which highlights the importance of the upcoming PPI and CPI data on May 14 and 15 as expected macro catalysts, especially if they are higher than expected.

Separately, Grayscale Bitcoin Trust (GBTC) saw inflows in the first two days since its transition to an open-end fund. Although the source of these inflows is unclear because they have higher management fees (1.5%) compared to similar spot products (less than 0.5%), this development marks the completion of a structural capital rotation. We believe a significant portion of early GBTC outflows were related to bankruptcy proceedings (e.g., Genesis and FTX), profit realization on GBTC discount trading (40% discount to NAV a year ago), and a shift to low-fee products (<0.5% vs. 1.5%). While we have previously cautioned against using flow data as a preferred indicator of future price action, going forward we do not expect structural distortions in flow data.

On-Chain: Aave’s Progress

Meanwhile, Aave recently revealed plans for the fourth iteration (V4) of its protocol as part of the Aave 2030 long-term roadmap. The proposed V4 incorporates architectural improvements including a unified liquidity layer (for flexible scaling of borrowing functionality), fuzzy rates (for interest rate curves previously controlled by governance), and liquidity premiums (adjusting borrowing rates based on collateral composition). V4 also focuses on strengthening the use of its GHO stablecoin and incorporates other improvements such as improved risk management and liquidation engines.

While the proposed mainnet launch date is in Q2 2025, we view this announcement (along with other major announcements from existing DeFi protocols like Uniswap and Maker this year) as an early roadmap for DeFi protocols to mature in their core functionality, even as they maintain market dominance and continue to innovate in other areas. This could set a precedent for new protocols in terms of decentralization, long-term token utility, and iterative feature rollouts.

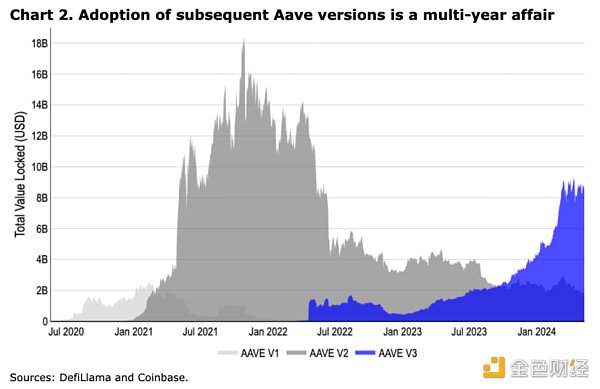

Scaling DeFi protocol functionality is a technical challenge, especially compared to traditional web2 companies whose mantra is to "move fast and break things." Successful DeFi protocols rarely scale their initial architecture in a way that is transparent to end users. Instead, they deploy new versions and incentivize active liquidity migrations. This applies not only to Aave, but also to other leading protocols like Uniswap, Curve, Pendle, and others. These cross-version liquidity migrations are a difficult task as users need to actively switch. In fact, despite the launch of Aave V3 as early as 2022, it was not until September 2023 that Aave V3 surpassed Aave V2 in total locked value (TVL). We believe that the adoption cycle of Aave V4 may also go through a similar process.

Despite the large number of functional improvements in the new version, the cautious migration of liquidity highlights the relative importance of the Lindy effect in the DeFi market. That is, the trust gained from market time seems to be more important than new mechanisms that may be attractive to a small number of users. The adversarial environment of decentralized technology means that time is often the most reliable way to determine the security of the protocol, which is more important than audits and theories. We think this highlights the characteristics of the immutability of smart contracts and the financialization of web3 products, that is, how to maintain stable security in rapid innovation. As a result, we believe the long-term adoption cycle for crypto products may differ from what we see in web2 markets. The consequences of a web3 finance vulnerability are far more severe for end users than a web2 data vulnerability that does not disrupt core application functionality.

In addition, the Aave 2030 roadmap appears to compete with Maker’s Endgame, especially Aave’s renewed focus on its GHO stablecoin. Many of the elements proposed in Aave 2030, such as Aave’s specific network, GHO’s cross-chain liquidity layer, augmented reality asset (RWA) integration, and updated protocol branding, are reminiscent of Maker’s Endgame vision.

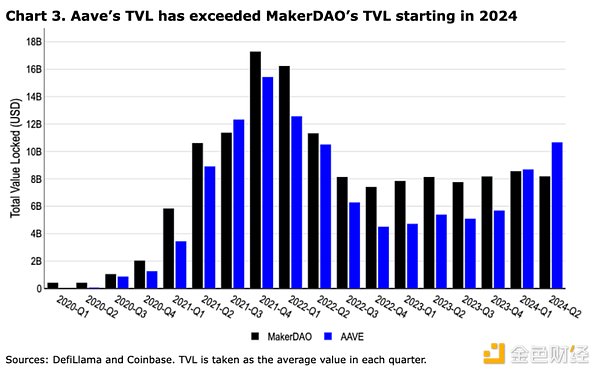

With TVLs of $10.5 billion and $8.2 billion, respectively, both protocols are significant sources of lending in the space. However, while Maker borrowers are limited to DAI, Aave supports lending across a wide range of assets beyond its own GHO stablecoin. Given that DAI’s market cap has only grown from $5.3 billion to $5.4 billion YTD, questions remain around its ability to increase cross-chain adoption and gain market share. That said, it is interesting to note that Aave appears to be focusing on the decentralized stablecoin space, even though the market for this space has been shrinking relative to centralized stablecoins like USDC. With DAI demand on hold, Aave actually surpasses Maker as the largest lending DeFi protocol by early 2024. However, we are still in the early days of web3. While Maker’s Endgame plan and Aave’s 2030 roadmap offer a promising vision for the future of these protocols, we believe these developments may be overlooked by the market in the short term as the macro environment remains the anchor of attention in the near term.

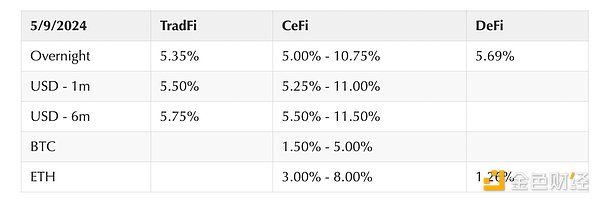

Crypto and Traditional Finance

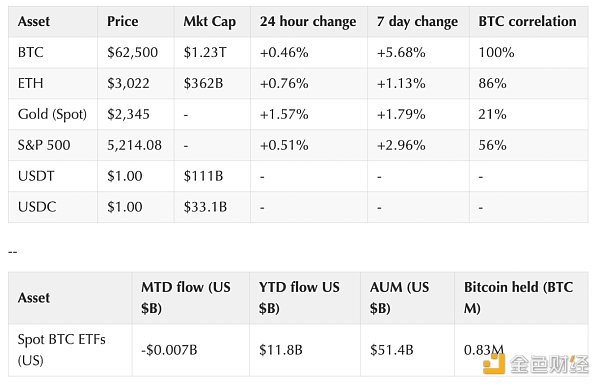

Source: Bloomberg (as of 4 p.m. Eastern Time on May 9)

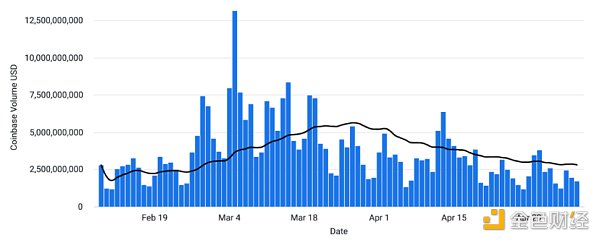

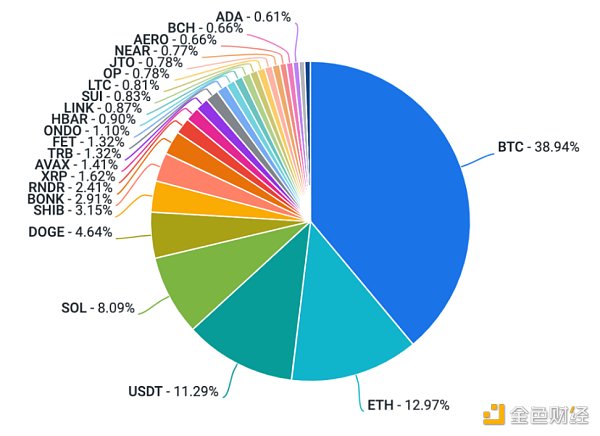

Coinbase Exchange and CES Insights

Coinbase platform transaction volume (US dollars)

Coinbase platform transaction volume (asset ratio)

Funding rate

Noteworthy Crypto News

Institutions

Regulatory

The U.S. Securities and Exchange Commission (SEC) issued a Wells Notice to Robinhood Crypto for suspected securities violations (The The Block)

QCP receives in-principle approval from Abu Dhabi regulator (Coindesk)

SEC files final response in Ripple XRP case (Cointelegraph)

General

Friend Tech sees resurgence in activity following V2 launch (The Defiant)

Bitcoin network surpasses 1 billion on-chain transactions (The Defiant)

Vitalik Buterin proposes EIP-7702 to improve account abstraction on Ethereum (The Block)

Coinbase

Friend Tech sees resurgence in activity following V2 launch (The Defiant)

Bitcoin network surpasses 1 billion on-chain transactions (The Defiant)

Vitalik Buterin proposes EIP-7702 to improve account abstraction on Ethereum (The Block)

Coinbase class=" list-paddingleft-2">Coinbase Benefits from ‘Hostile Regulatory Environment’: Bitwise (The Block)

Global Perspective

Europe

UK FCA Says 30% of Financial Crimes Will Come from Crypto Firms in 2023 (Crypto News)

Europe’s Second-Largest Bank BNP Paribas Buys Shares of BlackRock Spot Bitcoin ETF: SEC Filing (Decrypt)

Crypto Banking Firm BCB Group Receives Regulatory Approval in France as an Electronic Money Institution and Digital Asset Service Provider

Vodafone Looks to Integrate Crypto Wallets with SIM Cards (TradingView)

German Central Bank President Calls for Rapid CBDC Adoption to Remain Competitive (CryptoSlate)

Asia

Hong Kong Spot Bitcoin and Ethereum ETFs See $11M in First Launch (Watcher Guru)

Chinese Police Arrest Suspect Who Created Numerous Fake Identities to Claim STRK Airdrops (Crypto Briefing)

PwC China and Xalts Form Strategic Partnership in Blockchain and Tokenization (RWA Tokenizer)

South Korea bans cryptocurrencies in updated donation law (CoinTelegraph)

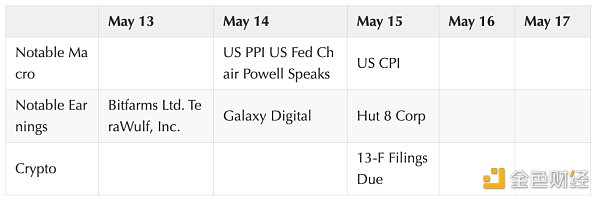

Big events in the coming week

Sanya

Sanya