Why Bitcoin prices fell after Trump reached a US-China tariff deal

While the stock market surged after the U.S.-China trade deal was announced, Bitcoin prices unexpectedly fell.

JinseFinance

JinseFinance

Author: Chetanya, Researcher at The Spartan Group; Translation: Jinse Finance xiaozou

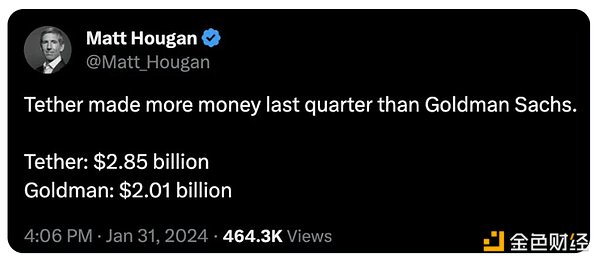

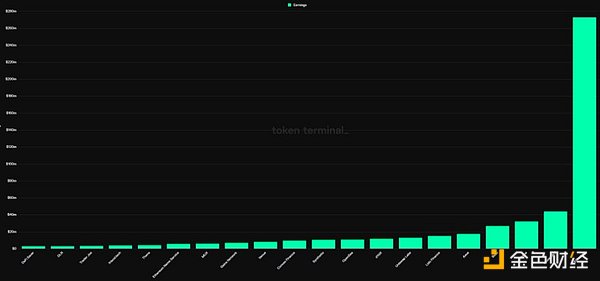

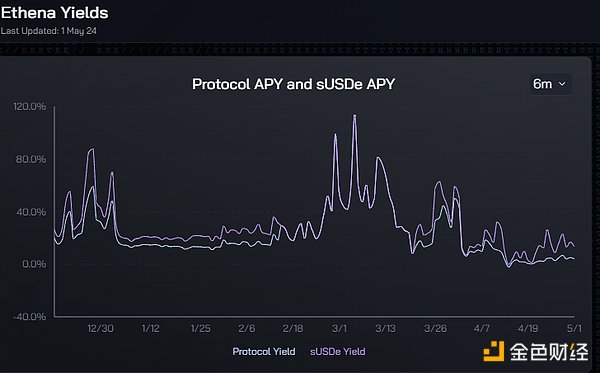

Ethena Labs is the fastest growing player in the high-profit field of stablecoins - as can be seen from the skyrocketing returns of Tether and Maker, etc.

I am a big supporter of non-fiat-backed stablecoins, and projects that can solve the stablecoin trilemma will have a huge market opportunity.

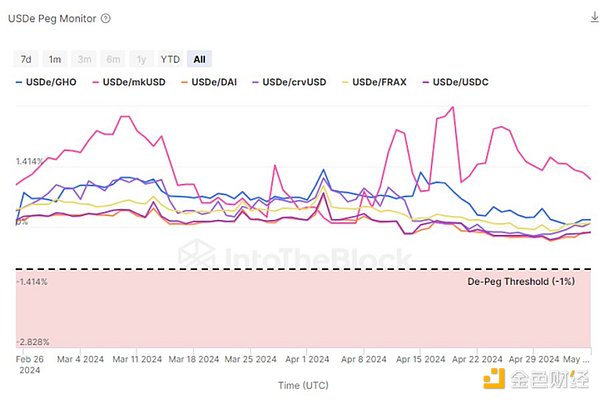

USDe's TVL soared to $2.3 billion. Ethena quickly became the highest-yielding DeFi protocol, second only to ETH and MKR.

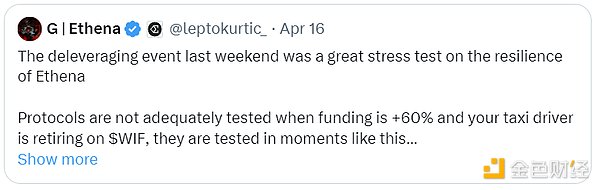

Interestingly, I was surprised by the TVL resilience after the recent leverage craze, and the protocol's perfect management of redemptions and USDe pegs. This will boost market confidence in the product and attract a large number of USDe holders when the market rebounds.

sUSDe provides a scalable way to earn double-digit market-neutral returns, making it a valid alternative to USDT/USDC. As the Anchor protocol showed in the last cycle (ATH TVL: $18 billion), the demand for stable returns is very large. I hope that traders, exchanges, funds, etc. will keep a portion of USDe stablecoins while gradually deploying funds.

Seraphim and his team quickly integrated USDe into large DeFi protocols, including Frax Finance, Pendle, Morpho Labs, etc., and USDe showed early signs of DeFi expansion. With the upcoming CeFi integration (Bybit is the first), USDe has a good chance of becoming one of the largest stablecoins.

The growth of BTC and SOL collateral may not be taken into account. This could greatly expand the TAM and bring USDe's TVL to over $10 billion in this cycle.

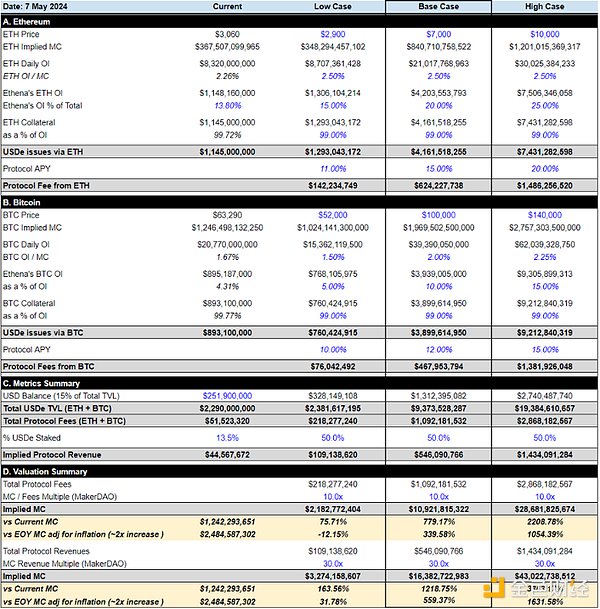

When ENA is compared with lending protocols and stablecoin protocols in terms of TVL, fees, and revenue indicators, ENA seems to be overvalued in the fully diluted case. However, in the MC (market value) dimension, the valuation seems reasonable.

I think MC is a more appropriate indicator at least in the short term, as the first major unlock will be opened in early 2025. Before that, the floating range will remain around 10-20%.

Baseline, I expect ENA TVL to grow to about $10 billion. This will enable it to earn over $1 billion in fees and generate over $500 million in revenue depending on the utilization of USDe (or the sUSDe exchange rate). ENA's upside could be 5-10x, which would imply a market cap of $5-10 billion.

These forecasts assume that this cycle is as prosperous as the last one.

Ethena's design risks are largely well handled. However, a more pressing question is how they will manage TVL once the points/Shards program ends. They are able to generate high protocol revenues and offer an abnormally high exchange rate to sUSDe holders, largely due to the low collateralization rate of USDe (currently around 13.5%). Essentially, currently USDe holders are incentivized not to stake to earn more “points/Shards”.

After the points program ends, USDe holders will not have accumulated any value, which means there is no natural demand for USDe. I expect some of the gains to be shared with USDe holders, or the sUSDe/USDe exchange rate will approach 100%, reducing protocol revenue and thus reducing the utility of ENA.

But I believe that Ethena’s founders and team will have some strategies to deal with this issue in the future.

While the stock market surged after the U.S.-China trade deal was announced, Bitcoin prices unexpectedly fell.

JinseFinanceEthena Labs has refuted claims of unfairly staking 180 million ENA tokens in its crypto farming event. Amidst mixed reactions and a 6% drop in ENA’s value, the token has since rebounded. Ethena assured stakeholders of transparency and adherence to protocol.

Catherine

CatherineIsn't it said that crypto is a hedge against geopolitical crises? Now when there is a war, the price is falling. What's going on? Recently, Iran and Israel have been attacking our wallets back and forth. It was not like this n years ago.

JinseFinanceGoogle Removes Bitcoin, Ethereum, Solana Price Charts From Search.Google’s removal of cryptocurrency price charts has led to uncertainty, with declining search interest adding to a broader shift in how the public interacts with digital assets.

WenJun

WenJunEthena’s native token is losing momentum; will a turnaround effort risk everything?

JinseFinanceBloomberg reveals that concerns over inflation and uncertainty have led to decreased trading volumes on cryptocurrency exchanges, causing Bitcoin, ETH, SOL, XRP, and SHIB prices to plummet.

Alex

AlexA combination of on-chain, fundamental and technical factors point to more pain ahead for too many bulls.

Cointelegraph

CointelegraphNetwork outages and decreasing smart contract reserves add further downside pressure to SOL price.

CointelegraphA mix of on-chain, fundamental, and technical factors suggests more pain for Ether bulls ahead.

CointelegraphSOL price can preserve the bullish bias, however, as its two multi-month support levels converge for the first time.

Cointelegraph