Every August, central bankers from around the world gather in Jackson Hole, Wyoming, a ski resort in the central United States, for a "symposium" organized by the Federal Reserve Bank of Kansas City. Bankers take the opportunity to discuss monetary policy and its effectiveness in "managing the economy," specifically "controlling" inflation and providing the right amount of "liquidity" to the financial system.

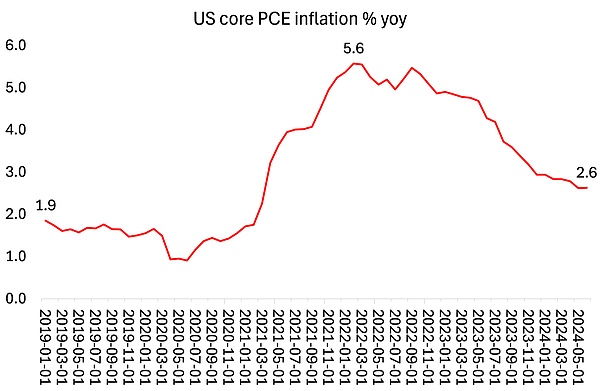

This year's symposium comes as the Federal Reserve faces the dilemma of whether to cut its "policy" interest rate, as the economy shows signs of cooling but inflation remains "firmly" falling toward the Fed's 2% target. The so-called policy rate sets the floor for all borrowing rates for households and businesses in the United States (and most of the world). It is currently at its highest level in 23 years.

In early August, financial markets panicked and began selling corporate stocks in response to the Fed's decision not to cut the policy rate at its July meeting, followed by July employment data showing a sharp drop in net job growth and a rise in the unemployment rate. However, markets gradually calmed down after the latest inflation data showed a further (modest) decline in inflation, especially as Fed Chairman Jerome Powell began to make it clear that the central bank would cut interest rates at its September meeting. Powell reiterated this view in his speech at the Jackson Hole Economic Symposium on Friday. "We have resumed progress towards our 2% objective. I am increasingly confident that inflation will return to 2% sustainably... The labor market has cooled significantly from its previous overheating. The labor marketseems unlikely to be a source of rising inflationary pressures in the near term... We do not want or welcome a further cooling of labor market conditions.Now is the time for a policy adjustment. The way forward is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks."

Powell then claimed that the Fed's monetary policy has prevented a recession in the US economy and reduced inflation. “Our restrictive monetary policy has helped to restore the balance between aggregate supply and aggregate demand, ease inflationary pressures, and ensure that inflation expectations remain anchored.” He argues that prices are rising because of a combination of increased consumer spending and supply shortages. That’s true, but the question is which factor was dominant. Most, if not all, studies of the inflationary period show that supply factors dominated, not excess consumer demand, government spending or “excessive” wage growth – arguments central bankers used to justify big rate hikes.

But Powell hinted at the real reason in his speech, saying: “High inflation is a global phenomenon that reflects a shared experience: rapidly growing demand for goods, tight supply chains, tight labor markets, and sharply higher commodity prices.” This also explains the subsequent decline in inflation: “The supply and demand distortions caused by the pandemic, as well as the severe shocks to energy and commodity markets, were important drivers of high inflation, and the reversal of these factors was a key part of the decline in inflation. These factors took much longer to dissipate than expected, but ultimately played an important role in the subsequent deflation.”

Nevertheless, Powell continued to promote the claim that the central bank’s “restrictive monetary policy” played a role by“moderating aggregate demand.” Powell also reiterated the myth that the central bank’s monetary policy helps anchor inflation expectations,” which is allegedly the key to controlling inflation. But this is again nonsense, as recent research clearly shows that “expectations” have little effect on inflation. As Fed economist Rudd recently summarized:“Economists and economic policymakers believe that households’ and businesses’ expectations of future inflation are the key determinant of actual inflation. A review of the relevant theoretical and empirical literature shows that this belief rests on extremely shaky foundations, and that uncritical adherence to it can easily lead to serious policy errors.”

Powell has also proposed other mainstream concepts to explain inflation and to justify their “restrictive monetary policy.” The first is the so-called “natural rate of unemployment” (NAIRU). The theory holds that there is an unemployment rate that is low enough to sustain economic growth without inflation, but not high enough to indicate a recession. But the NAIRU is another feast of ephemeral and fickle nature that cannot be measured.

The NAIRU is related to the so-called Phillips curve, a product of Keynesianism that holds that when the labor market is too “tight” (i.e., the unemployment rate is below the NAIRU), excessive wage increases will lead to inflation. There is a “trade-off” between wages and inflation. This theory was empirically refuted in the 1970s when the economy experienced “stagflation” (i.e. rising unemployment, slow growth and rising inflation).

Since then, several studies have shown that there is no “curve” at all, and that there is no correlation between movements in unemployment, wages and inflation.

In fact, Powell’s comments on the NAIRU are the exact opposite of what he said at the 2018 Jackson Hole Symposium. At the time, Powell suggested that there might be no use in following the usual traditional “indicators” (i.e. the NAIRU, which is used to measure when the economy is at its optimal speed) or the natural rate (which is used to measure when borrowing costs are appropriate).

Again, the idea that there is a natural rate that keeps inflation in check without hurting economic expansion, and that central banks should measure and stick to this rate, does not fit with the reality of capitalist production. Even hawkish ECB President Isabel Schnabel admitted: “The problem is that it cannot be estimated with confidence, which means it is extremely difficult to operationalize… The problem is that we don’t know exactly where it is” (!)

Apparently, these natural rates of harmonious non-inflationary growth are constantly moving! “Navigating by the stars sounds simple. However, using the stars to guide policy has recently proved challenging in practice because our best assessment of the position of the stars has shifted significantly. Schnabel continued: “Experience has revealed two realities about the relationship between inflation and unemployment that are directly related to the two questions I began by asking. First, the stars are sometimes far from where we perceive them to be. In particular, we now know that the level of unemployment can sometimes be misleading about the state of the economy or future inflation relative to our real-time estimates of the NAIRU (u*). Second, the reverse is also true: inflation may no longer be the first or best indicator of tight labor markets and rising pressures on resource utilization.” Then inflation is useless as an indicator.

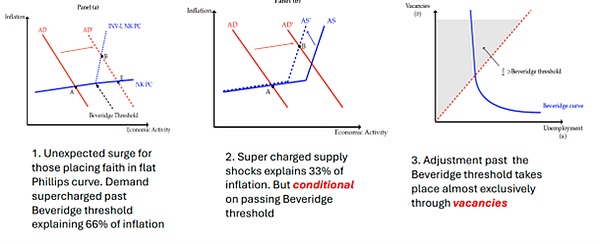

The 2024 Jackson Hole Symposium continued with papers from several well-respected mainstream economists on the effectiveness of monetary policy. One of the papers revisited the Phillips and Beveridge curves for explaining the surge in U.S. inflation after the 2020 pandemic crash. The Beveridge curve describes that as job openings increase, inflation rises and vice versa. Speakers told central bankers that“The pre-surge consensus on these two curves needs to be substantially revised. ” In other words, existing mainstream theories cannot explain the recent post-epidemic inflation surge. The speaker tried to propose a series of revised curves that are now based on job openings rather than unemployment.

Nevertheless, Powell still declared monetary policy a success: “All in all, the healing of the pandemic distortions, our efforts to control aggregate demand, and the stabilization of expectations have combined to put inflation on a path to our 2% target that looks increasingly sustainable. ” And this is without the recession that was feared and spooked financial markets only three weeks ago. A “soft landing” for the economy is still on track, with the “Goldilocks” scenario of strong economic growth, low unemployment and low inflation on the horizon.

I argued in a previous article that the market crash three weeks ago did not yet foreshadow a recession. For me, the key indicator is first and foremost corporate profits. So far, profits in major economies have not fallen into negative territory.

Source: Refinitiv, corporate profits in five major economies weighted by GDP, my calculations

But the U.S. economy and other major economies are far from out of the woods. Price inflation remains “firm,” that is, it looks like inflation will be at least around 1% above the central bank’s target.

This is also what the ECB presidents attending the seminar are worried about. Bank of England Governor Bailey said: "The question we still face is whether this persistent factor will decline to a level consistent with inflation reaching the target on a sustained basis, and what needs to be done to achieve this goal. As the overall inflation shock fades, is the persistent decline basically determined, or does it also require a negative output gap, or are we experiencing a more lasting change in the setting of prices, wages and profit rates that will require monetary policy to remain tight for a longer period of time? ” ECB Chief Economist Philip Lane similarly doubts that monetary policy can play a role in the “last mile” of the “fight against inflation”.

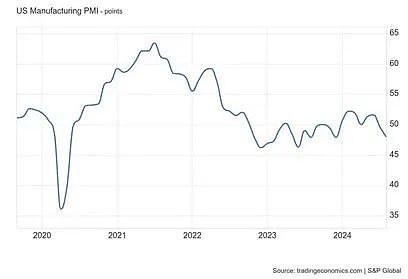

Meanwhile, among the major economies, real GDP growth (and especially real per capita output growth) has been very weak. Only the United States has seen a notable expansion, and even there, sales growth did not exceed 1% if exports and inventories are stripped out. The rest of the G7 economies are either stagnant (France, Italy, UK) or in recession (Japan, Germany, Canada). The situation is not much better in the other advanced capitalist economies (Australia, Netherlands, Sweden, New Zealand). Manufacturing is in deep contraction in almost all major economies.

Moreover, there will soon be a new US president who will either want to raise import tariffs to record levels, thereby strangling world trade and driving up import prices; or impose new taxes on corporate profits - neither of which is good news for US capital.

The Jackson Hole symposium celebrated success, but what it really revealed was that central bank monetary policy played a small role in bringing inflation down from its 2022 peak; it played a small role in achieving output or investment growth; and it had little ability to prevent rising unemployment or future production declines. All high interest rates have done is to drive many small businesses into bankruptcy or more debt; and to drive mortgage rates and housing rents to peaks. Cutting rates now will only stimulate the stock market, not the economy.

Preview

Gain a broader understanding of the crypto industry through informative reports, and engage in in-depth discussions with other like-minded authors and readers. You are welcome to join us in our growing Coinlive community:https://t.me/CoinliveSG

JinseFinance

JinseFinance