In our crypto circle, although there are various innovations in technology and application scenarios, for us old leeks, the biggest impact is the innovation in asset issuance methods.

Almost every time there is a new asset issuance (Ge Jiu Cai) method, it will bring a wave of wealth effect.

Today, let's sort out the characteristics of previous asset issuance methods:

POW

When Bitcoin, the dragon of our cryptocurrency, first appeared, the issuance method was PoW (proof of work), and all early tokens were in this mode, including Litecoin/Dogecoin and early Ethereum.

The advantage of this method is that as long as the working method has a unified standard (usually mathematical operations), anyone can join.

In the early stage of the project, the coverage that can be collected is high and the threshold is low.

Of course, after the project becomes popular, the threshold in the later stage is not high either. Not only hardware, but also electricity costs and operation and maintenance capabilities must be competed.

Although this issuance method is user-friendly, it cannot raise funds for the project party.

Private Equity

This method has actually been running in traditional industries for many years, and there is actually no essential difference between private equity in the encryption industry and traditional private equity. Investors and project parties can negotiate the conditions.

However, most projects did not issue coins when conducting private financing, so they developed into SAFT with reference to SAFE of equity investment.

SAFT stands for Simple Agreement for Future Tokens, which is a highly compliant method. Now, almost all mainstream projects use this method to raise funds.

However, this method is mainly suitable for professional financial investors, and the threshold for retail investors to participate is still a bit high.

IXO

The IXO we are talking about here includes various derivative forms of ICO/IDO/IEO.

Let's first talk about ICO (Initial Coin Offering), the first public offering of digital currency.

ICO is the initial token offering, which originated from the concept of initial public offering (IPO) in the stock market. It is the first issuance of tokens by blockchain projects.

The early ICO was very similar to private placement, and the project party had to prepare a lot of project information to introduce the project to investors, but the recent ICO has been led astray by Solana, and the project party can just send a tweet and leave an address.

This has been introduced in our previous Solana marketing video.

With the deepening of the gameplay, ICO has evolved into IDO and IEO

IDO is the full name of Initial DEX Offering, which refers to the first issuance of tokens based on a decentralized exchange (DEX).

In plain words, the project party builds a pool on Uniswap or other DEX, which is IDO. Retail investors can buy this token on dex. Currently, the mainstream method of Tugou projects is IDO.

IEO stands for Initial Exchange Offerings, which is similar to IDO. If the project party does not start on dex but on a centralized exchange cex, it is IEO.

Currently, the threshold for IEO is higher than that for DEX, because anyone can build on dex, and centralized exchanges will still have some audits on projects. Most of the tokens issued through IEO are projects that have raised some money through private placement.

Airdrop

Many crypto projects will issue coins through Airdrop when they need active communities.

Friends who often pay attention to cryptocurrencies must be familiar with this concept, that is, to make money!

However, this method has become increasingly difficult recently. On the one hand, many project parties are cracking down on witches, and it is becoming increasingly difficult to expand profits through technical means. Moreover, the airdrop rules of some projects are becoming increasingly opaque. For example, the founder of the taiko project even refused to disclose the rules:

At present, it seems that there are more and more conflicts between project parties and users in the airdrop issuance method, and it has even evolved into a counter-party. The first thing most people do after getting the airdrop is to sell it, for fear that they will sell it too late and not get the price. Fair launch Fairlaunch It is precisely because of the growing opposition between the project owners and users in the airdrop method that the fair launch model has become popular in 23 years, and the representative asset is Inscription. In this way, the project owners and retail investors grab the chips together, and shout together after grabbing them. However, this kind of game with no threshold, although fair on the surface, can be said to be strangled by scientists in the end. A large number of chips of many projects were snatched away by scientists, and scientists became actual dog dealers, with more chips than the project owners. At the same time, this method of project cannot raise money, and it is impossible to rely on scientists with a large number of chips to build.

Node Sales

The time has come to 2024. Recently, more and more projects have issued tokens through the node sales model.

Because a decentralized network itself needs a large number of nodes, in the POW era, the user's mining machine is actually a node.

However, this method cannot obtain financing for the project party. The money that users use to buy mining machines is actually given to production companies that have nothing to do with the project.

The essence of the node sales model is that the project party can obtain financing by selling nodes, and users can also participate in project construction and obtain benefits.

This method may be the mainstream method for many encryption projects in the future, and it is better than the various methods mentioned before.

Issuance method | Decentralization | Participation threshold | Fund raising |

POW | Yes | Low | None |

Private placement | No | High | Yes |

IXO | No | Low | Yes |

Airdrop | No | Low | None |

Fair Launch | Yes | Low | None |

Node Sales | Yes | Low | Yes |

What are the projects that currently use node sales?

There are three leading projects this year: XAI, Aethir, and Sophon

XAI

This round of node sales can be said to be driven by XAI.

XAI is a project launched on Binance in January this year. This project is the son of Arbitrum and is a Layer3 for gaming.

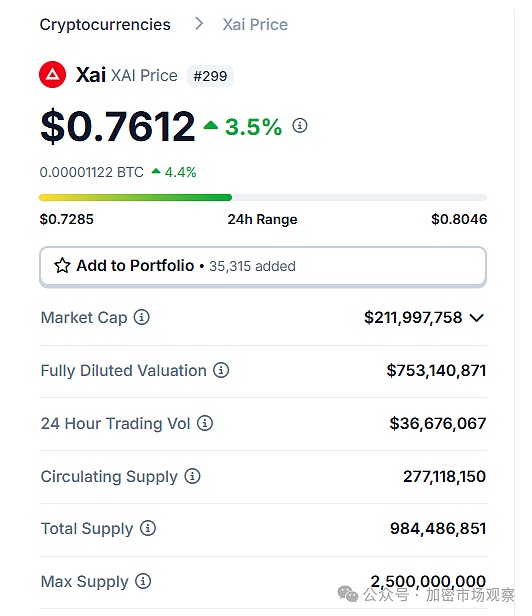

The XAI project sold 35,155 nodes for 13,080 ETH, raising 400 million USD based on the Ethereum price at the time.

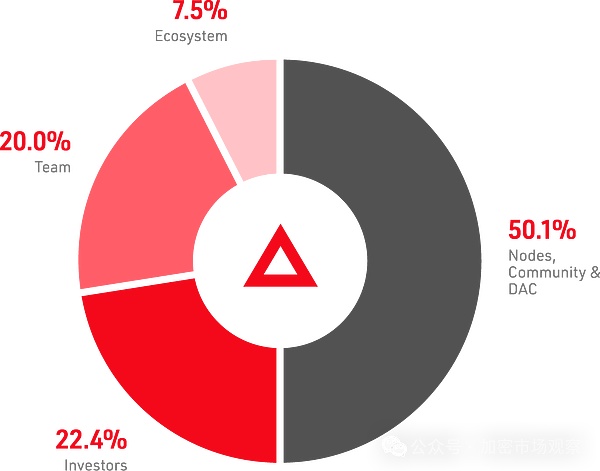

In the token economics of this project, 85% of the tokens are released for node rewards, about 1 billion. Based on the recent market value of 0.76 USD, the average floating profit of node investors is about 20 times.

Investors and teams have a 6-month lock-up period. After the node investors have mined for a few months, should they have already recovered their capital before other investors have unlocked it?

Actually, it is not. After the node mines the token, it does not get the token immediately, but esXai. It takes 180 days to convert esXai into Xai. There are two options. If it is converted in 15 days, you can only get 25% of Xai. If it is converted in 90 days, you can get 62.5% of Xai.

Aethir

You should be familiar with the Aethir project. I have introduced it before when I introduced AI depin. It is also a leading project in AI computing power.

Aethir started selling nodes to the outside world in March this year. It has sold 74,040 nodes for 41,627 ETH, which is 130 million US dollars at the price at that time.

The release rules of Aethir are not clear, but it is stated that there is a 4-year release period. The node reward is only 15% of the total, and it is expected to be around 5%~7% in the first year.

The fundamental reason is that Aethir has reserved a large part of the rewards for the computing power providers for mining.

Sophon

Sophon is a modular blockchain project. In March this year, it received $10 million in financing from OKX.

Sophon has sold 121,261 nodes, with a sales amount of 31,087 ETH, worth 96 million US dollars.

See, since the fundraising method of node sales has been introduced, private placement is no longer popular?

The final return tests the project's pattern

However, node sales are still a new issuance model. As the first project to try this round, XAI's tokens have not yet reached the 6-month unlocking period. However, according to the calculation of 62.5% of XAI tokens redeemed in 90 days, node investors should have recovered their capital long ago.

The tokens of Aethir and Sophon have not yet been officially issued, so this model is still in its early stages, and in essence it is similar to private placement, except that through the node sales model, the investment threshold can be lowered, and the project's infrastructure construction has also been completed.

The node sales phase of the aforementioned XAI/Aethir/Sophon has ended. The star project that is still selling nodes recently is CARV. Interested friends can search for relevant information by themselves.

Our crypto industry has been developing for so many years, and this year's node sales token issuance model does seem to be more suitable for crypto than other methods.

The way to directly launch on the public chain is the most primitive ICO. It cannot meet the needs of long-term business construction, and users are easily cut by the project party; sending it directly to the user's wallet for free is Airdrop, which has caused opposition between users and project parties; the threshold for private placement participation is high, which is in line with the characteristics of our crypto decentralized and widely participated.

Only through this node sales model can users get better financing conditions than private placement, and the project party can also complete the infrastructure construction. Why not?

Cheng Yuan

Cheng Yuan