"Geographic economics" is a new term covering international economic theory and policy. Gillian Tett of the Financial Times said that in the past "it was widely believed that rational economic interests rather than dirty politics were dominant. Politics seemed to be a derivative of economics, not a derivative of economics. This is no longer the case. The trade war launched by US President Donald Trump has shocked many investors because it seems so irrational by the standards of neoliberal economics. But whether it is "rational" or not, it reflects a shift: economics has given way to political games, not only in the United States but in many other places."

Lenin once said:"Politics is the most concentrated expression of economics."He believed that national policies and wars (other forms of politics) are ultimately driven by economic interests, namely the class interests of capital and the competition between "many capitals". But Lenin’s view has obviously been turned upside down by Donald Trump. Today, economics is dominated by political games; the class interests of capital have been replaced by factional political interests. So we obviously need an economic theory that can model this situation, namely geographical economics. Today, geographical economics has obviously emerged to make this hegemonic politics respectable and "realistic". Liberal democracy and "internationalism" and liberal economics, that is, free trade and free markets, are no longer important to economists who were trained to advocate an economic world of equilibrium, equality, competition and "comparative advantage" for everyone. All this is gone: today economics is about the power struggle between countries to advance their own national interests.

A recent paper argues that economists must now reckon with power politics over economic advantage; especially when hegemons like the United States achieve economic advantage not by increasing domestic productivity or investment but by using threats and force against other countries:However, hegemons often seek to influence foreign entities that they cannot directly control. They do this either by threatening the target entity with negative consequences if it does not take the desired action, thereby reducing the external option of participation constraints; or by promising the target entity positive benefits if it takes the desired action.

According to these World Bank authors, this “power economics” actually benefits both the hegemon and the objects of its threats:“Hegemony can be constructed in a way that is friendly to macroeconomists.”

Really? Tell that to China, which is facing sanctions, bans, high export tariffs, and a global blockade strangling its economy—all initiated by the current hegemon, the United States, which fears losing its hegemony and is determined to politically weaken and debilitate any opposition by any means (including war). Tell that to the world’s poorer countries, which face high tariffs on exports to the United States.

Of course, international cooperation between equals to expand trade and markets was always an illusion. There was never trade between equals; there was never a “fair” competition between capitals of roughly equal size, either within economies or on the international stage. The strong devour the weak, especially in times of economic crisis. And the imperialist core of the Global North has extracted trillions of dollars of value and resources from peripheral economies over the past two centuries.

However, some elites did shift their views on economic policy, especially after the 2008 global financial crisis and the ensuing long period of low economic growth, investment, and productivity. In the early post-World War II period, international trade and financial institutions were largely established under US control. The profitability of capital in the major economies was high, which allowed for the expansion of international trade and a revival of European and Japanese industrial power. This period was also the period of dominance of Keynesian economics, whereby the state took action to "manage" economic cycles and supported industrial development through incentives and even certain industrial strategies.

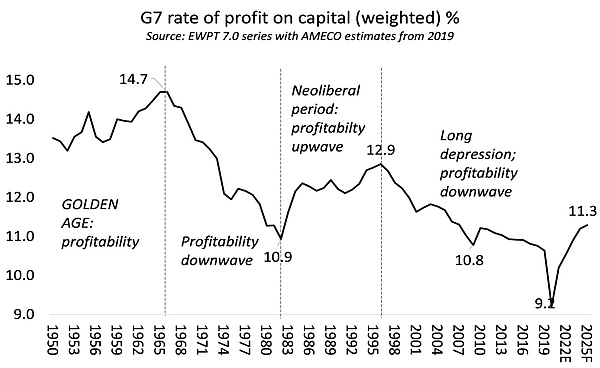

This "golden age" ended in the 1970s, when the profitability of capital fell sharply (according to Marx's laws) and the major economies suffered their first simultaneous recession in 1974-75, followed by a deep recession in manufacturing in 1980-82. Keynesian economics proved a failure, and economics returned to neoclassical free-market ideas of free movement of trade and capital, deregulation of state intervention and industrial and financial ownership, and repression of labor organization. Profitability in the major economies has (slightly) recovered, and globalization has become the creed; in reality, imperialism has expanded its exploitation of the periphery under the guise of international trade and capital flows. But Marx's law of profitability has once again exerted its gravitational pull, and profitability in the production sectors of the major economies has declined since the millennium. Only the credit-driven boom in finance, real estate and other non-productive sectors has temporarily masked the underlying profitability crisis (the blue line in the figure below shows profitability in the US production sector, and the red line shows overall profitability). But in the end, all this led to a global financial collapse, a euro debt crisis and a long depression, exacerbated by the 2020 recession brought on by the pandemic. European capital was shattered. And American hegemony now faces a new economic rival: China. China’s rapid growth in manufacturing, trade and, more recently, technology has not been affected by the economic crisis in the West. Thus, as Gillian Tett has argued, in the 2020s, “the pendulum of thought is now swinging again, towards a more nationalistic protectionism (with a touch of military Keynesianism), in keeping with historical regularity. In the US, Trumpism, an extreme and unstable form of nationalism, now seems to be being seriously studied by the new school of “geoeconomics”. Biden initiated Keynesian government intervention/support to protect and revitalize America’s ailing productive sectors, with an “industrial strategy” that included government incentives and funding for US tech giants, while imposing tariffs and sanctions on competitors (such as China). Now Trump is doubling down on this “strategy”. Protectionism internationally has been combined with government intervention at home, with weakened government services, halted climate change mitigation spending, deregulated finance and the environment, and strengthened military and homeland security forces (especially increased deportations and intimidation). style="">This crude power politics of hegemony is now being given a logic by right-wing economists, and even benefits all Americans. In a new book called American Industrial Policy, two economists who are popular with the "American Dream" (Maga) group, Marc Fasteau and Ian Fletcher, write. They are members of the so-called "Council for a Prosperous America", which is funded by a group of small companies that mainly engage in domestic production and trade. "We are an unparalleled alliance of manufacturers, workers, farmers and ranchers, working together to rebuild America for ourselves, our children and our grandchildren. We value high-quality jobs, national security and domestic self-sufficiency over cheap consumption. ” This is an institution based on class solidarity between capital and labor, aimed at “making America great again.”

Fastow and Fletcher argue that the United States has lost its hegemony in global manufacturing and technology due to neoclassical free market liberal economics:“The idea of laissez-faire has failed, and a strong industrial policy is the best way for the United States to remain prosperous and secure. Trump and Biden have enacted some policies, but the United States now needs some systematic and comprehensive policies, including tariffs, competitive exchange rates, and federal government support for the commercialization of new technologies (not just the invention). F&F's "industrial policy" had three "pillars": rebuilding key domestic industries; protecting those industries from foreign competition through import tariffs and sanctions on foreign economies whose governments erected barriers to U.S. exports; and "managing" the dollar exchange rate until the U.S. trade deficit disappeared, i.e., the dollar depreciated. F&F rejected Ricardo's theory of comparative advantage trade, which remains the basis of mainstream economics today, arguing that, ceteris paribus, "free" international trade would benefit all countries. They believed that "free trade" would actually reduce output and income in countries like the United States because cheap imports from low-wage countries would destroy domestic producers and reduce their ability to capture global export market share. In contrast, they argued that protectionist policies such as import tariffs could raise productivity and income in the domestic economy. style="">“America’s free trade policy, formed in an era of global economic dominance that has long since vanished, has failed in both theory and practice. Innovative economic models show that well-designed tariffs (to take just one example of industrial policy) can bring us better jobs, higher incomes, and GDP growth.” Yes, according to the author, tariffs will bring higher incomes for everyone.

F&F represents the interests of home-based American capital that can no longer compete in many global markets. As Engels argued in the 19th century, so long as the hegemonic economic power dominates international markets for its products, it will support free trade, but once it loses its dominance, it will adopt protectionist policies. (See my book Engels, pp. 125-127). This is exactly what happened to British policy in the late 19th century. Now it’s America’s turn.

On the other hand, protectionists are wrong to claim that import tariffs and other measures can restore a country’s previous market share. But F&F’s industrial strategy does not rely solely on tariffs. They define industrial policy as

“deliberate government support for industry, which falls into two categories. The first category is broad policies that support all industries, such as exchange rate management and R&D tax credits. The second category is policies that target specific industries or technologies, such as tariffs, subsidies, government procurement, export controls, and government-sponsored or funded technological research.” ”

F&F’s industrial strategy is not working. In an economy, productivity growth and cost reduction depend on increasing investment in areas of productivity improvement. But in a capitalist economy, this depends on the willingness of profit-oriented businesses to increase investment. If profitability is low or falling, they will not invest. This has been particularly true of the experience of the past two decades. F&F wants to return to wartime policies and Cold War strategies to build domestic industry, science, and military power. But this will only work if there is a massive shift to direct public investment through state-owned enterprises that develop national industrial plans. F&F does not want this, and neither does Trump.

This sums up the US motivation to abandon the neoclassical laissez-faire and free trade economics that has until now dominated the academic ivory towers of economic departments and international economic institutions. The economic dominance of the United States (and Europe) has been eroded to the point where the risk of Chinese global domination within a generation is extremely high. Therefore, the United States must act decisively.

Abandon the concepts of free competition, markets and trade - they never actually existed. Introduce the realism of winning the struggle for political and economic power at all costs. This is the essence of the new geographical economics, which may soon appear in the economics departments of universities in the Global North, despite the opposition of the currently dominant neoclassical and neoliberal professors.

Preview

Gain a broader understanding of the crypto industry through informative reports, and engage in in-depth discussions with other like-minded authors and readers. You are welcome to join us in our growing Coinlive community:https://t.me/CoinliveSG

Brian

Brian