In September 2024, VISA released a report on stablecoins, which deeply analyzed the penetration of stablecoins in emerging markets. This article will take you through the main findings of the report.

In recent years, stablecoins have gradually been integrated into the global economy, especially in emerging markets. VISA's latest report shows that stablecoins, as the latest currency carrier or form of expression, have spread to all aspects of the financial life of ordinary users after being initially used as collateral or medium of exchange for crypto assets. More and more retail and institutional users have also begun to accept this emerging technology, promoting further innovation in the global payment system.

In the report, VISA combines the survey results of cryptocurrency users from five key emerging market economies (Brazil, India, Indonesia, Nigeria and Turkey) with new on-chain estimation data, plus qualitative analysis, to form a comprehensive picture of global stablecoin usage. The report focuses on the use of stablecoins in non-crypto fields, such as remittances, cross-border payments, salary payments, trade settlements and B2B transfers.

I. Overview of the Stablecoin Market

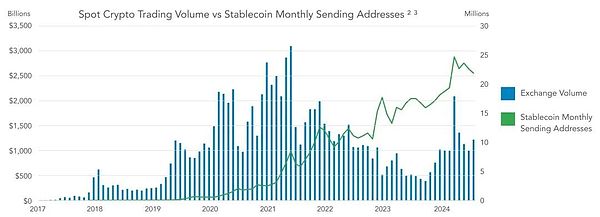

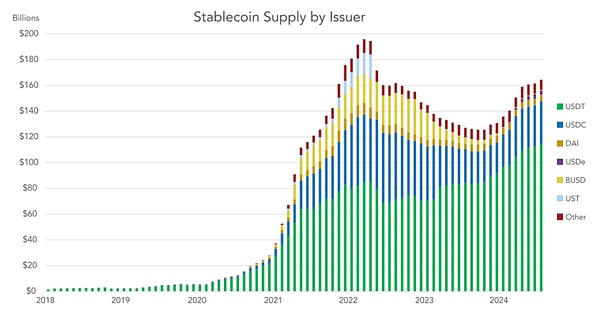

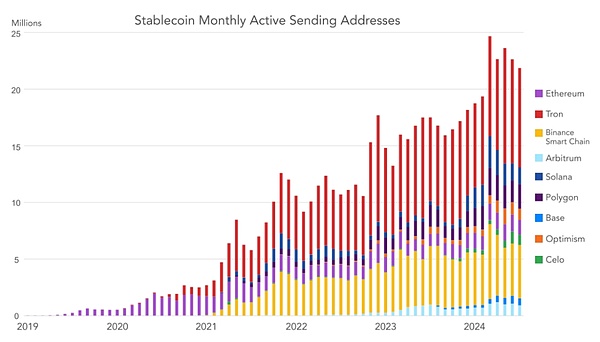

Stablecoins are the "killer application" in the current crypto field. Today, the total value of stablecoins in circulation on the market exceeds $160 billion, while in 2020, this value was only a few billion dollars. More than 20 million addresses conduct stablecoin transactions on public blockchains every month. In the first half of 2024 alone, the settlement amount of stablecoins exceeded $2.6 trillion. Stablecoins have significant advantages over existing payment systems: on-chain programmability, strong audit capabilities, transaction settlement, self-custody of funds, and interoperability.

Although stablecoins were initially used by traders and cryptocurrency exchanges as a medium for collateral and asset transactions, they have now crossed this category and are widely used in the global economy. In emerging markets, the application of stablecoins in payments, currency substitution, and obtaining high-quality returns is accelerating.

Based on the difference between stablecoin activity and crypto market cycles, it is clear that the use of stablecoins is no longer just for crypto users and transaction use cases.

Non-transactional uses of stablecoins are increasing, especially in emerging markets. They are used for currency substitution (to escape volatility or depreciation of local currencies), as a substitute for US dollar bank accounts, for inter-business payments and consumer payments, for various forms of income products, and for trade settlement. Stablecoins are particularly attractive in countries with high inflation or in countries where the fiat financial system is lacking when US dollar banking services are absent or difficult to obtain.

2. On-chain stablecoin data

2.1 The stablecoin market is growing year by year

Since 2017, the total supply of stablecoins has grown rapidly. At that time, the total circulation of stablecoins was less than $1 billion, and this figure peaked at about $192 billion in March 2022 before the collapse of Terra's UST and the credit crisis. The credit crisis suppressed cryptocurrency native interest rates, depressed cryptocurrency trading volumes, and damaged the balance sheets of crypto-native companies. After the credit crisis basically subsided, from December 2023, as the calls for the approval of the Bitcoin ETF in the United States grew louder, major crypto assets began to rebound and the supply of stablecoins began to recover.

In recent months, various regulators have passed clear stablecoin legislation in the hope of attracting issuers. Some of the jurisdictions that have been most active in developing stablecoin regulatory frameworks include the European Union, Singapore, Dubai, Hong Kong and Bermuda.

2.2 Corrected, adjusted data

For this study, VISA performed a lot of denoising and deduplication work, and ultimately came up with a more conservative estimate of settlement volume. Adjusted settlement volume is still a difficult number to estimate, and VISA does not regard its estimates as authoritative, but believes that this data is still close to the truth.

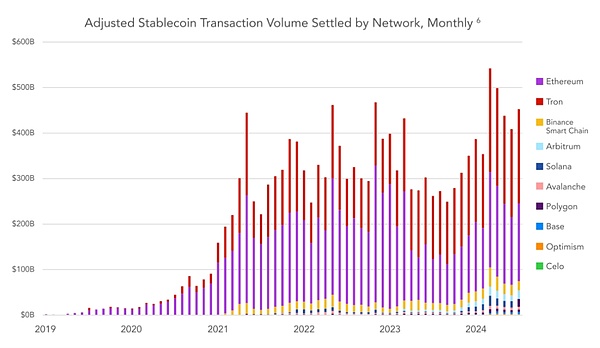

According to VISA's adjustments, it is conservatively estimated that the total settlement volume of stablecoins in 2023 will be US$3.7 trillion, while in the first half of 2024 it will be US$2.62 trillion, and the annual settlement volume in 2024 is expected to be US$5.28 trillion. It is worth noting that despite the sell-off of crypto assets and the decline in trading volume in 2022 and 2023, the settlement volume of stablecoins has continued to grow steadily over the market cycle. This once again shows that stablecoins have attracted a group of new users who are not only interested in using them for exchange settlement.

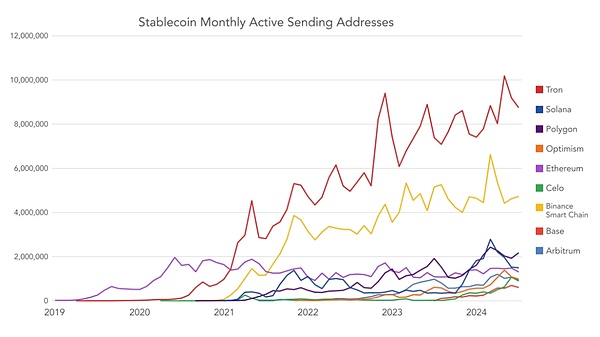

After denoising, as of June 2024, the most popular blockchains by settlement value are: Ethereum, Tron, Arbitrum, Base, BSC and Solana.

The most popular stablecoin transfer blockchains are: Tron, BSC, Polygon, Solana and Ethereum.

2.3 Dollarization of Stablecoins

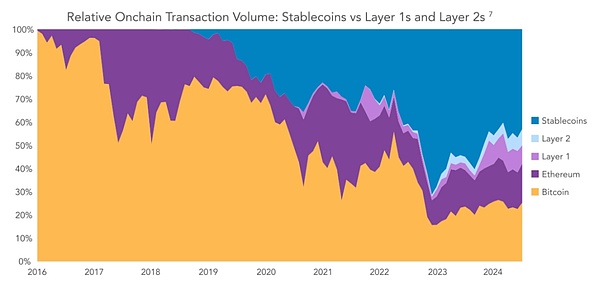

When stablecoin settlement volumes are compared to native crypto assets, the phenomenon of “blockchain dollarization” emerges. While Bitcoin and Ethereum have historically been the dominant medium of exchange on public blockchains, stablecoins—and almost exclusively stablecoins pegged to the U.S. dollar—have gradually captured an increasing market share.

Currently, stablecoins account for about 50% of the total value settled on public blockchains, and have reached 70% at their peak. The second most popular currency used by stablecoins is the euro, with a supply of $617 million as of June 2024, accounting for 0.38% of the entire stablecoin market. While there are stablecoins using the lira, Singapore dollar, yen, and some other fiat currencies, no stablecoin other than the dollar and the euro has a peg to more than $100 million.

III. Emerging Market Survey Report

VISA surveyed approximately 500 people from Nigeria, Indonesia, Turkey, Brazil and India, with a total sample of 2,541 adults. VISA's goal is to better understand how individual users interact with stablecoins.

The survey data shows that the usage of stablecoins is growing, the frequency of transactions is increasing, the penetration rate of investment portfolios has increased significantly, and in addition to the use scenarios of cryptocurrency transactions, its usage methods are becoming more diversified.

3.1 Types of Stablecoin Activities:

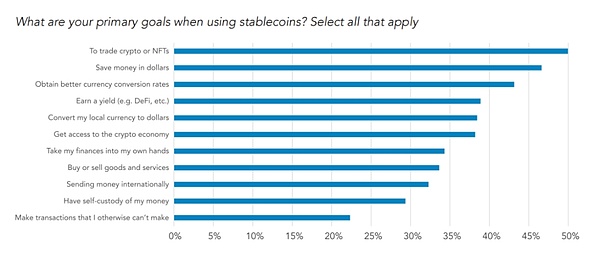

In VISA's sample, the main purpose of using stablecoins is still trading cryptocurrencies or NFTs, but other non-cryptocurrency uses are not far behind. Overall, 47% of respondents said one of their main purposes was to store funds in US dollars, 43% mentioned getting a better currency exchange rate, and 39% said they wanted to earn a profit.

The results are clear: in the countries surveyed by VISA, non-crypto uses account for a large part of the way stablecoins are used.

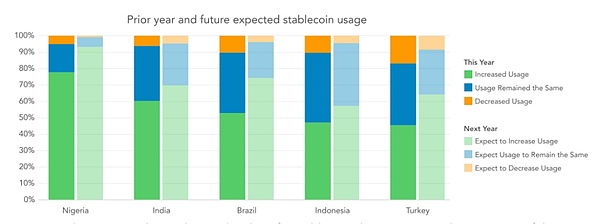

By far, the most popular use is currency exchange, followed by shopping and cross-border transactions. Notably, the majority of respondents in all countries in the sample said they had used stablecoins for non-cryptocurrency transaction scenarios. In all countries surveyed, the use of stablecoins has been growing over time. 57% of users reported an increase in their use of stablecoins in the past year, and 72% believed that they would increase their use of stablecoins in the future.

3.2 Stablecoin Penetration

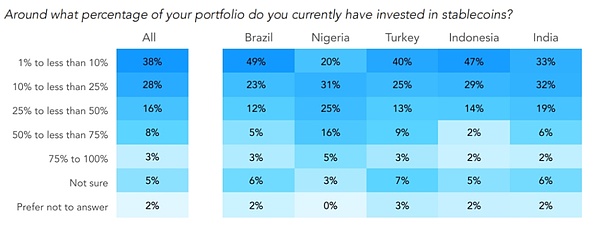

VISA is also interested in the penetration of stablecoins in users' portfolios. At the country level, Nigerians have a significantly higher percentage than other countries, followed by Turkey and India. In the sample of Indian users, the wealthiest respondents reported a larger proportion of stablecoins in their financial portfolios.

Findings by country:

VISA's survey found that Nigerians had the highest preference for stablecoins among the countries surveyed - far higher than other countries. Nigerians trade most frequently, stablecoins make up the largest proportion of respondents' portfolios, they report the most non-crypto trading uses, and they have the highest self-awareness of stablecoins.

Interestingly, there are differences in the main purposes of stablecoin use by users across countries. Trading cryptocurrencies is the most common purpose across the sample, but it varies at the country level. In Turkey, the most common purpose was to earn a yield, followed by trading cryptocurrencies; in Indonesia, it was to get a better currency exchange rate, followed by trading cryptocurrencies and saving in USD; in Nigeria, the most common purpose was to save in USD, followed by trading cryptocurrencies and getting a better currency exchange rate.

The most active countries in the sample using stablecoins are Nigeria, India, Indonesia, Turkey and Brazil. In terms of the proportion of stablecoins in the portfolio, Nigeria is still far ahead, followed by India, Turkey, Brazil and Indonesia.

Survey results by age:

Overall, the results by age are in line with expectations: younger people are more likely to use stablecoins. Young people are more likely to try a variety of different stablecoins and have a larger proportion of stablecoins in their overall financial portfolio.

While there were no significant age differences in most usage categories, younger people were more likely than older respondents to use stablecoins to save USD, convert local currency to USD, or gain access to the crypto economy. Younger age groups used stablecoins more frequently across all non-crypto use cases: paying for goods or services with stablecoins, transferring remittances, and receiving wages with stablecoins.

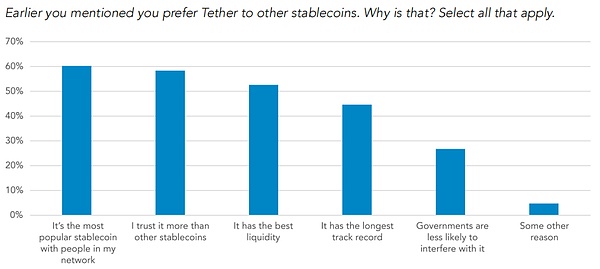

3.3 Tether Preference for USDT

Tether is widely considered to be the most popular stablecoin among users in emerging markets. Users reportedly most often cited reasons for preferring Tether as its network effect, followed by greater trust in Tether and Tether’s best liquidity.

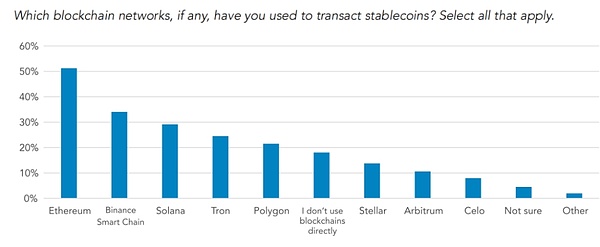

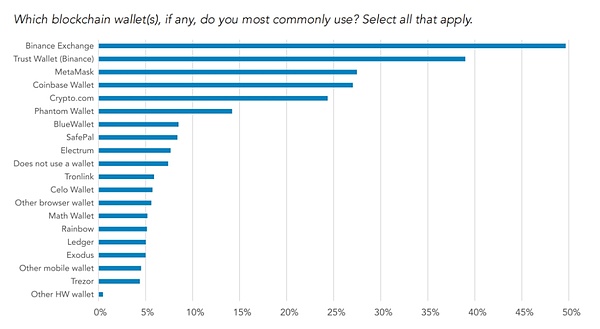

3.4 Blockchain and Wallet Usage

According to the report, Ethereum is the most popular blockchain network in all regions, followed by BSC, Solana and Tron.

The most popular non-custodial wallets are Trust Wallet, MetaMask and Coinbase Wallet. Among all respondents, more than half said they use Binance exchange as a wallet, which is more popular than any other non-custodial wallet. Notably, 39% of Nigerian respondents admitted to using Phantom wallet (mainly Solana client).

Fourth, Conclusion

In this study, VISA first demonstrated that the use of stablecoins is growing from an on-chain perspective, whether measured by monthly active addresses, total supply, or settlement amount. In particular, VISA's new transaction amount estimates show that stablecoins have become an important settlement tool that can rival existing transfer networks while avoiding the overestimation problem that is common in on-chain data in the past.

VISA's survey results overturn the common belief that stablecoins are only used for speculative crypto asset transactions.47% of the crypto users surveyed said that they use stablecoins for the purpose of US dollar savings, 43% of respondents mentioned efficient currency exchange, and 39% mentioned earning income. While access to cryptocurrency exchanges remains the most prominent use case for respondents, a range of ordinary (non-crypto) economic activities are also represented.

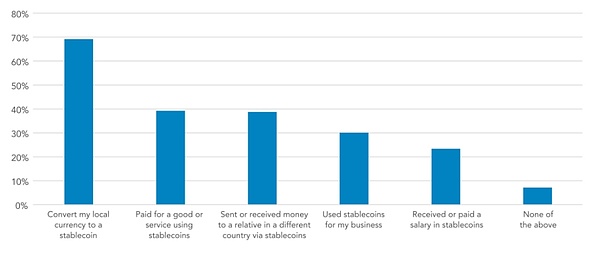

When asked about non-crypto stablecoin activities, the most common use case was currency substitution (69%), followed by payment for goods and services (39%) and cross-border payments (39%). It is clear that stablecoins have evolved from simple transaction collateral to a commonly used digital dollar instrument in the countries surveyed.

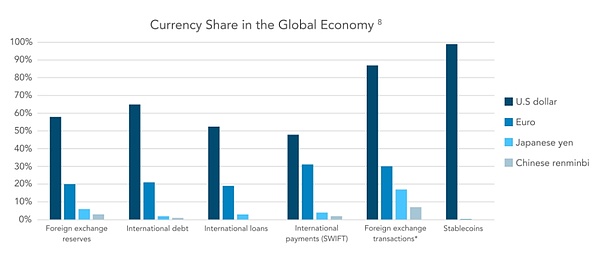

What’s more, almost all stablecoins (about 99%) are pegged to the U.S. dollar. Discussions about stablecoin regulation in the United States cannot ignore the fact that a large number of individuals and businesses in emerging markets rely on these networks for savings, cross-border payments, remittances, and corporate cash management. In almost all of the countries surveyed, stablecoins are increasingly becoming a substitute for scarce U.S. dollar banking services. When discussing the merits of stablecoins, the potential benefits of efficient access to alternative hard currency for billions of users in emerging markets must have a place.

JinseFinance

JinseFinance