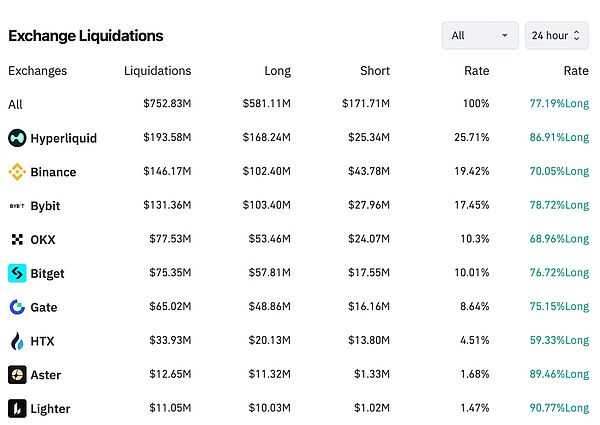

For a long time, Binance has been hailed as the "world's largest exchange" in the crypto world. However, recently, I've begun to have increasingly strong doubts about this label, which has long been ingrained in the minds of retail investors. Of course, with its vast matrix of public chains, ecosystems, wallets, and VC footprint, Binance remains the most influential super platform in the crypto industry—this is undisputed. What truly deserves re-examination is another, more fundamental question: In the most essential and important battlefield for exchanges—trading itself, especially in the large-scale, high-fee, price-determining futures market—does Binance firmly hold its position as the industry leader? Does it still possess an absolute advantage that is difficult for other competitors to shake? And in terms of innovation leadership in other niche areas, are there any players who surpass Binance? The reason I raise this question isn't because of a short-term data change, but because of several recent seemingly minor events—which may not seem significant individually, but collectively are gradually eroding my existing perception of Binance's market position. Contract trading volume is facing challenges. Firstly, in the recent volatile market, Hyperliquid's liquidation data has surpassed Binance's. As shown in the chart below, Hyperliquid's liquidation amount in the last 24 hours was approximately $193 million, while Binance's was $146 million.

Odaily Note: Data is from Coinglass, as of 14:00 on February 2nd

One point of contention here is that Binance's liquidation data push frequency is limited to once per second, so data platforms like Coinglass may experience some delays when scraping it.

However, based on our observations, it is indeed true that more and more large investors are choosing to open positions on Hyperliquid.

Typical examples include "Brother Machi," "1011 Insider Whale," James Wynn, AguilaTrades, "CZ Opponent's Plate," "14-Game Winning Streak Whale," Gambler@qwatio, and Low-Stack Degen—these are the eight legendary figures... You can criticize them as gambling addicts, but where there are gambling addicts, there is turnover, and turnover is the lifeblood of exchanges. This situation arises because, compared to the unavoidable "black box" suspicion of CEXs, all orders, transactions, clearing, and settlements on Hyperliquid are executed on-chain, naturally possessing advantages in transparency and fairness. In the first half of last year, a prominent figure who had founded several well-known projects over the years (whose name I won't mention) suffered a targeted liquidation on a certain CEX (not Binance, to clarify), losing hundreds of millions of dollars. The platform, however, never disclosed details of its internal order matching and liquidation. The second event was last week when Jeff, the founder of Hyperliquid, posted a comparison of the BTC contract order books on Hyperliquid (right side of the image below) and Binance (left side of the image below) on X. The chart showed that Hyperliquid had a narrower bid-ask spread and a deeper order book for BTC. Jeff then boldly declared, "Hyperliquid has become the world's most liquid cryptocurrency price discovery platform." This is not an isolated case. A real-time look at the order books of other major tokens like ETH and SOL on Hyperliquid and Binance reveals that the former's liquidity performance is no less than the latter's. The expansion of new token listings has been slow. Over the past year, compared to many second-tier exchanges, Binance has significantly tightened its pace in terms of "official listings," delegating more of its high-frequency trading testing to Binance Alpha. However, the performance of many listed tokens has been unsatisfactory. Furthermore, due to the explosive popularity of Chinese memes, Alpha's focus has shifted further towards the BSC ecosystem. Following the 10.11 incident, controversies surrounding Binance have continued to escalate, raising questions about Binance's listing strategy. A few days ago, Solana co-founder natoly Yakovenko (toly) criticized Binance on X and was unfollowed by CZ. Prior to this, there was already a prevailing sentiment that Solana ecosystem projects were shifting towards Bybit. Looking ahead, Binance may not have the same dominance in future token listings and pricing as it once did. More importantly, with the continued slump in native crypto assets, the industry has turned to asset classes derived from traditional finance, such as stock tokens and precious metals, as a new breakthrough. However, Binance's progress on this path is somewhat slower compared to Hyperliquid and other very active CEXs (Bitget, Gate, Bybit, etc.). Last Monday, Binance officially launched its first cryptocurrency-equity contract, TSLA (Tesla), and today it followed suit with INTC (Intel) and HOOD (Robinhood). Meanwhile, Binance's pursuers, such as Gate and Bitget, are more aggressively expanding into traditional asset classes, from stock tokens to precious metals, from indices to commodities; competitors have already begun their battle for potential users. On the centralized side, Hyperliquid, leveraging its open architecture of HIP-3, has already launched dozens of traditional assets, including pre-IPO stocks like OpenAI and Anthropic, through a more flexible custom market approach, accumulating considerable trading volume around these assets—traditional assets recently accounted for half of Hyperliquid's trading volume rankings. What has changed? Looking at the current arguments together, it's difficult to conclude that "Binance has lost its throne." Binance remains the most important liquidity hub. But what I think is truly alarming is not that Binance's market share has been surpassed in the short term by any specific second-tier exchange, but rather that Binance is continuously facing structural challenges in its core trading arena. What Binance is losing is not market share, but the power to define "what an exchange is." For a long time, Binance was considered the "world's largest exchange" not only because of its unparalleled liquidity, but also because—where price discovery occurs, where mainstream funds trade, and where new assets should be tested first—the industry's default answer was Binance. However, as more and more high-net-worth individuals prioritize "verifiability, fairness, and traceability" over fees and brand image, as price discovery is reorganized on-chain, and as the testing ground for new assets gradually shifts from the exchange's back-end to a verifiable market mechanism on the front end, Binance, in its strongest and core area, is not facing the challenges of traditional competitors, but rather rivals that could potentially shift the industry paradigm. While the article discusses specific categories, the underlying issue is the most fundamental value of exchanges: where do prices originate, and who guarantees trust? Perhaps Binance should consider how deep its competitive moat truly is.

XingChi

XingChi