特朗普家族重磅加密计划!World Liberty Financial推进“稳定币”项目,已进入产品开发阶段

据知情人士透露,美国前总统特朗普家族旗下加密项目World Liberty Financial正筹划推出一种新型稳定币,目前该项目已进入产品开发的关键阶段。

Miyuki

Miyuki

Author: NingNing

The Bitcoin on-chain Tx Volume chart in Glassnode's latest weekly report is very confusing. The 30-day SMA structure of Tx Volume from October 2023 to present is very similar to that from October 2020 to September 21, which will lead some people in the market to conclude that "we are already in a super bull market and the bull market is already halfway through."

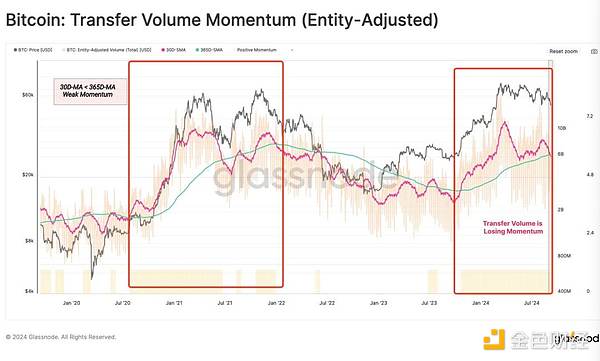

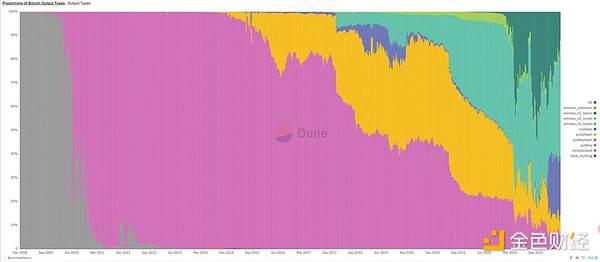

The confusing thing about this chart is that the structure of the Tx Volume used for comparison has changed dramatically. The Taproot Witness TX related to inscriptions and runes has grown rapidly since 23 years ago, accounting for 41.8% of the Tx Volume at its peak, which was not seen in the previous cycle.

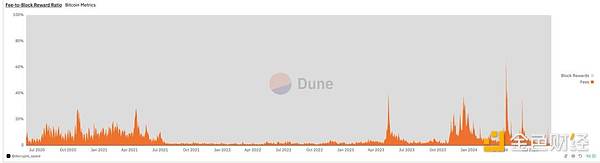

This can also be verified from the change chart of Bitcoin mining fees. Excluding the impact of the inscription/rune boom period, the base scale of mining fees from 23 years to now is completely incomparable with the bull market from March 20 to July 21, and is only slightly higher than the bear market in 22 years.

Therefore, the so-called "bull market" that we experienced from October 23 to March 24 was not a real super bull market, but a market composed of two seasonal markets (one autumn market + one spring market) and the new asset issuance boom.

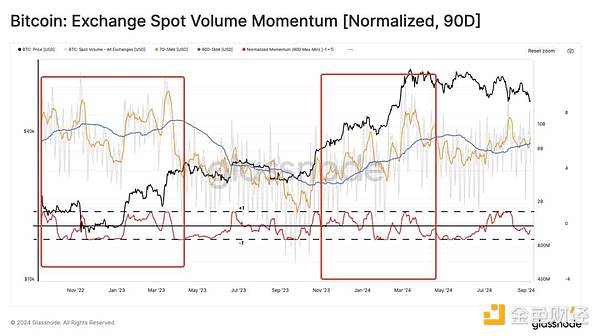

The trend of spot trading volume in exchanges from November 22 to the present also proves this point. As shown in the figure, there are only seasonal fluctuations, and there is no trend of rising.

To summarize, the myth that "halving brings a bull market, and a bull market every four years" has been falsified this year. The reason for this myth is that the Bitcoin halving cycle has always been highly coincident with the Federal Reserve's monetary cycle. This is because Bitcoin was born in the era of the subprime mortgage crisis, and the production reduction every four years happened to be at the end of the Federal Reserve's interest rate reduction cycle and the recovery period of the Merrill Lynch clock.

However, this round was delayed by one year due to the Federal Reserve's monetary cycle, resulting in a halving of half a year in 24 years, but only seasonal market conditions without a super bull market. However, there is no need to be pessimistic about this. The absence of a super bull market in 24 years means that a super bull market will come in 25-26 years.

据知情人士透露,美国前总统特朗普家族旗下加密项目World Liberty Financial正筹划推出一种新型稳定币,目前该项目已进入产品开发的关键阶段。

Miyuki马斯克警告美国债务危机,并宣布“金融紧急状态”。随着美国35.7万亿美元债务引发市场担忧,比特币表现强劲,涨幅媲美黄金。马斯克多次强调美国经济面临严峻挑战。

Alex

AlexChangpeng Zhao, founder of Binance, made his first public appearance since his prison release at the Binance Blockchain Week in Dubai, discussing his reflections on his incarceration and future plans. He expressed a renewed appreciation for personal connections, a commitment to education, and intentions to invest in emerging sectors while remaining optimistic about the future of cryptocurrency.

Joy

Joy近年来,迷因币的快速崛起及其高回报率吸引了大量市场关注,但知名NFT收藏家Pranksy近日在推特上公开批评迷因币,表示每天醒来看到迷因币的存在令他沮丧,并直指其“毫无价值”。

Weiliang

Weiliang根据《The Information》报道,Meta 正在开发自主 AI 搜索引擎,计划将其整合至 Meta AI,以提供最新资讯和实时事件摘要,降低对 Google 和 Bing 的依赖。为此,Meta 特别组建了一个工程团队,已投入八个月时间建设搜索引擎数据资源库。

AlexPudgy Party will bring Pudgy Penguins into mobile gaming with a fun, teamwork-focused experience available globally in 2025. Built on the Mythos blockchain, it blends digital gameplay with real-world items and community engagement, making it accessible and customisable for players of all ages.

Weatherly

WeatherlyCardano 宣布将整合比特币 Rollup 协议 BitcoinOS,成为比特币的二层网络(L2),以释放高达 1.3 万亿美元的比特币流动性。不同于依赖中心化托管商的封装比特币,Cardano 的 BitcoinOS Grail bridge 让用户可以无信任地将比特币转移至 Cardano 网络,参与 DeFi 等多种应用。

MiyukiStephen Mollah recently claimed to be Satoshi Nakamoto at a press conference in London but failed to provide any credible evidence to support his assertion. The event, which was marred by technical issues and confusion, left attendees frustrated and questioning the validity of Mollah’s claims, which echo similar unproven assertions made by others in the past.

Anais

AnaisPaxos has launched its Global Dollar (USDG), a new stablecoin approved by Singapore's Monetary Authority, which is backed 1:1 by the US dollar and managed by DBS Bank. This initiative aims to enhance compliance and security in the stablecoin market while expanding USDG's global reach through partnerships with various crypto platforms.

AnaisImmutable has received a Wells Notice from the SEC, raising concerns about the classification of its IMX token as a security following a 2021 listing and private sales.

Weatherly