玻利维亚Bisa Bank开通USDT交易及跨境支付服务,加速稳定币在本地的应用

玻利维亚加速采用稳定币技术,Bisa Bank成为该国首家提供USDT交易服务的银行。客户可通过其平台进行USDT的购买、出售、持有及跨境汇款,进一步推动稳定币在玻利维亚的普及和金融现代化。

Alex

Alex

On February 19, 2024, the Financial Services Agency (FSA) of Japan approved the "Report of the Working Group on Fund Settlement System, etc." at the General Meeting of the Financial Services Council (chaired by Chairman Hiroyuki Kamisaku).

The report is the final result of seven rounds of discussions in response to the consultation request of the Minister of Finance in August 2024. The core content of the report involves a new regulatory framework for cryptocurrencies (virtual currencies) and stablecoins, especially specific suggestions on user protection in the event of exchange bankruptcy, the establishment of intermediary business, and asset utilization rules for stablecoins. This policy move marks a further refinement of Japan's regulation in the field of cryptocurrencies and stablecoins, aiming to balance innovation and risk control.

This article will provide an in-depth interpretation of this new regulatory framework from four aspects: policy background, main content, policy impact and future prospects.

In November 2022, the bankruptcy of FTX, the world's second largest cryptocurrency exchange, shocked the entire cryptocurrency industry. The collapse of FTX not only resulted in billions of dollars in user asset losses, but also exposed the weak links in the regulation of cryptocurrency exchanges. As an important participant in the global cryptocurrency market, Japan's regulator, the Financial Services Agency, responded quickly and began to re-examine the shortcomings of the existing regulatory framework.

Japan included cryptocurrencies in the scope of regulation through the Funds Settlement Law as early as 2017, and established a relatively complete exchange license system. However, the FTX incident shows that existing regulatory measures alone are still not enough to deal with extreme situations such as exchange bankruptcy. Therefore, the Financial Services Agency launched a new round of regulatory reforms in 2024, aiming to strengthen user protection and improve market transparency.

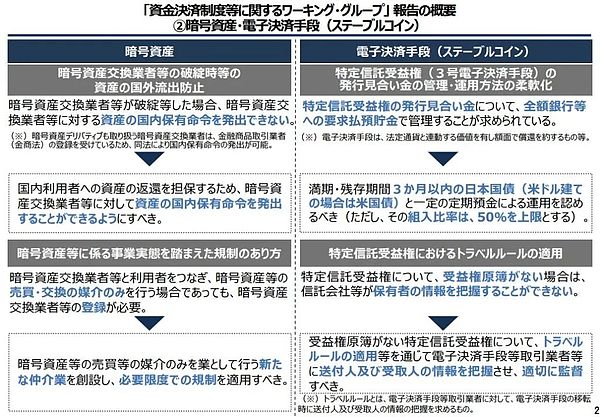

The report proposes that new clauses will be introduced in the Funds Settlement Law with reference to the relevant provisions of the Financial Instruments and Exchange Act to strengthen user protection when cryptocurrency exchanges go bankrupt. Specific measures may include:

Asset isolation requirements: require exchanges to strictly separate user assets from their own assets to prevent user assets from being used to repay debts in the event of bankruptcy.

Bankruptcy liquidation priority: clarify the user's priority right to repayment in bankruptcy liquidation to ensure that user assets can be returned first.

Information disclosure obligations: require exchanges to regularly disclose their financial status and asset custody status to enhance transparency.

These measures are intended to prevent the recurrence of similar FTX incidents and provide users with a safer trading environment.

The report also proposed a new business model - cryptocurrency trading intermediary business. This type of intermediary will adopt the "affiliation system", that is, it must be affiliated with a specific exchange to conduct business. Unlike traditional exchanges, intermediaries do not directly custody user assets, so their regulatory requirements are relatively loose:

No property custody obligations: intermediaries do not directly hold user assets, reducing the risk of misappropriation or loss of funds.

Simplified access conditions: intermediaries do not need to meet strict property-based requirements, nor do they bear direct obligations for anti-money laundering (AML) and combating terrorist financing (CFT).

Business scope restrictions: intermediaries are only responsible for buying and selling, and do not involve complex businesses such as asset custody and liquidation.

The establishment of this new business model aims to lower the market entry threshold and promote market competition, while ensuring the business compliance of intermediaries through the "affiliation system".

The report proposes important adjustments to the stablecoin asset utilization rules. According to current regulations, stablecoin issuers must deposit equivalent assets in banks in the form of "required deposits". The new framework allows issuers to use part of their assets for low-risk financial products such as short-term government bonds and time deposits:

New asset categories: Stablecoin issuers are allowed to invest no more than 50% of their assets in short-term government bonds and time deposits.

Risk control: A 50% cap is set on the proportion of new asset categories to ensure that the asset reserves of stablecoins have sufficient liquidity.

This adjustment aims to improve the asset utilization efficiency of stablecoin issuers while controlling risks through proportion restrictions.

The biggest beneficiaries of the new regulatory framework are ordinary users. By strengthening user protection measures when an exchange goes bankrupt, the security of users' assets will be significantly improved. In addition, the establishment of intermediary businesses may reduce transaction costs and provide users with more options.

For exchanges, the new regulations will increase their compliance costs, especially the requirements for asset isolation and information disclosure. However, these measures will also help enhance the credibility of exchanges and attract more users. For intermediaries, the establishment of new formats provides small and medium-sized enterprises with opportunities to enter the market, but the "affiliation system" also means that their business independence is restricted.

The adjustment of the stablecoin asset utilization rules will increase the issuer's asset yield, thereby enhancing its profitability. However, the 50% ratio cap also limits the issuer's risk-bearing capacity and ensures that the stability of stablecoins is not affected.

The new regulatory framework further consolidates Japan's position as a global leader in cryptocurrency regulation. By balancing innovation and risk control, Japan is expected to attract more international capital and projects to its market.

With the implementation of the measures proposed by the Financial Services Agency to strengthen user protection, Web3 security compliance companies such as Beosin play a vital role in this process. Beosin focuses on security compliance in the crypto asset industry and provides comprehensive smart contract security audits and compliance services. Through these technical supports, crypto asset service providers can operate within the compliance framework and effectively prevent potential security risks.

This new regulatory framework of the Japanese Financial Services Agency marks a new stage in the regulation of cryptocurrencies and stablecoins. However, with the rapid development of technology and the constant changes in the market, regulators still need to remain flexible and respond to emerging risks in a timely manner.

Possible future development directions include:

Cross-border regulatory cooperation: The global nature of the cryptocurrency market requires regulators in various countries to strengthen cooperation and formulate unified regulatory standards.

Technology-driven regulation: Use tools such as blockchain technology and artificial intelligence to improve regulatory efficiency and transparency.

User education: Strengthen the popularization of cryptocurrency knowledge among ordinary users and improve their risk awareness and self-protection capabilities.

The new regulatory framework approved by the Financial Services Agency of Japan is an important milestone in the field of cryptocurrency and stablecoin regulation. By strengthening user protection, establishing intermediary business and adjusting the rules for the use of stablecoin assets, Japan has not only promoted market innovation, but also provided an important reference for global cryptocurrency regulation. In the future, with the gradual implementation of this framework, Japan is expected to occupy a more important position in the global cryptocurrency market.

玻利维亚加速采用稳定币技术,Bisa Bank成为该国首家提供USDT交易服务的银行。客户可通过其平台进行USDT的购买、出售、持有及跨境汇款,进一步推动稳定币在玻利维亚的普及和金融现代化。

Alex在以太坊和其基金会遭遇广泛批评之际,以太坊共同创始人Vitalik Buterin(V神)上周在社交平台X上引发大量关注。他发布了关于以太坊路线图的文章,并明确回应了对以太坊基金会频繁出售ETH的质疑。

Alex美国总统大选临近,特斯拉CEO兼X平台负责人马斯克(Elon Musk)近期高调力挺共和党候选人川普。今日,马斯克分享了一张柴犬的狗狗币(DOGE)梗图,推动DOGE币在一小时内上涨约3%。

Miyuki

MiyukiA DWF Labs partner was dismissed after being accused of drugging a woman he invited to discuss a job opportunity in Hong Kong. The incident, reportedly caught on CCTV, is now under police investigation.

Joy

Joy最新消息指出,輝達的GB200 AI伺服器即将出货,微軟、Google、Meta、亚马逊AWS等科技巨头正争相购入高性能的GB200 NVL72机柜。鴻海作为主要代工厂,订单已爆满,股价随之攀升至三个月来的新高。

Weiliang

WeiliangAlameda Research is suing KuCoin to recover over $50 million in frozen assets linked to the FTX collapse, claiming KuCoin has unjustly refused to release the funds. KuCoin has stated the assets were frozen due to suspicious activities and is following legal orders regarding the situation.

Weatherly

WeatherlyConsensys has announced a 20% workforce reduction, cutting approximately 162 employees, due to economic challenges and ongoing regulatory disputes, particularly with the SEC.

Anais

Anais10月29日(周二),美国最新就业数据显示9月份职位空缺降至2021年初以来的最低水平,裁员增加,暗示劳动力市场正在趋缓,致使股市走势不明。同时,10月消费者信心指数攀升至今年新高,市场对经济前景的担忧有所缓解。在美国大选前夕,比特币自6月以来首次突破73,000美元大关。

Alex作为微软的重要股东,贝莱德将通过投票参与微软是否应探索比特币收购的决策。

Miyuki据知情人士透露,美国前总统特朗普家族旗下加密项目World Liberty Financial正筹划推出一种新型稳定币,目前该项目已进入产品开发的关键阶段。

Miyuki