What is the main theme of this bull market?

Crypto market, what is the main line of this round of bull market? Golden Finance, the main line of this round is already relatively clear.

JinseFinance

JinseFinance

Author: Sima Cong

People are risk-averse and at the same time, they are averse to hints that reveal risks.

Any selling behavior itself will exacerbate price declines. But people choose to turn a blind eye to the "inherent risks". Now, Michael Saylor and his micro-strategy itself are the biggest time bombs or untimed ones, depending on the following:

Although less likely than Biden during Trump's presidency, if the SEC decides to investigate MicroStrategy's "unique" strategy;

According to the Investment Company Act of 1940, if a company's main business is holding investment assets rather than actual operations, it should be registered as an investment company and subject to stricter supervision. If MicroStrategy's main asset is Bitcoin, should it be registered as an investment company?

Whether MicroStrategy actually holds the number of bitcoins it claims, and whether these assets have verifiable proof on the chain, its holdings are not fully transparent;

According to the most optimistic valuation, MicroStrategy's fair price is between US$202.45 and US$214.67, while the conversion prices of its convertible bonds due in 2031 and 2032 are US$232.72 and US$204.33, which objectively requires MicroStrategy to increase its stock price;

According to my valuation model, EV/EBITDA 18 times, Implied EV/REV 3 times, MicroStrategy's stock price needs to return to 188.9 Only US dollars can eliminate the premium, which is equivalent to buying Bitcoin spot at par, but this price cannot realize the conversion price of its convertible bonds in 2031 and 2032;

Don't forget that in March 2024, MicroStrategy's stock price was still running in the $200 range (considering stock splits), and the Bitcoin price at that time was $70,078.

Trump quickly filled his regrets and gaps, at least, it also provided material.

I mean the tweet material of the founder of MicroStrategy.

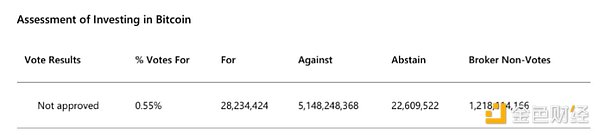

According to public reports, the vast majority of Microsoft shareholders rejected its proposal to establish a Bitcoin reserve.

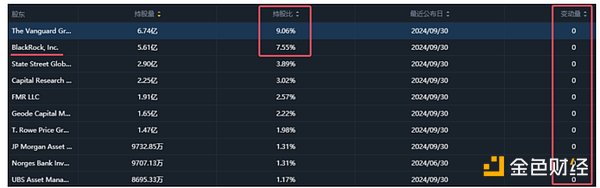

Microsoft's board of directors had earlier urged shareholders to reject a proposal from the National Center for Public Policy Research that the company invest 1% of its total assets in Bitcoin to hedge against inflation. At the annual meeting, MicroStrategy Chairman Michael Saylor gave a three-minute speech trying to convince Microsoft shareholders to support the proposal. His company has invested billions of dollars in Bitcoin. Data shows that Microsoft's largest shareholders are institutional investors, including Vanguard and BlackRock.

At the meeting, Michael Saylor, chairman of "Bitcoin giant" MicroStrategy, cited the sharp rise in MicroStrategy's stock price since adopting the Bitcoin strategy as a case to try to convince Microsoft shareholders to support the NCPPR's proposal.

Seller emphasized the growing public and political support for Bitcoin, citing the pro-cryptocurrency remarks made by incoming US President Donald Trump and the Bitcoin investment products launched by Wall Street companies. He described the trend as part of a broader "cryptocurrency renaissance."

Microsoft's board of directors opposed the proposal, calling it "unnecessary" and citing existing processes for managing and diversifying the company's financial assets.

This is not just an option for Microsoft, legendary investor and Bridgewater Associates founder Ray Dalio still chooses gold. Because he believes cryptocurrencies still face unique challenges.

"The reason I'm worried about cryptocurrencies is first and foremost privacy," Dalio said. "The government knows exactly what you own, where it is, and that's an effective way to tax it."

Dalio said that while Bitcoin has "advantages," the number one cryptocurrency has yet to fully "prove itself." He also doesn't believe Bitcoin is a proven hedge against inflation.

"The reliability of cryptocurrency, like, 'Is it correlated with inflation? Is it correlated with those things? No, not really, not very well,' he said. 'It's still very much a speculative tool.'"

He added that, unlike gold, Bitcoin probably won't become a major reserve currency anytime soon.

"It's unlikely to be a reserve of money, it won't work," Dalio said.

But there is Trump in the currency circle. Trump's so-called "crypto-friendly policy" expectations have not only helped Bitcoin reach a historical high of 100,000 US dollars, but also brought endless imagination. The latest picture is like this:

If you check the Twitter account of MicroStrategy Chairman Michael Saylor, you will find that the following style of stickers and text is an infinite loop.

It is intended to spare no effort to promote Bitcoin's "broader vision".

But this is just an episode in Michael Saylor's vision. His long-term vision is this: In 2045, the price is $13 million per coin, accounting for 7% of the world's wealth.

This is his short-term vision, that is, the vision for next year:

Let's talk about reality.

The suggestion that big companies like Microsoft promote the establishment of Bitcoin reserves may not only be part of the broader "cryptocurrency renaissance" that Michael Saylor talks about and that he has been promoting with his tweets, but it is also a practical consideration, even imminent.

And this risk is obscured by the following picture:

The charismatic leader like a messiah, the once-in-a-lifetime stock price performance that even exceeds Nvidia, and the historical high of Bitcoin!

The so-called establishment of Bitcoin reserves, the essence and the first step is to buy, which is crucial to Michael Saylor and his MicroStrategy, and it is a matter of life and death.

Michael Saylor's "debt/equity, Bitcoin, stock price" game is a double Ponzi structure, which has become the biggest time bomb in the current cryptocurrency field.

Inherent risks

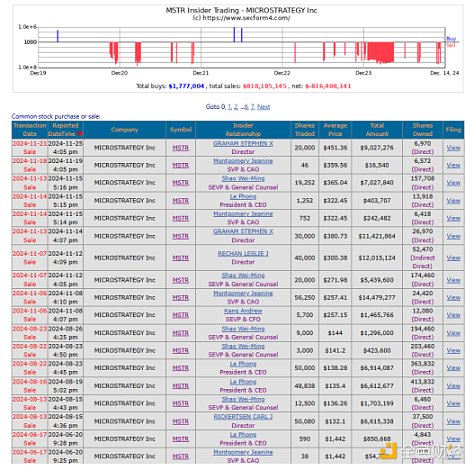

First, we need to note that although Michael Saylor has been making every effort to promote Bitcoin as a grand vision for the future, he and MicroStrategy's senior management team have been selling stocks (https://www.secform4.com/insider-trading/1050446.htm), which is an obvious contradiction and warning signal. Of course, you can think that they are selling stocks in exchange for funds to buy Bitcoin.

According to its website, MicroStrategy "provides software solutions and expert services to provide actionable advice to everyone." Since 2000, the company has accumulated a net loss of $1.4 billion. In addition, its revenue has deteriorated over the past decade.

As a software solutions company, it has gone bankrupt. However, its CEO Michael Saylor transformed a shaky technology business into a leveraged Bitcoin holding company.

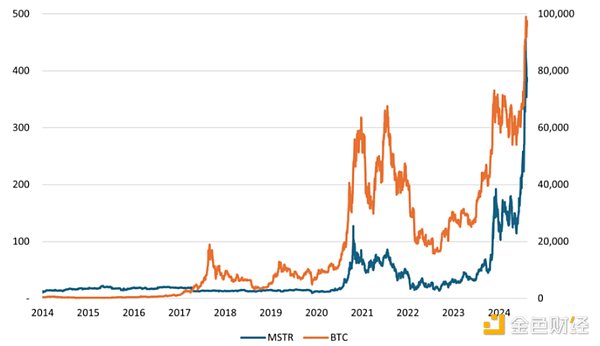

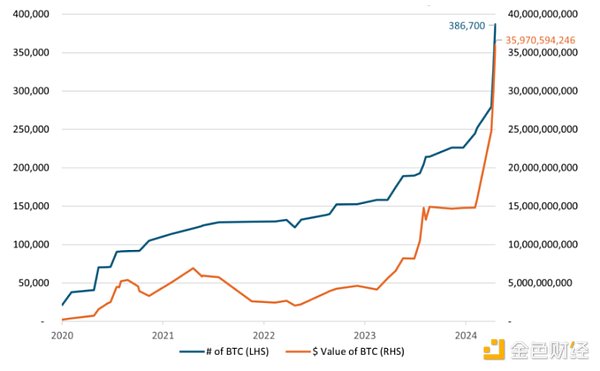

The chart below shows that once they started buying Bitcoin in 2020, its price was closely correlated with Bitcoin. The company is essentially a leveraged Bitcoin holding company, so this relationship is likely to strengthen further as it buys more Bitcoin.

According to its public disclosure, as of 2024-12-8, it holds 423,650 BTC.

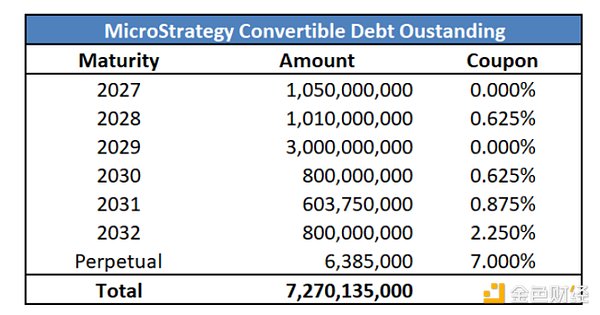

Convertible debt financing

MicroStrategy borrowed $7.27 billion using convertible bonds alone. The proceeds were used to purchase Bitcoin.

Convertible bonds are unique because they offer investors the benefits of a bond with the bonus of equity exposure. Assuming the convertible bond issuer does not default, bondholders will receive their initial investment back at maturity, earn interest, and have a call option that allows them to buy the company's stock at a specific conversion rate.

On November 21, 2024, MicroStrategy issued $3 billion of 0% convertible notes that will mature on December 1, 2029.

Its stock was trading at $430 at the time of issuance, with a conversion price of $672. The investor is willing to take the call option instead of paying interest. The stock option has value if MicroStrategy's stock rises more than 50% over the next five years. If the stock doesn't go above $672, the investor will receive a 0% return on their investment.

There's also opportunity cost to consider. MicroStrategy has a junk (B-) S&P credit rating. According to the ICE BOA Index, similar bonds yield 6.75%. A 6.75% return on investment compounded over five years provides a 47% total return.

So, the investor gives up a 47% five-year total return in the hope that MicroStrategy's stock will double in five years and break even, rather than holding a similarly rated junk bond.

On paper, it's genius. The plan is simple: borrow at zero interest with the convertible bond, buy Bitcoin, and pay off the debt when the stock converts at a low price. As long as the stock price keeps rising — and Bitcoin hovers around $100,000 at least — we’re talking about one of the most successful feats of financial engineering ever.

Bitcoin miner Mara has also joined the fray, putting $8.5 million in convertible bonds to refinance the debt and, naturally, buy more Bitcoin. The terms are pretty sweet: zero coupon and a 40% conversion premium.

The real attraction is MicroStrategy’s stock — or, more precisely, its volatility.

How could it raise $3 billion with zero coupon and a conversion price of $672.40 per share when the stock was trading at $433? The answer lies in the stock’s explosive volatility, driven and amplified by its Bitcoin holdings. That volatility significantly boosted the value of the embedded call options in the bonds, which in turn offset the cost of the bonds themselves. As a result, the company is able to borrow money at much lower rates than traditional debt.

MicroStrategy's stock is volatile. Its 252-day historical volatility is currently (2024-12-7) 106% (meaning an average daily move of 6.6%!) The implied volatility of a 30-day option on its stock is 2.5 times that of a similar-duration option on Bitcoin itself.

MicroStrategy isn’t embarrassed about this: in its third-quarter earnings report, management touted that MicroStrategy options trade at a higher implied volatility than any S&P 500 stock.

Option prices are derived from the current stock price, strike price, time to expiration, implied volatility, interest rates, and dividends. All of these factors are known except for implied volatility.

Implied volatility measures how much investors think the underlying stock will move in the future.

Convertible debt is priced based on a company’s credit risk, the bond’s interest rate, and the value of a call option. The higher the redemption value, the more proceeds the issuing company can collect. In this case, the incredibly high implied volatility of MicroStrategy’s stock pushed up the value of the options, enabling the company to raise more money.

Provided by The Block, showing that MSTR’s implied volatility is about twice that of Bitcoin.

Once MicroStrategy recast itself as an avid buyer of Bitcoin, volatility soared, first to over 70% and later to over 100%. The dynamic is self-reinforcing: Acquiring more Bitcoin amplifies stock price volatility, enabling MicroStrategy to issue convertible bonds on increasingly favorable terms, which it then uses to buy more Bitcoin—further fueling volatility. And so the cycle continues.

Michael Saylor is touting Bitcoin to drive up the implied volatility of his stock, thereby enabling him to issue debt as cheaply as possible.

He himself is a promoter and accomplice of this mechanism.

Because investors limited to fixed income investments now have a way to gain exposure to Bitcoin. However, for others who want to own Bitcoin, there are better options. MicroStrategy's stock is valued at at least twice as much as its Bitcoin holdings. And, as a reminder, its software business has almost no value. It can even be said that it has negative value. Therefore, investors who want to buy Bitcoin should just buy Bitcoin or one of the many available Bitcoin ETFs.

As of 2024-12-12, the premium to the current price of Bitcoin is 2.2 times.

Historically, convertible bonds in the energy industry have been the "richest" with implied volatility as high as 35-40%, while convertible bonds issued by technology companies have recently reached 40-45%. According to IFR, MicroStrategy's convertible bonds have an implied volatility of 60% in the market, which is unprecedented in the equity-linked market.

Investors in these bonds use various trading strategies to obtain volatility benefits, one of the classic methods is the so-called gamma trading. This strategy involves buying bonds and shorting stocks, dynamically adjusting the size of the short position to keep the combined position neutral to the stock price. The net effect is to buy when the stock price is low and sell when the stock price is high, while maintaining a long position in the convertible bond.

Here's how it works:

The investor first shorts a proportion of MicroStrategy stock based on the convertible bond's "delta" (a measure of the bond's price sensitivity to stock price changes). As the stock price rises, the bond approaches "parity", the bond's delta value increases, and the investor needs to sell more stock to remain neutral. When the delta reaches 1, the investor's short position will be equal to the number of shares expected to be converted from the convertible bond. Conversely, when the stock price falls, the bond is significantly "out of the money", the delta value decreases, and the investor needs to buy back the stock and reduce the short position. Continuous position adjustment can gain benefits from stock volatility without being affected by its overall trend.

An analogy is to harnessing wind energy: As long as there is wind, no matter which direction it blows, turbines will spin to generate electricity. For traders, volatility is the "wind" that drives their strategies. For MicroStrategy, its stock is well suited to this trade: high volatility, good liquidity, and easy to borrow to short.

The gamma trading strategy is not for amateur investors. It is very complex and requires constant adjustment of positions.

If stock volatility calms down, these volatility-based arbitrage opportunities may disappear, leaving the gamma trading "windmills" idle. (This can happen, for example, because investors in convertible bonds sell shares when the stock price rises and buy shares when it falls, thereby suppressing volatility.)

MicroStrategy's stock volatility has cooled in recent weeks, which may cause some investors to suffer losses, although these losses are insignificant compared with the previous rich gains from convertible bonds.

The potential reward for convertible bondholders is a price for MicroStrategy stock above the conversion price.

The risk of owning debt is twofold.

First, assuming the company does not default, bond investors will get their money back if the stock price falls below the conversion price. However, they will get nothing in five years.

The worst-case scenario emerges when one considers how MicroStrategy will pay off its $7.2 billion in convertible debt when it matures. Unlike most companies, the answer does not lie in the revenue it earns. Their cumulative after-tax net income since 2000 is negative $1.5 billion. The average quarterly loss over the past eight quarters is $316 million. The last time they had a profitable quarter was in 2021. Even at MicroStrategy's peak profitability, its cumulative net income is only about $650 million.

The company could issue more stock to pay off its bondholders. This would dilute existing shareholders and could reduce the share price and the value of the convertible options.

Conversely, MicroStrategy could issue more debt to pay off old debt. However, if the price of Bitcoin falls, bondholders might not accept the convertible debt and instead demand a high interest rate.

Finally, they could sell Bitcoin to pay off their bondholders. Such a plan could work if Bitcoin is trading at a high price. However, if the price is much lower, it could be very problematic. Of course, if one of the world's three largest Bitcoin holders sells in large quantities, it could seriously hurt the price of Bitcoin.

MicroStrategy's five previously issued convertible bonds - currently deeply "in-the-money", with conversion prices ranging from $143.25 to $232.72.

What happens if the price of Bitcoin (and MicroStrategy's stock price) plummets? If the situation reverses, how will MicroStrategy repay up to $6.2 billion in bond principal?

In-the-money refers to the state when the conversion value is higher than the face value of the bond.

Formula: Conversion value > Bond par value

Investor preference:

In the in-the-money state, investors tend to convert bonds into stocks because they can get higher returns.

The market price of convertible bonds reflects their dual attributes:

Bond value (debt attribute);

Conversion value (stock attribute).

When MicroStrategy's stock price is much higher than the conversion price, the price of convertible bonds is mainly determined by the conversion value of the stock. At the current stock price, the "debt value" of the bond has been completely covered by the conversion value of the stock, or even exceeded.

Each bond has a unique identification code, such as CUSIP (commonly used in the U.S. bond market) or ISIN (international standard).

Currently, the prices of MicroStrategy's previous five convertible bonds have fully reflected their conversion value, similar to the "parity" status.

If the price of Bitcoin (and MicroStrategy's stock price) plummets, MicroStrategy will face a catastrophe:

First, MicroStrategy's free cash flow cannot cover its debt, and its software business is losing money;

Selling Bitcoin to raise cash may be a last resort, but can you imagine one of the world's three largest Bitcoin holders stepping out and calling for an order to sell even 10,000 Bitcoins;

And the person who stepped out is precisely the man who spared no effort to promote Bitcoin's grand revival: Michael Saylor?

In this case, the rigid redemption of debts required by creditors coupled with the sharp drop in Bitcoin prices may cause a greater shock than the FTX incident;

The essence of MicroStrategy is a double Ponzi structure:

First, MicroStrategy's convertible bond model is essentially a Ponzi takeover of stock prices, using high volatility to earn profits (the gamma trading shown above), regardless of whether the stock rises or falls, as long as volatility is there, it is profitable, because this strategy is extremely risky. Once volatility decreases, convertible bond investors must hope that the stock price will find a buyer, otherwise they will lose everything.

This is a Ponzi scheme of stock price;

Second, the conversion price of convertible bonds previously issued by MicroStrategy is roughly 143 to 232, and the current stock price is far higher than the conversion price. However, if Bitcoin falls sharply, and the most recent convertible bond conversion price is US$672, this means that objectively the buyer needs to take over immediately. But note that even using the most optimistic valuation model, MicroStrategy's stock price is roughly only between 203 and 215 (including its Bitcoin price). Therefore, once the conversion cannot be made, MicroStrategy needs to repay the debt, but MicroStrategy's free cash flow is only about 10 million (2023 financial report); it can only borrow new debt to repay old debt. This is the second part of the Ponzi structure, the debt Ponzi.

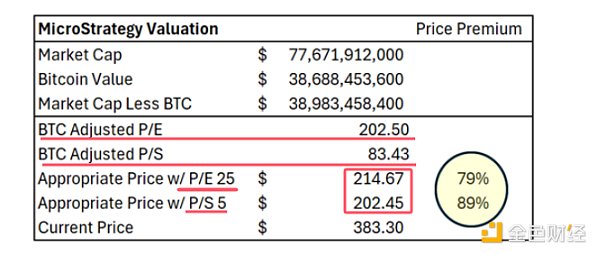

Taking the most optimistic valuation assumptions as follows: The company's market value minus the market value of its BTC holdings, combining this metric with TTM recurring EPS, the underlying business trades at a P/E ratio of 202.5. Assuming the appropriate P/E and P/S ratios for the underlying business are 25 and 5, respectively. These are very broad assumptions, as the revenue and EPS growth of the underlying business is very small in the long run. Under these conditions, the fair value price of MSTR (including its BTC position) is calculated to be between $202.45 and $214.67.

Please note that according to the most optimistic valuation and my personal valuation model;

MicroStrategy's fair value is between US$202.45 and US$214.67, while the conversion prices of its convertible bonds due in 2031 and 2032 are US$232.72 and US$204.33, which objectively requires MicroStrategy to increase its stock price;

At the same time, based on the current Bitcoin price (US$100,924) and MicroStrategy's stock price (US$411), when the Bitcoin price falls by 21% (assuming that the β between the stock price and the Bitcoin price is 3.14, this data is calculated based on historical data), the Bitcoin price is US$79,730 at this time, and MicroStrategy's stock price will fall to a death price, which will immediately trigger the conversion price of all convertible bonds. The rigid debt principal needs to be fully redeemed.

Even if β is adjusted to 2, the price of Bitcoin only needs to fall by 33%, which is roughly $67,619;

Don’t forget that in March this year, MicroStrategy’s stock price was still running at $200 (considering stock splits), and the price of Bitcoin at that time was $70,078.

MicroStrategy cannot stop because the subsequent trigger price exceeds $672.

Crypto market, what is the main line of this round of bull market? Golden Finance, the main line of this round is already relatively clear.

JinseFinanceAOVM is an AI layer protocol built on top of @aoTheComputer, combining AO's hyper-parallelism with AI large models.

JinseFinanceIn the core mechanism of Arweave, there is a very important concept and component, which is the storage fund Endowment.

JinseFinanceNaver and Kakao merge to create Project Dragon Token, a new cryptocurrency set to leverage their extensive user bases. Despite initial challenges, the merger aims to consolidate Asia's blockchain market and inject vitality into the domestic coin industry.

Weatherly

WeatherlyAs a product of its times, Dogecoin has its own set of problems. DogeLayer is here to fix just that.

Max Ng

Max NgNothing quite as scary as as innocent NFT holders unknowingly acquiring "money laundering tools.", and Tte platform's forensics data-driven approach protects holders from exactly that.

BrianJinseFinanceJinseFinanceJinseFinance

BrianJinseFinanceJinseFinanceJinseFinance Cointelegraph

Cointelegraph