Currently, Bitcoin prices continue to consolidate not far below their historical peaks, and long-term investors have begun to accumulate Bitcoin assets again for the first time since December 2023. At the same time, as the first batch of Ethereum spot ETFs were historically approved for listing in the United States, the price of Ethereum rose by 20% accordingly.

Summary

Although the prices of Bitcoin and Ethereum have been consolidating in small fluctuations since March, the markets of these two assets have shown relative strength after a long period of consolidation after experiencing historical price peaks.

The approval of the Ethereum spot ETF by the U.S. Securities and Exchange Commission (SEC) gave the market a surprise, causing the price of ETH to rise by more than 20%.

The net flow of Bitcoin spot ETFs in the United States turned positive again after four weeks of net outflows, indicating that demand from the traditional financial sector has rebounded.

Selling pressure from long-term holders has dropped significantly, while investor behavior has returned to an accumulation pattern, suggesting that the market needs higher volatility to drive the next wave.

Poised for a Rally

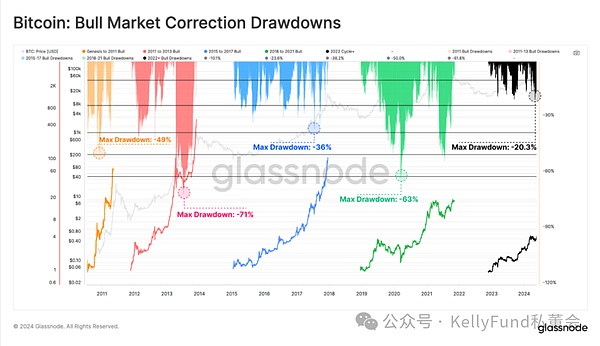

After the lowest price drop since the FTX crash (-20.3%), Bitcoin price has started to recover towards its all-time peak, reaching $71,000 on May 20. Compared to previous situations, the pattern of price retracements in the 2023-24 uptrend seems to be very similar to the retracements seen in the 2015-17 bull run.

The 2015-17 uptrend occurred during the infancy of Bitcoin, when there were no derivatives available to analyze the asset class. But now we can compare it with the current market structure, which suggests that the 2023-24 uptrend may be mainly from spot-driven markets. The launch of spot ETFs in the United States and the inflow of funds just support this assertion.

Figure 1: Bitcoin bull market adjustment retracement

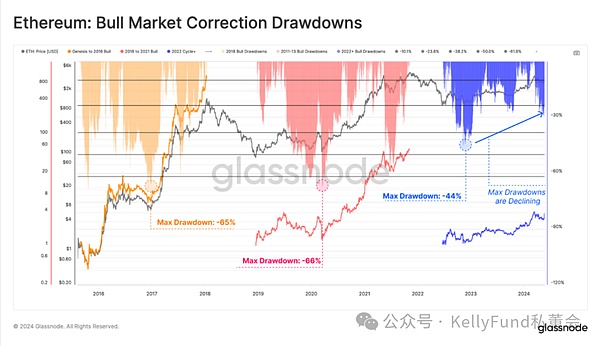

Since the low point generated by the FTX collapse, Ethereum's adjustment range has been significantly smaller than in previous cycles. This market structure shows that between each consecutive pullback, market resilience is being strengthened to a certain extent, while downside volatility is also decreasing.

However, it is worth emphasizing that Ethereum's recovery is slower than Bitcoin. In the past two years, ETH has performed significantly worse than other top crypto assets, which is mainly reflected in the relatively weaker ETH/BTC ratio.

Nevertheless, the approval of an Ethereum spot ETF in the United States is a broadly unexpected development that could provide the necessary catalyst to spur strength in the ETH/BTC ratio.

Figure 2: Ethereum bull market correction retracement

“Diamond Hands” Dominate the Market

(Note: “Diamond Hands” refers to investors who hold highly volatile financial assets and hold them even under extremely high selling pressure)

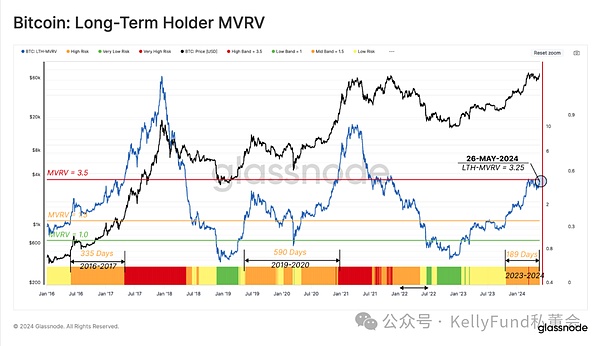

As prices rise due to new buying pressure, the importance of selling pressure from long-term holders also grows. Therefore, we can measure the reasons that are sufficient to stimulate them to sell assets by evaluating the unrealized profits of the long-term holder group, and evaluate the actual situation of the sellers through their realized profits.

First, the MVRV ratio of long-term holders reflects the multiple of their average unrealized profits. Historically, the trading profits of long-term holders in the transition stage between bear and bull markets are above 1.5 but below 3.5, and this stage can last for one to two years.

If the market's upward trend continues and eventually forms a new historical price peak in the process, the unrealized profits of long-term holders will expand. This will greatly increase their desire to sell and eventually lead to a certain degree of seller pressure, which will gradually exhaust the demand that appears in the market.

Figure 8: Bitcoin Long-Term Holder MVRV<span yes'; mso-bidi- font-size:10.5000pt;mso-font-kerning:1.0000pt;">

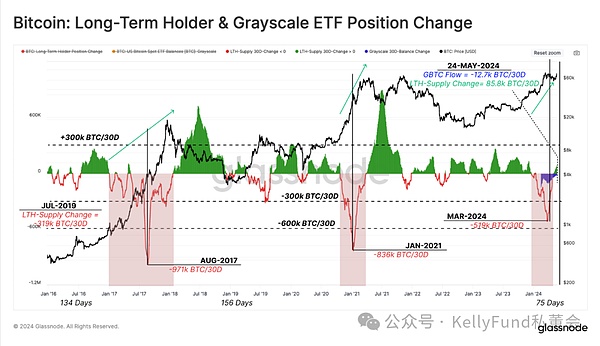

To conclude this analysis, we will assess the spending rate of long-term holders through the 30-day net position change in supply from long-term holders. The market experienced its first major asset allocation from long-term holders in March as Bitcoin was heading towards a new historical peak.

In the past two bull markets, the net distribution rate of long-term holders reached 836,000 to 971,000 bitcoins/month. Currently, the net selling pressure from them peaked at 519,000 bitcoins/month at the end of March, of which about 20% came from Grayscale ETF holders.

After this "squandering" state, the market ushered in a cooling-off period, and the local accumulation of assets caused the total supply from long-term holders to increase by about 12,000 bitcoins per month.

Figure 9: Changes in long-term holders and Grayscale ETF holdings<span yes'; mso-bidi- font-size:10.5000pt;mso-font-kerning:1.0000pt;">

Summary

After Bitcoin price hit an all-time high of $73,000, seller pressure narrowed significantly as a large number of long-term holders began to reallocate their Bitcoin assets. Subsequently, long-term holders began to re-accumulate Bitcoin for the first time since December 2023. In addition, the market demand for spot Bitcoin ETFs has also clearly rebounded, which has led to positive capital inflows in the market and reflected huge buyer pressure.

In addition, with the SEC's approval of the US Ethereum spot ETF, the competitive environment between Bitcoin and Ethereum has become evenly matched. This allows digital assets to further deepen their presence throughout the traditional financial system and is also an important step forward for the industry.

JinseFinance

JinseFinance