Enjin Completes Early Governance Snapshot, Plans Airdrop Distribution

Distribution of these rewards is anticipated within 48 hours, and users will be able to monitor the allocation progress through their Enjin wallets.

Alex

Alex

Author: Fairy, ChainCatcher

Robinhood's stock tokenization plan is in full swing. Last night, it had completed the minting of 213 US stock tokens on the Arbitrum chain, covering mainstream targets such as Nvidia, Microsoft, and Apple.

The most eye-catching of these is that Robinhood has extended its tokenization tentacles to unlisted private companies, including OpenAI and SpaceX. But just this morning, OpenAI officials urgently issued a "cut-off": no cooperation, no participation, no endorsement, and no approval of any equity transfer.

This tough statement quickly sparked controversy:Can unlisted stocks be tokenized? Do the tokens correspond to real equity?

In this regard, we have sorted out the core controversies and practical dilemmas of the current market regarding "stock tokenization", hoping to provide everyone with a clearer perspective.

1. Tokens ≠ Equity

Most stock token products on the market are essentially price-anchored derivatives, and the structure behind them is closer to trust funds or ETFs. They provide a "shadow target" on the chain of a stock price, rather than a real equity registration.

Under this model:

Users do not have any shareholder status;

No voting rights, cannot participate in corporate governance;

Do not have legal ownership of assets;

Need to bear similar fund custody and management fees every year.

Crypto KOL AB Kuai.Dong joked: "We control the market and issue additional shares ourselves. The former securities firms have become the Fed of the cryptocurrency circle today."

Second, the tokenization of unlisted stocks may trigger corporate governance conflicts in private equity

Tokenizing the equity of unlisted companies on the chain seems to be an innovation that breaks through the limitations of traditional finance, but it touches on complex and sensitive areas in terms of legal reality and corporate governance.

Private companies may restrict the "transfer" of equity through articles of association, shareholder agreements or investment memoranda. The "transfer" here does not only refer to changes in ownership, but often covers broad behaviors from pledges, derivative design to trading rights.

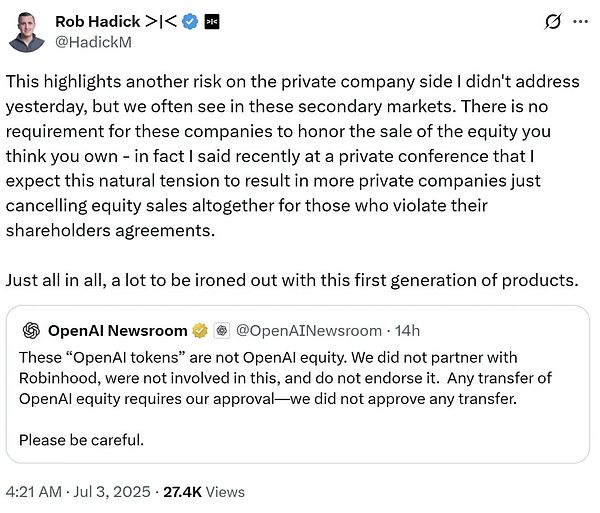

In the Robinhood and OpenAI incident, Dragonfly partner Rob Hadick pointed out that these companies are not obliged to recognize "equity sales that you think you own." He expects this natural contradiction to lead more private companies to directly cancel equity sales that violate shareholder agreements. This phenomenon is common in the secondary market.

Crypto KOL qinbafrank proposed another situation: in the private equity secondary market, the circulating shares of unlisted companies are often not direct equity, but the LP shares of the investment fund behind the unlisted company (usually held through an SPV structure and exercised by the GP). The transfer of these LP shares does not require the official consent of the company, and even the unlisted company may not be aware of the changes in the LP shares of the investment institution. However, despite the flexibility of LP share trading, it is also accompanied by extremely high information asymmetry risks.

In addition, companies such as OpenAI may always resist stock tokenization for the sake of maintaining pricing power in the secondary market, which also brings challenges to companies that promote the tokenization process.

Third, the incremental benefits are questionable and have limited appeal to large funds

Although stock tokenization has advantages such as "all-weather trading" and "global barrier-free access" at the narrative level, from the current perspective, its incremental benefits to the overall market structure are still limited, especially in attracting institutional funds. There are natural constraints.

Crypto KOL Phyrex pointed out that most of the stock tokens currently circulating on the chain are not issued by securities firms, and the core problem is that actual delivery cannot be achieved. Failure to deliver means that the price deviation may not be able to return to normal in a short period of time, and it is difficult to make positive arbitrage. In addition, it has not obtained legal approval from regulatory agencies such as the SEC, and it is impossible to attract institutional funds with large-scale trading capabilities to enter the market.

More importantly, the traditional stock market does not operate 24 hours a day, and the all-weather trading mechanism of on-chain stocks and coins is "time-dislocated" with it. Under the premise of being unable to deliver, if price anchoring is completely dependent on the oracle, the price disconnect between coins and stocks will become the norm, and deep sharing between stocks and coins cannot be achieved, resulting in systemic disadvantages in price depth and volatility.

Fourth, the triple hidden dangers of audit, compliance and security

In the last round of attempts at stock tokenization, the lack of compliance was the common crux of the failure of almost all projects. Although the overall regulatory environment of the crypto industry has improved slightly in recent years, the regulatory framework for stock tokenization is still highly uncertain or even blank.

Currently, Coinbase is actively seeking approval from the US SEC to provide users with stock tokenization trading services under the compliance framework, but there is no clear result so far.

At the same time, smart contracts and asset custody issues constitute another systemic risk in this track. Stock tokenization projects usually rely on smart contracts to undertake key functions such as asset mapping, position records and equity settlement, but once they encounter external attacks, on-chain assets may suffer irreversible losses. In the absence of supervision, it will be more difficult for users to seek legal remedies or recover corresponding assets off-chain.

If the platform (such as xStocks) has problems in operation or system, the exchanges and other partners it connects to may be quickly affected, resulting in "domino-style" involvement.

"Stock tokenization" has once again become the focus of the industry, which undoubtedly opens up a broad imagination space for on-chain finance, but the market risks behind it cannot be ignored. This journey of change is still full of unknowns and tests.

Distribution of these rewards is anticipated within 48 hours, and users will be able to monitor the allocation progress through their Enjin wallets.

AlexExplore how Riot, TeraWulf, and CleanSpark are uniquely positioned for success in the Bitcoin mining industry post-halving. This article delves into their innovative strategies, focusing on sustainability, efficiency, and the implications of Bitcoin halving for the cryptocurrency market.

Brian

BrianAccording to the Financial Times, the UN report identifies online gambling platforms, particularly those operating illicitly, as major conduits for cryptocurrency-based money laundering, with Tether being a preferred choice.

AlexExplore the groundbreaking potential of Retik Finance (RETIK) in our in-depth article. Discover how RETIK sets itself apart from Bitcoin and other cryptocurrencies with its advanced technology, enhanced security, and user-centric design. Delve into the future of digital finance with Retik Finance, poised to redefine the cryptocurrency landscape.

Weiliang

WeiliangExplore Larry Fink's, BlackRock CEO, insights on Bitcoin, Ethereum, and the transformative potential of ETFs and tokenization in shaping the future of finance.

Miyuki

MiyukiExplore the UN's latest report in this comprehensive article, revealing how USDT is central to a clandestine banking system across Southeast Asia, raising significant concerns about digital currency misuse in money laundering and organized crime.

BrianExplore the intricate legal battle between Binance and the SEC in 'Binance Strikes Back: A Detailed Look at the Counter to SEC’s Terra Lawsuit Claims.' Delve into the complexities of cryptocurrency regulation, the application of the Howey Test in digital assets, and the potential implications for the future of digital currencies. This comprehensive article provides expert insights and a balanced perspective on this pivotal legal dispute.

WeiliangExplore the intricate legal battle between Coinbase and the SEC scheduled for a pivotal court decision on January 17, 2024. Understand the implications for cryptocurrency regulation and the future of digital assets.

MiyukiKakao Pay has been a prominent mobile payment and digital wallet service player in South Korea's financial landscape since its establishment in 2014.

AlexExplore how OpenSea is revolutionizing the NFT marketplace by onboarding millions into the Web3 space. This insightful article delves into OpenSea's strategies, challenges, and potential impacts on the cryptocurrency community and the digital economy.

Brian