Author: Paul Timofeev, Gabe Tramble Source: Shoal Research Translation: Shan Ouba, Golden Finance

Digitalization of Financial Services

Throughout the history of human civilization, technology and capital markets have always developed side by side. The origins of written language can be traced back to account books, dating back thousands of years to the Sumerian cuneiform in ancient Mesopotamia, when people used symbols on clay tablets to record the ownership of livestock and goods. Doing so effectively made the Sumerians the most advanced ancient civilization of their time, as they were now able to effectively manage economic resources, promote trade and taxation, and allocate goods and labor within the city-state.

The ability to accurately record and verify asset ownership ultimately formed the backbone of civil society and the modern economy. Without such mechanisms, chaos would ensue. The tulip bubble, the stock market crash of 1929, and the financial crisis of 2008 are all classic examples of the consequences of failing to provide reliable settlement and security of ownership of economic assets throughout history.

As human civilization has evolved, so have ledgers; from clay tablets and paper certificates to computers and software programs. Technological innovations may often conform to existing market structures, or conversely, new technologies may create opportunities to disrupt the existing structure of a market, changing its underlying architecture, operations, and the participants involved.

Often, the financial services industry adopts new technologies not voluntarily, but as a response to emergencies that need to be addressed. The paperwork crisis of the 1960s led to the creation of NASDAQ, the world’s “first electronic stock market,” in 1971. This marked the biggest change to the system for clearing and settling securities transactions to date. In 1973, the Depository Trust Company (DTC) was established to eliminate the liquidity of certificate transfers by holding them in a single depository with a unified accounting ledger. However, it wasn’t until after 9/11 and the grounding of U.S. air travel that the 21st Century Check Clearing Act was passed, making it legal to clear images of paper checks instead of paper copies. It wasn’t until 2012, during Hurricane Sandy, when the DTCC vaults flooded and nearly 1.7 million security certificates were damaged, that people finally got rid of paper checks. Today, there’s still plenty of room for improvement. DTCC data shows the real cost of this rather complex and outdated system, with tens of billions of dollars in traded contracts going undelivered every day.

DTCC gives a good explanation of the risks involved: “Not only will the original transaction fail, but the party purchasing the securities may have pledged those securities in a subsequent transaction that will now also experience a delivery failure, creating a chain reaction.”

This raises the question - can blockchain solve this problem?

The Role of Tokenization

At a high level, tokenization is the process of encoding assets of economic value and their associated ownership claims on a blockchain. Blockchains are digital distributed ledgers that record and store transaction information, providing immutability (barring theoretical but increasingly difficult or costly attack vectors) and transparency of events, enabling public observability, where anyone can observe and verify that an event occurred.

“Real World Assets” (RWAs) have become a colloquial term for a variety of non-crypto assets that can be tokenized. (Kyle Samani of Multicoin Capital points out that the term “real world” is redundant, “You’re telling people who don’t use crypto that you don’t live in the real world and that you want the real world to be some weird crypto world,”but for convenience, this article will continue to use the term RWA.Real-world assets can range from financial assets like fiat currencies, commodities, stocks, and bonds to illiquid assets like real estate.

The design of the blockchain offers many compelling benefits for the tokenization of RWAs and nearly any tradable asset.

First, the atomicity of blockchain mitigates the main settlement risk of cash on delivery systems, as blockchain transactions usually exist in the form of multi-legged operations, where either all legs succeed or all legs fail. Using blockchain also eliminates the need for various intermediaries, thereby reducing costs for both buyers and sellers. This, in turn, can improve the efficiency of markets that oversee the buying and selling of various assets. Greater efficiency, coupled with the information transparency provided by blockchain, brings new opportunities for the accessibility of financial assets. Another key benefit that tokenization can achieve is increased liquidity and easier access to certain asset classes, allowing more potential market participants to participate in them, so that the liquidity of their markets grows and deepens over time. This goes hand in hand with the emergence of fractional ownership, which has brought great results to the "new generation" of financial services businesses such as Robinhood. Tokenization is not a new concept. One could argue that the history of tokenization dates back to colored coins on Bitcoin; the core idea was proposed by Meni Rosenfeld in a 2012 research paper, which was to “color” a small portion of Bitcoin with additional metadata, effectively creating a unique token that could represent ownership of an asset other than Bitcoin itself, such as a commodity, stock, or bond. Although colored coins gained momentum at the time, the idea has become obsolete as the crypto industry has evolved further. Another early version of tokenization is DigixDAO, founded in 2014 and based in Singapore, the first crowdfunding and major DAO on Ethereum. Digix will allow the existence of assets to be publicly verified through its chain of custody through its Proof of Provenance (PoP) protocol, which is built on top of Ethereum and the InterPlanetary File System (IPFS). Tether has been minting USDT on-chain since 2015 by depositing an equivalent amount of fiat currency into its reserve bank account and then issuing a corresponding number of USDT tokens on the blockchain. Circle has also been doing the same thing with USDC since 2018. According to the Rwa.xyz dashboard, at the time of writing, the total value of RWA on-chain is over $175 billion, with stablecoins accounting for the vast majority ($164 billion). The Downsides of Tokenization Some, including Larry Fink, believe that the tokenization of financial assets such as fiat currencies, commodities, stocks, and bonds is the future of the financial industry. In theory, anything with economic value can be tokenized. However, while some of the main benefits of trading assets on a blockchain may be compelling, it is important to consider the downsides of tokenization and, therefore, consider whether there are other financial tools that can more efficiently trade assets on a blockchain. Overall, tokenizing RWA requires significant effort and diligence to manage from an operational and custodial perspective. In order to ensure that the tokenized asset accurately reflects its physical underlying asset, the token issuer must purchase the underlying asset every time a new token is minted or sell the underlying asset every time a token is burned. Depending on the asset in question, the issuer must also be able to manage any operations related to the physical asset (i.e., a precious metal token issuer must manage the storage, insurance, delivery, and procurement of the metal in addition to managing the asset reserve). Overall, this can be a difficult task that is costly and takes a lot of time to implement in practice, especially at a scalable level. The adoption of tokenized assets also requires significant progress and action from a regulatory and legal perspective, which is often a long process as the situation varies from country to country. In the United States, the past four years have been largely unfavorable to crypto products and services. Meanwhile, in the European Union, the MiCA regulatory framework will be implemented by the end of this year, while Singapore and Hong Kong have been pursuing more crypto-friendly policies. There are also legal complexities associated with determining ownership and handling the disputes that arise, and local laws and regulations (i.e., at the state or municipal level) make this process even more thorny. What if investors don’t want ownership, but simply want to gain price exposure to these assets in a simpler, lower-cost, and overall more efficient way? This is where synthetic assets come into play. A synthetic asset is a financial instrument that is designed to mimic the value of an underlying asset without the investor having to hold that asset. Synthetic assets can be created and traded on a blockchain without actually having to go through any of the complex logistical processes associated with tokenization, thus simplifying the creation of on-chain markets. So far, only one type of synthetic derivative has been particularly successful - so all roads lead to Rome.

What perpetuals do

Perpetual swaps (perps) are a type of derivative contract that allows investors to speculate on the future price of an asset without a pre-determined expiration date. These financial instruments can be held indefinitely, which is an important distinction from traditional derivative contracts that involve an expiration date and must be settled before or during the expiration date. Similar to contracts for difference (CFDs), perpetual swaps provide investors with a financial instrument that allows them to speculate on the price movement of an asset for an indefinite period of time using leverage, but do so while maintaining a single, unified contract.

Although perpetual futures draw much inspiration from the Hong Kong Gold and Silver Exchange’s perpetual futures market, it was first proposed by Robert Shiller in a 1992 research paper in response to the lack of liquid derivatives markets for many components of global wealth, such as human capital/labor costs, real estate, private financial assets, and macroeconomic indices.

“In order to create a market for the present value of the cash flows represented by some dividend or rent index, we need to create a permanent claim on the cash flows represented by that index.” - Shiller

Motivated by the lack of hedging tools in infrequently priced, illiquid markets, Shiller proposed perpetual futures contracts as an excellent comprehensive risk management tool for a wide range of use cases, including labor cost markets, commercial real estate, commodities, and agriculture. Given the large spreads these markets often face, Shiller believes perpetual contracts can offer hedgers significant cost savings and reduce basis risk. In short, perpetual futures are designed to facilitate price discovery for assets that are illiquid or difficult to price. Unfortunately for Shiller, the difficulties of implementing perpetual futures contracts have hampered their adoption in the capital markets and financial services sectors. These include regulatory hurdles, lack of adequate infrastructure, and the complexity of properly pricing the underlying assets, but ultimately, perpetual futures are traded almost exclusively in the over-the-counter (OTC) market. Believe it or not, the first use case for perpetual contracts was cryptocurrency trading, and it remains the only active use case to date.

Perpetual Contracts in Crypto

In 2011, Alexey Bragin sought a way to differentiate his Bitcoin futures ICBIT exchange from other exchanges on the market, which led to the creation of “inverse perpetual contracts” where contracts were settled in Bitcoin but priced in USD. However, it wasn’t until BitMEX launched its first perpetual leveraged swap product, XBTUSD, that perpetual contracts began to gain widespread adoption. BitMEX renamed its derivative contracts to perpetual swaps and introduced features designed to attract smaller, crypto-native traders rather than large financial institutions, including small contract sizes, Bitcoin-inspired contract design, minimum margins, and low trading fees.

At the time, cryptocurrencies were primarily traded off-chain through centralized exchanges (CEXs), but this would soon begin to change with the rise of spot decentralized exchanges (DEXs) in the late 2010s. At its core, a DEX is simply a set of smart contracts, plus an interface for users to interact with from their wallets, allowing anyone to trade any supported asset while maintaining full custody of their own assets. The first derivatives DEX was born in August 2017 when Antonio Juliano launched dYdX on Ethereum, eventually shifting focus to become the first perpetual DEX in April 2021 with dYdX v3. Since then, the number of perps on DEXs has continued to grow with the rise of L2, with on-chain perps trading over $2.7 trillion according to Artemis.

Perpetual swap exchanges share some key features, such as funding rates, underlying price discovery mechanisms. Perpetual swaps have no expiration date, so an ongoing payment mechanism is required where counterparties pay each other based on market conditions at a particular time. When the funding rate is positive, longs pay shorts. When the funding rate is negative, shorts pay longs.

Nevertheless, the growing number of Perp DEXs has led to a variety of designs and functional implementations worth dissecting.

Order Books

Order books have long been the default price discovery mechanism for exchanges, where buy and sell orders are listed and matched on a unified matching engine. A common adaptation of this model is to utilize an off-chain order book for trade matching, while executing and settling trades on-chain. This model enables protocols to avoid incurring gas fees and being hampered by network performance, while still benefiting from the transparency of on-chain settlement and trader self-custody. Going a step further is a fully on-chain order book, where the matching of trades also occurs on-chain. This model has historically been difficult to implement, as latency and throughput limitations of the underlying chains have enabled sophisticated actors to conduct front-running and mezzanine attacks and extract value at the expense of uninformed retail traders, who in turn receive worse price settlement on their trades. However, the rise of high-performance execution environments — whether new general-purpose L1s, application-specific chains, or rollups — seek to mitigate this problem by significantly reducing block times, thereby minimizing information asymmetry between market participants.

Peer-to-Peer Pools

Peer-to-Peer Pools Perpetual DEXs use a self-matching algorithm where buy and sell orders are routed through a central liquidity pool and matched using a price feed oracle. Pioneered by GMX, this model operates with two counterparties - liquidity providers (LPs) who lend funds to the central pool and traders use these funds to complete trades. While LPs bear inventory risk, they are subsidized through trading fees, liquidation rewards, and funding fees, while traders benefit from price execution on a real-time price index with low slippage. However, this dynamic creates an adversarial environment between LPs and traders: LPs profit from traders' negative P&Ls, but suffer losses from pool rebalancing when traders are profitable.

Virtual AMM

Another design implementation that has emerged in the perp DEX space is the virtual AMM (vAMM) pioneered by Perpetual Protocol (a well-known name). Similar to Peer-to-Pool, vAMM uses a two-party system consisting of LPs and traders. However, instead of leveraging real tokens to provide liquidity, vAMM leverages virtual synthetic assets (i.e. perps). In this model, there is no actual liquidity pool in the protocol; traders are able to leverage assets stored in the smart contract vault.

Perp DEX has made great progress since its inception, but its potential remains untapped due to being limited to trading crypto assets. Let’s dive into a specific protocol that aims to expand the utility of on-chain perps beyond crypto assets to enable the on-chain trading of almost anything in your eToro account - the Ostium Protocol.

Ostium Protocol Deep Dive

What is Ostium?

The Ostium Protocol is an open-source decentralized exchange for trading blue-chip crypto assets and RWAs in the form of on-chain perpetual contracts. At its core, the protocol is a set of smart contracts that live on Arbitrum Layer 2, consisting of a trading engine and liquidity layer, as well as an internal oracle and automated custody system that are key supporting infrastructure components. In summary, the protocol offers several key products: virtual access to off-chain assets (assets that do not exist on-chain); a shared liquidity layer consisting of two capital pools (liquidity buffer + market making vault) that settle trades and act as counterparties to traders; near sub-second price information enabled by a dual oracle system; automation of key trading functions including liquidations, stop-loss, and limit orders; and a strategic risk-adjusted fee structure to capture and minimize the directional risk posed by open positions on the shared liquidity layer.

From a design perspective, Ostium chooses to use a peer-to-pool model, but it also has its own unique twists, which are explained in detail below. The choice of a peer-to-pool model makes sense because the market is not mature enough to make markets for long-tail assets such as soybeans or hog prices; instead, using a shared liquidity layer for price discovery allows for a more scalable deterministic model.

Ostium’s Vision

Ostium believes that the best way to meet trader demand for on-chain RWA leverage, short-term and medium-term price exposure is through oracle-based perpetual contracts. Its goal is also simple: to become the premier destination for trading almost any asset in the form of oracle-based perpetual contracts.

The cryptocurrency market and macroeconomic environment are increasingly converging, and the post-pandemic macroeconomic situation has stimulated the interest of more and more macro-focused traders. The reaction of cryptocurrencies to the yen carry trade and the Nikkei index unwinding is a good example; if someone went around telling altcoin traders to pay attention to the Bank of Japan’s movements because it will have a significant impact on the performance of their tokens, they would be laughed at. However, last week, this theory was proven to be correct. Polymarket’s surprising rise in a US election year also demonstrates interest in speculating on the outcomes of real-world events; in fact, there is even a positive correlation between Bitcoin’s price and Donald Trump’s odds of being elected president. Ostium proposes that perpetual contracts will be the preeminent financial tool to power a boom in blockchain capital markets. Let’s take a deeper look at the components that are working together to realize this vision.

Key Protocol Components

Ostium Trading Engine

The Ostium Trading Engine is a key feature of the Ostium protocol, facilitating trading of assets supported by the protocol by coordinating interactions between traders and LPs. After depositing collateral, traders can choose to go long or short; place market orders, limit orders, or stop orders, and customize leverage settings (Ostium offers up to 200x leverage). The Gelato function is used to continuously track price changes and determine whether orders need to be automatically executed (liquidation, stop loss, profit orders), while using a pull-based oracle mechanism to call prices on demand. During the position, users can update their positions (update profit, update stop loss, or add collateral) without paying additional fees. Positions can be closed manually or automatically; triggered by a stop loss order (negative P&L), take profit (positive P&L) order, or liquidation. If a trader’s collateral value drops by 90%, the keeper triggers a liquidation event and the remaining collateral (10%) is transferred to the market making vault as a liquidation reward.

Opening Price and Price Impact

To protect LP capital from the risks associated with peer-to-pool based pricing models, Ostium has implemented a price discovery approach that incorporates real-time market liquidity conditions when determining the price at which traders open positions. While the mid-price is often used as a neutral valuation metric, relying on it alone can be misleading in situations where liquidity significantly impacts the quality of execution a trader receives. Instead, Ostium employs a scaled bid-ask spread model that more accurately reflects true market conditions and costs associated with different trade sizes.

The bid-ask spread represents the difference between the highest price a buyer is willing to pay (the bid) and the lowest price a seller is willing to accept (the ask), and in Ostium's model, this spread is adjusted dynamically. Under this model, the spread is linear with the position size, meaning that the larger the trading volume, the larger the spread. Therefore, traders will not always get the bid or ask price, but rather a scaled version of these prices, such as 0.1 times the middle bid spread or 2 times the middle ask spread, depending on the specific circumstances of the transaction.

When a trader opens a long position, he is quoted a proportionally calculated ask price, and when he opens a short position, he is quoted a proportionally calculated bid price. Similarly, when closing a long position, he is quoted a proportionally calculated bid price, and when closing a short position, he is quoted a proportionally calculated ask price.

This can be expressed by the following formula (assuming K is a constant):

< mjx-c>< /mjx-mi>

Oral Liquidity Layer

Rather than a central limit order book (CLOB) model, Ostium operates as a liquidity pool-based DEX, similar to well-known perp DEXs such as GMX. This model enables the protocol to maintain an imbalance of open interest, but there is a key difference between the Ostium model and traditional perp contracts, where liquidity providers directly benefit from traders' losses, creating an adversarial relationship between two sets of market participants who are equally important to the protocol.

Ostium's Shared Liquidity Layer (SLL) consists of two capital pools - a liquidity buffer, which serves as the first layer of settlement for positive PnL trades, and a market making vault, which acts as a fallback when the liquidity buffer is exhausted. Note that the capital in the liquidity buffer comes from accumulating traders’ PnL, while the market making vault is open to LPs for deposits in exchange for liquidation rewards and 50% of the opening fee. The core idea is that by creating two isolated pools with strategically defined fee structures, LPs primarily benefit from increased trading volume and OI growth. LB is designed to absorb traders’ PnL, thereby stabilizing LPs’ APY while traders continuously earn positive PnL, which means that traders and LPs should benefit from protocol growth at the same time. Liquidity Buffer LB is the primary settlement layer for trades on Ostium, meaning that trade execution does not require a direct counterparty. Given that LPs cannot deposit or withdraw from LB, this ensures that the value accumulated by LB reflects organic trading activity on Ostium.

LB funds positive P&L trades while capturing any value from negative P&L trades when positions are closed. When one side is unbalanced, OI deviates from 0 and LB absorbs volatility in trader returns and helps stabilize APY LP's earnings.

Consider the following possible states of delta exposure in the protocol depending on market conditions;

Perfect Balance - When traders' long and short positions are equal, the protocol's delta exposure is 0 and the market is stable as positions naturally cancel each other out.

Imbalanced OI – When trader positions are imbalanced, i.e. there are more longs than shorts or vice versa, the shared liquidity layer will step in to compensate for the imbalance and regain delta exposure.

Extremely Imbalanced OI – When no trader takes one side of the market (all longs or all shorts are closed), the liquidity buffer takes all the delta risk.

If a series of large trades with positive P&L are closed in succession, the liquidity buffer may be depleted by settlements that must be paid. If this happens, the protocol will turn to the Market Making Vault (MMV) for trade settlement.

Market Making Vaults

Ostium’s MMVs are smart contracts structured as liquidity pools where LPs deposit funds to earn an APY defined by liquidation rewards and 50% trader opening fees to cover the delta exposure risk they take. This will play a particularly important role in the early stages of the protocol, as ongoing trader P&L may take a while to accrue to LBs, so incentivizing LPs to deposit MMVs is critical to the Ostium protocol.

Upon depositing capital into an MMV, LPs receive an Ostium Liquidity Provider (OLP) token, which can be used as a standard deposit receipt. OLP tokens are minted on deposits and destroyed on withdrawals, and LP rewards are distributed according to a rebasing model where they compound directly to increase the value of the OLP token (if Alice starts with 100 OLP and earns a 10% reward, she will have 110 OLP upon withdrawal). As a means of incentivizing stickier capital among LPs, Ostium will enable annual lock-up boosts to support longer-term lockers in earning larger rewards. Supporting Infrastructure Ostium leverages two key off-chain infrastructure components, an oracle and an automated custody system, designed to support operations on the trading engine and SLL as efficiently as possible.

RWA Oracle

To address the complexities of RWA (i.e., OTC trading hours, futures contract rollovers, opening price gaps), especially when dealing with a variety of less traded, long-tail assets with low volume and high volatility, Ostium Labs developed an in-house oracle service and configured it to its unique needs. However, operating a fully in-house oracle service places significant trust assumptions on protocol users, as their trading results and liquidity provision depend on the functionality of this oracle. To ensure disintermediation and mitigate the risks associated with operating an in-house oracle, the node infrastructure is operated and managed by Stork Network, an open data marketplace consisting of a decentralized network of data publishers. Note that this model operates on a pull-based oracle system, meaning that prices are communicated on-chain only when there is a clear need to execute a trade, saving costs associated with constantly publishing data on-chain. In short, Ostium’s RWA oracle is custom-built by Ostium Labs, while its nodes are operated and managed by Stork Network. Crypto Oracles In addition to RWA, Ostium also offers leveraged trading for BTC and ETH. For these assets, prices are pulled via Chainlink data streams, which are purpose-built to provide applications with on-demand access to high-frequency market data.

Automatic Keeping System

To execute and manage conditional trades (i.e. “long HOG at $80, take profit at $100”), perp DEX uses specialized agents called Keepers. Protocols typically run Keepers first and then gradually become decentralized over time, although there is never a guarantee that they actually will be decentralized. Under this approach, the experience of traders and LPs remains more dependent on the underlying protocol. As a result, Ostium has outsourced the responsibility of running its Keeper network to the Gelato Network; from day one, Gelato Functions will be used to monitor market order price requests routed on-chain, as well as existing open interest, to understand the necessary conditions to trigger RWA automated orders. Automated orders include limit orders, stop limit orders, take profit, stop loss, and liquidation.

Fee Structure

Ostium seeks to ensure that every source of risk in the protocol is mitigated - open interest skew, high pool utilization, and high asset volatility - by strategically implementing fees. Ostium charges a fixed fee when a position is opened, and a compounding fee when an open position is maintained. The fixed fee is used to cover the associated infrastructure costs, while the variable fee is designed to mitigate the various protocol risks listed above.

When a position is opened, Ostium charges an opening fee, which is composed of five variables to account for external factors that affect a particular trade. Three of the variables depend on the trader's asset, leverage, and position size, while the remaining two depend on the protocol's OI deviation and exploitation conditions. The size of the opening fee depends on its impact on the protocol's conditions; trades that increase OI deviation (i.e., short positions that increase the short OI of an asset) create greater delta exposure for the LB and therefore incur a higher base fee. In addition, exploitation fees are charged if trades push OI above a certain threshold during periods of high utilization. As a means of encouraging arbitrage on Ostium, which is critical to maintaining price stability and equilibrium, traders are charged a "taker" fee if leverage exceeds 10x or OI deviation increases with trading. Conversely, if leverage is less than 10x and OI deviation decreases with trading, traders are charged a "maker" fee.

Maintenance Fee

Throughout the trading period (while positions are open), compounded fees will be used to a) help guide the protocol OI towards equilibrium via the funding fee and b) mitigate LPs’ directional risk exposure via the volatility fee.

The funding fee functions similarly to the standard funding rate on perpetual exchanges, aiming to close the gap between long and short OI so that the protocol reaches equilibrium and minimizes the delta risk of LPs in MMV. However, unlike CEXs that can charge funding rates, Ostium automatically charges the position value on the “hot” side and injects that value into the PnL on the “unhot” side, with the gains realized in the trader’s PnL when the position is closed. Additionally, this fee is velocity-based, meaning it is an integral of the length and magnitude of the previous imbalance. This design feature is intended to incentivize arbitrageurs to completely eliminate OI imbalances, compensating arbitrage behavior to a greater extent if the negative externality of the previous state is large. The formula is expressed as a percentage per day and can be expressed mathematically as: At the same time, the volatility fee is designed to capture the external impact of market volatility on LPs. The fee is automatically deducted from the trader's position size and is deducted from the position profit or loss when the position is closed. From an LP perspective, a 10x long position on a relatively stable asset like the Euro carries far less risk than a 10x long position on an asset that is more volatile intraday like oil. LPs must be appropriately compensated for the additional volatility risk they may be taking. However, it is also important to ensure that this fee does not deter traders from trading volatile assets, thereby affecting funding rates. Therefore, the volatility fee is strategically designed to be 10x lower than the funding fee. The fee is automatically deducted from the trader's position size and from the position profit or loss when the position is closed, which can be mathematically expressed as: fr(v) = F(Vs(s−1)Vs−v−s + 1) LP Rewards It is worth mentioning that LPs who deposit funds to MMV will receive a) 50% of the account opening fee, and b) 100% of the liquidation reward.

To summarize, here is the capital flow at each stage of an Ostium transaction;

Opening Trades: A percentage of the initial collateral is reserved for the protocol opening fee and is evenly (50/50) split between the market making treasury (where LPs deposit money) and protocol revenue.

Holding Trades: Volatility fees are accumulated period by period on open positions and go directly into the liquidity buffer.

Liquidity Buffer = 0: LP MM Vault settles trades if and only if the liquidity buffer is exhausted (see here for more details):

If Positive P&L:

If Negative P&L:

Unliquidated: The liquidity buffer receives the trader's losses;

Liquidated: 90% of the initial collateral (trader losses) goes into the liquidity buffer, and the remaining 10% goes into the LP MM vault (liquidation reward)

Risks and Considerations

The main risk of trading perpetual contracts on any exchange boils down to the liquidation risk. When opening a position, traders deposit collateral; through leverage, they can take on position sizes far greater than the value of their collateral (up to 20x on Ostium). However, the flip side is that losses are magnified just as gains are, which can lead to rapid liquidations if the market suddenly moves in a direction that is unfavorable to the trader. When a trader's losses equal the initial collateral used to open a position, the position must be liquidated to avoid the protocol incurring a bad debt (a deficit that must be covered). On Ostium, liquidations must occur before the value of the collateral drops to zero; therefore, liquidations occur when the value of the collateral drops to 10% of the original deposited collateral. While Ostium has developed many built-in mechanisms to mitigate the directional risks that affect liquidations, traders who open positions using leverage must still be familiar with these associated risks and implied losses. On the other hand, the biggest risk for LPs depositing to MMV is directional exposure risk; this occurs when LPs are exposed to sudden changes in underlying market prices, which is caused by the simultaneous occurrence of high OI imbalances and high volatility. The following matrix illustrates how the risk of directional exposures changes accordingly:

Competitive Landscape

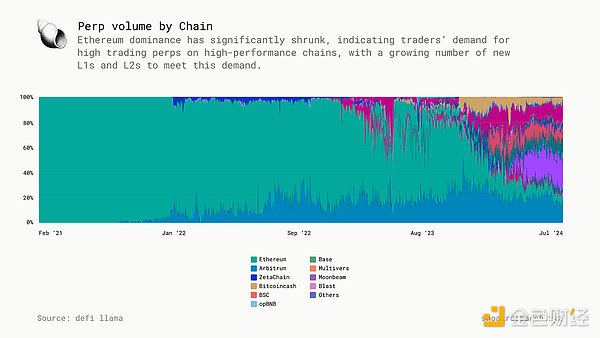

Perpetual swap trading is largely dominated by centralized exchanges (CEX), which can be explained by the lack of sufficient decentralized exchange infrastructure in the early stages of blockchain and cryptocurrency development (Uniswap V1 was launched in 2018), as well as the lack of sufficient blockchain infrastructure to achieve low fees and high performance. With high-performance Layer 1 (i.e. Solana) and rollups (i.e. Arbitrum, Base) hosting more and more on-chain activities, blockchain is not only a resilient and secure ledger for storing information, but also a high-performance network that can achieve near-instant settlement and transmission of information and value.

Ostium’s Advantages

Currently, there aren’t many teams building exchanges to facilitate trading of RWAs as on-chain perps. As such, Ostium has an opportunity to gain a first-mover advantage here and build a moat around its product. That said, if Ostium open-sources its code, one can expect many forks to be launched, in addition to the various protocols that could be built on top of Ostium. Forks aren’t a bad thing — sometimes imitation is indeed flattery, and a large number of forks can often be an indication of a good idea and a strong core product. That being said, vampire attacks could be a cause for concern — a perps DEX could decide to offer a similar market to Ostium, but provide greater incentives for traders and LPs through inflationary token issuance (so far — Ostium has no token). However, Uniswap is still ahead of Sushiswap in most metrics today, and Ostium will likely do the same if it acts and launches in time.

Ostium open-sourcing its code also raises some questions - what can be built on top of the RWA perps exchange? Will these developments benefit Ostium, and if so, how? Can Ostium gain enough momentum and adoption initially so that potential competitors have more incentive to build or integrate on top of Ostium, rather than trying to build a competing product more directly (i.e. something similar to the Curve/Convex ecosystem)?

Protocol KPIs and Roadmap

Given that Ostium is currently in the public testnet stage, protocol data must be treated with caution as numbers may change as the mainnet launches. That being said, looking at the testnet leaderboard, the numbers for the latest competition look pretty impressive; Total Traders 15.9k || Total Volume 88.9k || Total Volume $13.54B Looking ahead, we are excited about several things at Shoal; firstly, Ostium has just recently completed its first smart contract audit with Zellic, and is expected to release details of another audit with Three Sigma in the near future; the mainnet is about to launch, apparently 95% complete; and it seems that the Ostium mobile app is also in the works. In addition, we have posed several questions to the Ostium team below that can serve as a guiding framework for future research.

Questions about Ostium

Why build on Arbitrum/L2 as opposed to an L1 like Solana which is optimized for the speed and performance required for the Perps market?

Why build on Arbitrum specifically?

How do you imagine the MEV landscape in commodity markets? How does this differ from crypto markets, if at all?

With its open source code, does Ostium envision any product or service being built on top of the exchange?

Conclusion

The Case for Bringing Capital Markets On-Chain

To quote Larry Fink’s grand vision for tokenization again; imagine a globally accessible distributed ledger with hard-coded immutable evidence of who is buying, who is selling, and who owns how much of an asset at any given time, and everything can be settled near-instantly. This scenario describes a fairly egalitarian financial services industry, but it also illustrates the ultimate purpose of blockchain - to achieve transparency, immutability, and faster settlement than existing services and markets.

Meanwhile, Grayscale’s Zach Pandl believes that many types of assets (such as stocks) are relatively well served by their current digital infrastructure, and it is not obvious whether public blockchains are a better solution. Instead, he believes that the potential key advantage of tokenization is greater network effects. By implementing a universal platform to host all assets globally, we can create a financial system that is more powerful, more accessible, and less expensive than existing solutions.

Ostium: Perpetual Contracts Are Better Than Tokenization

Ostium believes that perps will eventually preempt trading of tokenized RWAs as the primary means of bringing non-crypto assets on-chain. A large part of the reason perps have become so popular and successful in the crypto space is that they “allow for simple directional bets and abstract away the complexity of expiring futures and options.” Where tokenization is plagued by operational management and regulatory hurdles, perps offer significant efficiency and listing advantages. All that is really needed to build a perps market on-chain is sufficient liquidity and a strong supporting data feed. This becomes especially easy for protocols whose pricing feed infrastructure is deeply integrated with existing traditional financial data service providers. Unlike tokenization and its associated complexities (i.e. composable KYC mandatory token standards), perpetual contracts do not require the underlying asset to exist on-chain - traders here only trade derivative contracts. To build a liquid perps market on-chain, the underlying spot market does not need to be on-chain or directly integrated into the cryptocurrency. This is not to say that tokenized markets will not exist - one day everything will be settled on-chain. Capital markets will likely gravitate to blockchain networks for enforcement and verifiability, which will happen in two ways, as eloquently described in An Unreal Primer; first, by recognizing RWA tokens as bearer assets across jurisdictions, thereby enforcing the legal protections of the owner; and second, by integrating collateral and other forms of lender protection directly into smart contracts to provide stronger guarantees than the existing legal system.

However, the reality is that it will take a long time for every liquid open market to be issued and settled on the blockchain, as it will take a long time for blockchain to become the ultimate record book and source of truth for financial institutions. Until then, perpetual contracts ultimately offer a better option for traders as they offer more flexibility, leverage, and segmentation than spot markets. Going forward, Ostium is betting that perpetual contracts will become the default listing engine for RWAs and be able to support market liquidity and depth to incentivize participation from traders of all backgrounds and interests.

One could argue that a potential barrier to wider adoption of perpetual contracts by retail investors is the complexity of these financial instruments. Perpetual contracts require many additional factors to be considered compared to spot markets, such as the relationship between collateral and leverage, how the funding rate works and how it affects profits and losses, and the difference between the price of the underlying asset and the price of the perpetual contract. That being said, Robinhood made options fun and accessible to retail investors, generating $154 million in revenue for them in Q1 2024 alone, and options are likely more complex than perpetuals, which are also the most successful product developed around crypto assets. So, perhaps all we’re missing is a user-friendly perpetual DEX for trading nearly any asset on-chain.

Where else can people bet on the price of hogs, soybeans, oil, foreign exchange, etc. through an on-chain platform?

Preview

Gain a broader understanding of the crypto industry through informative reports, and engage in in-depth discussions with other like-minded authors and readers. You are welcome to join us in our growing Coinlive community:https://t.me/CoinliveSG

Competitive Landscape

Competitive Landscape  Ostium’s Advantages

Ostium’s Advantages

Bernice

Bernice