Ethereum vs. Solana: Advantages and Challenges

This article compares Ethereum and Solana, exploring their strengths and weaknesses. We hope that readers will gain a clearer understanding of the uniqueness of each platform.

JinseFinance

JinseFinance

Following a proposal aimed at limiting the rapid expansion of Staking Pools, the current Ethereum community is discussing another measure to change ETH policy, which is driven by Liquidity Driven by surge in demand for re-staking and re-staking protocols.

Abstract

Following the proposal to reduce the ETH issuance rate, the Ethereum community is currently engaged in a heated debate over more ETH policies.

Innovations in pledge methods such as liquidity pledge, heavy pledge and liquidity heavy pledge have brought additional benefits to investors opportunity, and there is no doubt that this has significantly boosted staking demand in the market.

But another potential impact that has to be taken seriously is that people may worry that the increasing popularity of pledged derivatives may weaken Ethereum Its function as a crypto asset triggers changes in the governance power of the Ethereum network.

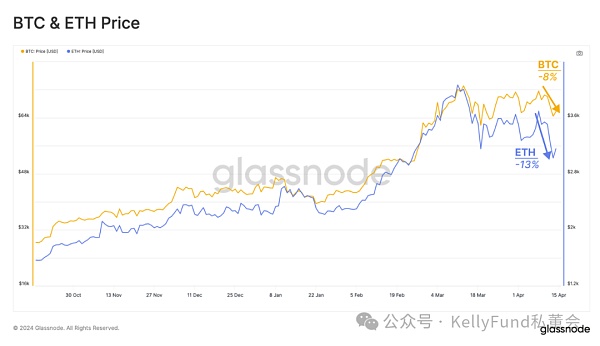

Over the weekend, geopolitical tensions in the Middle East continued to intensify. Given that cryptoassets are the only assets that trade over the weekend, the impact was immediate - crypto markets immediately saw a significant decline over the weekend. BTC prices fell by 8%, while ETH prices fell by 13%. Although the market stabilized and recovered slightly after this wave of decline, it then continued to fall sideways. In the wake of this incident, investors are cautious about the long-term impact that the attack on Israel may have on the crypto asset market.

There has been considerable controversy within the Ethereum ecosystem regarding potential changes to its issuance rate. The discussion this time was triggered by a proposal by two Ethereum researchers to slow down the issuance of ETH and thereby reduce staking rewards. The overall goal of this proposal is to curb the rapid growth of Staking Pools at this stage, to better manage new staking methods such as liquidity staking and re-staking to establish their growing dominance, and to protect Ethereum as a crypto asset. Function.

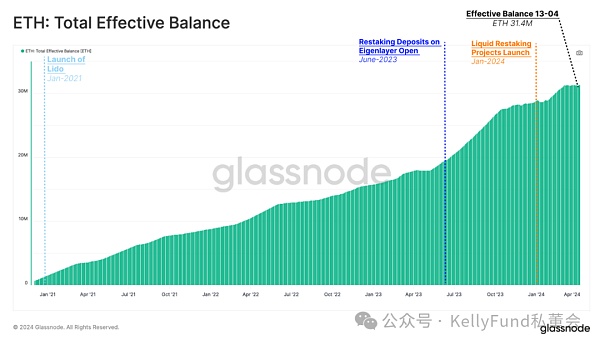

26% of the amount). In addition, we can also see that the growth rate of pledged ETH is still accelerating in recent months - especially when new staking protocols such as the Eigenlayer re-pledge agreement in June 2023 and the liquidity re-pledge agreement in early 2024 were After launch.

Distorted incentive mechanism

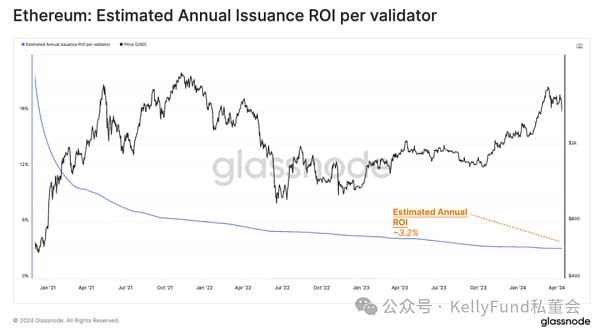

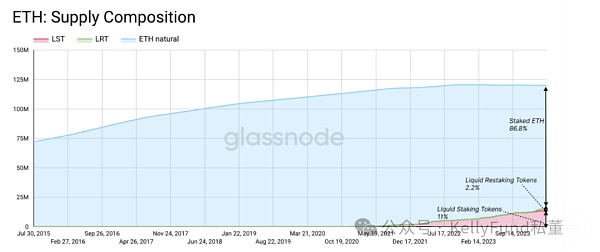

Originally, the design concept of proof of stake was that as the staked ETH increased, each The marginal income of validators will decrease. Therefore, this mechanism can realize self-regulation of the size of the Staking Pool. Currently, a total of 31.4 million ETH is pledged in the Staking Pool, and the annual interest rate of each validator is expected to be approximately 3.2%.

However, new technological developments such as maximum extractable value (MEV), liquidity staking, re-staking and liquidity re-staking have brought more profitable opportunities. As a result, the incentives and demand for users to stake have increased, and this demand has now exceeded the vision when Proof of Stake was originally designed.

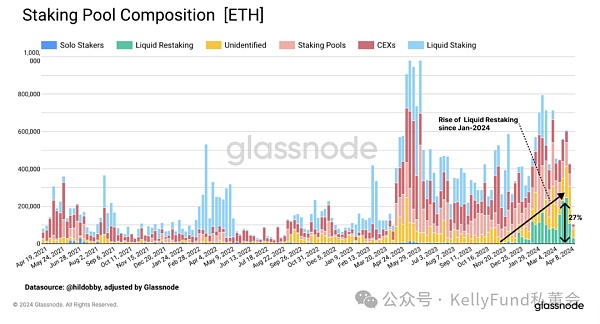

If we classify the Ethereum assets participating in the pledge according to different staking protocols, we will find that since the beginning of this year, the number of assets pledged by liquidity-heavy staking providers The amount of ETH pledged has increased significantly, and the amount pledged under the protocol now accounts for 27% of the total amount of new pledged ETH, while the amount of new pledges from liquidity staking providers has been decreasing since mid-March.

The concept of heavy staking was introduced by the EigenLayer protocol last year. Under the EigenLayer protocol, users are able to deposit their staked ETH or liquid collateral assets into EigenLayer smart contracts, which can then be used as secure collateral assets by other protocols such as Rollup, Oracle, and Bridges. In addition to the native staking benefits from the Ethereum main chain, stakers under heavy-staking protocols can also earn additional fees from these protocols.

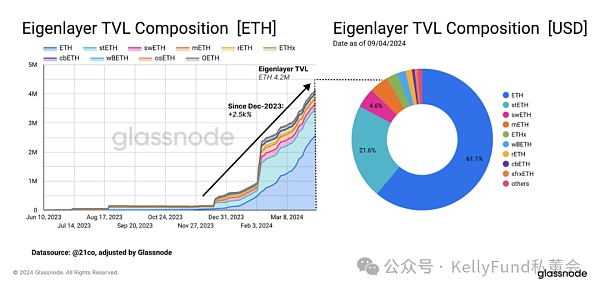

Since the launch of the protocol, the pledged assets on the Eigenlayer protocol have surged, and its total locked value (TVL) currently exceeds 14.2 million ETH (worth approximately 13 billion Dollar). Another point we need to note is that the high demand for heavy staking from staking investors also partly comes from high expectations for the Eigenlayer airdrop event.

Under the Eigenlayer protocol, more than 61.1% of TVL comes from native pledged ETH, while the rest is composed of pledged assets in the liquidity pledge agreement, of which Lido’s stETH is in the leading position, accounting for 21.5% of the total TVL.

The rise of liquidity staking

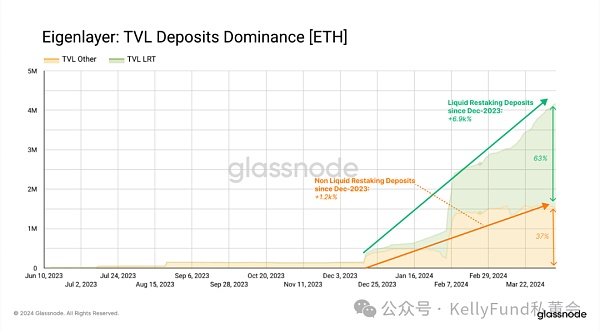

Liquidity staking works very similarly to liquidity staking, allowing users Rehypothecate their assets and receive liquidity in their rehypothecated assets in return. There is no doubt that this seems to be a staking strategy preferred by Eigenlayer users - currently, 63% of ETH staking in Eigenlayer is through liquidity-heavy staking providers.

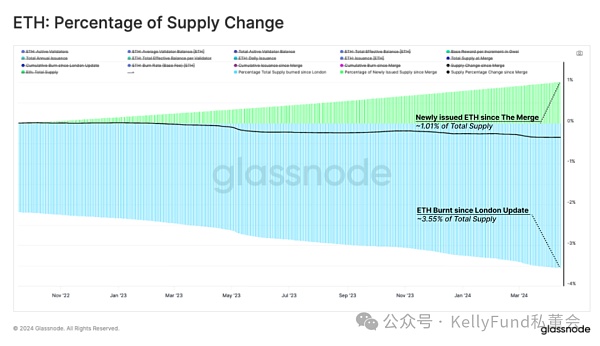

Currently, researchers from the Ethereum Foundation are concerned about the already high and growing staking rate. While staking more ETH will result in lower financial rewards for each validator, the total rewards they pay may still lead to inflation if the total amount of ETH staked becomes large. Currently, new Ethereum issued since the merger accounts for approximately 1.01% of the total supply, which is not a value that can be taken lightly – although it is still offset by the destruction of approximately 3.55% of the supply during the same period.

As more and more ETH enters the Staking Pool, inflation begins to affect the ever-dwindling number of ETH holders. In other words, wealth is being transferred from the shrinking pool of non-collateralized ETH holders to the growing pool of staked ETH holders.

Over time, this decline in the "real yield" component may make it less attractive to non-staking ETH holders and may simultaneously Weakening the function of ETH as a general equivalent in the Ethereum ecosystem. Affected by this, the role of performing the function of "general equivalents" may be migrated to assets like stETH under the liquidity staking agreement or the liquidity heavy pledge agreement, and originally these assets were only regarded as accepting Ethereum. Tools for staking pressure. This development will inevitably have some side effects. For example, we can foresee that projects that issue these derivative assets will have a huge impact on the governance and stability of the Ethereum execution layer and consensus layer.

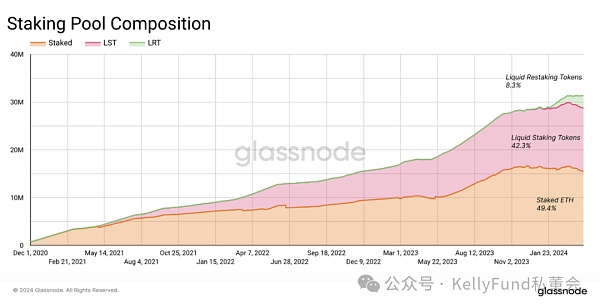

Today, we have noticed that half of the ETH staked is provided through these derivative projects. Among them, 42% of pledged ETH reflowed through liquidity-pledged derivatives, while another 8% of pledged Ethereum flowed back into the market through liquidity-heavy pledged derivatives.

The concerns of Ethereum researchers also apply to the general equivalent nature of Ethereum itself. Of the total supply of ETH, 11% are liquidity-pledged derivative assets, while 2.2% of the assets come from financial derivatives generated under the liquidity-heavy pledge agreement.

The proposal put forward by the Ethereum Foundation aims to control the annual issuance of Ethereum, thereby reducing the incentive for new pledgers to enter the Staking Pool. If this proposal is implemented, it is expected to slow down the growth rate of staking growth. However, these proposals have met with strong opposition from the community, with many believing that they should not make any changes at this time, and they have also questioned whether it is necessary to update the ETH policy again.

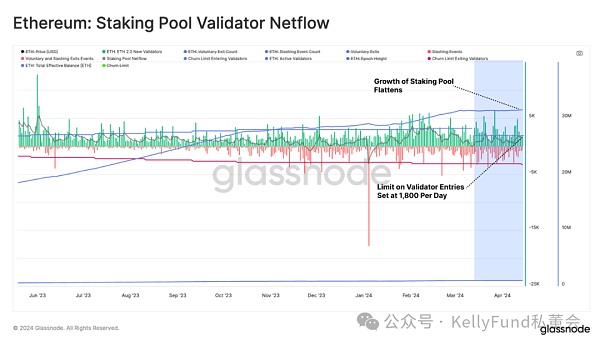

During the last Dencun upgrade, we found that with the upgrade, the growth of the Staking Pool has been slightly restricted - this hard fork introduced There is a limit of up to 8 new validators per epoch every 6.4 minutes, and it replaces the original churn limit function. It turns out that this effectively limits the number of validators and the amount of Ethereum pledged that can enter the Staking Pool, temporarily relieving some pressure on the Ethereum ecosystem.

Summary

Currently, the Ethereum ecosystem is discussing whether it is necessary to modify the proposal of the ETH issuance rate to explore this To what extent can policies slow down the expansion of Staking Pools? The ultimate goal of this proposal is to mitigate the impact of new innovations such as liquidity staking and re-staking on the Ethereum ecosystem. These innovations were originally designed to increase the profit opportunities for users.

As far as the current situation is concerned, the surge in staking (currently reaching 31.4 million ETH, accounting for approximately 26% of the total network supply) is driven by major players such as the Eigenlayer protocol. Promoted by the pledge agreement. These developments are increasingly leading to a surge in liquid staking assets, but in the long term this may start to diminish Ethereum’s role as a general equivalent in its vision. Currently, the Ethereum Foundation proposes to limit the annual issuance volume to slow down the growth of the Staking Pool, but these proposals have been strongly resisted by the Ethereum community.

This article compares Ethereum and Solana, exploring their strengths and weaknesses. We hope that readers will gain a clearer understanding of the uniqueness of each platform.

JinseFinanceThe merger was intended to turn ETH into ultra-sound money, but now it’s even more ultra-resilient

JinseFinanceVitalik released the EIP-7706 proposal, proposing a supplement to the existing Gas model, separating the gas calculation of calldata and customizing a base fee pricing mechanism similar to Blob gas to further reduce the operating cost of L2.

JinseFinanceThe Dencun hard fork has been completed on the Goerli, Sepolia and Holesky testnets, and the mainnet will be launched on Epoch 269568 (approximately March 13, 2024).

JinseFinanceThis means that users can now lock up their Ethereum through the new feature via Lido or Rocket Pool to earn financial r...

decrypt

decryptThe transition from PoW to PoS will have a great impact on Ethereum, including: the reduction of ETH issuance (meaning that ETH becomes deflationary), Gas prices will not drop, and energy consumption will be reduced by 99%.

Cointelegraph

CointelegraphA new Ethereum-based player in the decentralized finance (DeFi) space is making waves, projected to profit from the upcoming Merge ...

Bitcoinist

BitcoinistLower than expected inflation data sparks an instant rally in crypto, while the U.S. dollar pays the price.

Cointelegraph Nulltx

NulltxIn response to soaring inflation, Argentina has increasingly become a crypto-friendly country when it comes to cryptocurrency adoption.

Cointelegraph