Author: Lawyer Wu Wenqian, Mulana Investment Mangement

June 1 is an important date set by the Securities and Futures Commission of Hong Kong.

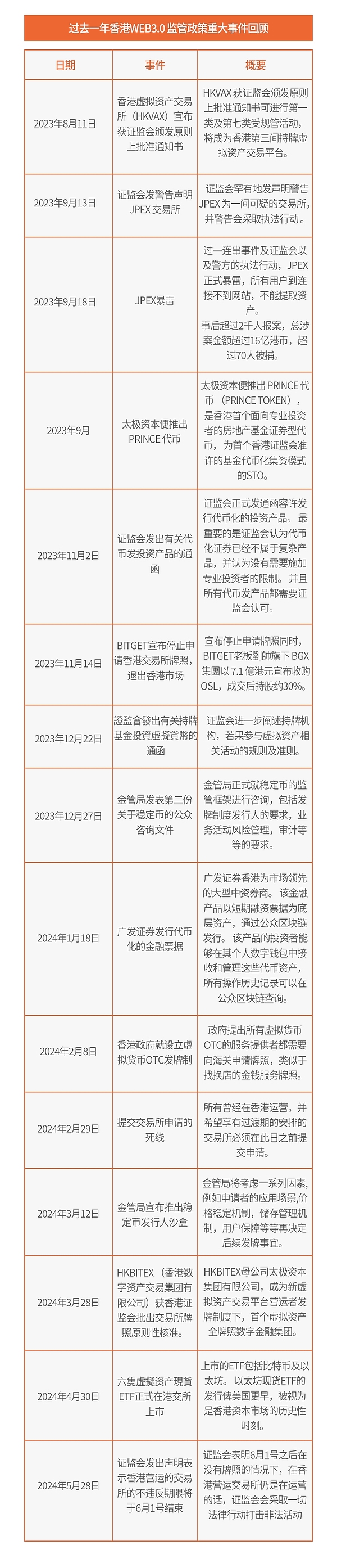

Exchanges operating in Hong Kong before June 1 last year can enjoy the benefits of the transition period arrangement, that is, they can trade without obtaining a license. It will operate until May 31 this year. After today, June 1, all exchanges must obtain a license or permit from the Securities Regulatory Commission before they can operate.

In the past year, more things have happened in the Hong Kong Web3 market than in every previous year, and the development has been much faster than in the past.

Look back at the policy and regulatory development of Web3 in Hong Kong from June 1 last year to May 31 this year.

Before June 1, 2023, various exchanges, or institutions interested in applying for exchange licenses, are busy building the simplest exchange , using the fastest method to attract users and increase user transaction volume. The purpose is to be eligible for transitional treatment and can continue to operate until May 31 this year, during which license applications will be submitted.

By the time the license application deadline closed on February 29 this year, there were a total of 24 applicants. There are many leading exchanges, including Binance, Huobi, OK, kucoin, Gate, Bybit, etc.

Basically all leading exchanges have withdrawn their applications. The most shocking thing is of course the news a few days ago that OK decided to withdraw its application. After all, it’s no secret that OK has invested significant resources in applying for a license.

As for the withdrawal of the application by the leading exchange, I think the following interpretation can be made:

1 . They all took the initiative to withdraw their applications, and it was not that the China Securities Regulatory Commission rejected the applications. There is a clear difference between the two. A voluntary withdrawal can be caused by the exchange, after weighing factors such as cost, future business development, number of competitors, etc., and finding that there is a big gap between cost and future development, so it gives up.

2. The Hong Kong market is small, and the exchange only allows customers from 18 countries (mainly European and American countries) to register remotely. Hong Kong already has two licensed exchanges, and two more have received in-principle approval, but the domestic market has not yet been opened. The competition among various exchanges can be said to be huge. With high operating costs, the market believes that the exchange will not be able to make money for at least a few years.

3. If you have paid attention to Coinbase's policy on Hong Kong, you will find that in February last year, Coinbase issued an announcement to suspend Hong Kong users. However, since the beginning of this year, it was discovered that Hong Kong users can register on Coinbase. This means that overseas exchanges may not operate in Hong Kong, do not promote in Hong Kong, and do not deliberately attract Hong Kong users, but they can still allow Hong Kong users to actively register on the platform.

4. Each of the leading exchanges has some non-compliance, such as opening contracts or derivatives products to Hong Kong users. The China Securities Regulatory Commission made it clear in 2018 that any contract product falls into the category of securities and requires a license before it can be issued. It may be more difficult for exchanges to explain past non-compliance, making it more difficult to obtain a license.

Based on the above reasons, I think it is a rational choice to actively withdraw the application. It is the right choice for the long-term development, sustainability, cost-effectiveness, etc. of the entire exchange.

By the way, looking back at the strategies of various exchanges, the acquisition of OSL by Bitget affiliates is a very smart move. It’s no wonder that Bitget is one of the fastest growing exchanges in recent years.

Although exchanges are very important, they are only a part of the entire cryptocurrency ecosystem. The Hong Kong government has recently made great efforts to promote tokenized securities and RWA. Most of RWA's underlying assets are traditional securities products. Hong Kong’s regulators and investors are relatively familiar with it.

It is worth noting that GF Securities and NV Technology jointly issued tokenized short-term financing notes at the beginning of the year. Both institutions have Chinese-funded backgrounds or are friendly with Chinese-funded institutions. As a pioneer, GF Securities has the opportunity to enable more Chinese financial institutions to boldly promote virtual currency-related products in the future.

RWA has a wide range of application scenarios. In the future, if it is combined with the Hong Kong dollar stable currency, the possibility of horizontal development will be greater. For example, if RWA products can be used as collateral to borrow Hong Kong dollar stablecoins, and the stablecoins can be connected to decentralized product pledges, then the traditional market and the currency market can be integrated.

Another point worthy of attention is the implementation of spot ETFs in Hong Kong.

Investors in spot ETFs can purchase them through traditional securities investment accounts, without the need to set up additional virtual asset wallets and trading accounts. Different from US ETFs, investors can also apply for and redeem physical virtual currencies, and it is open to retail investors. Hong Kong’s ETFs are certainly making history.

In addition, the market for investment in virtual asset funds seems to be active again recently. Also worth noting is the latest investment immigration program launched this year. Although the products recognized by the investment immigration program do not include virtual assets, limited partnership funds (LPF) or open-end fund companies (OFC) opened by asset management companies licensed by the China Securities Regulatory Commission can be used as part of the 30 million investment in the investment immigration program. 10 million, and these two funds do not limit the assets or products in which they can invest. This means that both LPF and OFC can invest in virtual currencies. Therefore, no matter what, if you choose to invest in virtual currencies, it is recommended that you cooperate with a company that has been approved by the China Securities Regulatory Commission to upgrade to invest in 100% virtual asset management.

In terms of licenses, in addition to exchange licenses, the Hong Kong government is also actively promoting stablecoin sandboxes and OTC licenses this year. It is understood that the Monetary Authority attaches special importance to the application scenarios of stablecoin licenses and believes that stablecoins should not only be used as trading pairs on exchanges. The application scenarios should be broader and more versatile than pure transactions.

The three licenses of exchanges, OTC, and stablecoins are supervised by three different government departments, but they are all coordinated by the Financial Services and the Treasury Bureau. This arrangement will help the government establish a stable and transparent regulatory environment, maintain policy continuity, and enable Web3 to develop sustainably.

In summary, compared with last year’s overwhelming publicity and massive activities, it is obvious that all industry stakeholders this year are bowing their heads and doing practical work to support the bull market. Make preparations for the development of Web3 in Hong Kong. Despite this, I think there are more actual developments and opportunities than last year.

List of applicants whose license applications have been returned, refused or withdrawn:

Joy

Joy