Hong Kong Considers Spot Crypto ETFs Amid Regulations

Hong Kong's SFC explores the potential of spot crypto ETFs while navigating shifting regulations and market dynamics in the wake of recent cryptocurrency challenges.

Hui Xin

Hui Xin

Author: Jinming Source: HashKey Capital Translation: Shan Ouba, Golden Finance

Institutional uptake of stablecoins and tokenized real-world assets (RWAs) has accelerated significantly: the market capitalization of stablecoins has now exceeded $250 billion, while RWA assets under management have increased from $15.7 billion year-to-date to $23.91 billion, driven primarily by tokenized private credit and Treasury products. The successful issuance, settlement, and custody of these digital instruments has bolstered confidence in the ability to transform traditional market rails to achieve similar efficiency gains in other asset classes—most notably equities, which have emerged as the next logical frontier for institutional tokenization. While still in its infancy compared to stablecoins and tokenized Treasuries, early players have made progress that promises to make tokenized equities long-term. Early pioneer Backed Finance began packaging blue chip stocks and ETFs into ERC-20 tokens and joined the Tokenized Asset Coalition in 2025, subsequently launching “xStocks,” a new series of over 55 stocks and ETFs that are scheduled to be listed on Kraken and integrated with Solana DeFi, marking a decisive step towards the mainstreaming of tokenized stocks. The Solana Foundation, AIX, Jupiter, and Intebix also signed a memorandum of understanding to develop a dual listing mechanism for companies seeking IPOs.

According to Statista, by 2024, the market value of listed stocks worldwide will reach $124.63 trillion, with annual trading volume exceeding $120 trillion. Despite the massive size of today's equity capital markets, stocks still operate on traditional financial infrastructure and are subject to exchange trading hours and T+2 settlement times, which can lead to inefficiencies. Leveraging blockchain technology, tokenized stocks can allow investors to unlock 24/7 trading, near real-time settlement, liquidity for unlisted public companies, improve operational efficiency, and gain opportunities through DeFi protocols.

24/7 trading. One of the key features of blockchain technology is that assets are managed by smart contracts with programmable rules, so there is no need for a centralized institution to facilitate trade execution. Through equity tokenization, this can reduce intermediary costs and allow trades to be executed 24/7 with near real-time atomic settlement.

Improve operational efficiency. The World Economic Forum pointed out that corporate actions are the most important unstructured data burden in the capital market, with more than 3.7 million event announcements generated in the United States each year, and corporate action errors causing more than 45% of brokers to lose more than $1 million each year. Programmability helps automate manual trading and post-trading functions, minimize corporate action errors and compliance costs, and thus improve operational efficiency.

Liquidity for private companies. For investors, selling shares in privately held companies is often a slow and arduous process, and comes with a lack of liquidity. For companies, equity tokenization can speed up the financing process by up to 30% while expanding the investor base, according to a report by DAMREV.

Composability. Using popular token standards enables tokenized equity to be used across different blockchain ecosystems, both private and public, and unlocks innovative DeFi use cases such as securities lending/financing that are typically not available to retail users, while also improving capital efficiency. The programmability of smart contracts for collateral management can be applied to equity, unlocking greater liquidity, just as crypto assets are widely used as collateral for on-chain financing.

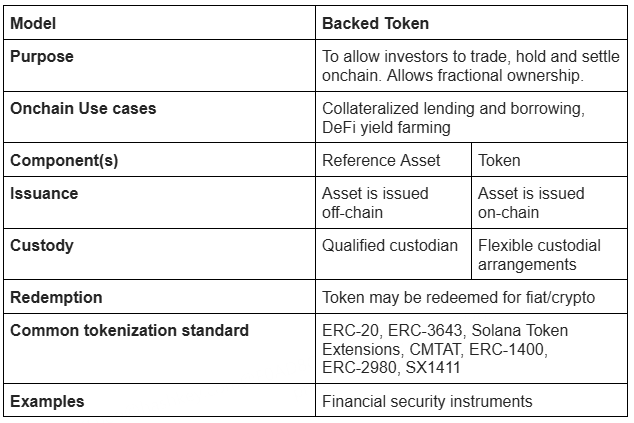

Tokenized equity requires a reference asset (which can be publicly issued or privately issued shares) to create a tokenized version. Reference assets are stored in a regulated custodian for security, while holders of tokenized shares can store them in their own wallets. A transfer agent is required to manage transaction records and corporate actions. Currently, most tokenized equity agreements do not allow for redemption of the underlying shares; instead, redemptions are made in fiat or crypto. The decision to issue tokenized shares depends on being able to fully leverage the programmability and efficiency of blockchain technology. Token programmability enables issuers to embed regulatory requirements and other policies related to the issued assets, thereby automating complex processes. A range of token standards, such as ERC-1400, ERC-3643, and Solana’s token extensions, have streamlined the on-chain issuance process by providing institutional-grade features tailored to issuer-specific needs. Post-tokenization, effective asset management is also critical, including tax management, ongoing regulatory review, regular asset valuations, and coordination of corporate actions. The table below summarizes the tokenization models used for backing assets such as shares.

Tokenization Model

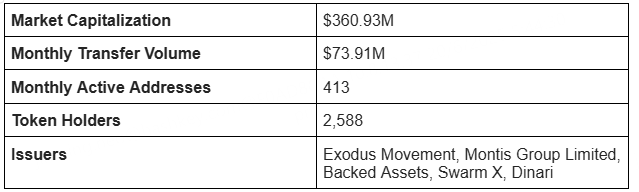

Currently, tokenized equity is still in its infancy, with a total market capitalization of $363.4 million, which pales in comparison to the size of traditional equity capital markets. The majority of tokenized equity is on the Algorand blockchain, with Exodus Movement’s Class A common stock tokenized on Algorand having a market cap of $284 million as of this writing. Despite Algorand’s dominance, other blockchains such as Plume, Base, Solana, and Ethereum are emerging as viable ecosystems for deploying tokenized equity. Emerging blockchains such as Ondo (Ondo Global Markets) and Converge, which position themselves as risk-weighted (RWA) blockchains, are also emerging to capture the growth opportunity of tokenized securities.

On the regulatory side, supportive regulatory policies have facilitated the initial adoption of tokenized equity.

Switzerland – Swiss Distributed Ledger Technology Act. Under the Act, companies can issue shares digitally on a blockchain, which has enabled numerous Swiss companies to tokenize their shares to gain liquidity while remaining compliant with regulations.

United States – Regulation S exemption under the U.S. Securities Act. Regulation S is a safe harbor under the U.S. Securities Act of 1933 that permits the issuance and sale of securities outside the United States exclusively to non-U.S. citizens without registration with the U.S. Securities and Exchange Commission, provided that no directed sales are made within the United States and no U.S. citizens participate during the distribution period.

Germany-Liechtenstein Blockchain Act. The Token and Trusted Technology Service Providers Act (TVTG) was enacted in October 2019 and will come into force in January 2020. The Act establishes a comprehensive legal framework for tokenized rights and assets (including equity, debt, etc.) by introducing a token container model, and any right can be embedded in a token. The Act authorizes the Liechtenstein Financial Market Authority to conduct supervision and issue participant licenses.

Key Performance Statistics of Tokenized Equity

Value of Assets on Each Blockchain

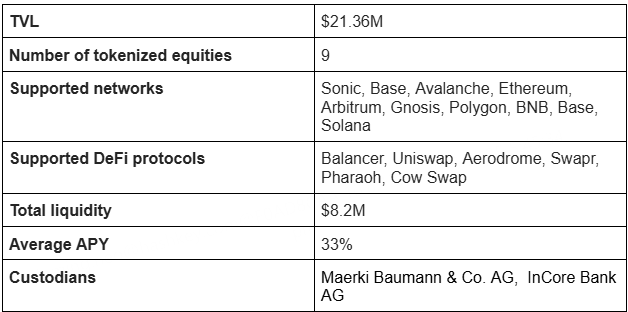

Backed Finance is a Swiss-based startup that issues Swiss-compliant “tracking certificate” tokens (bTokens/soon to be xStocks) that track the movements of listed stocks and ETFs. Each token is collateralized 1:1 with the underlying security and held in a separate, bankruptcy-proof escrow account. Backed Finance has implemented Chainlink’s Proof of Reserves, ensuring that users can verify the adequacy of asset reserves. Token minting and transfers are performed on a public blockchain in accordance with Switzerland’s Distributed Ledger Technology (DLT) Act, with plans to connect to Solana for exchange listings. bTokens do not provide ownership of the underlying asset, nor do they transfer any of its accompanying rights, including voting rights.

Tokenized stock holders can increase their yield by providing liquidity to DEX pools and receive swap fees and incentive income. Currently, Backed Finance's tokenized stocks have a total liquidity of $8.2 million, with an average annualized yield of 32.74%. The composability of tokenized stocks enables its assets to be used on various DeFi protocols and public chains.

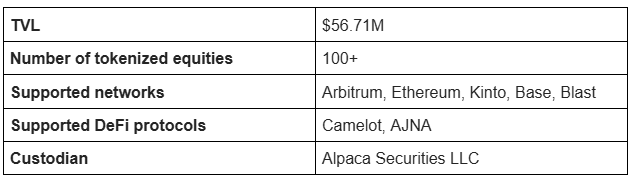

Dinari, Inc is a transfer agent registered with the U.S. Securities and Exchange Commission (SEC) that uses dShares to tokenize equity. Each dShare represents an off-chain stock, and each dShare issued has a 1:1 collateral guarantee. To issue dShare on the chain, companies must first undergo a KYB audit, and customers also need to undergo a KYC audit. When a user purchases dShare, the custodian will be responsible for custody of the underlying reference assets they purchase. dShare tokens are compatible with ERC-20 code and can be used on platforms such as Ethereum, Base, Blast, Arbitrum One, and Kinto. To meet regulatory requirements, the protocol regularly reports dShare's reserves and hires independent third-party auditors for verification. The issued tokens are also subject to transfer restrictions based on regulatory requirements in the location of the reference assets. However, current dShares do not have voting rights, although they can enjoy dividends from the underlying reference assets as well as fractional share ownership.

Swarm X

Swarm is a tokenization platform headquartered in Germany and regulated by the German Federal Financial Supervisory Authority (BaFin). SwarmX GmbH, the issuing SPV, is responsible for purchasing the target securities and custodial them with an institutional custodian. Once the token trustee verifies custody status, Polygon mints a security token pegged to the ISIN and trades through Swarm’s dOTC and AMM pools. The tokens are fully backed and redeemable for the underlying asset (USDC) once total requests reach $100,000, with monthly reserve disclosures.

Solana

Solana aims to build a high-speed, low-cost L1 network and increase its efforts to drive adoption of tokenized shares on its network. Sol Strategies, a public company building infrastructure for Solana, has signed a memorandum of understanding with Superstate to explore issuing its common shares on the Solana blockchain through Superstate’s “Opening Bell” tokenization platform. Additionally, the Solana Foundation has signed a memorandum of understanding with the Astana International Exchange (AIX), Intebix, and Jupiter to explore the development of a dual listing mechanism for companies listed on AIX. In addition, Solana’s token extension capabilities provide greater token flexibility and allow compliance strategies to be embedded in tokens. Issuers can also tokenize the processing of dividends, stock splits, and other corporate actions, eliminating tedious and time-consuming manual processing.

Ethereum

A pioneer in tokenized securities through the ERC-20 and newer ERC-3643 standards, which are built for licensed and compliant securities such as tokenized equity. ERC-3643 meets strict regulatory requirements by embedding investor rules and issuance rules, ensuring compliance at the smart contract level. Today, Ethereum is the largest risk asset network, accounting for 60% of the market share of tokenized risk assets.

Plume Network

Plume Network recently launched its mainnet (Plume Genesis) and has launched over $247 million worth of tokenized risk assets (RWA) (including private equity and treasuries). The platform has built a dedicated institutional-grade risk asset (RWA) tokenization framework and protocol (Arc & SkyLink) to support cross-chain issuance and compliance. The platform's ecosystem currently covers more than 200 projects, including well-known DeFi players such as Morpho, Curve and Matrixdock, and the total locked value (TVL) of its various tokenized assets has exceeded $247 million.

Trust Wallet

Trust Wallet is a non-custodial wallet with over 15 million monthly active users, and the company recently announced that it will begin supporting RWA assets by the end of Q3/Q4 this year.

Taurus

Taurus is an enterprise digital asset custody and tokenization platform that provides an end-to-end tokenization solution compliant with Swiss law for clients who want to tokenize any type of real-world asset. Taurus-Capital and Taurus-Protect are its institutional tokenization and custody solutions, allowing clients to issue and custody tokenized assets on the Solana blockchain.

Fireblocks

Fireblocks is a digital asset infrastructure provider that offers a comprehensive platform that meets the digital asset needs of enterprises. In terms of tokenization, Fireblocks also provides comprehensive services covering token minting, management, distribution and custody. Its tokenization policy engine allows customers to configure granular policies and user permissions to prevent unauthorized token operations. Customers can also deploy their tokenized assets on more than 80 different blockchains, supporting ERC, SPL, XRPL, etc.

In April 2021, non-custodial crypto wallet provider Exodus Movement, Inc. became the first U.S. company to tokenize its common stock, selling shares directly to retail investors through a Regulation A+ offering. The shares were issued on the Algorand blockchain in the form of security tokens, with Securitize acting as transfer agent and issuance platform. The unique feature of this offering is that the tokens are minted on a public blockchain and can only be purchased by investors using cryptocurrencies such as Bitcoin, Ethereum and stablecoins. However, the tokenized EXOD does not give investors voting, governance or economic rights, and cannot be traded independently of the Class A common stock. In addition to offering tokenized equity, the company's shares have been listed for trading on the New York Stock Exchange American Stock Exchange in 2024.

Although Exodus Sports shares do not confer any shareholder rights when traded separately, their tokenization paves the way for future companies to conduct similar activities, enabling them to take advantage of new financing methods and provide a smoother trading experience. With more regulatory clarity in the future and the continuous improvement of token standards, we can expect to see token holders gain more shareholder rights.

Despite the many benefits of tokenization, the acceptance of tokenized stocks by cryptocurrency users has been difficult to increase. This can be attributed to the high educational background of cryptocurrency native users and the prevalence of Web2 brokerages, which offer more competitive features and stock products than Web3 brokerages. In addition to fierce competition, issuing stocks on the blockchain also faces additional complexities.

Issuing assets on the blockchain incurs costs associated with network fees, which need to be paid to validators for processing transactions and maintaining blockchain security. In cases of severe network congestion, these costs can be quite high. In addition, smart contract vulnerabilities, MEV-related risks (such as front-running, sandwich attacks), oracle manipulation, or protocol layer vulnerabilities may affect the security and reliability of the issuance process, which may hinder the adoption of regulated institutions.

The limited trading hours of traditional stock markets may affect the ability of issuers to trade stocks after hours to maintain fully secured collateral value. In the event of a major event after hours, the issuer may be unable to rebalance the collateral, resulting in a temporary mismatch in asset backing or increased price volatility in the secondary market. For example, secured financing that accepts cash, stocks, private equity, and cryptocurrencies as collateral is more susceptible to the price and liquidity risks of these assets.

If tokenized equity does not bring the same benefits as traditional equity, such as voting rights, dividend rights, etc., this may also inhibit its adoption, especially for institutions and activist investors seeking enforceable legal claims.

Privacy is an important consideration for financial institutions when executing transactions. However, the lack of a common, industry-wide privacy encryption standard has led to slow adoption by institutional investors. Zero-knowledge proofs are still computationally intensive, and smart contract standards differ from current institutional technologies. The computational complexity of FHE requires modifications to the EVM to be implemented on-chain, which also affects scalability and gas fees.

As the number of institutional-grade blockchains increases, the problem of liquidity fragmentation is becoming increasingly prominent. Many of these tokenized equities face insufficient liquidity in DEX pools.

Regulators may also be concerned about investor protection issues if tokenized platforms are widely used by smaller private companies to raise funds. Typically, venture capital and private equity investments are limited to accredited and institutional investors. As access is opened up to a wider range of retail investors, retail capital is more susceptible to poor liquidity and higher risk of capital loss. The current state of tokenized stocks, especially in Switzerland - one of the countries with the most friendly digital asset policies for tokenized securities - still struggles to guide liquidity and retail demand.

As traditional market rails begin to directly connect to public chain infrastructure and regulators formalize rules for tokenized securities, the main frictions - settlement processes, compliance, and custody - are gradually being eliminated. With clear know-your-customer (KYC), anti-money laundering (AML) and investor protection regulations built into smart contract standards, banks and transfer agents are ready to adopt tokenized shares for collateral management and 24/7 trading, and retail venues will follow suit as liquidity increases. Notably, BX Digital, a subsidiary of the Boerse Stuttgart Group, received a distributed ledger technology (DLT) trading platform license from the Swiss Financial Market Supervisory Authority (FINMA) in mid-March, and the company is working with 5 partners to promote the settlement of tokenized assets such as stocks, bonds and funds between institutional market participants. Players such as Chainlink are also leading the adoption and liquidity of public chains through its Chainlink Runtime Environment (CRE), which facilitates a secure, synchronized and seamless trading experience between private permissioned chains and public unlicensed chains. In addition, Ethereum Layer2 and the newer Layer1 are emerging as potential venues for the deployment of tokenized securities due to their competitive advantages of high throughput and low cost. Broad adoption of token standards such as ERC-3643 among industry participants is also critical to driving composability and token interoperability.

In summary, while the tokenized equity market is still in its infancy, it is by no means a flash in the pan. Supported by institutional adoption, technical standardization, and regulatory clarity, tokenized equity is expected to gradually achieve sustainable expansion as traditional systems merge with decentralized systems.

Hong Kong's SFC explores the potential of spot crypto ETFs while navigating shifting regulations and market dynamics in the wake of recent cryptocurrency challenges.

Hui XinDespite the decline, Binance remains the top exchange in many sectors.

Alex

AlexDZ Bank in Germany launches blockchain-based digital assets platform, catering to institutional clients and paving the way for wider cryptocurrency accessibility.

Hui XinA 62-year-old Malaysian woman has fallen prey to a cryptocurrency investment scheme, resulting in a substantial financial loss. This incident highlights the dangers associated with fraudulent crypto ventures that proliferate on social media.

Jasper

JasperYuga Lab's feud with OpenSea is escalating- and the platform shows that its not a case of 'all bark and no bite'

Clement

ClementCardano and Polkadot are teaming up to transform the launch and operation of new blockchains, ushering in a new era in crypto space.

Aaron

AaronKraken is currently evaluating potential blockchain developers, including Polygon, Matter Labs, and the Nil Foundation, for their network-building project. This follows in the footsteps of Coinbase, a rival crypto exchange that initiated its own project called Base.

Jixu

JixuKraken, the prominent U.S. cryptocurrency exchange, is contemplating collaboration with leading blockchain technology firms to create its layer 2 network, according to undisclosed sources familiar with the situation.

AaronJulia Leung, the Chief Executive Officer of the Securities and Futures Commission, revealed that the city is considering allowing ordinary investors to use spot ETFs

ClementTruth Labs alleges CCP's Ethereum dominance, citing ETH holdings and crypto involvement, raising decentralisation concerns.

Hui Xin