Author: Liu Jiaolian

Overnight BTC (Bitcoin) fell to 55k, trying to make up for the automatic rebound after the July 5 spike (53.3k-56.7k). The author introduced a data analysis by Willy Woo. It indicates that there are a large number of so-called "paper BTC" in the contract market, that is, "fake" BTC synthesized with only US dollar stablecoins as collateral, which has brought huge resistance to the rise of BTC.

Because the theoretical supply of the US dollar is infinite, the supply of "paper BTC" is also infinite. A lot of purchasing power is wasted on buying "paper BTC", thereby suppressing the purchasing power that promotes the real rise of the market.

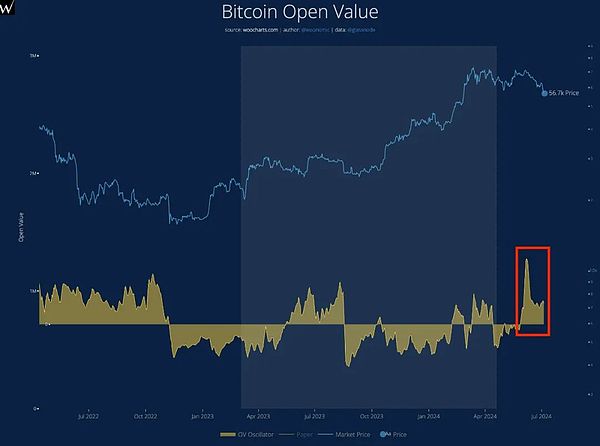

As can be seen from the above figure, the data in the red box shows that the main force of this wave from 72k to 53k is a large number of "paper BTC" opening short orders.

According to Willy Woo statistics:

- The German government has only sold 9332 spot BTC (real BTC)

- Since the recent 72k peak, up to 170,000 "paper BTC" have been synthesized and sold!

Therefore, Willy Woo recommends that for those who want to leverage BTC, it is best not to go long in the contract market, but to borrow u to buy spot BTC.

Two reasons:

“(1) Any OTC trader with USD collateral can buy futures, and you are also creating new synthetic BTC supply, which creates a bearish environment.

“(2) When buying spot using margin (borrowing USD), only BTC holders can sell it to you. This creates a supply shortage and a very bullish environment.”

And there’s an added benefit: “In a bull market, it’s much cheaper to fund a long position with borrowed USD or USDT than with futures or perps.”

In short:

[1] Buy spot, only real BTC holders can sell to you

[2] Buy contracts, any USD holder can sell to you!

The selling power of item [2] is unlimited because the supply of US dollars is unlimited.

Some netizens objected to Willy Woo's statement. The netizen said: "If there is a net long exposure in futures, whether it is perps or CME, market makers will invest more funds to buy spot and short futures to obtain higher funds/spreads - converting long exposure to the underlying asset." "The decline in BTC prices is not due to "synthetic Bitcoin", but because OG holders and miners sold more BTC than they bought." Willy Woo retorted: "In fact, this is a naive view of the entire system. What you describe is only part of the system, and a less important part. (1) If there is a net long demand, liquidity providers will participate in basis trades to transfer spot liquidity to futures. Our company has $50 million to $150 million in basis trades at any time through a group of managers, and we also track nearly 600 quantitative companies. Our data shows that basis trades account for about 10% of bets. 25%.

“Note that basis trades are also net bearish because the carry spread is a tax on the money bought, and spot buying moves almost all of that money into the market.

“(2) The main problem now is… directional traders can sell BTC without owning it. They can sell it with USD collateral.”

“There is a lot of data showing that this effect is real.

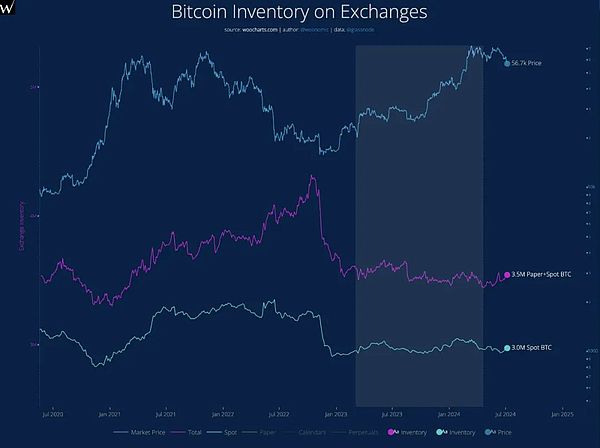

“The chart below makes this clear. Whenever order volume grows and “tradable BTC” floods exchanges, prices fall.

“The 2021 bull market is the first one that has not run away with the index (surge), and has not reached normal highs at all. This is related to the significant rise in “paper BTC”, as sellers can sell futures paper money simply by collateralizing it with USD... In 2017 and before, only BTC Holders can sell, but sellers are limited, so there is an exponential runaway (surge). "

The above netizen continued to refute his rebuttal:

"1. MMs (market makers) like Susquehanna are the largest holders of BTC ETFs, and they are using BTC ETFs for basis trading, so BTC ETFs are not the least important part. They are the main driver of inflows/outflows of BTC equivalent funds, and BTC market participants will judge market sentiment by tracking them religiously.

“2. Yes, futures buyers need to pay capital, but this also provides them with leverage that spot cannot get. If you expect BTC price to double in the next 12 months, then the financing cost of 11% APY is very low, because it allows buyers to control 10 times more buying power than spot. In total, their return on capital is 8.3 times higher than spot.

Basic calculation:

$100 spot -> $200 in 1 year, or $100 profit.

$100 10x leverage, $1000 -> $2000 - (1500) * 11% = $1835. For simplicity, we assume that the cost basis for the year is linear, so $1500 is halfway between $1k and $2k.

After 1 year, profit of $835 using futures 3. This gets back to my next point, which is that most BTC investors new to the BTC market are not BTC natives. They have USD bills to pay and want to see USD profits. OG holders also seem to like USD profits, as they have been selling, which I’m sure you’ve seen on-chain. BTC is being sold off not because of some evil contrarians or synthetic BTC, but because market participants have shown through their actions that they want to see returns to pay their bills in USD — not hold something they can’t yet trade and hope it goes up one day. 4. Yes, futures allow speculators to short the underlying asset with USD as margin. But this is no different than any other established commodity/index. If BTC is truly like a maxis like you, then you can’t expect it to go up. As valuable and scarce as claimed, a) it should be able to withstand these normal market pressures, as any other commodity/index would be affected by these pressures; b) you should celebrate such shorting because it will only create higher buying pressure if they are squeezed by overwhelming demand.

"5. The core of the problem is that you want more people to join the BTC belief because you are an early adopter. After the ETF, I think it is late in the game and the exponential returns we have seen in the past are over, unless the Fed prints money like crazy, and Powell has not indicated that he is going to print money so far.

Over time, given the inflationary nature of fiat currencies, the price of BTC is likely to rise, but if it is really digital gold as people like to compare it, we should also expect its stable volatility and returns comparable to gold, which is not as interesting for most crypto speculators without leverage in the form of futures and options."

Seeing this, I believe that readers have understood their respective views and positions.

However, when positions appear, it also means that the discussion is about to start to change. From discussing the matter at hand, they began to attack personally - not attacking the other party's appearance (Internet confrontation is not face-to-face), but attacking the other party's position and motivation.

In fact, it is not difficult to find that there is a consensus between the two sides, that is, since the bull market in 2021, a considerable part of the incremental funds and new leeks have been diverted to the contract and futures markets, resulting in insufficient purchasing power in the spot market.

Willy Woo studied the data and found that the short selling of "paper BTC" hindered the market's surge. According to the rules of the contract market, for every short order, there will be a long order. The reason why the shorts can open shorts is precisely because the longs go to open longs.

In the past, when there was only spot to play, new speculative traders who entered the market could only buy BTC spot first if they wanted to make a profit. But now with futures contracts, they can open shorts directly without having to buy BTC spot first.

This is exactly what the netizens on the line said. Since the ETF, most of the new players entering the market are not long-term investors who hoard BTC for a long time, but speculative traders who are based on the US dollar and hope to make US dollars every day.

Although their diversion of the spot BTC market suppressed the extent of BTC's significant deviation from the median regression line during the bull market and smoothed out the surge, their speculative trading also brought more abundant liquidity to this market.

In short, the market is more mature. The more mature it is, the more it will surge and plummet with a relatively smaller amplitude. This makes people who expect to reap a wave of profits during the surge not very happy, but for long-term holders, it is just the opposite. The surge will only greatly increase the cost of adding positions, which is not as good as a steady rise and steady happiness.

XingChi

XingChi