Author: Rishabh Gupta Compiler: Block unicorn

Introduction

In December 2024, three German marketing professors did something that should scare every business that accepts cryptocurrency payments. They decoded 22.7 million retail stablecoin transfers and reconstructed complete customer intelligence for eight direct-to-consumer (D2C) brands—including wallet share, order frequency, average order amount, and peak sales hours.

No hacking skills are required. No internal permissions are required. All it takes is public blockchain data and a few lines of Python scripting.

This is the stablecoin privacy paradox in 2025.

Stablecoins are taking off. The numbers are astounding: stablecoin usage on Base is no longer a niche experiment. Token Terminal’s analysis shows that total L2 transaction volume reached approximately $3.81 trillion in the first quarter of 2025 alone—an all-time high, outpacing the early growth curve of major credit card networks.

Stablecoin transaction volume on major chains

Even after deducting internal hops, the number is still in the trillions. 65% of Ethereum’s total locked value—about $130 billion—is now concentrated in stablecoins. Tether holds nearly $120 billion in U.S. Treasuries and has a quarterly profit of $10 billion. Businesses that use Stripe’s stablecoins sell in twice as many countries as those that don’t.

By all important metrics, stablecoins have achieved product-market fit, and their scale is large enough for traditional fintech companies to take a hard look.

So why am I writing about privacy for an industry that’s already making tons of money?

Because the success of stablecoins has made them the most dangerous payment method in the world. Not dangerous for users, but dangerous for businesses.

Every transaction you make is a data point for your competitors to analyze. Every salary you pay becomes workplace intelligence. Every invoice you settle exposes your supply chain. Every customer payment exposes your business model. In the rush to adopt stablecoins, we’ve built a global financial surveillance system where your business intelligence is just a search away on Etherscan.

The irony is that we’ve created the most efficient cross-border payment system in history, but it broadcasts your financial strategies to anyone interested in viewing it.

This isn’t about ideology or cypherpunk dreams. Here’s the cold reality: Your competitors probably know your customer acquisition costs better than your CMO does.

With stablecoin payments expected to reach $2 trillion by 2028, this problem will only get worse.

We’re on our way to $5 trillion. Why is this scary?

Stablecoins are breaking every growth record in crypto. 65% of Ethereum’s total locked value — about $130 billion — is now in stablecoins, institutional money is pouring in at an unprecedented rate, and we’re witnessing a complete transformation of global payments.

The promise is real: Instant cross-border transactions, minimal fees, 24/7 operations. No wonder businesses using stablecoins are selling to twice as many countries as they do now.

But what few people talk about: All of these benefits come with a hidden cost—complete financial transparency.

Some current privacy nightmares

The Salary Comparison Trap

Alice, a founder who just raised $500,000, $200,000 of which was in crypto. She hired three developers from India, Vietnam, and Argentina, with salaries set to local market levels. Everyone preferred crypto payments—faster, cheaper, and without the hassle of banking procedures.

Then reality hits. Each developer discovers everyone else’s salary on-chain. Those with lower salaries start hinting for raises. Alice wants to help, but has a limited budget. While every salary is competitive locally, transparency is causing resentment. The “Envy Tax” study proves this is not an isolated case — it’s a quantifiable phenomenon. Companies either overpay high performers or accept the reality of undermining team morale.

This is not theory. This is happening in many crypto-native (and now internet capital markets, non-crypto-native) startups.

Privacy Nightmare

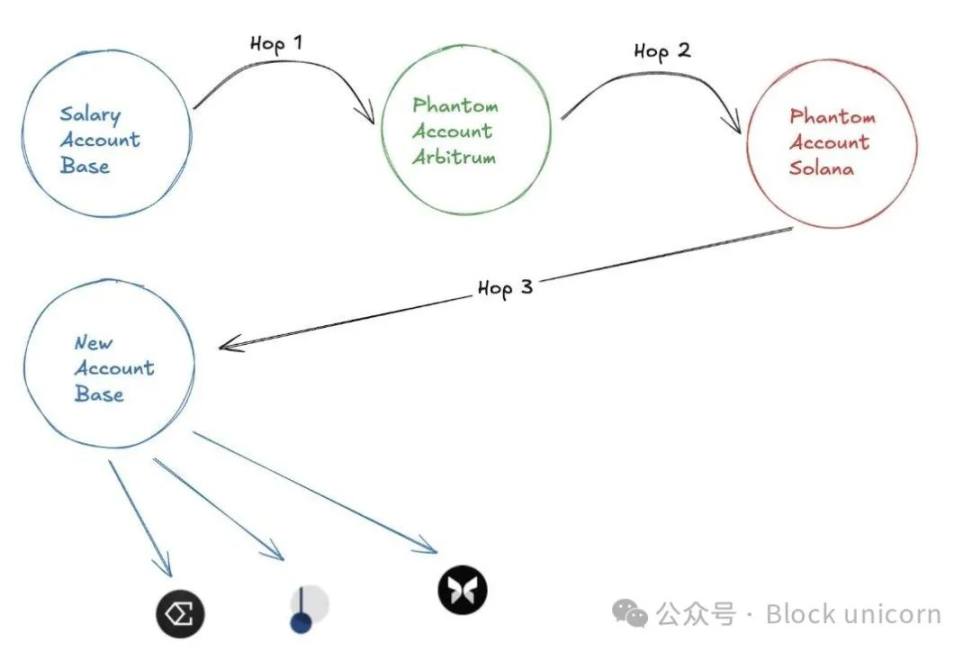

Bob is a blockchain developer working at a well-known L2 protocol with a monthly salary of $12,000. He deposits his salary into a hardware wallet — safe and professional. But now he needs to buy groceries, pay rent, and make a living.

If he spends directly from his payroll account, his landlord, ex, and competitors will know exactly how much he earns and what he has. So, Bob does what thousands of people do: he "mixes" his funds through centralized exchanges, or blurs his financial tracks through 3-4 bridge transactions and multiple conversions.

Ironically, we built decentralized finance (DeFi) to get rid of intermediaries, but privacy issues force users back to centralized services - now with added fees, tax complexity, and compliance risks.

Competitive Intelligence Disaster

Charlie runs a successful online pharmacy in Argentina that accepts USDC payments. His competitor, Don, notices Charlie’s growth and decides to investigate. Through a few hours of on-chain analysis, Don discovers that 80% of Charlie’s transactions are concentrated in a specific time period. Further digging reveals Charlie’s entire customer acquisition strategy — target demographics, regions, effective marketing channels.

Don gets Charlie’s hard-earned business intelligence for free. No corporate espionage required. Just Etherscan.

Institutional Time Bomb

These are just the issues at the retail level. The impact at the institutional level is life-or-death.

When every money flow is visible, when every strategic deal is public, when your competitors can track your cash flow in real time – how do you compete? How do you negotiate? How do you maintain strategic advantage?

Corporate Fiscal Reality: Imagine a Fortune 500 multinational considering rebalancing $2 billion of funds between Asian subsidiaries. Traditional channels: 3-day settlement, $50k in fees, zero transparency. Transparent stablecoins: Instant settlement, $100 in fees, but strategy fully exposed.

Some fiscal rebalancing reveals regional performance. Every supplier payment exposes supply chain relationships and pricing. Every internal transfer between jurisdictions shows which markets are being prioritized and underperforming. Payment timing patterns can reveal company plans or market entry strategies months in advance.

With stablecoins, the efficiency gains are huge. The privacy costs are deadly.

Institutions claim privacy is their primary concern, but they build on transparent chains. This disconnect between stated needs and actual infrastructure is a disaster.

But here’s the thing: they have no choice. Most of the activity happens on public chains. Liquidity dominates there. 90% of DeFi protocols run there. Stablecoins are settled there. Composability with existing infrastructure is non-negotiable for many participants. For example, Paypal was the first to launch its stablecoin on Solana.

One central crypto bank I spoke with mentioned that their current “solution” is to split order execution into departments, with one team managing position information and another handling execution - this is done to ensure that no one has the full picture.

Even Bitcoin's biggest corporate advocate, Michael Saylor, understands the danger. He strongly warned against making wallet addresses public, saying "no institutional-grade or enterprise security analyst would think it's a good idea to make all traceable wallet addresses public."

However, despite Saylor's cautious approach, blockchain analysis platform Arkham Intelligence gradually tracked MicroStrategy's Bitcoin holdings. In February 2024, they announced that they had identified 98% of MicroStrategy’s Bitcoin holdings, and by May 2025, they had found an additional 70,816 BTC, tracing a total of 525,047 BTC (about $54.5 billion) — 87.5% of the company’s total holdings.

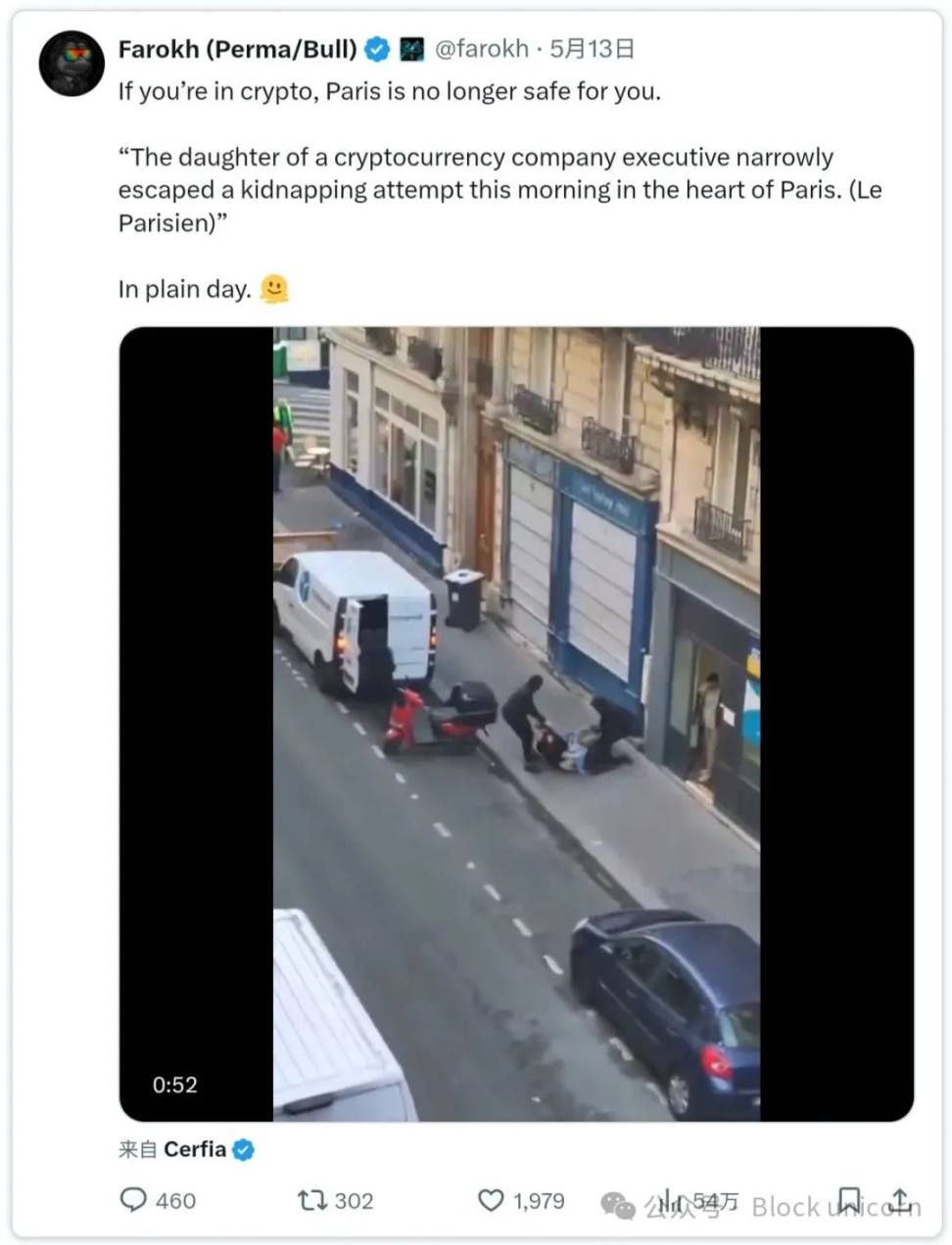

The dangers are not limited to finances. In France, four masked men recently attempted to kidnap the daughter and grandson of Paymium CEO Pierre Noiza in broad daylight in central Paris. The family was targeted precisely because the transparency of the blockchain exposed their wealth to criminals.

This is not an isolated incident. Jameson Lopp maintains a comprehensive database of hundreds of physical attacks on crypto holders. The pattern is clear: blockchain transparency leads to real-world violence.

Every year brings new cases:

Home invasions where victims are tortured to hand over private keys

Kidnappings demanding cryptocurrency ransom

Targeted robberies at conferences and parties

Attacking family members to force compliance

When your wallet address is public, you expose more than just your financial strategy. You and your family have a target painted on your back. The “$5 wrench attack” is no longer a theoretical problem — it’s become a growing pattern with hundreds of verified cases.

Disasters at Scale

What’s really scary: These problems multiply as adoption scales.

$100 billion: annoying but manageable

$1 trillion: severe competitive disadvantage

$5 trillion: total collapse of trade secrets

We are building a global financial system where everyone can see each other’s cards. This is not a feature — it’s a catastrophic vulnerability.

With stablecoin payments expected to reach $2 trillion by 2028, we’re not talking about a future problem. We’re already experiencing it. Every day we delay, more business intelligence leaks, more salary data becomes public, and more competitive advantage evaporates.

The question isn’t whether stablecoins need privacy, but whether we’ll implement privacy protections before a transparency tax becomes too expensive.

Why All “Solutions” Have Failed (So Far)

The crypto industry has been trying to solve the privacy problem for years. Billions in venture capital, thousands of hours of developer time.

Yet, in 2025, Bob still needs to perform four bridge operations to pay his rent privately.

Let’s be honest about why all solutions (except mixers) have failed to scale.

Privacy Chains

“We will build privacy from the ground up!” a dozen L1 and L2 chains have promised.

Reality Check:

Bridge Delays: Wait 20 minutes to transfer funds in, another 20 minutes to transfer out

New Wallet Setup: Download special software, create new keys, learn a new interface

Chain Sync Issues: “Why does my balance show zero? Oh, it’s still syncing…”

Liquidity Desert: Want to exchange? Good luck dealing with 15% slippage

Ghost Town Problem: Private Transactions Only Work with Network Effects

Why It Failed: Asking users to leave their current chain for privacy is like asking them to move to a different country for better privacy laws. This friction kills adoption before it even gets started.

Additional Privacy Tools

Some protocols have tried a different approach: offering privacy on top of an existing chain. But there are also disadvantages:

User experience:

You need to download new software (hopefully not malware)

You need to generate zero-knowledge proofs (ZK proofs)

You need to pay 10 times the gas fee for private transactions

You need to trust other users to comply (they often don’t)

Pray that there are no vulnerabilities in the smart contract (there may be)

Centralized Exchange (CEX) Mixing

The reality is: people use Binance or other CEX as a privacy tool. Deposit from one address and withdraw to another address. Centralized mixing requires extra steps.

Problem:

KYC defeats the purpose

Exchanges may freeze your funds

Tax nightmare for many users

Unavailable in many jurisdictions

User experience degrades dramatically

Why it “works”: Because it’s readily available. This says something about the state of privacy tools.

Are there regulatory concerns about bringing privacy features to stablecoins?

Remember that regulators are not against confidentiality per se – they are against privacy facilitating bad actors and preventing law enforcement from taking action.

Here are the measures we believe are necessary:

View key access: There should be an access control list in place that allows certain view keys to be checked if there is a problem.

Transparency on demand: Amounts and counterparties are encrypted by default, but a court order can unlock the full transaction trail - no forks, no re-issuance of tokens.

Real-time AML/CTF screening - Every time liquidity is brought into a privacy protocol, it should be checked to ensure that its source is legitimate, or that the address has interacted with or is a high-risk address. This goes beyond sanctions and covers terrorist financing, human trafficking, and other major vulnerabilities.

Anti-mixing guardrails: Funds should not be completely untraceable.

Emergency Freeze Switch: Multi-Signature allows tokens to be locked instantly, but due process must be followed.

Provide regulators with the same subpoena-level access they have today, without giving the world a permanent view of everyone’s salaries, invoices, and trading strategies.

What’s Next?

Stablecoins are one of the most efficient payment systems in history, but unfortunately, they are surveillance networks where every commercial transaction is public data. With nearly $5 trillion in stablecoin volume, every dollar is broadcasting your strategy to your competitors. This is not a long-term sustainable plan. Clearly, the solution is not to abandon stablecoins — it’s to add privacy protections that are compatible with existing infrastructure and meet regulatory requirements.

Weiliang

Weiliang