USDe economic model and potential risk analysis

Ethena, USDe economic model and potential risk analysis Golden Finance, fully collateralized semi-centralized stablecoin

JinseFinance

JinseFinance

Author: Liu Ye Jinghong

Ethena is a star product in this period. Both ENA, which was directly launched on Binance, and its stablecoin USDe have received huge attention. Even though the market sentiment is relatively low now, Ethena's TVL is still $2.4 billion.

Many people see the product model of issuing stablecoins by pledging tokens and giving high returns. The first thing they think of is Terra's UST algorithmic stablecoin, which also absorbed a TVL of nearly $10 billion from 2021 to 2022 with a 20% yield, and then collapsed with Terra Luna.

It is estimated that many readers will have this doubt, worrying or suspecting that Ethena is another imitation of UST and will also explode. But I want to give a conclusion here: Ethena's USDe will not explode, but Ethena will have marginal effects as the market size increases, and it is very likely that the USDe income will be infinitely close to zero. USDe issuance logic Although USDe, like UST, uses mainstream cryptocurrencies as collateral and is issued at a par value of $1, the actual fund operation logic of the two is completely different. UST is very simple in fund operation. The amount of UST issued is the same as the value of the cryptocurrency pledged by the user. But the core is that UST is deeply bound to Luna. The higher the market demand for UST, the more deflationary effect it will have on Luna, pushing up the price. And the higher the price of Luna, the more UST can be minted.

Therefore, the essence of UST's fund operation is to use the virtual market value to push up the market. With the issuance of Luna, a nearly unlimited number of UST appeared on the market, and finally this 10 billion fund collapsed.

On the other hand, USDe is much more complicated in fund operation.

First of all, although USDe's collateral is mainstream cryptocurrency, it currently does not accept ordinary users to deposit ETH or BTC directly. It only allows the purchase of USDe by depositing a series of stablecoin assets (USDT, USDC, DAI, etc.), so that there is no liquidation risk for ordinary users.

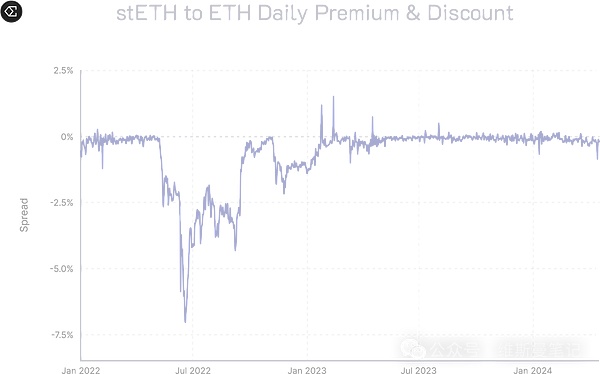

For whitelist users (usually institutions, exchanges, and whales), they can deposit LST assets, that is, stETH to mint USDe, so whitelist users need to bear the liquidation risk. However, since Ethena will hedge, they actually only need to bear the ETH/stETH spread risk, and Ethena predicts that this spread risk will be triggered only when it reaches 65%. The largest price difference in the history of ETH/stETH is nearly 8% during the Terra explosion in 2022.

Therefore, under the normal operation of the product, this liquidation risk is almost impossible to occur, so we can change the context: Ethena will only be liquidated when Lido's stETH has systemic risks.

In addition, since Ethena's leverage ratio is close to spot, even if liquidation does occur, it does not mean that Ethena will directly explode and lose all collateral, but will gradually liquidate according to the relevant positions. And it should be noted that Ethena is not a decentralized execution product. It is a centralized product with a centralized asset management team operating 7*24 hours and has cooperation agreements with major exchanges. Therefore, Ethena stated in the official document that when there is a real liquidation risk, the asset management team will manually intervene to reduce the risk.

Secondly, after completing the deposit collection, Ethena did not lie on the books, but adopted a more anti-Web3 intuitive centralized asset management.

Whether it is the stablecoin from ordinary users or the LST assets of whitelist users, they will be split according to the par value of 1 US dollar, and the two operations of "holding spot in the form of stETH" and "opening ETH short orders in cooperative exchanges" will be carried out respectively. Therefore, the official value equation is obtained:

1 USDe = 1 USD ETH + 1 USD ETH short perpetual contract

Therefore, when Ethereum rises, the floating profit brought by the rise of spot ETH will offset the floating loss of ETH short orders; when Ethereum falls, the floating profit of ETH short orders will offset the floating loss brought by spot ETH. Finally, USDe is stabilized at the par value of 1 US dollar.

In addition, Ethena completely relies on centralized exchanges for risk hedging, and currently has more than ten cooperating exchanges, including Binance, OKX, Bybit, Bitget, etc. Therefore, Ethena avoids Web3 hacker attacks in terms of fund security, and obtains liquidity far exceeding that of decentralized exchanges, as well as lower operating fees.

USDe's income sources are only two:

Rewards obtained from pledged assets;

Funding rate and basis earned from risk hedging;

The rewards obtained from pledged assets are very easy to understand, that is, the consensus rewards obtained by staking ETH. Currently, Ethena guarantees income by holding stETH, and the current annualized interest rate is about 3%.

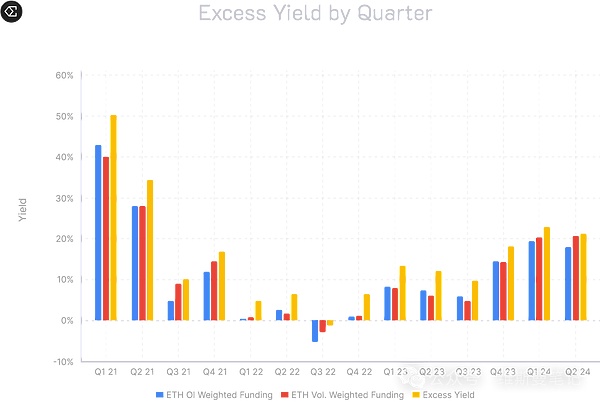

The most worth mentioning is the second income earned from risk hedging. Basis is actually the well-known term arbitrage, and the funding rate is the rate paid by the long and short parties to each other in the contract transaction based on the market advantage.

According to Ethena's calculations, the yield of term arbitrage is 18% in 2021, -0.6% in 2022, 7% in 2023, and 18% so far in 2024. Although the market conditions are very different every year, the long-term average yield is above 10%.

As for the funding rate, the yield depends on the bull and bear market. When Bitcoin was trading sideways at more than $70,000 last month, Binance's funding rate was as high as 0.1%, which directly pushed the yield of sUSDe to 30%.

But there is a very important point here. The core of Ethena's hedging method is to short ETH, which means that once the market weakens, Ethena will need to pay the shorting fee. Therefore, Ethena will see a situation where the yield of sUSDe is infinitely close to zero for a period of time in a bear market.

However, Ethena also found based on data backtesting that historically, ETH and BTC perpetual futures had negative returns on 19.1% and 16.1% of the days, respectively. The average return of ETH during the entire period was 8.79%, while the average return of BTC was 7.63%.

The most extreme case is still in 2022, when Ethereum PoW hard fork arbitrage caused the market to have a negative quarterly average return.

Therefore, from a year-by-year perspective, the strategy implemented by Ethena is indeed profitable in the long run. However, it is a bit anti-human for the cryptocurrency circle, because cryptocurrency players often use stablecoins to manage their finances in the bear market, and take out stablecoins to charge in the bull market. The yield volatility curve of Ethena is just the opposite. Its yield is very high in the bull market and very low in the bear market.

Although Ethena seems to be perfect in theory and all kinds of risk control are taken into account, there are still some potential black swan risks, and I think they are not too far away.

Currently, Ethena's risk hedging strategy relies entirely on centralized exchanges to execute, but the exchange itself is a risk point. For example, daily downtime and unplugging of network cables are likely to widen the price gap, but these can be solved by compensation or rollback. What really cannot be solved is policy and systemic risks.

The United States has become increasingly strict in regulating cryptocurrency exchanges. First, Binance's CZ was pledged for mining, and then various exchanges were sued by the SEC. What's more, will there be the next FTX to go bankrupt, causing Ethena to have huge bad debts? These are all black swan risk points.

As the leader of the Ethereum LST track, Lido has not had any major security incidents so far. But once it happens, not only Ethena's collateral, but even the Ethereum ecosystem will be hit hard. Don't forget that two years ago, before Ethereum switched to PoS upgrade, stETH had a large amount of depegging.

There is a joke in the currency circle that if you short contracts, you are shorting your own business. That's right, Ethena does this.

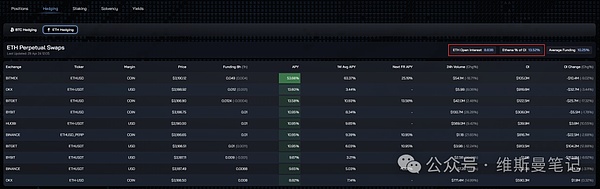

This is the data dashboard from Ethena. The entire market has ETH open contracts of 8.6 billion US dollars, and Ethena's position accounts for 13.52%, or 1.162 billion US dollars. It is also worth noting that the 86% of the market's US$10.6 billion contracts include positions on both the long and short sides. Even if the long and short sides are divided equally, the short-selling funds should be 4.3 billion US dollars. Ethena only shorts in the contract market, which means that Ethena occupies 27% of the entire ETH air force funds.

This is only a few months after Ethena went online and the market was sluggish. Once the market returns to the upward cycle and Ethena's earnings begin to rise, more funds will inevitably be deposited in Ethena, and this air force position will be even larger.

And because Ethena has more and more short positions, the funding rate that needs to be paid will be higher when the market goes down, and at this time there will be a marginal effect that causes the return to be infinitely close to zero.

Let me write a small summary. Ethena is indeed a well-designed product, but it is not DeFi, nor is it a Ponzi like UST. If I were to describe it accurately, Ethena is a fund product based on cryptocurrency.

It incorporates the risk hedging gameplay of traditional finance into cryptocurrency and captures returns from more drastic fluctuations. At the same time, because of the permissionless nature of blockchain, anyone can buy such a fund product without KYC or AML.

Ethena, USDe economic model and potential risk analysis Golden Finance, fully collateralized semi-centralized stablecoin

JinseFinanceEthena Labs' USDe stablecoin faces scrutiny amid comparisons to Terra's troubled history, prompting reflection on risk management strategies.

Weiliang

WeiliangIf we believe that [decentralization] requires satisfying both [permission-free issuance] and [de-custody] conditions, then USDe does not meet the requirements, so it is appropriate to classify it as a [fully collateralized semi-centralized stablecoin].

JinseFinanceBybit has forged a strategic alliance with Ethena Labs, bringing forth Ethena's USDe stablecoin to the Bybit platform. USDe, a decentralised monetary solution, operates independently from traditional banking systems. It leverages delta-hedging staked Ether (ETH) for comprehensive collateral backing.

JoyJinseFinance

JoyJinseFinanceLove it or hate it, a crypto crackdown seems imminent, especially with the U.S. government urging Congress to accelerate its progress on crypto regulations.

Catherine

CatherineHopefully Ethereum becomes a system more like Bitcoin.

链向资讯

链向资讯Hope Ethereum becomes a more Bitcoin-like system

Ftftx

FtftxTo understand the content and imagination of Taproot's upgrade, we must first understand some bitcoins.

Cointelegraph

CointelegraphThe root cause of RBI’s concern appears to be that digital assets could undermine India’s rise as a global power.

Cointelegraph