Is RWA a product or a transaction?

What exactly is RWA (real world asset tokenization)? Is RWA a product or a transaction?

JinseFinance

JinseFinance

Author: Ye Kai; Source: Ye Kaiwen

RWA originated not from Web3.0, but from Web2.5. At present, it can only be regarded as a transitional form of Web2.1/2.2. Therefore, the early development of RWA is more like the tokenization of real-world financial assets (debt, equity, financial products, etc.), rather than the tokenization of real-world physical objects. Assets are somewhat different from physical objects. If we want to look at it from the perspective of real-world financial assets, we must consider the industry. There is a classic ADF framework for industrial analysis: Assets-Dealers-Finance. RWA, which focuses on industrial upgrading, will be integrated with real-world industrial assets and industrial transactions (on-chain certificates and Oracle mechanisms, etc.), and then tokenize financial products based on assets and transactions.

For example, for RWA of green energy and RWA of crude oil, their financial products cannot avoid the commodity trading of energy or crude oil, and their tokenization cannot avoid the realization of related exchange functions.

Due to the existence of industry, the transaction scale of this asset can be expanded. If an ordinary real-world asset is placed in the context of an industry, its transaction scale and transaction method will also be very diversified, thus giving rise to diversified industrial transaction finance (Trade Finance).

Depending on the different categories of real-world assets, industrial transactions may have different trading markets and methods such as on-site trading, electronic trading, over-the-counter trading, and bulk trading. The electronic trading of an agricultural product such as ginger or garlic may have a transaction scale of more than 20 billion, in which there will be abundant trading finance phenomena such as futures-spot arbitrage, dealers, virtual positions, and price manipulation.

Take the garlic industry as an example. When Ye Kai was working on the Rural Revitalization Fund, he investigated the very common agricultural product Shandong Electronic Trading Market for garlic. Garlic farmers plant garlic, and local pickers and dealers purchase garlic from scattered farmers and bring it to the wholesale market. After the wholesalers purchase it, it enters the "market" for concentration; some of the middlemen in the market are similar to the "brokers" in the stock market, providing garlic speculation intermediary services to help speculators collect, sell, and refrigerate and store garlic on their behalf. The big middlemen are often those dealers with thousands or tens of thousands of tons of cold storage; "big speculators" with tens of millions or hundreds of millions of funds buy or sell hundreds of tons of garlic through middlemen. These big speculators are basically from other places, including Fujian, Zhejiang, Guangdong, Hebei, Heilongjiang, etc.; garlic farmers and garlic dealers, as retail investors, follow the trend and speculate when the market is hot; at the same time, garlic electronic trading is also fueling the trend, helping to boost or depress prices.

The trading and financial phenomenon of garlic is often: when speculators see an opportunity, they will purchase a large amount of garlic through middlemen. In this way, in addition to the wholesale volume and export volume of regular transactions in the market every day (normal consumption of the garlic industry and export to Japan and South Korea, etc.), investors will also buy lock-up warehouses in middlemen's cold storage, and sometimes provide leveraged financing. When the market is frenzy, industrial speculators directly speculate on the warehouse receipts of garlic in cold storage. For 1,000 tons of garlic warehouse receipts, the previous speculator may spend 60 million yuan to buy at 3 yuan per catty, and then sell it to the next speculator who continues to be bullish at 4 yuan per catty, totaling 80 million yuan. What is bought and sold are warehouse receipts, and garlic does not leave the cold storage at all. When demand is strong, electronic trading will help push garlic prices up all the way, and then when demand falls, the trading market will also be magnificent.

Louis Dreyfus, one of the four major international grain traders ABCD, has been quietly laying out the entire agriculture, food industry and financial industry, and its penetration into the cotton industry is centered around trading and finance.

China's cotton industry was relatively closed in the early days and the market was difficult to grasp. Louis Dreyfus first hired a group of elites from China's cotton industry with high salaries, especially senior executives from cotton and linen companies in some provinces and cities, and formed a senior team that not only understands the international market but also the Chinese market together with Louis Dreyfus' international talents. Then, through a perfect futures trading mechanism and strong financial strength (overseas funds and domestic bank funds), cross-market operations were carried out through the two cotton futures markets in New York and Zhengzhou, thereby affecting the domestic futures market prices. At the same time, the imported cotton in the spot market and the warehouse receipt cotton purchased and processed domestically were used to cooperate to affect the domestic spot market prices, and finally achieve the dual benefits of futures and spot arbitrage in the futures and spot markets. Finally, with the full opening of China's cotton market, Louis Dreyfus and many international cotton traders quickly intervened and quickly became the most influential industrial capital group in the cotton industry with strong capital.

Non-ferrous metals are very core assets among bulk commodities. As the core of global non-ferrous metal transactions, the London Metal Exchange has also laid the foundation for transactions and finance in the non-ferrous metal industry. However, the complexity of procurement, smelting, finishing, and trade in various production areas and manufacturing industries makes the non-ferrous metal industry more complicated.

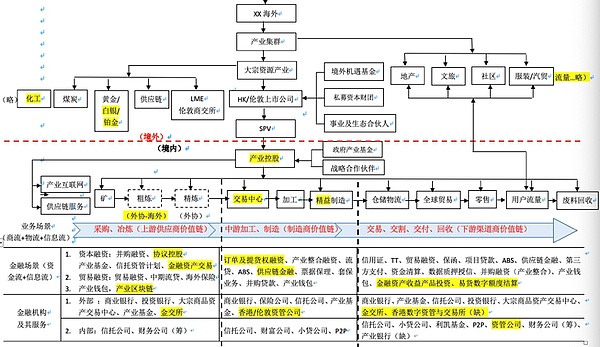

I will not expand on the details of the non-ferrous metal industry here. I will share a framework diagram of industrial upgrading that Ye Kai gave to a Fortune 500 non-ferrous metal group five years ago, which basically gives you a glimpse of the whole picture.

(XX Industry Forest Map Sketch)

There are many cases of industrial transactions, such as emerging asset carbon emissions. There are many related exchanges in China, including the Shanghai and Wuhan Carbon Emissions Exchanges for official carbon emission quotas, the Beijing Green Exchange, and many registered Oriental Carbon Emissions Exchanges, as well as the Macau International Carbon Emissions Exchange. The scale of a carbon emission transaction is not yet mature, but there are already so many exchanges. It is conceivable that the importance of industrial transactions and pricing power. Then the RWA around carbon emissions must be integrated or upgraded with relevant exchanges.

The latest is the hydrogen energy exchange. The hydrogen energy strategy is relatively recent. Transactions and finance related to hydrogen energy and industry, including hydrogen price index, hydrogen energy infrastructure green bonds, supply chain finance for hydrogen production equipment, etc., are also a very large market.

There are two situations for replacement or upgrade design. One is that the newly established industrial exchange can learn from the ideas of blockchain and RWA for upgrade design. The other is that the RWA exchange with virtual asset resources can integrate the financial tokenization of industrial assets and transactions to realize the industrial exchange.

Since industrial exchanges must support diversified trading methods, especially conventional spot trading in the industry, the replacement design of RWA exchanges needs to fully consider the needs of industrial trading and finance. The model of its industrial RWA exchange can be designed as: "spot trading + RWA trading + liquidity pool".

(ChatGPT Raw Picture)

The implementation of spot trading is not complicated. It mainly depends on the refinement of the core logic of the business, and the delivery note voucher can be grasped. The assets and transactions of the industry are not necessarily all physical goods, various logistics, transactions and other records on the chain. As long as the assets are numbered basic data based on the digital system and consensus algorithm of the industry, the relevant transaction flow is Hash encrypted into the on-chain document, and the delivery note of NFT (non-homogeneous token) is generated on the chain. The spot transaction can be a delivery note/warehouse receipt, and the trading system is equivalent to a centralized order book trading system.

The realization of RWA transactions involves multiple links of industrial transactions, from payment settlement of transaction orders to accounts receivable, warehouse receipt pledge and supply chain finance, as well as fixed income bonds, margin trading, accounts receivable ABS, etc. of financial products, which will involve the design of stablecoins, equity, franchise and tokenized products of the industry.

RWA will have diversified trading methods, based on the bill of lading NFT pool, with decentralized AMM, OTC bulk, and may also require some centralized order book functions.

The bill of lading NFT of spot trading, designing NFT swaps in RWA transactions, becomes an option transaction. And some income-type RWA products may come from the spread or interest rate swap of the bill of lading NFT.

Most of the liquidity pools of real-world assets are similar to Uniswap's asset pools, but there are also some consumable assets whose liquidity pools have certain dissipative properties, so different AMM algorithms need to be specially designed.

RWA transactions reserve arbitrage space and products for Makers and Brokers, so there will be spot (bill of lading NFT) contracts, pledge leverage, and futures arbitrage.

Since RWA transactions have asset liquidity pools, there will be industry capital pools, deposits and withdrawals, and payment settlements, but they are tokenized or stablecoins, just like the "industrial currency" designed by Ye Kai when he was doing supply chain finance nearly ten years ago, which is based on the share and split transfer of the credit and commercial bills of core enterprises within the industrial chain. In fact, you can understand this as a stable currency, or as a tokenized credit line for industrial RWA transactions.

RWA transactions also involve contracts, which are equivalent to options on real-world assets. Of course, this is slightly different from cryptocurrency options, because this has the redemption of physical assets as a guarantee, at least it will not be completely zeroed out.

The core of blockchain is a creditless model, while transactions and finance in traditional industries are basically based on credit. Industrial financing depends on big data such as corporate credit, ratings, and asset inventory transactions. These are all centralized, and they are centralized around the core enterprises of the industrial chain, which is very unfriendly and exploitative to upstream and downstream small and medium-sized enterprises.

RWA transactions focus on industries, which can gradually form a decentralized creditless model, form a consensus algorithm in diversified transactions, and the liquidity pool and capital pool will grow a decentralized asset pricing algorithm. In this process, because RWA is tokenized, it is possible to further generate utility and governance tokens for industrial transactions, which can be used to incentivize counterparties and pledge rewards, etc., making it more inclusive and efficient. Similarly, because the industrial stablecoins or industrial tokens in RWA transactions, as the "industrial currency" circulating within the industrial chain, greatly improve the capital turnover rate and reduce the cost of capital, and can moderately increase leverage.

RWA transactions can also not take the equity securitization design, but take alternative investments. Because most of the real-world physical assets are alternative assets, the model of "spot trading NFT + RWA NFT + liquidity pool + liquidity fund" can be used, which is equivalent to a physical electronic disk, taking the non-securities route, physical assets supporting and empowering the real industry, doing a good job of KYC and AML, and upgrading to "ATS RWA exchange + localized broker + industry cluster institution community +..."

Industry has a clustering effect. For example, mining in Canada, global mineral resource transactions, mining companies listed, etc., are mostly on the TSX, and hydrogen energy may be in Japan or Australia with a high probability, because these two countries are national hydrogen strategies and the largest purchasing countries. In theory, if you are the largest purchaser, you have the conditions to dominate the trading platform and pricing power. If not, it means that you have not done well and have been passed by other industrial capital combined with industrial exchanges.

The upgrades that RWA Exchange brings to industrial exchanges are very clear and necessary:

Improve efficiency

Reduce capital costs

Increase capital turnover

Increase transparency of trade assets, transaction flow, warehouse receipts, bills of lading and invoices

Monetization of trade credit

Diversified financing and bill lending and reasonable leverage

left;">Achieve flexible industrial resource mismatch, small-scale inclusive finance can be split and circulated, and liquidity

Someone may ask: Which industries have room for upgrading?

For RWA exchanges, emerging industries may have more opportunities. After all, there are no mature exchanges and no mature valuation systems, and the entire industry is in the early stages of development. Therefore, the following industries can be paid more attention to:

AI computing power

Green electricity

Hydrogen energy

Certain financial attribute products such as agarwood, whiskey, ancient tea trees, etc.

What exactly is RWA (real world asset tokenization)? Is RWA a product or a transaction?

JinseFinanceIt seems obvious that the real-world asset tokenization space has huge growth potential in the future. But what exactly is this trend, why is it attracting so much attention and hype, and how can you make the most of it?

JinseFinanceRussian commodity companies that have experienced difficulties in conducting financial transactions with Chinese partners have begun using cryptocurrencies for payments.

JinseFinanceBuffett bought shares of Japan's five largest trading companies, namely Mitsui & Co., Mitsubishi Corporation, Sumitomo Corporation, Itochu Corporation and Marubeni Corporation. From the perspective of returns, the shares of the five major trading companies, denominated in yen, have increased by at least 2 times and at most nearly 5 times.

JinseFinanceJinseFinanceBank of Russia plans to pilot cross-border payments using digital assets and central bank digital currencies, according to a deputy governor.

Others

OthersSBF and Zhu Su trade blows over alleged media control.

cryptopotato

cryptopotatoBlockchain technology has proven to be transparent and could make international trade transparent and even more secure.

Cointelegraph

CointelegraphThe crypto exchange said it had $48 million in exposure with Babel Finance and $5 million with Celsius — both firms faced liquidity and insolvency issues, respectively.

CointelegraphThe Philippine Department of Trade and Industry waved off a Binance ban proposal, citing a lack of regulatory stance on cryptocurrencies from the central bank.

Cointelegraph