Detailed explanation of Pandora’s value and valuation

Pandora, a detailed explanation of Pandora's value and valuation. Golden Finance, wherever there is money and traffic, the most innovation will break out.

JinseFinance

JinseFinance

By @gnsGoblin

Source: Twitter

This article aims to compare the revenue and valuation of some well-known decentralized perpetual contracts exchanges (DYDX, GMX, GNS, IDEX).

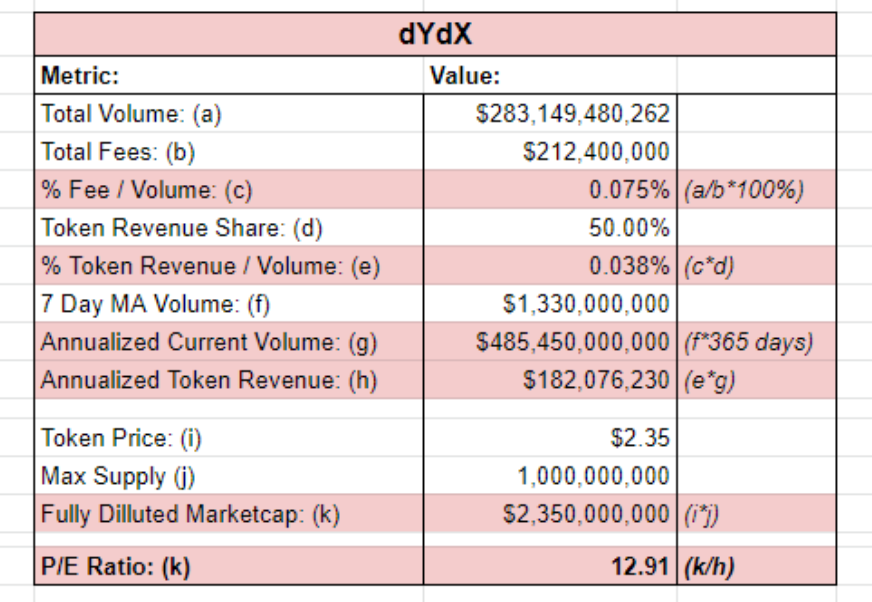

First, let’s take a look at @dYdX, the largest and most used perpetual contract DEX currently on the market.

We can see that the dYdX token has a P/E ratio of 12.91 based on current trading volume and fees.

While there is currently a revenue share, dYdX has plans to decentralize as it transitions to V4 .

The token economics of this are still TBD, but for comparison I assume a realistic scenario where token holders get 50% of the income.

As the largest perpetual exchange, I think its fee model of 0.075% of total transaction volume is a good benchmark for comparison with other protocols.

The P/E ratio of 12.91 is actually lower than I expected, from this perspective, I think dYdX may be undervalued, however, without knowing the future token economics, this is still speculation.

The data source I use to analyze dYdX comes from the @tokenterminal page .

Really hope someone can confirm the accuracy of the data.

Before we move on to analyzing other projects, I would like to say that I don't think dYdX is a real competitor to GMX or GNS as they are more like a CEX with self-hosting.

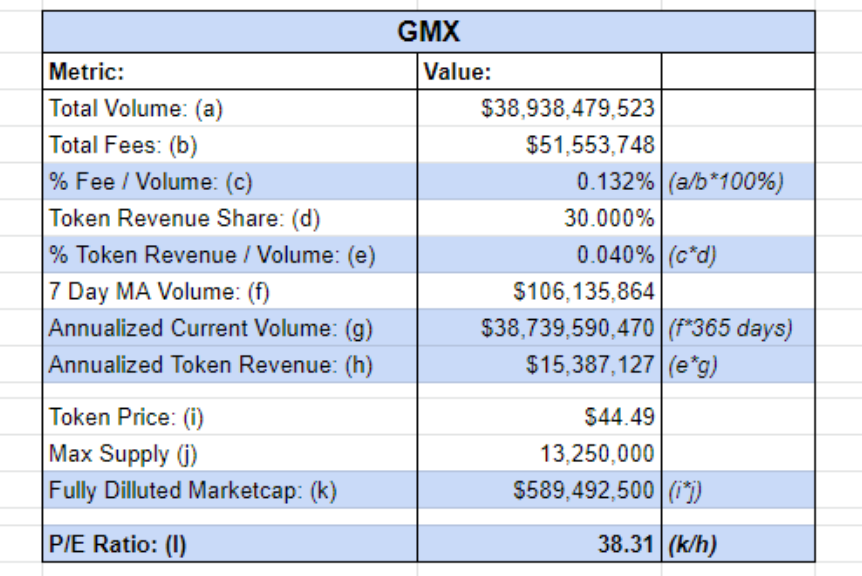

Next, we take a look at the famous decentralized perpetual exchange @GMX_IO on @arbitrum .

According to my calculations, they currently trade at a P/E ratio of 38.31.

I'm sure I'll get some comments about max supply vs. circulating supply and esGMX.

When making comparisons in this regard, it is important that we consider the maximum supply because even though esGMX may not be liquid, revenue is still allocated to these tokens.

We can observe that the fee percentage is much higher than both dYdX and GNS. I suspect this is because swaps have higher fees than perpetuals.

Overall, I think the P/E ratio is around 40, which, while higher than other items, is actually reasonable for GMX with the upcoming updates to PvP AMM and X4 .

In my opinion, there is still room for growth in this area, and I wouldn't be surprised to see the number around 100.

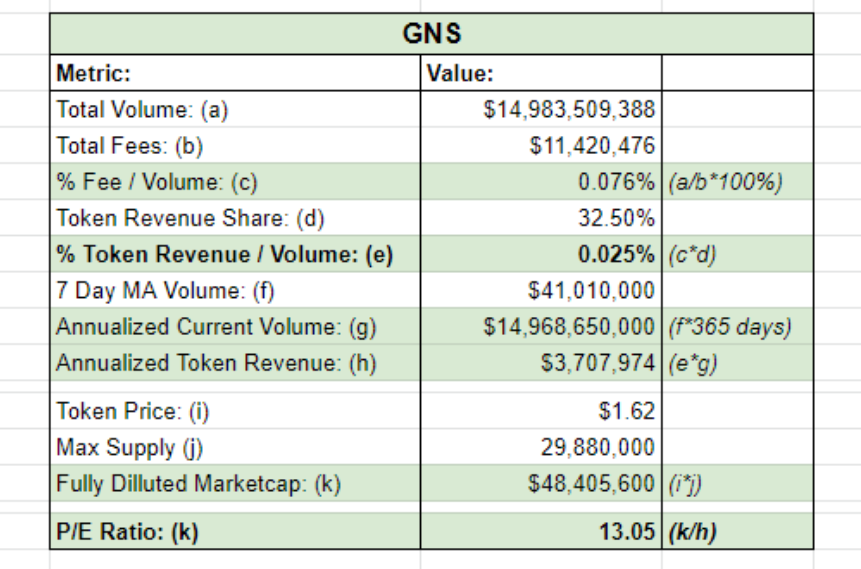

Next we look at @GainsNetwork_io , based on the current transaction volume and price, we can conclude that the PE ratio of this project is 13.05.

We can see that fees/volumes are basically in line with dYdX, which is quite surprising. I think this fee structure for GNS is correct.

At a P/E level of 13.05, I think GNS is undervalued, especially compared to GMX and IDEX.

I think there's a lot of room for growth.

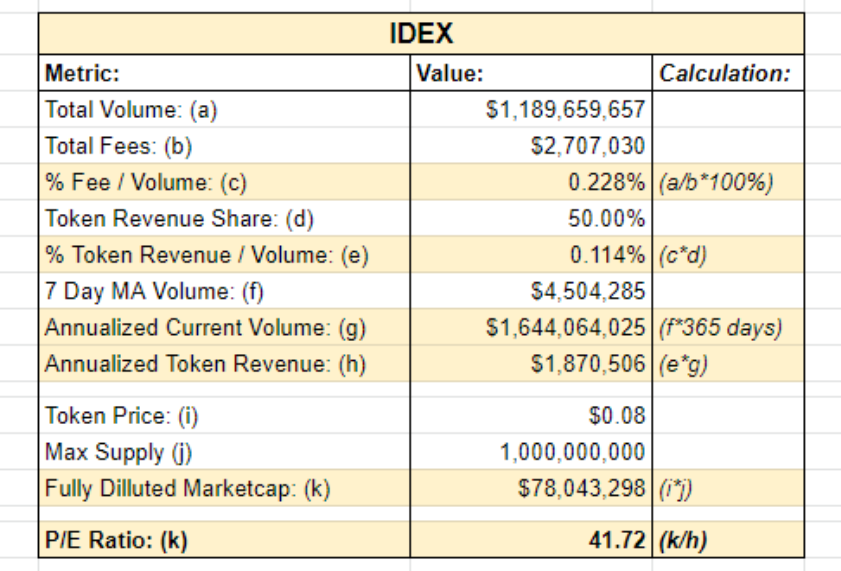

Finally, we look at @idexio .

It has similar token economics to GMX and GNS, and I think it's worth a look.

What surprised me the most is that the protocol's fees are very high relative to volume and P/E, especially compared to the other protocols mentioned in this article. Admittedly, I don't know much about IDEX, maybe there is something going on behind the scenes.

in conclusion:

There is a lot of room for growth in the sustainable DEX field, and I hope the analysis in this article is useful to you.

I also believe that each project can succeed and grow in competition with the other, rather than a winner takes all.

Pandora, a detailed explanation of Pandora's value and valuation. Golden Finance, wherever there is money and traffic, the most innovation will break out.

JinseFinanceAs the first Ethereum Rollup to feature a decentralized orderer, Metis is significantly positioned in the highly competitive layer-2 (L2) network space.

JinseFinanceGolden Weekly is a weekly blockchain industry summary column launched by Golden Finance. The content covers key news of the week, market and contract data, mining information, project trends, technology progress and other industry trends.

JinseFinanceWorldcoin's value soars in Singapore, user base grows despite privacy concerns.

Huang Bo

Huang BoFTX's new bankruptcy plan proposes valuing digital assets at the bankruptcy date, potentially disadvantaging creditors.

AlexJinseFinance

AlexJinseFinanceIn a significant blow to OpenSea, a colossal wave of devaluation has hit the NFT marketplace. Coatue Management, a prominent player in asset management, has sent shockwaves through the market by slashing OpenSea's valuation by a drastic 90%.

Jixu

JixuAccording to Cointelegraph Research, VCs invested $14.67 billion into blockchain startups Q2. Web3 projects have attracted significant interest.

Cointelegraph

CointelegraphThe Birth of an Application Chain

链向资讯

链向资讯The raise comes as total value locked on the Avalanche blockchain remains steady at around $14.6 billion.

Cointelegraph