Learn about BlobScriptions in one article

Ethereum's Dencun upgrade in March 2024 introduced a concept called Blob. Blob is a novel data storage concept designed to reduce transaction costs for layer 2 scaling solutions.

JinseFinance

JinseFinance

Note: The original author is Vitalik Buterin, the co-founder of Ethereum.

Special thanks to Dan Robinson, Hayden Adams, and Dankrad Feist for their feedback and review.

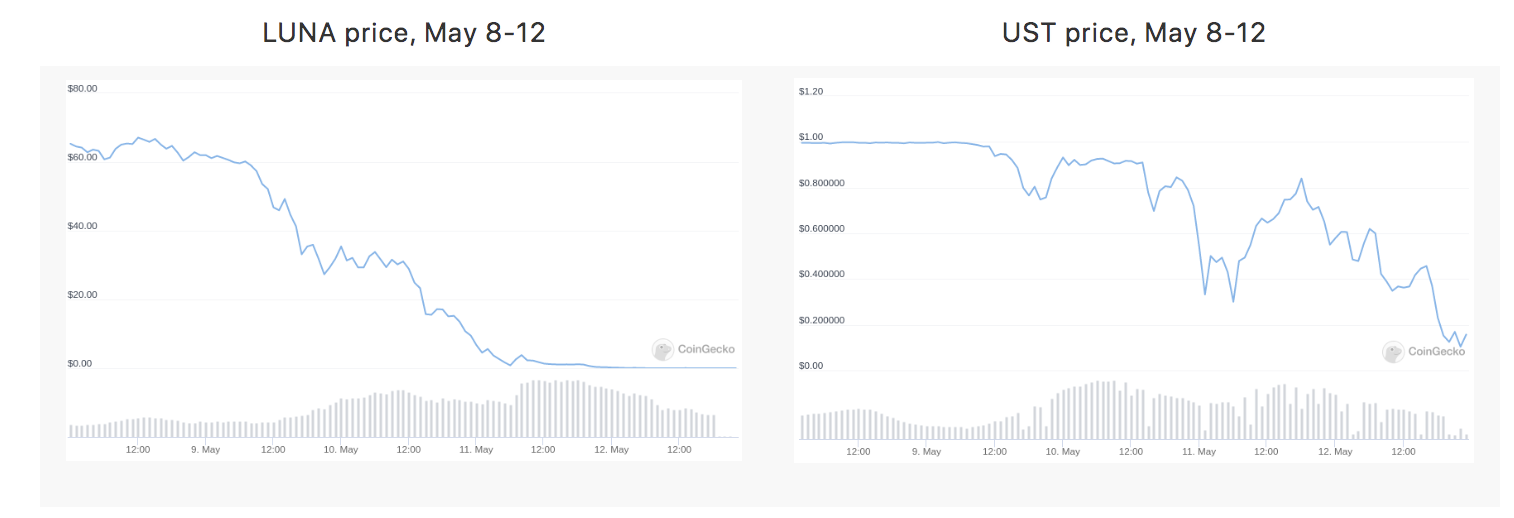

The recent LUNA debacle, which resulted in losses of tens of billions of dollars, has sparked a firestorm of criticism against the category of "algorithmic stablecoins," with many arguing that they are "fundamentally flawed products." Greater scrutiny of DeFi financial mechanisms, especially those that strive to optimize “capital efficiency,” is very welcome. And a greater acknowledgment that current performance is no guarantee of future returns (or even a complete crash in the future) is more welcome. What goes so wrong, though, is that people paint all automated pure-crypto stablecoins with the same brush and dismiss the entire category.

While there are plenty of automated stablecoin designs that are fundamentally flawed and doomed to collapse, there are many more theoretically survivable but high-risk stablecoins, and there are also plenty of stablecoins that are theoretically very healthy and have survived in practice extreme test of crypto market conditions. Therefore, what we need is not stablecoin boostism or stablecoin doomsdayism, but a return to principle-based thinking . So, what are some good principles for assessing whether a particular automated stablecoin is truly stable?

For me, I started testing to see how stablecoins respond to two thought experiments.

For the purposes of this article, an automated stablecoin is a system with the following properties:

In practice, (2) means that the target mechanism must be some kind of smart contract that manages some reserve of cryptoassets and uses these cryptoassets to prop up prices when prices fall.

Terra-style stablecoins (roughly the same as seigniorage shares, though with many implementation details different) work through a dual-coin model, which we refer to as stablecoins and volatilecoins (in Terra's case, UST is the stablecoin and LUNA is the fluctuating currency). Stablecoins use simple mechanisms to maintain stability:

What is the price of Volatcoin now? The value of volcoins may be purely speculative, relying on the assumption that there will be greater demand for stablecoins in the future (which would require burning volcoins to issue). Alternatively, the value of volcoins could come from fees: transaction fees for stablecoin <-> volcoin transactions, or annual holding fees charged to stablecoin holders, or both. But in all cases, the price of the fluctuating coin comes from anticipation of future activity in the system.

In this post, I focus on RAI rather than DAI, as RAI better embodies the pure "ideal type" of collateralized automation stablecoins, backed only by ETH. While DAI is a hybrid system backed by centralized and decentralized collateral, this is a reasonable choice for their product, but it does make analysis trickier.

In RAI, there are mainly two types of participants (there are also holders of FLX, which is a speculative token, but they play a less important role):

There are two main reasons to become an RAI lender:

If the price of ETH falls, and the safe no longer has sufficient collateral (that is, RAI debt is now more than 2/3 of the value of ETH deposited), a liquidation event will occur. By offering more collateral, the safe is auctioned off for others to buy.

Another major mechanism to understand is the redemption rate adjustment. In the case of RAI, the target value is not a fixed amount of dollars, instead it moves up or down, and the rate at which it moves up or down is adjusted according to market conditions:

In the non-encrypted real world, nothing lasts forever. Companies always fail, either because they couldn't find enough users in the first place, because the strong demand for their product no longer exists, or because they were replaced by a stronger competitor. Sometimes, there are partial meltdowns where the company falls from mainstream status to niche status (eg MySpace). These things have to happen to make room for new products. But it’s important to note that in the non-crypto world, users are usually not too hurt when a product shuts down or hits a landslide. Of course there were a few people who fell through the cracks, but overall the shutdown was orderly and the problems were manageable.

But what about automated stablecoins? What happens if we look at stablecoins from a bold and radical perspective, that the ability of the system to avoid crashing and losing large amounts of user funds should not depend on a constant influx of new users? Let's see!

In the case of Terra, the price of Luna (LUNA) is derived from expectations of fees for future activity on the system. So what happens if expected future activity drops to near zero? The market cap of the volatile coin (LUNA) will drop until it becomes very small relative to the market cap of the stablecoin. At this point, the system will become extremely fragile, and a small downward impact on the demand for stablecoins may cause the target mechanism to issue a large amount of Luna, which will lead to hyperinflation of Luna. Stablecoins also lose value over time.

The collapse of the system can even become a self-fulfilling prophecy: if the system seems likely to collapse, it will reduce users' expectations of future fees, which is the basis of the value of the volatility currency, thereby further pushing down the market value of the volatility currency, Making the system more vulnerable could eventually lead to a crash, as we saw with Terra in May.

First, the price of volatile coins fell, and then, stable coins started to shake. The system attempts to support the demand for stablecoins by issuing more fluctuating coins. As users' confidence in the system was low, which resulted in few buyers, the price of volcoins dropped rapidly. Finally, once the price of volatile coins approaches zero, stablecoins also collapse.

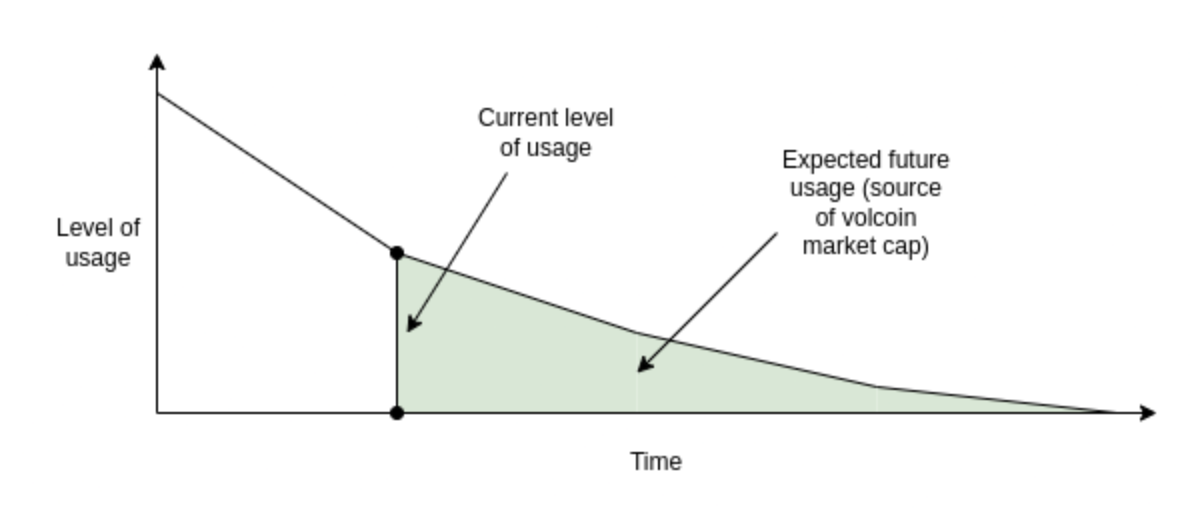

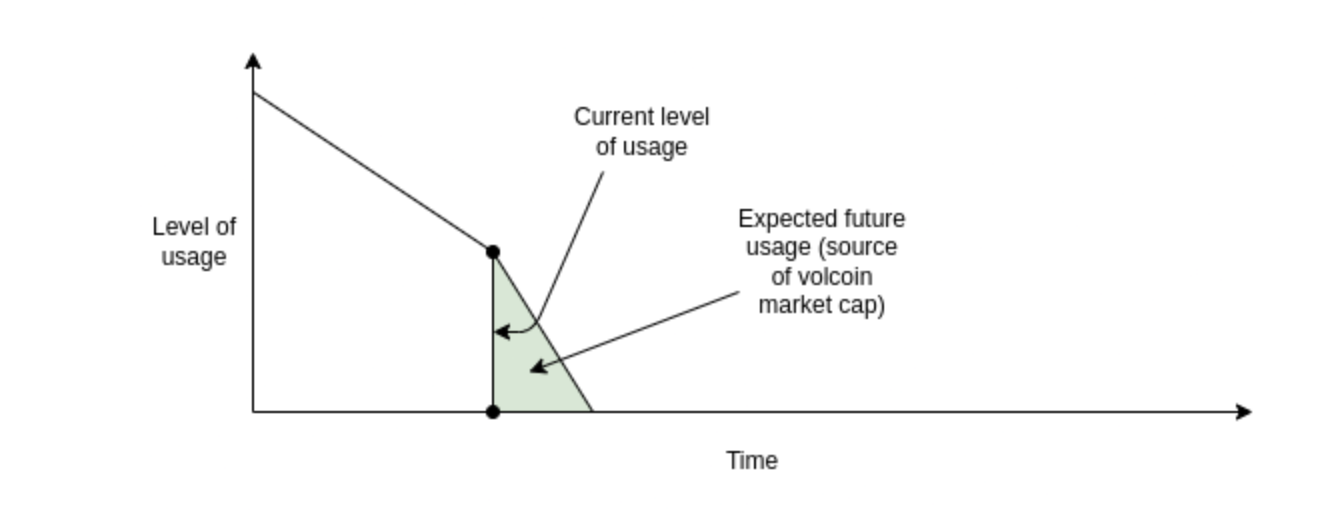

In principle, if demand falls very slowly, the expected future fees of a volatilecoin and its market cap equivalent to a stablecoin could still be large, so the system will continue to be stable at every step of its decline. But this slow decline in success is less likely than a more likely scenario of a rapid drop in user interest followed by a bang.

Safe Fall: At each step, there is enough expected future revenue to justify the volatility coin's market cap being sufficient to keep the stablecoin safe at its current level.

Insecure Descent: At some point, there is not enough expected future revenue to justify enough volatility coin market cap to keep the stablecoin safe, so a crash is possible.

The safety of RAI depends on assets outside the RAI system (ETH), so it is easier for RAI to land safely. If the decline in demand is unbalanced (thus, holding demand falls faster or loan demand falls faster), the redemption rate will be adjusted to balance the two. Lenders hold leveraged positions in ETH rather than FLX, so there is no risk of a positive feedback loop where a drop in confidence in RAI leads to a drop in demand for loans.

If, in the extreme case, all demand for holding RAI disappears at the same time, and there is only one holder, the redemption rate will skyrocket until eventually every lender's coffers are liquidated. The remaining single holders will be able to buy safes in a liquidation auction, use their RAI to instantly liquidate their liabilities, and withdraw ETH. This gives them a chance to get a fair RAI price and get paid in ETH from the safe.

Another extreme case worth examining is RAI becoming the main application of Ethereum. In this case, it is expected that there will be less demand for RAI in the future, which will lower the price of ETH. In extreme cases, there could be a cascade of liquidations leading to chaotic collapse of the system. But RAI is much more resistant to this possibility than Terra-style systems.

Currently, stablecoins tend to be pegged to the US dollar, with RAI being a minor exception, as its peg adjusts up and down based on the redemption rate, and the peg starts at $3.14 instead of $1 (the exact starting value is Friendly concession, since a true math buff would choose tau = 6.28 USD). But they don’t have to be, you can peg a stablecoin to a basket of assets, a consumer price index, or some arbitrarily complex formula (“an amount sufficient to buy the value of {global average CO2 concentration minus 375} hectares of Yakut forest land”). As long as you can find an oracle to prove the index and get people to participate in all aspects of the market, you can make a stablecoin like this work.

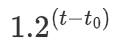

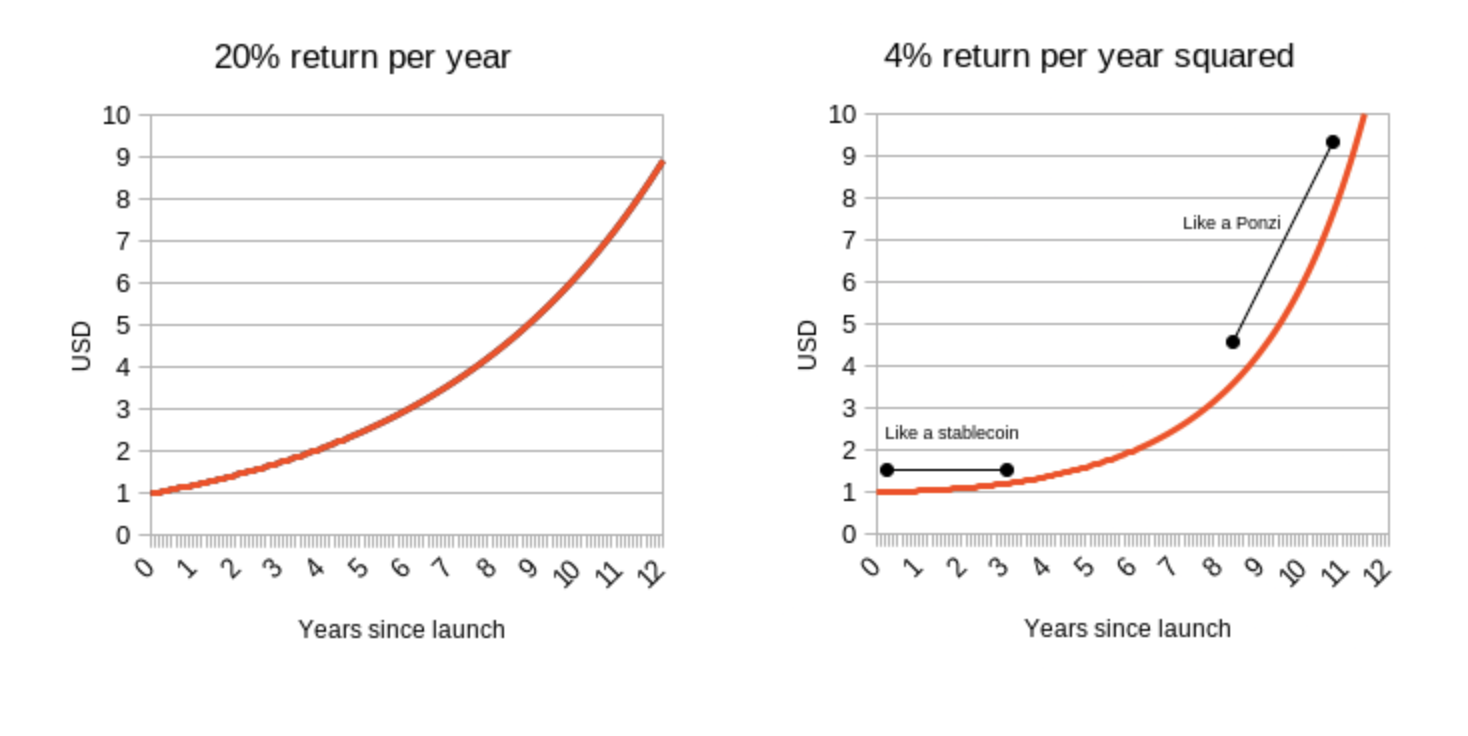

As a thought experiment to assess sustainability, let's imagine a stablecoin with a certain index: the number of dollars growing by 20% per year. In mathematical language, the exponent is

USD, where t is the current time in years and t0 is the time the system was started. A more interesting option is

USD, so it starts out like a USD-denominated stablecoin, but USD-denominated returns are growing at 4% every year.

Clearly, there is no real investment that returns anywhere near 20% per year, and absolutely no real investment that returns 4% per year forever. But what happens if you try it?

I will claim that there are basically two approaches to a stablecoin trying to track such an index:

It should be easy to understand why RAI is (1) and LUNA is (2), so RAI is better than LUNA. But it also shows a deeper and more important truth about stablecoins: For a collateralized automated stablecoin to be sustainable, it must somehow control the possibility of implementing negative interest rates. A version of RAI that programmatically prevents the implementation of negative interest rates (which early single-collateral DAI basically did) would also turn into a Ponzi scheme if pegged to a rapidly appreciating price index.

Even outside of the crazy assumptions that you build a stablecoin to track a Ponzi index, the stablecoin has to somehow be able to handle situations where demand for holding exceeds demand for borrowing even at zero interest rates. If you don't, the price rises above the peg, and the stablecoin becomes vulnerable to price movements in both directions, which are very unpredictable.

Negative interest rates can be achieved in two ways:

Option (1) has UX flaws where the stablecoin no longer clearly tracks "$1" and option (2) has developer experience flaws, but choosing one of the two seems inevitable - Unless you go the MakerDAO route and become a hybrid stablecoin that uses both pure crypto and a centralized asset like USDC as collateral.

In general, the crypto industry needs to move away from the attitude of relying on endless growth for security. Maintaining this attitude by saying "the fiat world works the same way" is certainly unacceptable, since the fiat world is not trying to provide faster than normal economic growth for anyone (except those who deserve the same venomous criticism) except in isolated cases).

Instead, we should evaluate the safety of a system by looking at its steady state, or even its pessimistic state under extreme conditions, and ultimately whether it can be safely shut down. If a system passes this test, that doesn't mean it's secure. It could still be vulnerable for other reasons (such as an insufficient collateralization ratio), or have code bugs or governance bugs. But robustness to steady state and extreme cases should always be the first thing we check.

Ethereum's Dencun upgrade in March 2024 introduced a concept called Blob. Blob is a novel data storage concept designed to reduce transaction costs for layer 2 scaling solutions.

JinseFinanceWill Beacon's coin issuance divert the value of Magic? Arweave's ecological project AO, which claims to be the Ethereum killer, is it valuable?

JinseFinanceRecently, the trend of Ethereum spot ETF has reversed, attracting great attention from the market and regulators. Based on the optimism about the US approval of the Ethereum spot ETF, the price of Ethereum has risen sharply this week and is currently priced at US$3,807.

JinseFinanceBitcoin and stablecoins are flying together, and the signs of a bull market or false fire are particularly obvious, attracting funds from the off-site and on-chain respectively.

JinseFinanceWe'll see how to use them, their definitions and how to use event topic hashes and signatures to filter logs, as well as some advice on when you should use these.

JinseFinanceMerlin Chain, understand MerlinChain in one article Golden Finance, early Merlin Chain is worth participating in

JinseFinanceLarry Fink has become somewhat of a leading global influencer on the Bitcoin market.

JinseFinance Cointelegraph

CointelegraphFinancial service platform Revolut launched a crypto educational tool on Polkadot (DOT) and the nascent industry. Aimed at making the ...

Bitcoinist

BitcoinistThe world is in a never-ending state of change. The norms of just a few years ago are in many ...

Bitcoinist