AB DAO 官方 Twitter 账号升级,提醒社区注意风险

AB DAO 官方 Twitter 账号已完成升级,新账号 为:https://x.com/ABDAO_Global

Alex

Alex

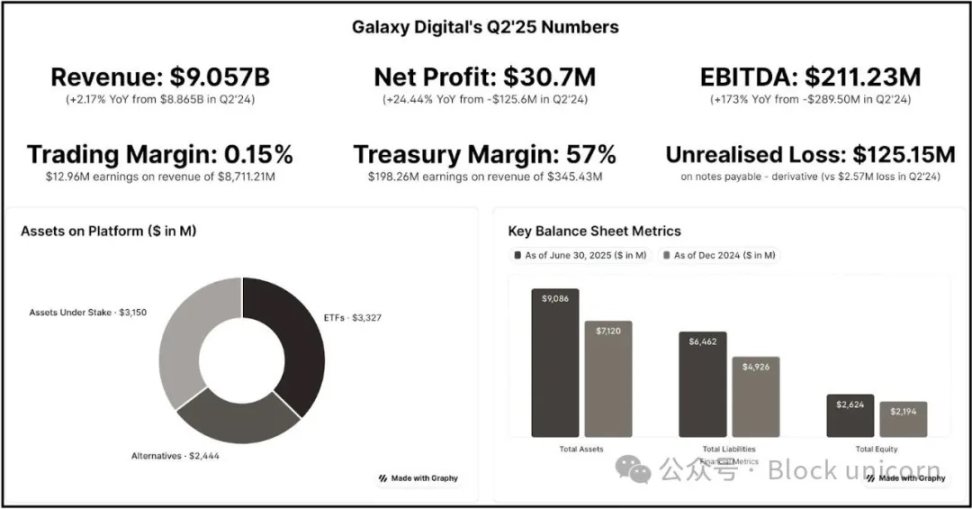

Galaxy's cryptocurrency trading business generated only $13 million in profit on $8.7 billion in revenue (a 0.15% margin) while paying out $18.8 million in quarterly compensation—core cash flow is negative.

AI Transformation: A 15-year, 526-MW contract with CoreWeave is expected to generate over $1 billion in annual revenue over three phases starting in the first half of 2026, with a 90% profit margin.

Control of 3.5 GW of capacity in Texas in a supply-constrained market where data center demand must increase fourfold by 2030.

$1.4 billion in project financing has been secured, validating commercial viability and eliminating execution risk.

The current model relies on cryptocurrency asset returns ($198 million in the second quarter) to fund operations, as capital-intensive trading yields meager returns.

The stock price retreated after a 17% rally as investors see no incremental revenue until the first half of 2026.

When you look at Galaxy Digital's second-quarter figures, it's easy to overlook one thing: what's coming next. A closer look reveals that the company, led by Michael Novogratz, is at a turning point in its transition from cyclical cryptocurrency trading to more stable AI infrastructure revenue.

Galaxy Digital is undertaking one of the largest business transformations in the cryptocurrency industry – a shift from low-margin trading to high-margin AI data centers.

Galaxy generated $31 million in net revenue for the quarter, and after adjusting for non-cash and unrealized charges, total adjusted EBITDA was $211 million. Of its total revenue, the trading business earned just $13 million in profit on $8.7 billion in sales—a mere 0.15% profit margin. Therefore, 95% of its revenue is barely profitable. By contrast, their new AI data center contract promises a 90% profit margin on over $1 billion in average annual revenue. While I am bullish on building AI and high-performance computing capabilities, I believe the promised profit margins are overly exaggerated. But don't just take my word for it; compare the profit margins reported by top AI data operators like Equinix and Digital Realty this quarter: 46-47%. However, I believe the direction is right, purely from a revenue generation perspective. Currently, the majority of Galaxy's revenue comes from its high-cost, low-margin trading business. The majority of its profit (revenue less expenses) comes from its asset and enterprise segments. The asset segment includes investments in digital assets and mining activities, equity investments, and realized and unrealized gains and losses on digital asset and equity investments. Its $2 billion asset pool serves as an investment vehicle and even a strategic source of capital when market conditions are favorable. The division generated $198 million in earnings, excluding non-cash unrealized gains. Unlike pure-play cryptocurrency companies, Galaxy's asset business generates capital by selling assets at strategic times. This is where I believe Galaxy's cryptocurrency asset strategy differs from Michael Saylor's Bitcoin asset strategy. Saylor's "buy, hold, never sell" strategy generated $14 billion in unrealized gains this quarter. However, these are only paper profits, and Saylor shareholders receive no share of them. Galaxy's situation is different. It not only buys and holds cryptocurrencies in its asset pools, but also makes strategic sales, resulting in realized profits. This is real money that shareholders can share in. However, I believe Galaxy's asset division is an unreliable source of income. As long as the cryptocurrency market is performing optimally, the division will consistently generate returns. But that's not how markets work, whether traditional or cryptocurrency. Markets are cyclical at best, making these returns heavily dependent on cryptocurrency market conditions. This is why Galaxy needs its AI transformation to succeed, as the current model is unsustainable. Market Opportunity Galaxy has positioned itself at the intersection of two massive trends: exploding demand for AI computing and a chronic shortage of U.S. power infrastructure. According to a McKinsey report, global data center demand is expected to quadruple from 55 GW in 2023 to 219 GW by 2030. Hyperscale cloud service providers are expected to invest $800 billion in capital expenditures (CapEx) on data centers by 2028, a 70% increase from 2025, but this is constrained by power supply. Galaxy's advantage lies in its 3.5 GW potential capacity at its Helios campus in Texas, enough to power over 700,000 homes in the state. With 800 MW already approved and another 2.7 GW under study by the Electric Reliability Council of Texas (ERCOT), Galaxy controls some of the largest available power capacity in the supply-constrained AI infrastructure market. A digital rendering of Galaxy's Helios AI and HPC data center campus in Texas. Galaxy's transformation is underpinned by a 15-year commitment with CoreWeave, one of the industry's largest AI infrastructure deals. CoreWeave has committed to providing 526 megawatts of critical IT capacity over three phases. A projected 90% profit margin is attributed to the asset-light nature of data center operations once the infrastructure is built. I saw a significant risk in the CoreWeave deal: execution. Just as I was considering the size of the capital raise, planning, and execution Galaxy needed, the company cleared the first hurdle. On August 16, Galaxy successfully closed $1.4 billion in project financing for the Helios data center, securing funding for the first phase of construction. This gave me greater confidence in how to mitigate key financial risks and validate the commercial viability of the Helios project. Galaxy's current cash flow reveals the volatility of its trading business while highlighting why AI infrastructure can provide real financial stability. The company ended the second quarter with $1.18 billion in cash and stablecoins, which sounds substantial, but the reality is more complex. Galaxy's trading business is capital-intensive, and margin lending requires significant cash reserves. Much of this $1.18 billion is not freely available. Galaxy's actual free cash flow generation is minimal. After paying $14.2 million in interest expenses and ongoing operating expenses, the core business barely breaks even at cash flow breakeven. This forces Galaxy to rely on the appreciation of the cryptocurrency market, specifically its treasury and mining operations, to generate funds to support operations amidst the inherent cyclicality and unpredictability. CoreWeave's three-phase contract structure and high-margin business characteristics could generate immediate positive cash flow. While margins may not be as high as 90%, even a more conservative 40-50% margin would still be more reliable and stable than the cyclical treasury business. Unlike trading operations, which require continuous investment in working capital and technology infrastructure, cash generated from data center operations can be reinvested in expansion or returned to shareholders. Galaxy's recent financing for the Helios project has helped address cash flow issues. By securing dedicated construction funding, Galaxy has separated infrastructure development from its operational cash flow needs. This is unachievable in a trading expansion, as the balance sheet capital required for trading expansion would compete directly with other business needs.

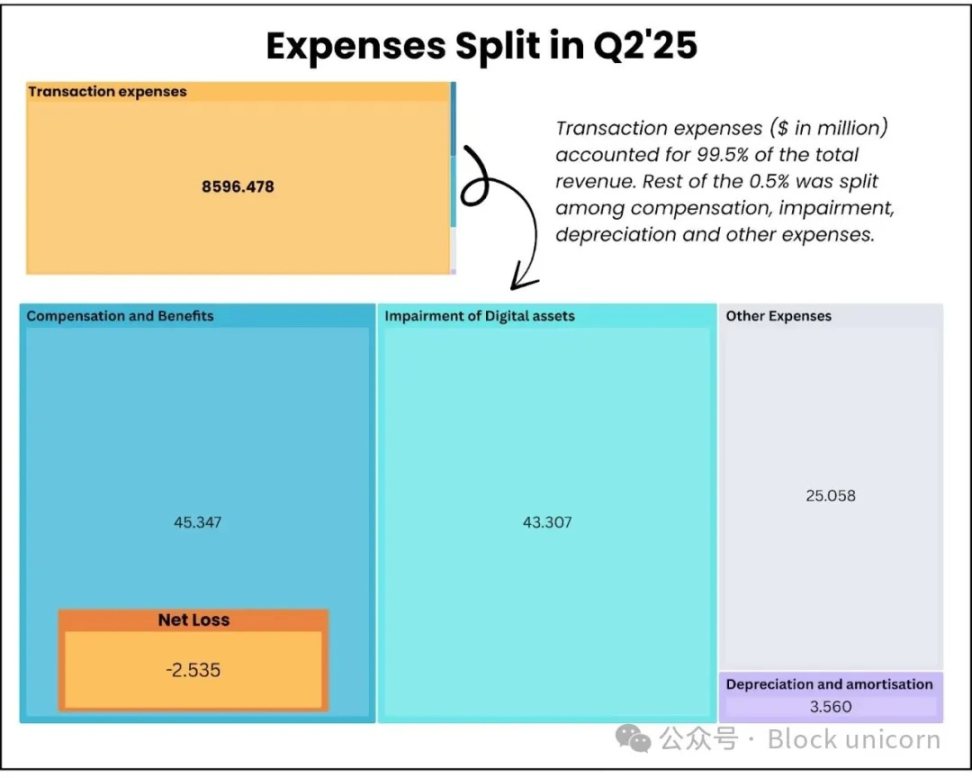

The digital assets division incurred $8.714 billion in total expenses, with trading fees accounting for the largest share ($8.596 billion). These expenses are purely pass-through costs with little room for improvement. Galaxy has little ability to optimize these costs, as they are unavoidable in a commoditized trading business where spreads continue to narrow.

Even more concerning, quarterly compensation expenses included $18.8 million in stock-based compensation, which had to be paid in cash. This means Galaxy is spending more to retain talent than its core business generates ($13 million). The transformation to AI infrastructure will change this. Once the facility is operational, data center operations require minimal variable costs. To put this into perspective, Galaxy's entire digital asset business generated $71.4 million in adjusted gross profit in the second quarter. At full capacity, Helios Phases 1 and 2 alone (approximately 400 megawatts) could generate $180 million in quarterly revenue, with a fraction of the operational complexity and costs of the trading business. Market Reaction: Galaxy's stock price rose slightly by 5% in the 24 hours following the release of its second-quarter earnings report and jumped approximately 17% within a week before investors began to withdraw their capital.

This may be because investors realized that $180 million of the $211 million gain came from non-cash adjustments and treasury gains, rather than operational improvements.

Investors may not have fully factored in Galaxy's complex transformation into AI infrastructure, as significant data center revenue is not expected until the first half of 2026.

I remain optimistic about long-term market sentiment given the potential for future growth. According to ERCOT research, Galaxy's addition of 2.7 gigawatts of capacity demonstrates the company's intention to solidify its position as a long-term infrastructure provider rather than a single-tenant facility operator. At full capacity, Galaxy's Texas operations will rival some of the largest hyperscale data center campuses operated by Amazon, Microsoft, and Google. This scale could provide it with negotiating leverage with other AI companies while also improving operational efficiencies and thus increasing profit margins. The company's expertise in cryptocurrency uniquely positions it in the emerging field where AI and blockchain technology intersect. The Way Forward: Galaxy is making a massive, polarizing bet. If its AI infrastructure transformation succeeds, it will transform itself from a low-margin trading company into a cash-generating machine. If it fails, it will spend billions of dollars on expensive real estate in Texas while its core business gradually declines. The $1.4 billion in project financing confirms external confidence, but I'm watching two key metrics: Can they actually deliver 133 MW of AI-ready capacity by the first half of 2026? And will those 90% profit margins be sustainable once they start covering real operating costs? Current operations provide sufficient cash flow to sustain the business, but continued strong performance in the cryptocurrency market is needed to make meaningful growth investments. The AI infrastructure opportunity promises sustained and reliable revenue potential, and its success depends entirely on execution over the next 18-24 months. The recent project financing close removes significant execution risk, but Galaxy must now demonstrate that it can successfully transform crypto mining infrastructure into an enterprise-grade AI computing facility to attract investors for a long-term bet.

AB DAO 官方 Twitter 账号已完成升级,新账号 为:https://x.com/ABDAO_Global

AlexThe latest trailer for HBO's documentary will reveal the true identity of Satoshi Nakamoto this week. Its producer admitted to confronting the real person in person and believed that Satoshi Nakamoto is still alive. According to betting market data, the market currently speculates that the most likely candidate is Nick Szabo, which coincides with Musk's early theory.

Miyuki

MiyukiArweave, Arweave's working principle and significance of existence Golden Finance, this article briefly introduces Arweave's working principle and value.

JinseFinance

JinseFinanceThe U.S. economy declined more than expected, global liquidity tightened more than expected, domestic industrial policies were not implemented as expected, the "black swan" event before the U.S. election had an impact, and expectations of global geopolitical turmoil rose more than expected.

JinseFinanceThe S&P 500 (an index of the top 500 US companies) is still below its mid-July peak and the level at the end of July when the “crash” began. What is causing this downward trend? Does it portend more serious problems for the US economy?

JinseFinanceOn August 8, the U.S. Federal Reserve took a major enforcement action against Pennsylvania-based Customers Bank, marking the U.S. government’s gradual increase in regulatory oversight of cryptocurrency-related businesses.

JinseFinanceJinseFinanceJinseFinanceThe Ethereum Foundation's Danny Ryan discusses how the Merge will increase security and explains how proof of stake impacts developers.

Future

FutureNigel Dobson, head of portfolio banking services at ANZ, said: "When we looked at this in depth, we came to the conclusion that this is a significant protocol shift in financial market infrastructure."

Cointelegraph

Cointelegraph