Understanding and analysis of the RWA track

I basically just observed the RWA track and rarely participated in it.

JinseFinance

JinseFinance

Before Ethena's high interest, Luna-UST's tragic past is just a thing of the past, and it has returned to a game of who can run faster.

Even MakerDAO's DAI can't escape the temptation, changing its usual low-risk nesting of USDC shells and actively embracing USDe's high returns.

Although Ondo issued USDY in less than three weeks, its TVL has risen from 100 million to 200 million, but it has pulled in the BUIDL fund established by BlackRock to resist risks together and jointly expand and strengthen the RWA ecosystem.

As we can see, the above three are all stablecoins, and they are also the latest developments of RWA - real assets on the chain, native arbitrage on the chain, and finally feeding back to real assets, forming three small worlds that are connected end to end but run independently.

Specifically, at this stage, RWA not only focuses on stablecoins, but also has the following new trends.

The real world is denominated in US dollars: Real assets focus on four major categories of assets: US Treasury bonds, US dollars, bonds and compliant stablecoins. Rather than saying that real assets are on the chain, it is better to say that US dollar-related assets are on the chain.

Dual Currency Standard in the Crypto World:The status of Bitcoin and Ethereum is generally recognized by the crypto world. Ethereum is not only an asset issuance chain, but ETH also plays a role equivalent to the "Bitcoin" reserve.

Fusion replaces change:Traditional finance and exchanges have become the infrastructure for the operation of cryptocurrencies. RWA comes from them and eventually flows to them. Even their existence is no longer a problem. The gravity of reality finally weighs down the head of dreams.

Each bull-bear cycle starts with Bitcoin, and then there is a large market for absorbing deposits, such as exchanges, DeFi or stablecoins, and then a liquidity crisis occurs in a certain project, and finally all collapses.

However, this cycle is different. On the one hand, OTC funds have brought in 60 billion yuan of ETF funds, which has improved the previous US dollar interest rate cuts. The interest rate hike cycle will cause a "tidal" dollar shortage worldwide. Bitcoin has acted as a reservoir, which has appropriately alleviated this harm. Of course, the reservoir still has more than 10 times of expansion space.

Summary Point 1: Bitcoin has duality. Even if it is a real asset, it is also an encrypted asset.

This reservoir has two development paths in the future. One is to continue to increase the capacity of Bitcoin, and the other is to seek more ETF products, such as Ethereum.

On the other hand, Ethereum's pledge system has created an "local currency deflation-recirculation" mechanism in the market. With ETH as the denominated asset, even if the pledged issuance assets (LSDfi) and the re-pledged issuance assets (LRTfi) eventually collapse, the pledge income of ETH itself will not decrease. During the bull market, with the huge increase in usage, it is deflationary.

That is, if you go long on ETH, the income denominated in US dollars will increase, and if you go short on ETH, the income denominated in ETH will not decrease, provided that ETH can become the Phoenix of the crypto world like Bitcoin.

Summary Point 2: As long as you can cross the bull and bear markets, it is possible to make profits for both long and short positions, and make up for losses in the bear market in the bull market.

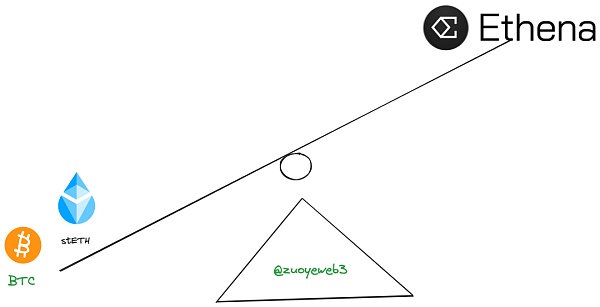

Now change the idea. If something is equal to the US dollar, that is, the US dollar is always priced at 1:1, and the gold and silver composite standard (BTC+ETH) is used as the issuance reserve, and it is seamlessly integrated with the exchange, then can USDe under this RWA model survive the bull and bear market?

Summary Point 3: Don't resist centralized exchanges, but use them as one of the sources of profit.

We cannot predict the future, we can only assume the future based on the past and give our own opinions. USDe is likely to collapse, but if the bull market is long enough, it may decline steadily and eventually disappear among the many currencies. If the price of ETH collapses sharply, then USDe will also collapse quickly.

Based on the above three points, let's use USDe to explain why this conclusion is reached.

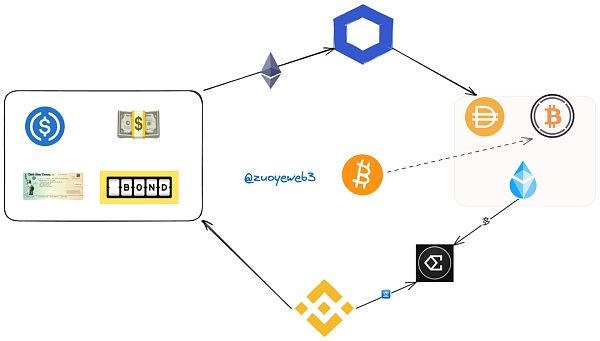

USDe issuance is linked to ETH's long and short orders. According to AC theory, spot trading is a perpetual contract with no leverage or 1x leverage. Buying is long and selling is short.

USDe's Delta neutrality can be understood in this way, that is, the collateral is stETH and BTC, etc., which is equivalent to buying long. At the same time, the corresponding short ratio is bought on the exchange, one positive and one negative. This is the so-called neutrality and risk hedging.

There are two benefits here. stETH comes with a 4% return. Secondly, shorting will receive a fee from the longs. The combination of the two means that during the bull market, the price of ETH will continue to rise, and the yield denominated in USDe will be ridiculously high.

Then the risk will follow. If the price of ETH falls, as mentioned above, the income denominated in USDe will not only disappear, but even the exchange will need to pay the long rate, and the assets will be insolvent and collapse instantly.

But the vitality here is that even if the price of ETH falls, the ETH-based income of stETH still exists. As long as it survives the bull market, ETH can still be sold for profit. People only need to firmly believe in this and not withdraw their funds.

During the bull market, everything is easy to say. For assets such as BTC/ETH, exchanges need short positions to maintain liquidity to a certain extent. In addition, they are already very skilled in unplugging network cables and plugging pins, so they don’t care much.

But as we can see, rather than saying that USDe is anchored to ETH derivatives for pricing, it is better to say that it relies on exchanges to operate. The exchange itself is a black box. This is not a problem that can be solved by accessing the oracle. What’s more, the USDe family members who feed themselves by the fee rate, I don’t know how the exchanges will respond.

USDe is really creative, I can’t help but write it in the middle of the article. Next is Ondo’s new business model and speculation about where MakerDAO’s DAI will go.

Among them, Ondo is actually more like tokenizing assets such as U.S. bonds, but it represents the characteristics of the comprehensive dollarization and "virtualization" of RWA-linked asset types, that is, physical assets such as real estate and other currencies are no longer the main direction in the future.

And MakerDAO represents the struggle of the on-chain protocol. MakerDAO's direct purchase of treasury bonds through proposals is still vivid in our minds. I didn't expect that the road of RWA is becoming more and more confused. Should it be on the chain, or the native assets off the chain, or combined, perhaps the idea still needs time to verify.

After discussing the BTC/ETH compound standard system, the entry of massive off-market funds is not all good news. The assets of asset management giants such as BlackRock and Franklin Templeton are more than ten times the market value of Bitcoin, but at least cooperating with them has the confidence and continuous ammunition support to resist SEC supervision. The trend of the three countries has been formed.

Traditional financial giants: opening up new battlefields, not only staying at the futures/spot ETF stage, but also hoping to enter the on-chain market and conduct more innovative combination experiments;

RWA project party: starting from the perspective of encryption, we hope to cooperate with traditional financial giants, with the goal of backdoor listing and compliance, becoming a mainstream financial investment option, rather than confronting regulators, or confrontation is a superficial gesture, the core is still to be appeased;

Regulatory authorities: try their best to block, and if they can't stop, they seek control. OFAC controls Ethereum nodes, SEC controls the definition of "securities", Congress and the Federal Reserve mainly focus on stablecoins and exchanges, and money laundering and illegal securities issuance are the most commonly used means.

From the perspective of Bitcoin and Ethereum, regulation has in fact been released, and the approval of the ETH spot ETF is only a matter of time. However, for smaller project parties, they do not have the ability to fight regulation alone. They have committed themselves to traditional financial giants and proactively carried out KYC/AML and other measures in the hope of reducing outsiders’ stereotypes of them as financial disruptors, and instead package themselves as innovators within the existing system.

Or it is difficult to involve real assets, the gravity of reality is too heavy. To put it simply and crudely, the route of RWA can be directly divided into three stages:

Eastern "chain reform craze", everything can be put on the chain, the main focus is traceability and recordability, such as Gongxinbao, but in the end it is a mess;

Western "tokenization", physical assets and virtual assets are tokenized and put on the chain, such as the real estate project RealT is the most typical, followed by Maple, Centrifuge and other lending products.

Then comes the current US dollar financial assets on the chain, and the integration and development of BTC/ETH's native assets and the existing financial system.

The above is my personal opinion. In the classification of RWA.XYZ, it is divided into four categories: lending, US debt, stablecoins and real estate. I still stick to my point of view. This round of RWA is only divided into US dollar-related assets on the chain, BTC/ETH off the chain, with stablecoins as the main issuance method and lending as a supplementary development path.

However, there will be three constraints, namely CeFi's control desire, CEX's evil impulse, and the big hand of supervision (SEC).

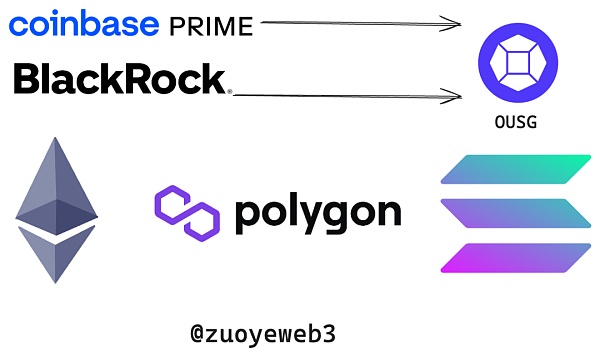

Take Ondo as an example. It has issued two main products, OUSG based on US debt and interest-bearing stablecoin USDY. In the future, the product types will be further updated. Their mechanism designs are relatively similar. They all work along the path of registered entities, four major audits, bank/institutional custody, and investment in US dollar assets. I will not go into details.

Take OUSG as an example. Its main asset composition is BlackRock's short-term treasury bond ETF products. However, Ondo has been deeply bound to BlackRock and will continue to promote cooperation with BlackRock's RWA product BUIDL, which is the most typical demonstration of two-way integration.

If we go one step further, we can directly help old money manage money. For example, Superstate, the founder of Compound, directly purchases US debt products and then issues them in token form. The process is of course boring. The core is that a group of Old Money has been born in the crypto world. They have gone through the Age of Discovery, which pursues high risks and high returns, and are ready to go ashore with the looted gold, silver and jewelry to live a peaceful life.

However, the continuous flow of living forces does not want to give up directly. For example, MakerDAO's DAI is ready to welcome the high returns of USDe. In the initial stage, 600 million DAI will be invested in it, and the maximum recharge can be up to 1 billion US dollars. Not only can DeFi nest dolls, but this stablecoin can also become the doll of another stablecoin. It must be noted that the essence of USDe is not the equivalent of the US dollar, but the volatility equivalent of ETH.

Faced with huge real assets, the crypto world is still a little immature. Compared with the asset management giants with trillions of dollars, the TVL of hundreds of millions and billions is simply not worth looking at. The more important question is whether we think RWA is an important asset form in the future, at least as mainstream as ETFs, or is it just a one-sided love in the crypto circle, and the tokens are fried after the good news, leaving a mess.

I basically just observed the RWA track and rarely participated in it.

JinseFinanceFrom the perspective of asset securitization, data assets are more of financial assets based on the income or cash flow brought by achieving this purpose.

JinseFinanceCompared with securities firms and investment banks in the traditional financial market, RWA, as the tokenization of real-world assets, is a sign of its mature development, with the emergence of professional and independent RWA crypto investment banks.

JinseFinanceWhat exactly is RWA (real world asset tokenization)? Is RWA a product or a transaction?

JinseFinanceWhen connecting crypto infrastructure to Offf Chain assets and their established regulatory framework, things can get very complicated. There are many obstacles, both technical and regulatory, that must be overcome to enable the flow of value.

JinseFinanceIt seems obvious that the real-world asset tokenization space has huge growth potential in the future. But what exactly is this trend, why is it attracting so much attention and hype, and how can you make the most of it?

JinseFinanceRWA, will RWA become the next hot spot? What are the projects worth paying attention to? Golden Finance, what is the next step for encrypting real-world assets?

JinseFinanceQuestions and answers about mocaverse, mutant ape, ORDI, SATS, ERC-3643

JinseFinanceJinseFinanceSustainability can be simply defined as the protocol staying online, resilient to attacks, and usable under all conditions. It also needs to be relevant and keep up with contemporary needs, so to speak.

Cointelegraph

Cointelegraph