Source: Liu Jiaolian

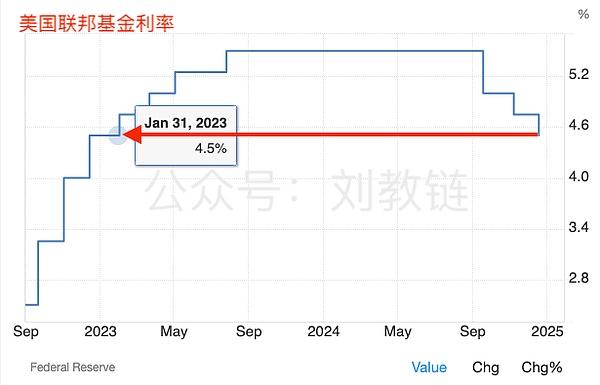

Overnight this morning, the Federal Reserve's December interest rate meeting ended as scheduled. The result was in line with market expectations, and the interest rate continued to be cut by 25bp. This result was beyond the expectations of some people who had previously speculated that the interest rate cut would be stopped. So far, since the second half of 2024, the Federal Reserve has cut interest rates three times, with a reduction of 100bp, or 1%, reducing the US federal interest rate from 5.5% to 4.5%.

This is back to the interest rate level at the beginning of 2023.

The interest rate cut has landed. The three major US stock indexes and the crypto market have all pulled back. Why? Because the expected interest rate cut has long been predicted by the market and overdrawn in advance. This has become a positive landing and a turn of events, the green mountains are still there, and the sunset is red several times.

Of course, the reason for the correction is related to the statement of the Fed Chairman that policy adjustments next year may be more cautious. After all, this is different from the radical expectations of some people in the market that interest rates will continue to be cut rapidly next year.

After all, in this Kondratieff depression period where radicalism is popular all over the world, being slightly less radical will be criticized as conservative. An incomplete interest rate cut is a complete non-interest rate cut.

If you stand in the middle as a moderate, you will be criticized by people standing on your right for being too left, and by people standing on your left for being too right. The so-called two sides are not people.

Why does Chinese philosophy like to talk about the doctrine of the mean? This is called making up for what is lacking. Chinese sages have long seen through that society is too easy to evolve into an "M-shaped" form, and people standing in the middle are the bravest. Without courage, you dare not stand in the middle. If you are not strong enough, you will be torn to pieces if you stand in the middle.

It is either black or white, either left or right, either heaven or hell, a thought can make you a Buddha, a thought can make you a ghost. Today is the blockchain revolution, tomorrow is the tulip scam.

It is easy to play tricks. It is difficult to be a big man floating between heaven and earth and standing tall. It is easy to blindly cater to the public sentiment of flattery or trampling. It is difficult to look at new things objectively and without prejudice and seize historical opportunities.

You don’t understand her goodness because you haven’t been with her. If you have been with her for a long time, you will know her goodness.

At the early morning press conference, Powell’s answer to reporters’ questions became popular.

The reporter asked about the US national BTC strategic reserve.

Powell replied: The Federal Reserve is not allowed to own Bitcoin. We are not seeking relevant legal changes.

What he said is indeed in line with the "current" status quo.

It’s just that this statement is more general, general and vague. We need to disassemble it carefully.

First, what is the nature of BTC in Powell's mind?

Looking back at the article "Bitcoin is back, breaking $100,000 for the first time" on December 5, 2024, Powell said publicly not long ago that in his opinion, BTC is more like gold. He said, "It is not a competitor to the US dollar, but a competitor to gold."

That is to say, he believes that BTC is a physical asset.

So, can the Federal Reserve directly "own" physical assets? Obviously not.

For example, gold. The US gold reserves are actually owned by the US Treasury. The real storage and custody are scattered in reserve warehouses across the United States (such as the Federal Reserve Bank of New York). According to the Gold Reserve Act of 1934, the Treasury Department issues gold certificates to record the value of the gold it owns. These gold certificates, issued by the U.S. Treasury, are the legal proof of the gold reserves.

Can the Fed own gold as a physical asset? No. The Fed can only own gold certificates as financial assets.

However, even to own gold certificates, it needs to act in accordance with the law. The key here is to legally include the value of financial assets in the Fed's balance sheet.

Under the Federal Reserve Act of 1913, the Fed can include gold certificates in its balance sheet as part of its reserve assets. Gold certificates are recorded in the Fed's balance sheet at a nominal value, representing the value of gold promised by the Treasury.

In accounting, the price of gold reserves is set by the International Monetary Fund Agreement Act of 1973, which is fixed at $42.22 per ounce of gold, not the market price. Regarding this pricing, Jiaolian discussed it in detail in the article 《How Much Gold Does the United States Hold?》 on November 14, 2023, so I will not repeat it here.

However, this pricing is not a set rule. For example, our central bank adjusts the pricing according to the market price.

Okay, after understanding this, we need to examine two questions in succession:

First, can the new US president authorize the Treasury Department to reserve BTC (bitcoin) and issue "bitcoin certificates" solely by presidential power?

Second, can the Federal Reserve, without revising the Federal Reserve Act of 1913, take the initiative to include "bitcoin certificates" in its balance sheet?

For the first question. John F. Kennedy, the 35th President of the United States, has already demonstrated this.

On June 4, 1963, President Kennedy signed an executive order, Executive Order 11110. The executive order authorized the US Treasury Department to issue "Silver Certificates" in the name of the Treasury Department based on the silver reserves owned by the Treasury Department in accordance with the Silver Purchase Act of 1920.

In essence, silver certificates are a form of US currency that can be exchanged for physical silver of equal value.

On November 22, 1963, President Kennedy was assassinated.

The voice of a female singer seemed to come from the radio:

"I want to ask if you dare / Love me like you said /

I want to ask if you dare / Love me like you said /

I want to ask if you dare / Love me like you said /

I want to ask if you dare / Love me like you said /

I want to ask if you dare / Crazy about love like me / What do you think of it?"

For the second question. The Federal Reserve has demonstrated it in person.

During the 2008 financial crisis, the Federal Reserve adopted a series of unconventional monetary policies, including purchasing MBS and other financial assets, to provide liquidity and support the US economy. This policy is called Quantitative Easing (QE).

Section 14, Section 2 of the Federal Reserve Act of 1913 provides that the Federal Reserve can purchase government bonds (such as U.S. Treasury bonds) to manage the money supply and stabilize the economy, but the Act does not explicitly authorize the Federal Reserve to purchase private assets that are not related to the government, such as mortgage-backed securities (MBS).

The core question is: Does the Federal Reserve's power belong to public power or private power?

After all, public power cannot be exercised without authorization by law. If the law does not explicitly stipulate that the Federal Reserve can personally purchase MBS, then its direct purchase of MBS is suspected of being illegal.

However, the Federal Reserve, as the central bank of the United States and even the central bank of the world, is a bug-like existence. The Federal Reserve is actually a private institution rather than a public sector. Private rights can be exercised if they are not prohibited by law.

So, this can be interpreted flexibly.

The usual explanation is this:

On the one hand, the Federal Reserve Act of 1913 does not explicitly prohibit the Federal Reserve from purchasing specific types of assets.

Secondly, the Fed found other laws to endorse its "emergency measures", including laws such as the Emergency Banking Act of 1932 and the Financial Stability Act of 2008. These laws authorize the Fed to adopt more unconventional monetary policies in specific emergency situations, and are considered to provide a legal basis for the Fed to purchase MBS during the crisis.

In short, in short, the Fed explained that the purchase of MBS was out of the need for monetary policy and financial stability, and was an emergency measure taken in response to the special circumstances of the financial crisis. Therefore, although these measures do not comply with the literal provisions of the Federal Reserve Act of 1913, the government has provided a legal basis for these measures through new authorizations.

In fact, courts at all levels in the United States have never explicitly ruled that these actions violate the Federal Reserve Act of 1913, but rather regarded them as emergency response measures.

Therefore, the conclusion is that, despite the legal gray area, this move is not considered a direct violation of the Federal Reserve Act of 1913.

The teaching chain has repeatedly mentioned that the Federal Reserve has been quietly replacing its "gray" MBS positions with legal US Treasury positions.

This shit has been wiped from 2008 to today.

So, even if it does not seek legal changes, the Federal Reserve can find a legal basis for what it does and does not do by flexibly interpreting the nature of its own power.

Finally, the teaching chain also needs to mention that the global central banks also have an international coordination organization called BIS (Bank for International Settlements). This is part of the international financial order after World War II.

The members of BIS are mainly composed of central banks around the world, and there are currently about 60 members. These members include central banks of important global economic countries, such as the Federal Reserve in the United States, the European Central Bank in Europe, and the People's Bank of China. It was founded in 1930 and is headquartered in Basel, Switzerland. It can be called a bank of central banks.

In 1974, the Bank for International Settlements (BIS) established the Basel Committee on Banking Supervision (BCBS) to develop regulatory standards and guidelines for the international banking industry.

The main function of the Basel Committee is to develop international standards related to bank capital adequacy, risk management, and bank supervision, especially regulations on capital adequacy ratios, liquidity requirements, risk-weighted assets, etc. It usually issues a series of regulatory standards and recommendations for reference and adoption by financial regulators around the world to ensure the health and stability of the banking system.

In 1988, the Basel Committee launched Basel I, which was the first standardization of global bank capital adequacy requirements.

In 2004, the Basel Committee issued Basel II, which is a further improvement and expansion of Basel I.

In 2010, after the global financial crisis, the Basel Committee launched Basel III, which is to improve the capital quality of banks and enhance the risk resistance of the banking system in crises.

It can be seen that BIS (Bank for International Settlements) and the Basel Committee play a vital role in global banking supervision. The Basel Committee was established through BIS and is responsible for formulating regulatory standards for the global banking industry, and the Basel Accords (I, II, III) are the specific embodiment of these standards.

Central banks around the world, including the Federal Reserve, usually need to formulate standards in the Basel framework through BIS if they want to include any assets in their balance sheets, that is, the so-called risk exposure to certain assets, and then the member central banks can act accordingly.

The Basel Accord is called an agreement rather than a law because it relies on the self-discipline of each member, rather than being enforced by violent agencies like the law.

Coincidentally, as early as December 2022, BIS issued a report, the main meaning of which is that central banks of various countries will be allowed to allocate no more than 2% of Bitcoin from 2025.

Cheng Yuan

Cheng Yuan