Technical interpretation: How does Merlin Chain work?

This article will focus on the Merlin Chain technical solution and interpret its publicly available documents and protocol design ideas.

JinseFinance

JinseFinance

Source: U.S. SEC official website Translation: Shan Ouba, Golden Finance

On Friday, August 23, local time, Federal Reserve Chairman Powell delivered a speech at the Jackson Hole Annual Meeting. As the global market was looking forward to the moment, the Federal Reserve Chairman publicly announced that the Federal Reserve has officially entered a rate cut cycle.

The following is the full text of the speech:

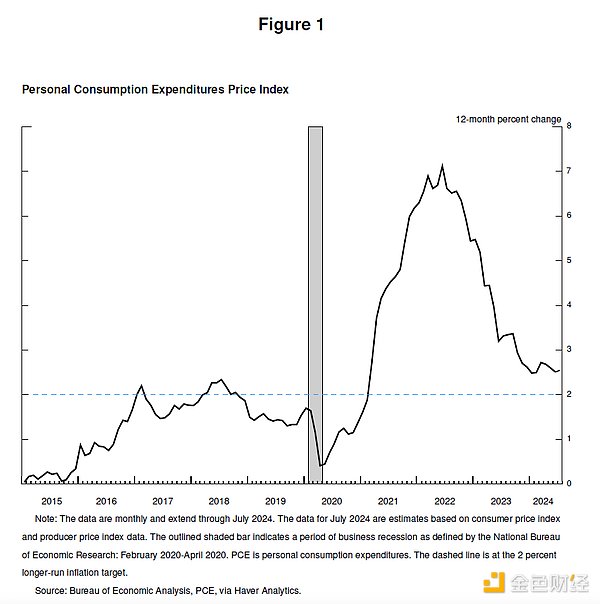

Today, four and a half years after the outbreak of the epidemic, the most serious economic distortions caused by the epidemic are fading. Inflation has fallen sharply. The labor market is no longer overheated, and conditions are now looser than before the epidemic. Supply constraints have normalized. The balance of risks facing our two major tasks has also changed. Our goal is to restore price stability while maintaining a strong labor market and avoiding a sharp rise in unemployment in the early deflationary period when inflation expectations are not stable. We have made great progress toward this goal. Although the task is not yet completed, we have made great progress toward this goal.

Today, I will begin by talking about the current economic situation and the future direction of monetary policy. I will then discuss economic events since the outbreak of the pandemic, exploring why inflation has risen to levels not seen in a generation and why inflation has fallen sharply while unemployment has remained low.

Let’s start with a look at the current situation and the near-term policy outlook.

For much of the past three years, inflation has been well above our 2 percent objective, and labor market conditions have been extremely tight. The Federal Open Market Committee’s (FOMC) primary focus has been, and rightly so, on reducing inflation. Prior to this episode, most Americans alive today had never experienced the pain of persistently high inflation. Inflation has caused tremendous hardship, particularly for those who have had the hardest time coping with the rising costs of life’s necessities, such as food, housing, and transportation. High inflation has induced stress and a sense of unfairness that persists to this day.

Our tight monetary policy has helped restore balance between aggregate supply and demand, eased inflationary pressures, and ensured that inflation expectations remain anchored. Inflation is now closer to our objective, with prices rising 2.5 percent over the past 12 months. After a pause earlier this year, progress toward our 2 percent objective has resumed. I am increasingly confident that inflation is on a sustainable path back to 2 percent.

Speaking of employment, in the years before the pandemic, we saw significant benefits to society from strong labor market conditions: low unemployment, high labor force participation, historically low racial employment gaps, and healthy real wage growth amid low and stable inflation, with these increases increasingly concentrated among low-income people.

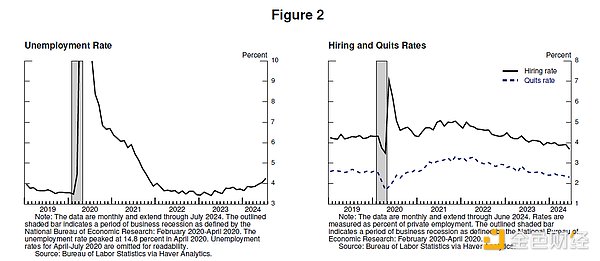

Today, the labor market has cooled significantly and is no longer as overheated as before. The unemployment rate began to rise more than a year ago and is now 4.3%, which, while still at a historical low, is nearly a percentage point higher than at the beginning of 2023. Most of the increase has occurred in the past six months.

So far, the rise in unemployment has not been due to the large-scale layoffs that are typically seen during a recession, but rather primarily reflects a significant increase in the supply of labor and a slowdown in the pace of hiring. Even so, a cooling in the labor market is still evident. Job growth remains solid but has slowed this year. Job openings have fallen, and the ratio of job openings to unemployment has returned to its pre-pandemic range. Hiring and quit rates are now below their levels in 2018 and 2019. Nominal wage growth has slowed. Overall, the labor market is much looser now than it was in 2019 (before the pandemic) - a year when inflation was below 2%. It seems unlikely that the labor market will become a source of inflationary pressures in the near term. We do not seek or welcome a further cooling in labor market conditions.

Overall, the economy is still growing at a solid pace. But inflation and labor market data suggest that the situation is evolving. Upside risks to inflation have diminished. Downside risks to employment have increased. As we emphasized in our last FOMC statement, we are focused on risks on both sides of our dual mandate.

Now is the time to adjust policy. The way forward is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.

We will do everything we can to support a strong labor market while continuing to move toward our price stability goal. With appropriate reductions in policy constraints, there is good reason to believe that the economy will return to inflation at a rate of 2 percent while maintaining a strong labor market. Our current level of the policy rate provides us with ample room to address any risks, including the risk of a further deterioration in labor market conditions.

Let us now turn to why inflation has risen, and why it has fallen significantly while unemployment has remained low. The literature on these questions is growing, and now is a good time to discuss them. Of course, it is too early to make a definitive assessment. This period will be analyzed and discussed for many years to come.

The arrival of the COVID-19 pandemic quickly shut down economies around the world. This was a period of uncertainty and serious downside risks. Americans, as they always do in times of crisis, adapted and innovated. The government response was unprecedented and powerful, especially in the United States, where Congress unanimously passed the CARES Act. At the Federal Reserve, we used our powers with unprecedented force to stabilize the financial system and help avoid a depression.

After a historically deep but short recession, the economy began to recover in mid-2020. As the risk of a deep, prolonged recession recedes and the economy reopens, we risk a repeat of the slow recovery that followed the global financial crisis.

Congress provided substantial additional fiscal support in late 2020 and early 2021. Spending recovered strongly in the first half of 2021. The ongoing pandemic shaped the pattern of the recovery. Persistent concerns about the pandemic weighed on consumption of in-person services. But pent-up demand, stimulus policies, pandemic-induced changes in work and leisure patterns, and additional savings from limited consumption of services combined to drive a historic surge in consumer spending on goods.

The pandemic also wreaked havoc on supply conditions. At the start of the pandemic, 8 million people dropped out of the labor force, and by early 2021 the size of the labor force was still 4 million smaller than before the pandemic. The size of the labor force did not return to its pre-pandemic trend until mid-2023. Supply chains were disrupted by worker displacement, disruptions to international trade links, and a dramatic shift in the structure and level of demand. Clearly, this is nothing like the slow recovery that followed the global financial crisis.

Inflation ensued. After running below target in 2020, inflation climbed sharply in March and April 2021. The initial surge in inflation was concentrated in goods in short supply, such as motor vehicles, where price increases were particularly large. My colleagues and I initially judged that these pandemic-related factors would not persist and therefore believed that the sudden increase in inflation would probably pass quickly and would not require monetary policy intervention—in short, that inflation was temporary. The long-standing standard view was that central banks could ignore temporary increases in inflation as long as inflation expectations remained anchored.

The idea of “temporary inflation” was widely accepted at the time, shared by most mainstream analysts and central bank governors in advanced economies. The general expectation was that supply conditions would improve relatively quickly, that the rapid recovery in demand would run its course, and that demand would shift from goods to services, reducing inflation.

For a while, the data were consistent with the assumption of temporary inflation. Monthly readings of core inflation declined each month from April to September 2021, albeit at a slower pace than expected. By mid-year, support for this assumption began to weaken, and our communications reflected this. Starting in October, it became clear that the data no longer supported the assumption of a temporary inflationary episode. Inflation rose and spread from goods to services. It became clear that high inflation was not a temporary phenomenon and that a strong policy response was needed if inflation expectations were to remain anchored. We recognized this and began adjusting policy in November. Financial conditions began to tighten. After winding down asset purchases, we initiated rate hikes in March 2022. By early 2022, headline inflation was above 6% and core inflation was above 5%. New supply shocks emerged. Russia’s invasion of Ukraine led to a sharp increase in energy and commodity prices. The improvement in supply conditions and the shift in demand from goods to services took longer than expected, in part because of the further development of the pandemic in the United States. The pandemic also continued to disrupt production in major economies around the world.

High inflation rates are a global phenomenon that reflects a shared experience: a rapid increase in demand for goods, tight supply chains, tight labor markets, and sharp increases in commodity prices. Inflation around the world is unlike any period since the 1970s. Back then, high inflation was entrenched—something we were deeply committed to avoiding.

By mid-2022, labor markets were extremely tight, with labor demand increasing by more than 6.5 million since mid-2021. This increase in labor demand is due in part to workers rejoining the labor force as health concerns begin to recede. But labor supply remains constrained, and by summer 2022 the labor force participation rate remained well below pre-pandemic levels. From March 2022 through the end of the year, job openings were nearly twice the number of unemployed people, indicating a severe labor shortage. Inflation peaks in June 2022 at 7.1%.

Two years ago from this podium, I discussed some of the pain that fighting inflation might bring, such as rising unemployment and slowing economic growth. Some have argued that a recession and prolonged high unemployment are needed to bring inflation under control. I expressed our unwavering commitment to restoring price stability across the board and to staying the course until that mission is accomplished.

The FOMC has not backed down, has steadfastly fulfilled our mandate, and our actions have powerfully demonstrated our commitment to restoring price stability. We have raised our policy rate by 425 basis points in 2022 and another 100 basis points in 2023. We have maintained our policy rate at its current tight level since July 2023.

The peak in inflation occurred in the summer of 2022. Inflation has fallen 4.5 percentage points from its peak in two years, all while unemployment has remained low, a welcome and historically unusual outcome.

Pandemic-related supply and demand distortions and severe shocks to energy and commodity markets were important drivers of high inflation, and their reversal was a key part of the decline in inflation. These factors took longer to unwind than expected, but ultimately played an important role in the subsequent decline in inflation. Our tight monetary policy has encouraged a modest decline in aggregate demand, which, combined with improvements in aggregate supply, has reduced inflationary pressures while allowing the economy to continue to grow at a healthy pace. As labor demand has slowed, the historically high level of job openings relative to unemployment has normalized, primarily through a decline in job openings without large and disruptive layoffs, making the labor market less of a source of inflationary pressure.

On the critical importance of inflation expectations. The long-standing view of standard economic models is that inflation will return to target as long as product and labor markets are balanced—without the need for an economic slowdown—as long as inflation expectations are anchored at our target. This is what the models say, but the stability of long-term inflation expectations has never been tested by persistently high inflation since the 2000s. Whether the inflation anchor will remain anchored is far from certain. Concerns about the decoupling of inflation expectations have fueled the view that lower inflation requires a slower economy, particularly in the labor market. The important lesson of recent experience is that well-anchored inflation expectations, combined with strong central bank action, can achieve lower inflation without requiring a slowdown.

This narrative attributes the cause of higher inflation primarily to the unusual collision between overheated and temporarily distorted demand and constrained supply. While researchers differ in their approaches and in their conclusions, a consensus appears to be emerging that I believe attributes the main cause of higher inflation to this collision. Overall, the combination of a recovery from the distortions of the pandemic, our efforts to moderately restrain aggregate demand, and the anchoring of expectations are putting inflation increasingly on a path that sustainably reaches our 2 percent objective.

Achieving lower inflation while maintaining a strong labor market is possible only if inflation expectations are anchored, reflecting public confidence that the central bank can achieve 2 percent inflation over time. That confidence has been built over decades and reinforced by our actions.

This is my assessment of events. You may see it differently.

In closing, I want to emphasize that the pandemic economy is proving to be unlike any previous period, and there is much to learn from this extraordinary period. Our Statement on Longer-Run Goals and Monetary Policy Strategy underscores our commitment to review our principles every five years through a comprehensive public review and to make appropriate adjustments. As we begin that process later this year, we will remain open to criticism and new ideas while preserving the strength of our framework. The limits of our knowledge—made apparent during the pandemic—require us to remain humble and skeptical, focused on learning lessons from the past, and nimbly applying them to current challenges.

This article will focus on the Merlin Chain technical solution and interpret its publicly available documents and protocol design ideas.

JinseFinanceFocus on the Merlin Chain technical solution and interpret its publicly available documents and protocol design ideas.

JinseFinanceBittensor has been one of the leading projects in the crypto + AI narrative. What does it do?

JinseFinanceThe Ethereum network has transitioned to proof-of-stake. Ethereum staking is a way ETH investors can earn a reward by locking up their coins.

Coindesk

CoindeskUsing the provably fair and verifiable random number generator provided by Chainlink VRF, smart contracts can access random values without compromising security or usability.

Cointelegraph

CointelegraphMetaPay, metaverse-based payment system, requires customers to have a MPay token to invest in the Metaxion universe.

CointelegraphAPE token holders make collective governance decisions, casting votes and deciding on issues such as fund allocation, rule framing, partnerships, project selection, and more.

CointelegraphSolana's ambition is to solve the blockchain trilemma; however, it still has various flaws, such as easy centralization, etc.

CointelegraphIn a cryptocurrency lending transaction, the borrower and the lender are two distinct roles. Borrowers provide cryptocurrencies as collateral to obtain loans from lenders.

CointelegraphThe borrower and the lender are two distinct actors in the crypto lending transaction. Borrowers put up cryptocurrency as collateral to secure a loan from a lender.

Cointelegraph