马斯克到底想要什么

马斯克是如何演变的:他如何从一个关注气候变化、想去火星的奥巴马时代传统自由主义者,变成一个右翼阴谋论传播者,一个积极为德国极右助选,并瓦解美国联邦政府的人?

JinseFinance

JinseFinance

Capital inflows remain weak, making it difficult to offset the market pressure of long-term selling. It remains to be seen whether, with interest rate cuts and the easing of the US-China trade conflict, capital inflows can return to ample levels, reverse the downward trend, or even rewrite the old cyclical pattern.

Two weeks ago, the US-China tariff war suddenly escalated, triggering renewed turbulence in global financial markets. Afterward, both sides, especially the US, continued to send signals of goodwill and eagerness to reach an agreement. The market gradually interpreted this as a "fight to promote talks" strategy, and the market subsequently stabilized. Over the weekend, delegations from both sides held their fifth round of talks in Malaysia. According to announcements from both sides on Sunday, over the two days, the two sides "held constructive discussions" and "reached preliminary consensus" on topics including export controls, reciprocal tariff extensions, fentanyl and drug control cooperation, further expanding trade, and measures related to Section 301 "shipping charges." The two sides will then proceed with internal approval procedures. The meeting between the leaders of the two countries at the end of the month is likely to take place as scheduled. Since the US government shutdown, the market has been struggling with a lack of economic and employment data. Finally, on October 24th, the first key data release—the Consumer Price Index—was released. The data showed a 3% year-on-year increase in the US CPI for September, below the 3.1% estimate and up from the previous reading of 2.9%. This means the Federal Reserve's October rate cut is nearly 100% certain, and expectations for a December rate cut on FedWatch have reached 91.1%. The continuation of the rate-cutting cycle has alleviated previous market concerns, and all three major stock indices hit record highs following the data release. Bitcoin also continued its weak rebound, but remains a long way from its all-time high. The US government shutdown has caused short-term liquidity problems. With Powell's statement that "the Fed will soon stop QT," the market's pressure has begun to ease. U.S. stocks AI and technology stocks have begun to release Q3 earnings reports. Tesla's earnings report fell short of expectations but still closed higher, indicating that the market is still optimistic about AI spending. Several leading companies will continue to release earnings reports next week, so keep a close eye on them. The US dollar index rebounded 0.39% this week, closing at 98.547, in a moderate state. After several weeks of short squeezes and rises, gold began to fall violently on Tuesday and has been in a weak state since then.

Crypto Market

In addition to the impact of the macro-financial market,

BTC and the crypto market are still subject to the influence of historical "cyclical laws."This week, exchanges still recorded an inflow of more than

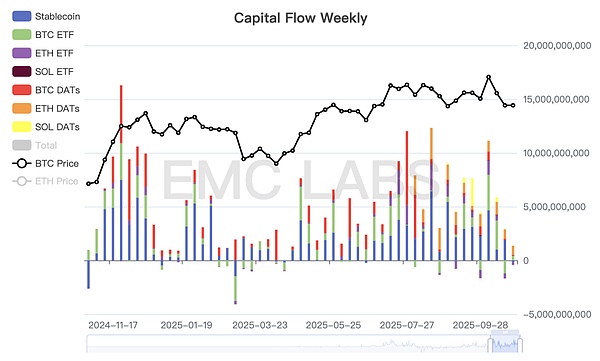

130,000 BTC, a slight decrease from last week, but the net outflow shrank to 2,775 coins, the lowest in recent times. This demonstrates that the transition between old and new cycles significantly impacts the market. Long-term investors reduced their holdings by over 39,000 tokens. This sustained sell-off during a decline often occurs during the confirmation phase of a bull market transition to a bear market. At this point, the buying power of short-term investors is insufficient to absorb the selling pressure. In the new market structure, the main drivers of selling pressure, DATs and BTC Spot ETF channel funds, also performed weakly this week. According to eMerge Engine statistics, total inflows into the crypto market this week were only 943 million, the lowest in several months.

Weekly Statistics of Crypto Market Capital Inflows

The weak trading performance is driven by the "cyclical law" that we have recently emphasized, which suppresses market sentiment. A change in this state will either require bullish forces within the new structure to actively go long and absorb selling pressure amid rising global risk appetite, or a relentless sell-off by long and short positions to confirm a bear market. Technically, BTC stabilized above its 200-day moving average and the "Trump bottom" (between $90,000 and $110,000) this week and continued its weak rebound, achieving a 5.4% weekly gain. ETH, on the other hand, stabilized above its 120-day moving average. BTC Price Daily Chart: The continued liquidation of the contract market following the resurgence of US-China conflict has resulted in a loss of over US$20 billion in notional value. Recently, BTC has rebounded alongside the weakness of US stocks, but the total amount of open interest remains low, indicating that leveraged funds are unlikely to become a key driver of the rebound in the short term. Based on a multi-dimensional analysis, we believe that the behavior of DATs and BTC Spot ETF channel funds in the future market will remain the only two forces maintaining BTC's rebound and even returning to a bull market. Cycle Metrics According to eMerge Engine, the EMC BTC Cycle Metrics indicator is 0, indicating that it is in a transition period.

马斯克是如何演变的:他如何从一个关注气候变化、想去火星的奥巴马时代传统自由主义者,变成一个右翼阴谋论传播者,一个积极为德国极右助选,并瓦解美国联邦政府的人?

JinseFinanceThe U.S. Securities and Exchange Commission (SEC) has sued Elon Musk, saying the world's richest man failed to disclose that he acquired "beneficial ownership" of Twitter in early 2022 so he could buy shares at a lower price.

JinseFinanceThe Tesla CEO’s influence over Donald Trump prompted ChatGPT developers to court the incoming administration.

JinseFinanceDurov is waging a full-scale war against all the capital and officials in this world. He doesn't care about the Russian government, the American government, Russian capital, or Western capital.

JinseFinanceElon Musk confirmed at a recent press conference that Tesla will soon enable Dogecoin payments, stating that DOGE will soon become one of the official payment methods for purchasing Teslas. But he did not specify when the payment method is expected to be enabled.

JinseFinanceThere was a discussion on X about whether Musk had started to increase his position in Bitcoin.

JinseFinanceWe look forward to actively embracing Meme culture Musk and promoting the birth of more million-fold Meme coins in this bull market.

JinseFinanceBut Musk's attitude towards Bitcoin has not always been so clear and positive. He once held different views on Bitcoin, and sometimes there were even reversals and contradictions.

JinseFinanceJinseFinanceThe world's richest man and Dogecoin's co-founder is debating whether Dogecoin actually has a Python script that can drastically cripple Twitter bot activity.

Cointelegraph

Cointelegraph