Author: Huang Guoping, Director of the National Finance and Development Laboratory, Science and Technology Finance and Development Research Center

Abstract:The stability and regulation mechanism of stablecoins is a core issue in the field of cryptocurrency, aiming to solve the problem of price fluctuations of digital currencies and enable them to have the functions of value scale and transaction medium. The essence is to seek a balance in the "triangle paradox" of asset efficiency, value stability and decentralization. Based on the analysis of the stability and regulation mechanisms of centralized stablecoins, decentralized stablecoins and hybrid stablecoins, this paper discusses the symbiotic development of stablecoins and decentralized finance, the mutual construction and institutional evolution of stablecoins and RWA mechanisms, and the improvement of the stablecoin ecosystem and the expansion of scenarios. The development of stablecoins has important implications and reference significance for the reconstruction and improvement of my country's digital RMB ecosystem, and provides a new path and direction for the internationalization of RMB.

Stablecoin's stabilization mechanism, application scenarios and policy implications

Introduction

Stablecoin is a cryptocurrency asset that is anchored to a specific value target (for example, legal currency, commodities or algorithmic mechanisms). Since Tether issued the world's first stablecoin USDT in 2014, by 2024, the global supply of mainstream stablecoins has reached a total of US$203.8 billion, an increase of more than 22 times compared with 2019. Stablecoins were originally designed to minimize price fluctuations by anchoring to specific assets (e.g., fiat currencies) or mechanisms, provide a reliable value scale and transaction medium for the crypto ecosystem, and solve the payment, settlement, and value storage problems caused by the high volatility of traditional cryptocurrencies (e.g., Bitcoin). With the expansion of the stablecoin market and the innovation of business models, its role and function as a bridge between decentralized finance (DeFi) and traditional finance, and promoting the integrated development of the real economy and the crypto economy, have become increasingly prominent. The rise of stablecoins is a key node in the digital transformation of the global monetary system, reflecting the structural game between the sovereign credit guarantee model and the technology-driven trust mechanism. However, the private issuance model of stablecoins has long been in a regulatory vacuum, forming an unbalanced state of "algorithmic trust first, institutional norms lagging behind." The collapse of UST in 2022 and the USDC de-anchoring crisis in 2023 exposed the systemic defects of pure mathematical models and centralized custody, prompting the regulatory framework to shift from passive response to active construction. The Guiding and Establishing National Innovation for US Stablecoins Act (hereinafter referred to as the "GENIUS Act") passed by the US Senate converts stablecoins into fiscal tools by forcing full (100%) US debt/cash reserves, building a "US dollar-US debt-stablecoin" closed loop to continue to promote US dollar hegemony. The Stablecoin Ordinance issued by Hong Kong, China explores regional financial autonomy with multi-currency anchoring (especially offshore RMB) and penetrating supervision, emphasizing the bottom line principles of full reserve reserves and mandatory redemption.

The emergence of stablecoins marks a paradigm shift in the form of currency in the digital age, and is a reconstruction of the financial order under the collision of sovereign credit dilution and technological empowerment. Digital currency brings profound changes to the modern payment system and can improve the reliability and efficiency of currency transactions, but it still belongs to the category of credit currency in essence.

From the practice of digital currency development and the current situation where national monetary sovereignty is unshakable, as long as there are sovereign states in the world and as long as sovereign states need to use sovereign currencies as a handle to regulate the economy, then any form of private currency can only be a token. Therefore, the government (monetary authorities) should strictly regulate the application and development of private digital currencies, including stablecoins, within a local scope. However, stablecoins pegged to legal tender (for example, USDT, USDC) may become the main form of currency compatible with national monetary sovereignty and market-oriented mechanisms in the digital age, both in theory and in practice.

The

State

Theory

ofMoneyTheory

ofMoneyTheory

ofMoneyTheory

ofMoney

Theory

ofMoney

Theory

ofMoney

Theory

ofMoney

Theory

Whether stablecoins can become the consensus currency for coordinating monetary sovereignty and private competition in the digital era and realizing the integration and development of the real economy and the crypto-token economy depends on the value stability of stablecoins. For example, USDT is issued by pegging the US dollar. Through the market arbitrage mechanism, the USDT price fluctuates around the 1-dollar anchor price and follows the principle of buying low and selling high to ensure currency stability. At present, the global economy is in a turbulent period, and investors and the market prefer stablecoins with relatively stable values. From the perspective of portfolio diversification and risk-return trade-off, stablecoins are even more competitive than the US dollar. Compared with other crypto assets, dollar-pegged stablecoins and gold-pegged stablecoins have lower volatility and higher returns, which are conducive to asset preservation and appreciation. Do stablecoins have real value stability? Existing research has not yet reached a consensus. In practice, the stability of stablecoins depends on the transparency and quality of collateral and external mandatory supervision and auditing. Some scholars have dynamically monitored the deviation of USDT price from the pegged USD and its stability, and concluded that USDT usually remains relatively stable and predictable. Some studies have also found that the volatility of stablecoins is statistically unstable, and the volatility of Bitcoin is one of the basic factors driving the volatility of stablecoins. This paper attempts to study the stability mechanism of stablecoins from the perspectives of value anchoring, regulatory mechanism and regulatory governance, and on this basis analyzes and discusses the application scenarios of stablecoins, and puts forward policy implications.

Main types and stability mechanisms of stablecoins

The anchoring mechanism and theory of stablecoins are core issues in the field of cryptocurrency, aiming to solve the problem of price volatility of digital currencies and enable them to have value scale and transaction medium functions. Due to the different issuance modes and value anchoring of different stablecoins, their value stability, regulatory mechanism and scenario application are also different. This paper selects the most representative currencies among the main types of stablecoins to analyze and study their stability mechanisms.

The value stability of stablecoins is determined by their linked assets and stabilization mechanisms. From the perspective of issuance mode, stablecoins are divided into centralized mode stablecoins, decentralized mode stablecoins, and stablecoins compatible with centralized and decentralized modes. Centralized mode stablecoins are issued by a single institution (for example, Tether, Circle). The core feature is that they rely on legal currency or commodity assets with a 1:1 full reserve, and ensure value stability through bank custody and regular audits. Centralized mode stablecoins (for example, USDT, USDC, PAXG) have strong compliance and high circulation efficiency, and are essentially an on-chain extension of the traditional financial system. The advancement of the US "GENIUS Act" has further strengthened the regulatory framework of centralized stablecoins, forcing issuers to divest non-reserve assets. Decentralized stablecoins are governed by decentralized autonomous organizations (DAOs) and driven by smart contracts (e.g., MakerDAO, Liquity), and are anchored by over-collateralized crypto assets (e.g., ETH, BTC) or algorithmic mechanisms. The typical characteristics of decentralized issuance models (e.g., DAI, LUSD) are censorship resistance and on-chain autonomy, and users have full control over asset keys, which is in line with the native values of Web3. Hybrid stablecoins (e.g., USDi, USD1) attempt to integrate centralized reserves and decentralized governance, with the key feature being a "dual-track architecture". Some assets are managed by licensed institutions (e.g., 80% of U.S. Treasuries), and some assets are managed on-chain through smart contracts (e.g., 20% of crypto asset collateral), and dynamic algorithms are introduced to adjust the reserve ratio. The hybrid model combines compliance foundation with flexible innovation, aiming to balance regulatory requirements and user sovereignty. However, this model faces the risk of governance division, and institutional decisions and community voting may conflict (for example, Aave's GHO interest rate dispute). In 2025, new projects such as USD1 are exploring a hybrid framework backed by the central bank, indicating that this model may become a key carrier of the game between regulation and innovation. According to the value anchoring mechanism (pegged assets), stablecoins are divided into fiat-collateralized stablecoins (for example, USDT, USDC), crypto asset (currency) collateralized stablecoins (for example, DAI), algorithmic stablecoins, and commodity-collateralized stablecoins (for example, PAXG). Fiat-collateralized stablecoins are pegged one-to-one with legal tender, and are exchanged by centralized issuing institutions. The issuer holds sufficient legal tender (for example, US dollars) or low-risk assets such as short-term government bonds as reserves. Crypto-asset collateralized stablecoins are decentralized and issued with smart contract technology. They are over-collateralized with a basket of mainstream crypto assets/currencies (e.g., Bitcoin, Ethereum) through margin to achieve a 1:1 anchor with legal tender. Algorithmic stablecoins (e.g., UST) are not backed by reserve funds or collateral. They use advanced algorithms to automatically adjust the dynamic balance mechanism of supply and demand to achieve a one-to-one peg between stablecoins and legal tender. Commodity stablecoins are backed by physical commodities (e.g., gold), and the value anchoring usually adopts a 1 token equals 1 unit of the pegged commodity mechanism. Cryptocurrencies, including stablecoins, are designed to overcome the various problems and contradictions caused by the over-centralized model of the traditional monetary and financial system. For example, in the "center-periphery" structure dominated by the US dollar, countries such as the United States, which are in the position of monetary center, exercise monetary hegemony without restraint, which harms the interests of developing countries and emerging market countries. Digital currencies, including private digital currencies and legal digital currencies, can circumvent the drawbacks of the unipolar world currency structure in terms of technology and concept, and help slow down the unbalanced development of the current international financial and monetary system. Stablecoins strive to achieve decentralization of governance and operators while maintaining value stability, thereby improving market transactions and capital efficiency. However, under the current economic, social and technological development conditions, stablecoins have the "Impossible Trinity" that value stability, decentralization and market efficiency cannot be achieved at the same time. At present, various types of stablecoins make appropriate trade-offs based on their own market positioning and application scenarios. For example, USDC sacrifices decentralization and strives to maintain price stability and high market efficiency; DAI sacrifices capital efficiency (high collateral ratio) and maintains price stability through decentralized operation and governance; UST attempts to improve market efficiency through a dual-currency mechanism on the basis of maintaining decentralized governance, which ultimately leads to a collapse.

The core challenge of stablecoin value anchoring is trust, not technical factors. Fiat-collateralized stablecoins rely on legal and audit trust, crypto-collateralized stablecoins rely on mechanism design and market depth, and algorithmic stablecoins rely on group psychology and unlimited growth expectations. At present, the development of stablecoins is evolving along the path of "transparent reserves + strong liquidity + progressive decentralization". As the compliance supervision of stablecoins continues to strengthen and the scenario ecology continues to improve and enrich, emerging forces driven by compliance and scenarios (for example, USD1, PYUSD, USDS) are emerging. The development of stablecoins has shifted from "scale expansion" to "scenario penetration". Future market competition will focus on compliance (for example, low-collateralization lending) and deep binding with the real economy through tokenization of real-world assets (RWA). See Table 1 for stablecoin issuance models and value anchoring.

Table 1 List of stablecoin issuance models and value anchors

Source: The author compiled based on public information.

The stablecoin market has formed a development pattern dominated by the two giants USDT and USDC, with multiple types of stablecoins coexisting, and the head effect is significant.The stability of stablecoins essentially depends on the synergy of the value anchoring mechanism and the dynamic regulation system.Fiat currency reserve stablecoins achieve value mapping through 1:1 full collateralization, and their stability depends on the liquidity and credit risk of reserve assets; crypto asset collateralized stablecoins rely on excess collateralization ratios (usually >110%) to build a safety buffer, and respond to the volatility of collateralized assets through price oracles and liquidation algorithms, but there is an inherent contradiction between capital efficiency and volatility transmission. Algorithm-regulated stablecoins maintain supply and demand balance through supply and demand functions (e.g., minting/destruction mechanisms, interest rate adjustments), but pure algorithmic models that lack value support are prone to death spirals due to reflexive expectations. The hybrid model combines the stability of fiat currency reserves with the profitability of on-chain assets, and introduces a dynamic rebalancing algorithm (e.g., the reserve ratio automatically adjusts with volatility) to achieve robust anchoring in multi-layer risk hedging. The core challenge of all mechanisms lies in how to design a negative feedback loop that is resistant to exogenous shocks, ensuring that price deviations trigger arbitrage forces rather than positive feedback runaway. In essence, the stability and regulation of stablecoins aims to achieve a balance from the "triangle paradox" of asset efficiency, value stability, and decentralization. Therefore, this article analyzes the stability and regulation mechanisms of centralized model stablecoins, decentralized model stablecoins, and hybrid model stablecoins.

1.Stability and Regulation Mechanism of Centralized Stablecoins

The centralized issuance characteristics of stablecoins are mainly reflected in the centralization of the issuing entity (the issuance right is controlled by a single entity), the reliance on central institutions for asset custody (for example, financial institutions, traditional vaults), and the centralization of the redemption mechanism (user redemption needs to be applied for by the issuer). At present, fiat-collateralized stablecoins and commodity-collateralized stablecoins mostly adopt a centralized issuance and governance model. Among them,

USDT and USDC issuance transaction scale accounts for more than 80% of the entire stablecoin market share.

The stability and regulation mechanism of the centralized issuance model stablecoin is essentially a combination of traditional financial credit and institutional constraints. It maintains value stability through a three-fold framework of strict reserve management, legal compliance, and market regulation. In terms of asset reserves, full and high liquidity methods are adopted, anchor assets and reserve assets are strictly consistent, and business and operational audits are strict and transparent. For example, the reserve assets of legal currency stablecoins are usually composed of cash and cash equivalents (short-term government bonds, commercial bills) to ensure high liquidity. In terms of legal supervision, a strict implementation of an institutionalized risk control system is implemented to meet the regulatory requirements of the government and regulatory authorities. For example, redemption guarantees require unconditional redemption at par, and reserve assets are independently deposited by licensed custodians and separated from the issuer's balance sheet. In terms of market regulation, follow the arbitrage balance mechanism and strengthen liquidity management. For example, when the market price of a stablecoin is greater than the anchor price (for example, $1), institutions issue more stablecoins, sell them for profit, and the price falls. When the market price is less than the anchor price, institutions buy stablecoins to redeem fiat currency for profit, and the price rises. In terms of liquidity management, automatic redemption circuit breakers are usually adopted. For example, when the daily redemption volume exceeds the threshold (for example, USDC is set at 1 billion US dollars), the service will be suspended to prevent the depletion of reserves.

Although the centralized model has a strict mechanism, there are still systemic risks. For example, the bankruptcy of the asset custodian leads to the freezing of reserve assets (cash), the single-point intervention of the regulator reduces the "anti-censorship" commitment, and the suspicion of black box operation of the issuing institution raises doubts about the repayment ability. In order to enhance trust and make up for the shortcomings, the centralized model stablecoin improves the shortcomings and defects of its own mechanism by introducing the concept and means of the decentralized model. For example, USDC deploys a reserve proof contract on Arbitrum, which makes the position address public in real time, facilitating on-chain reserve verification. The stability and regulation mechanism of centralized stablecoins is a correction of technical defects by institutional trust. It relies on legal reserves (e.g., legal currency, treasury bonds) and regulatory frameworks to strengthen value anchoring in volatile markets. Its future development tends to be technical enhancement within the compliance framework. The stability and regulation mechanism of typical centralized stablecoins is shown in Table 2.

Table 2 Stability and Regulation Mechanism of Typical Centralized Stablecoins

Source: The author compiled based on public information.

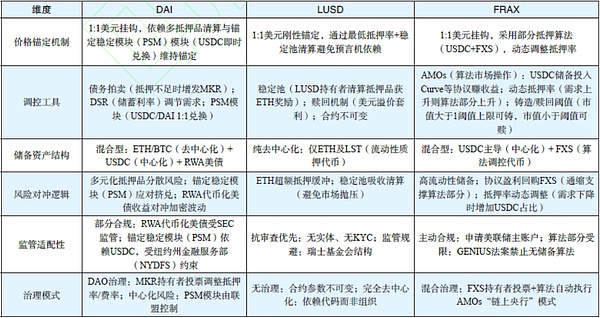

2.The stability and regulation mechanism of the decentralized stablecoin

The stability and regulation mechanism of the decentralized issuance model stablecoin is the core experiment of the DeFi paradigm. Its essence is to reconstruct the underlying logic of traditional currency, financial regulation and governance through the three-dimensional architecture of algorithmic autonomy, incentive game and on-chain governance. The decentralized issuance and regulation mechanism of stablecoins deeply reflects the typical characteristics of decentralized finance, namely composability (no permission to interact between protocols), anti-censorship (no centralized shutdown of nodes) and transparency (all rules are coded on the chain). Its stability mechanism contains three dimensions of dynamic balance.

First, adopt an over-collateralized capital buffer and risk control mechanism in the dimension of algorithmic autonomy. Compared with the centralized model of centralized issuance and governance by institutions, the core governance method of the decentralized model is algorithmic autonomy, and the composability of automated interactions between algorithmic protocols plays a key role. Users pledge volatile crypto assets (for example, ETH, BTC) to generate stablecoins, and smart contracts calculate the collateralization rate in real time (usually ≥150%). When market fluctuations cause the collateralization rate to fall below the liquidation threshold, it will trigger a liquidation closed loop on the entire chain, and the liquidator will bid for the assets through a combination of arbitrage strategies, and the remaining value after repaying the debt will be returned to the borrower, and the fine will be injected into the system insurance fund. The decentralized algorithmic autonomy and liquidation process is built in a building block-like manner based on the composability of the algorithm. The oracle network (e.g., Chainlink) provides price feeds, decentralized exchanges (e.g., Uniswap) provide liquidity depth, and lending protocols (e.g., Aave) undertake liquidation assets to achieve efficient redistribution of risks in an open ecosystem.

Second, dual-token game and algorithmic reflection regulation are adopted in the incentive mechanism and regulation dimensions. The price stabilization mechanism of the decentralized model stablecoin is rooted in the core of the DeFi arbitrage game. Taking DAI in the MakerDAO ecosystem as an example, the stablecoin DAI and the governance token MKR constitute an arbitrage equilibrium system. When the market price of DAI is greater than the anchor price, arbitrageurs destroy MKR to cast DAI and sell it for profit, increasing supply and depressing prices; when the market price is less than the anchor price, arbitrageurs destroy DAI to redeem MKR and buy DAI, and demand drives up prices. The arbitrage process relies on the free arbitrage mechanism of DeFi without permission, and the algorithm further strengthens the reflexive regulation, that is, the stablecoin collateral rate dynamically floats with price deviation. This move exposes the inherent systemic fragility of the decentralized model. For example, the algorithmic stablecoin UST in the Terra ecosystem depegged, causing the governance token LUNA to return to zero, and the arbitrage incentive reversal formed a death spiral. At this time, the protocol needs to be shut down (Emergency Shutdown) and the remaining assets are distributed according to the collateral ratio.

Third, in the on-chain governance and execution dimensions, follow the DAO macro constraints and progressive centralization compromise. The long-term regulation of decentralized stablecoins relies on the on-chain governance model. For example, in the MakerDAO ecosystem, the MKR holders of the governance tokens adjust key parameters such as the stability rate and collateral type through voting, and the governance proposal and execution process are all publicly available on the chain. Under the current technological, economic and social development conditions, the purely decentralized model faces real difficulties, forcing its governance paradigm to take certain centralized measures to overcome them. For example, in 2020, the 50% plunge of ETH triggered a liquidation crisis, forcing MakerDAO to introduce the centralized asset USDC as collateral; in 2023, MakerDAO will further increase tokenized U.S. Treasury bonds as asset reserves, which is essentially using traditional financial credit to make up for algorithmic defects. The gradual centralization of on-chain governance reveals the deep contradiction of DeFi, that is, the ideal of anti-censorship and the need for robustness cannot be achieved at the same time. Tokenized governance may complicate the problem. The holders of governance tokens have the motivation to improve system security and protect their own rights and interests, but they will also plunder value by reducing the collateral rate to induce malicious proposals such as liquidation.

The regulatory mechanism of decentralized stablecoins is a precise coupling of algorithms, economic incentives and human collaboration, which has the advantages of anti-censorship, no single point of failure, and high capital efficiency, but there are also black box and instability risks caused by complexity. In the future, the decentralized model may move towards a limited centralized hybrid architecture, that is, introducing traditional credit anchors (for example, U.S. Treasury bonds) through RWA tokenization, supplemented by DAO governance constraints. See Table 3 for the stability and regulatory mechanism of typical decentralized stablecoins.

Table 3 Stability and regulation mechanism of typical decentralized stablecoins

Source: The author compiled based on public information.

3.The stability and regulation mechanism of hybrid mode stablecoin

The hybrid issuance mode of stablecoins marks that the global monetary system has entered a new stage of integration of traditional credit and algorithmic trust. The essence is to reconstruct the underlying logic of value stability through layered architecture, dynamic algorithms and dual-track governance. The hybrid model is not a pure technological utopia, nor is it a simple digitization of traditional finance, but an institutional innovation that seeks dynamic equilibrium in the "impossible triangle" of efficiency, stability and decentralization.

First, the core stability mechanism of the hybrid model comes from layered reserves. The underlying core reserve assets are composed of fiat currency orRWA, which constitutes a centralized credit anchor (usually accounting for 50%-80%). The core reserve assets are managed by licensed custodians and use zero-knowledge proofs to achieve on-chain verifiable transparency to ensure the rigidity of the underlying value. The top-level risk assets are composed of volatile crypto assets (for example, ETH, BTC) as a decentralized buffer layer, and a risk absorption barrier is formed through the execution of over-collateralization by smart contracts (the collateral rate is usually 150%-200%) and the Dutch auction liquidation mechanism. The layered reserves constitute a "double firewall", using the centralized model of the bottom layer to resist systemic runs, and the decentralized model of the top layer to absorb short-term market fluctuations.

Second, the hybrid mode regulation logic relies on the dynamic algorithm reflection mechanism. When price fluctuations are in the normal range, for example, the price deviates from the anchor value by less than 3%, it relies on arbitrage games, destroys governance tokens, issues additional stablecoins, or reverses operations to maintain price equilibrium. When price fluctuations exceed the threshold, the algorithm will automatically trigger parameter adjustments. For example, when the volatility of collateral exceeds 80%, a 5% risk premium will be added to suppress leverage. When encountering a sudden "black swan" event, a cross-layer circuit breaker will be activated, and legal currency reserves will be used to redeem redemption requests first. At the same time, the crypto asset layer will enter the sub-pool liquidation to avoid cross-infection.

Third, the hybrid model governance structure reflects a profound compromise. Legal entities control RWA tokenized access and bank channels and other compliance nodes. DAO adjusts interest rates and liquidation rules through governance token voting. The two are interlocked and checked by veto power. Under the current technological, regulatory and governance environment, the inherent contradictions and paradoxes of the hybrid model itself rely on centralized credit endorsement to obtain stability, such as the ultimate repayment commitment of U.S. debt. At the same time, maintaining a decentralized module to practice the concept of anti-censorship makes user funds naturally flow to the low-risk layer (through buying and selling RWA), and the high-risk layer becomes a speculative configuration. The essence of the hybrid model stablecoin is the product of the compromise between the contradiction and conflict between the traditional financial order and the encryption ideal. It guarantees the bottom line of repayment through legal entities, optimizes resource allocation with code, and achieves a fragile balance between sovereign control and financial freedom. The DAO community adheres to the concept of decentralization in the erosion of centralization. In the future, if the hybrid model stablecoin can break through the shackles of the "trilemma" of stability, efficiency and decentralization, it may give birth to the ultimate evolution of the currency form. That is, the central bank digital currency (CBDC) serves as the "skeleton" to provide sovereign credit support; stablecoins serve as the "nerves" to achieve efficiency and innovation; and RWA serves as the "blood" to connect real value. This may determine whether humans can find the third way of currency in the tearing between algorithms and sovereignty, freedom and stability, and global and local. See Table 4 for the stabilization and regulation mechanism of typical hybrid stablecoins.

Table 4 Table of stabilization and regulation mechanism of typical hybrid stablecoins

Source: The author compiled based on public information.

Stablecoins andDeFi's synergistic and symbiotic development

Stablecoins andDeFi have a profound synergistic and symbiotic relationship, and together they form a crypto-financial system that is both innovative and fragile. As the basic liquidity layer and price stabilization mechanism of the DeFi system, stablecoins solve the core defects of the drastic price fluctuations in the crypto-asset market and the decentralized financial system by providing low-volatility asset anchoring, laying a feasible foundation for the core functions of decentralized lending, trading, derivatives, and payments. At the same time, DeFi reshapes the stablecoin stability and regulation mechanism through the innovation of the clearing mechanism, the expansion of the income and credit model, and the coordination of governance and liquidity, and promotes the coordinated evolution of stablecoins and DeFi beyond the "tool-scenario" symbiotic relationship to the "liquidity-protocol-income" trinity economy.

Stablecoins as the core infrastructure of the DeFi ecosystem promote the formation of a deep mutual relationship between the two through the triple functional coupling mechanism of liquidity base, value scale and risk buffer. The functional coupling of the two is not only reflected in the seamless connection of the technical layer, but also in the mutual enhancement of the economy.

At the liquidity base level, stablecoins solve the transaction friction caused by volatile crypto assets and provide low-risk settlement for DeFi. In the automated market maker (AMM) settlement model, more than 80% of the liquidity pools use stablecoins (e.g., DAI, USDC) as denominated assets, significantly compressing impermanent loss (IL). Lending protocols rely on stablecoins to build a credit derivative chain. Users pledge volatile assets (e.g., ETH) to borrow stablecoins, and their maximum debt value is constrained by the collateral ratio (debt ceiling = collateral value/collateral ratio), which can form a partial reserve system similar to that of a bank, thereby suppressing and mitigating the risk of a run. At the value scale level, it is reflected in the transfer of pricing power of stablecoins. DeFi interest rate markets (e.g., Compound) dynamically adjust interest rates based on stablecoin supply and demand: when the borrowing utilization rate (borrowing amount/deposit amount) exceeds the threshold, the algorithm automatically raises the deposit rate based on the stablecoin interest rate, forming a decentralized price signal. Yield farming strategies further transform stablecoins into yield anchors. For example, users deposit USDC to obtain a 3% base yield, and superimpose governance token incentives (e.g., COMP) to achieve cross-protocol arbitrage.

At the risk buffer level, stablecoins achieve relief and reduce decentralized financial risks through liquidation upgrades andRWA credit enhancement.For example, stablecoins use a dynamic engine driven by general artificial intelligence (AGI) to analyze collateral volatility, gas costs, and market depth in real time, optimize and adjust liquidation thresholds, and minimize risks and losses. For example, stablecoins can enhance the credit of RWA, block the death spiral of decentralized models, and promote the reconstruction and improvement of the revenue model. The functional coupling of stablecoins and DeFi is essentially an on-chain experiment of the traditional financial credit creation mechanism. When the legal currency system is limited by cross-border friction, the two work together to build a new paradigm of global liquidity flow in seconds.

DeFi systematically reconstructs the stablecoin development model through mechanism innovation, and promotes its evolution from a fiat currency mirror that relies on centralized credit to an on-chain native tool with endogenous stability and sustainable returns. The core of the reshaping process lies in the innovation of the mortgage architecture, the optimization of the liquidation algorithm, and the transformation of the income model, which together constitute the underlying logic of the evolution of stablecoins.

In terms of mortgage innovation,DeFi protocols break through the limitations of traditional fiat currency reserves or pure algorithmic models, introduce RWA's hybrid mortgage mechanism, and form a double-layer credit support of "crypto assets + RWA".TakeMakerDAO ecology as an example, DAI incorporates U.S. Treasury tokens into its collateral library. When market fluctuations trigger DAI decoupling, the smart contract automatically auctions Treasury bonds to repurchase DAI, using the low volatility of physical assets to block the death spiral. The essence of the hybrid mortgage mechanism is to transform low-risk assets in the traditional financial market into a "ballast stone" for on-chain stability, replace inflationary tokens with RWA's cash flow, and build a self-circulating model of "protocol income = RWA interest - operating costs", so that stablecoin holders can obtain real income rather than a Ponzi scheme.

At the level of liquidation optimization,DeFi solves the problems of oracle delay and insufficient market depth through a dynamic risk pricing model.For example,DeFi introduces an AGI-driven liquidation engine to analyze collateral volatility, correlation coefficients, and on-chain liquidity data in real time, and dynamically adjusts the liquidation threshold. For another example, the surge in on-chain gas fees has led to insufficient incentives for liquidators, and DeFi can temporarily increase the collateral discount rate to attract arbitrageurs. It is worth noting that cross-chain atomic liquidation innovation can eliminate liquidity fragmentation caused by cross-chain bridge risks. For example, Circle's CCTP protocol allows USDC to implement atomic destruction/casting on multiple chains, thereby achieving cross-chain instant liquidation in seconds.

At the level of revenue model reconstruction,DeFi's reshaping process focuses on the de-bubble of revenue sources and the automation of distribution.Traditional stablecoins rely on transaction fees or governance token inflation to maintain revenue,and

DeFi's reshaping of the development of stablecoins faces the challenge of institutional adaptability.

DeFi's reshaping of the development of stablecoins faces the challenge of institutional adaptability.

For example, the lack of a legal entity in DAO forced MakerDAO to rely on an offshore SPV to hold U.S. debt tokens, resulting in high compliance costs; Hong Kong's Stablecoin Ordinance established adequate reserves and redemption guarantees, but the cross-border confirmation of RWA rights needs to deal with the regulatory conflict between the U.S. SEC's securities determination and the EU MiCA's payment instrument classification, and it is urgent to break through through technical and institutional collaborative innovation. The essence of DeFi's reshaping of stablecoins is the on-chain migration of the credit creation paradigm. RWA provides physical asset endorsement, dynamic algorithms replace manual risk control, and real returns eliminate inflation models. When traditional finance is limited by the dilemma of cross-border settlement, DeFi builds a new paradigm of global liquidity in seconds through mechanism innovation.

Symbiotic Risks and Relationship Reconstruction

Stablecoins and DeFi synergistically promote the deep integration of traditional finance and decentralized on-chain finance. Stablecoins assume the three key functions of payment and settlement, underlying mortgage and accounting unit in DeFi. DeFi technology and mechanism innovation have further reshaped and innovated the development model of stablecoins. This symbiotic relationship is embedded with multiple tensions and may derive multi-level risks. The symbiotic relationship between stablecoins and DeFi is undergoing the dual test of systemic risk and institutional reconstruction. The mechanism of symbiotic risk generation is rooted in structural fractures in three dimensions. The first is the algorithmic regulation dimension. The reflexivity death spiral exposes the fatal flaws of the pure algorithmic stable regulation mechanism. The demand for stablecoins and the value of associated tokens form a self-reinforcing positive feedback loop through smart contracts (for example, the growth of UST demand pushes up the scarcity of LUNA). When market expectations reverse, the contract forced issuance mechanism will exponentially amplify the depreciation pressure. For example, UST evaporated $40 billion in market value in 72 hours. The second is the liquidation execution dimension. The gap between real-time pricing on the chain and RWA's low-frequency valuation (for example, quarterly real estate assessments) leads to distorted collateral rates. In particular, the irreconcilability between the legal liquidation process, which takes several months, and the stablecoin T+0 redemption demand amplifies the risks and conflicts of liquidation. The third is the sovereign regulatory dimension. The US SEC identifies RWA as a security, and the EU MiCA restricts the trading volume of non-euro stablecoins, revealing the fundamental contradiction between the borderlessness of the chain and the sovereign boundaries.

Faced with the multi-dimensional symbiotic risks of stablecoins and DeFi, it is necessary to reconstruct and improve technology and systems. In the field of risk pricing, a dynamic clearing engine can be used to convert traditional risk management and control models into executable codes on the chain by real-time analysis of collateral volatility, market depth and cross-asset correlation, thus technically bridging the gap between time and space. In the field of institutional integration, zero-knowledge proof technology can compile regulatory rules into autonomous codes, making compliance independent of manual intervention. The deep significance of the reconstruction process lies in the paradigm shift of financial infrastructure. Traditional cross-border clearing is subject to institutional friction (agency costs and judicial lags). The on-chain mechanism realizes the dimensionality upgrade of the global clearing network through spatial reconstruction (for example, RWA tokenization introduces physical asset liquidity), time compression (for example, AGI compresses risk response to seconds), and rule encoding (zero-knowledge proof embeds multi-national supervision). When algorithm transparency (explainable AI cracks the black box), legal adaptability (legislation grants DAO legal person status) and technical reliability (for example, quantum audit protocol) form a balance, stablecoins and DeFi will upgrade from instrumental complementarity to institutional symbiosis.

Stablecoins andRWA Mechanism Mutual Construction

Stablecoins andRWA Tokenization and integration are reshaping the infrastructure of the global financial system and promoting the deep integration of traditional finance and DeFi. The core of integrated development and change lies in the tokenization of RWA, which tokenizes physical assets such as real estate, bonds, and carbon credits through blockchain technology, giving them liquidity, programmability, and global tradability. As a value anchoring tool on the chain, stablecoins can provide transaction media, liquidity support, and cross-border settlement support for RWA tokenization. The coordinated evolution of the two can not only optimize the efficiency of capital allocation, but also give birth to a new financial paradigm. The introduction of the Stablecoin Ordinance in Hong Kong, China and the GENIUS Act in the United States not only laid the foundation for the compliance development of stablecoins, but also provided institutional guarantees for the on-chainization of RWA. The regulatory certainty of stablecoins has enhanced market confidence, and RWA tokenization has further enriched the underlying credit support of stablecoins. For example, MakerDAO has included the U.S. Dollar Treasury Token (OUSG) in the collateral pool, enabling DAI holders to obtain U.S. Treasury returns in compliance with regulations and de-bubble the stablecoin return structure.

On a technical level,RWA's on-chain nature relies on smart contracts, oracles, and cross-chain interoperability. Smart contracts ensure the automated distribution of asset returns.For example,RWA returns can be distributed to global investors in real time through on-chain smart contracts. The oracle is responsible for synchronizing off-chain asset data (e.g., real estate valuations, bond interest rates) to the blockchain to ensure the value consistency of on-chain tokens and physical assets. Cross-chain technology (e.g., Circle's CCTP protocol) further solves the liquidity fragmentation problem of RWA in a multi-chain ecosystem, enabling tokenized assets to flow seamlessly between different blockchains.

In application scenarios,the combination of RWA tokenization and stablecoins has shown great potential in green finance, cross-border payments and private credit.In green finance, GCL Energy and Ant Digits have cooperated to complete the world's first photovoltaic green assetRWA financing, tokenizing the income rights of distributed photovoltaic power stations and achieving instant settlement for global investors through stablecoins. ... the cross-border payment field, the JD-HKD stablecoin program launched by JD Technology achieves efficient clearing of cross-border trade through the Hong Kong regulatory sandbox, which can significantly reduce the cost and delay of the traditional SWIFT system.

The private credit market tokenizes the accounts receivable of small and medium-sized enterprises in emerging markets through unsecured lending agreements (for example, the Goldfinch agreement), injecting real income assets into DeFi while solving the redundancy problem of the middle links in the traditional credit market.

In the field of cross-border payments,

<

However, the integration process of stablecoins andRWA tokenization still faces multiple challenges. In terms of legal title confirmation,DAO lacks legal person status, resulting in RWA's off-chain asset custody relying on the offshore SPV structure, which increases compliance costs. The inconsistency of valuation standards leads to deviations in the on-chain pricing of non-standard assets (e.g., real estate, carbon credits), which may trigger market manipulation risks.

regulatory arbitrage issues are becoming increasingly prominent,and qualitative differences inRWA tokenization in different jurisdictions (e.g., security tokens vs. payment tokens) may lead to cross-border compliance conflicts.

In the future, the deep integration of stablecoins and RWA tokenization may evolve in three directions:Focus on the tokenization of highly liquid assets (e.g., U.S. Treasuries and money market funds) in the short term, expand to alternative assets such as real estate and private equity in the medium term, and achieve real-time clearing and global flow of trillion-level assets through quantum computing and

AI dynamic pricing technology in the long term. Quantheora's quantum stablecoin Q-Stable has attempted to incorporate multi-asset portfolios such as U.S. Treasuries, gold, and carbon credits into a dynamic anchoring mechanism, and adjust weights in real time through the AGI algorithm to maintain stability under extreme market conditions. At the same time, the advancement of regulatory technology (e.g., zero-knowledge proof audits) will further enhance the transparency of RWA tokenization, and the exploration of the Basel Accord on the chain may transform the risk management framework of traditional finance into executable smart contract rules. The mutual construction and integration of stablecoins and RWA tokenization mechanisms is not only a technical innovation, but also a deep-seated reform of the financial system. Hong Kong's regulatory sandbox, offshore SPV architecture and stablecoin legislation provide a test field for the mutual construction and integration of the two, but global compliance and standard unification still need to be broken through. As traditional financial institutions (e.g., BlackRock, JPMorgan Chase) accelerate the layout of on-chain assets and DeFi protocols (e.g., Aave, MakerDAO) continue to optimize the mortgage and liquidation mechanisms of RWA tokenization, a more liquid, inclusive and efficient global financial system is taking shape. The success of this process ultimately depends on the ternary balance of technical reliability, legal adaptability and regulatory coordination.

Stablecoin Ecosystem Improvement and Scenario Expansion

The ecological improvement and application scenario expansion of stablecoins have evolved from a simple technical experiment to an institutional and technological collaborative revolution deeply embedded in global financial governance. From the perspective of the application scenario structure of stablecoins, stablecoins have developed from the initial cryptocurrency medium to the fields of cross-border payment, DeFi, and RWA tokenization (see Table 5). For example, in the field of cross-border payments, stablecoins reduce transaction costs by 80% compared to traditional remittances. For another example, stablecoins are showing a rapid growth trend in e-commerce payments, value storage, and blockchain-based financial innovation. The process of ecological and scenario expansion not only depends on the evolution and innovation of stablecoins themselves, but also on building a dynamic and reasonable balance in the triangular relationship between regulatory framework, market structure and technical infrastructure.

Table 5 Application scenarios and functions of the stablecoin market

Source: The author compiled it based on public information.

First, in terms of the institutional framework, it has evolved from regulatory ambiguity to the foundation of a compliance framework, providing legal and policy guarantees for the widespread application and scenario expansion of stablecoins. Global stablecoin regulation and governance is undergoing a paradigm shift from passive response to active design. As the world's first formally implemented full-chain regulatory framework, the Stablecoin Ordinance of Hong Kong, China (effective on August 1, 2025) requires issuers to operate with a license, have full (100%) reserve asset coverage and third-party custody, and creatively allows licensed issuers to choose different fiat currencies as the anchor fiat currencies for issuing stablecoins. This institutional design not only prevents the risk of no reserves similar to the collapse of the Terra ecosystem, but also provides a test field for non-US dollar assets such as offshore RMB stablecoins, and promotes Hong Kong, China to become a multi-stablecoin hub. In contrast, the "GENIUS Act" of the United States reflects the logic of the extension of US dollar hegemony to the chain. It requires that the compliance of stablecoins must be anchored to the US dollar or US Treasury bonds, and only issued by entities registered in the United States. In essence, it transforms the stablecoin market into a new engine for US Treasury demand. The EU's MiCA framework adopts a defensive strategy to limit the daily trading volume of non-euro stablecoins (no more than 200 million euros) in an attempt to protect the status of the euro in the open market. The differentiated systems and policies in the process of stablecoin supervision and governance have profoundly shaped the boundaries and structure of stablecoin application scenarios. For example, the open framework in Hong Kong, China, has enabled institutions such as JD.com and Standard Chartered to apply for licenses to issue offshore RMB stablecoins to serve the trade settlement of the Belt and Road Initiative; the US system forces issuers such as Circle to allocate a high proportion of reserves to US bonds, strengthening the anchoring position of the US dollar in on-chain payments.

Second, in the dimension of ecological deepening, from payment tools to asset engines, the advancement promotes the dual breakthroughs of stablecoins in "expansion" and "penetration".As stablecoins transform from payment tools to asset engines, their application scenarios are experiencing the dual breakthroughs of "horizontal expansion" and "vertical penetration". In the field of cross-border payments, the traditional agency bank model faces efficiency bottlenecks due to the multi-layer intermediaries of the SWIFT system. Stablecoins can achieve "point-to-point" value direct access through the native settlement capabilities of blockchain. For example, the multilateral central bank digital currency bridge (mBridge), which connects the central bank systems of multiple countries (regions) such as China and Saudi Arabia, supports the direct exchange of CBDC and offshore RMB stablecoins, which can reduce corporate cross-border settlement from 3-5 days to seconds. For another example, 20 African countries have achieved free and instant transfer of USDT through the cooperation between Aptos and YellowCard, and Kenyan farmers do not need to bear the high handling fees of traditional channels when paying Nigerian suppliers. In the field of integration of the real economy and on-chain finance, the core leap of stablecoins lies in their becoming the value medium of RWA tokenization. For example, in the Ensemble sandbox of the Hong Kong Monetary Authority, Longxin Group split the income rights of 9,000 charging piles into 100 million yuan of digital assets, and international investors subscribed through offshore RMB stablecoins and obtained automatic dividends on the chain. In the field of public governance, the smart contract capabilities of stablecoins are used to reshape government services. For example, the Colombian bank Bancolombia issued the COPW stablecoin anchored to the local currency. Farmers receive agricultural subsidies through mobile phones, and the funds are automatically locked in production purposes such as seeds and fertilizers, effectively reducing the risk of misappropriation. The above cases show that stablecoins have been upgraded from transaction settlement tools to programming interfaces for social resource allocation.

Third, in terms of technical support, from tool support to scenario innovation, the reconstruction and improvement of stablecoin functions are promoted. The innovation of application scenarios depends on the continuous evolution of underlying technologies, which is mainly reflected in three aspects: First, the breakthrough of cross-chain interoperability breaks the blockchain"island" effect. For example, the development of new technologies such as LayerZero full-chain protocol enables USDC, USDT, etc. to achieve seamless circulation between mainstream public chains such as Ethereum and Solana. Second, the two-way enhancement of compliance and security. Regulatory requirements force the upgrade of risk control technology, and zero-knowledge proof technology is used for on-chain supervision and auditing, which can not only ensure transparency but also avoid the disclosure of commercial secrets. Third, the integration and docking of traditional financial systems is realized, while improving efficiency and maintaining the bottom line of financial security. For example, the quasi-stablecoin JPMD that JPMorgan Chase Bank is preparing to promote is supported by regulated deposits and is piloted on the public blockchain. In essence, traditional financial institutions actively connect with crypto-chain finance without giving up compliance, stability or control. Although the stablecoin scenario is expanding rapidly, its ecological reconstruction and improvement still face the triple challenges of monetary sovereignty game, commercial sustainable development and technical trust bottleneck. First, the essence of private stablecoins is to build a "quasi-central bank system" parallel to sovereign currencies, which will erode the monetary sovereignty of the country where the business is located. Secondly, the current mainstream stablecoin income depends on reserve interest. The decline in deposit interest may lead to a decrease in net profit, forcing the issuer to explore new sources of income such as handling fees and intermediary fees, which will weaken the cost advantage of traditional payments. Finally, the technical ethics and risk issues derived from technical black boxes and loopholes have led to a bottleneck in public technical trust, which is an important factor hindering the expansion of stablecoin applications and the improvement of the ecosystem. For example, cases such as algorithmic stablecoin depegging (e.g., Terra crash) and Curve pool reentry attacks that caused DAI to fluctuate dramatically indicate that smart contract vulnerabilities are still the main source of systemic risk. The development of stablecoins can only avoid the new monopoly of financial hegemony in the digital age and truly realize the positive cycle of scenarios and ecology of "technology empowerment, institutional protection, and scenario implementation" through multilateral collaboration (e.g., mBridge project) to establish a rule framework that takes into account both efficiency and fairness.

Summary and enlightenment

Driven by the global wave of digital currency, stablecoins have evolved from marginal financial experiments to key variables in the reconstruction of the international monetary system. The evolution of their technical characteristics, market ecology and regulatory framework has promoted the integrated development of traditional finance and on-chain finance while challenging monetary and financial sovereignty. The development of stablecoins has important implications and reference significance for the reconstruction and improvement of my country's digital RMB ecosystem, and provides a new strategic path and direction for the internationalization of RMB. From the four dimensions of institutional adaptability, ecological synergy, technical controllability and global governance discourse power, we can build a digital RMB as the core infrastructure and RMB stablecoin as the driving force for business and market innovation, promote the modernization and internationalization of my country's monetary and financial system, and contribute Chinese solutions to the reshaping and improvement of the global monetary and financial system in the digital era.

First, maintain a dynamic balance between monetary sovereignty and market vitality in terms of institutional innovation. Global stablecoin regulation presents three paradigms of competition. The US dollar standard model of the "GENIUS Act" forces stablecoins to anchor US bonds, which is an extension of the US dollar hegemony on the chain and in the crypto economy. The EU's MiCA framework is characterized by defensive openness and limits the daily trading volume of non-euro stablecoins. The "Stablecoin Ordinance" of Hong Kong, China pioneered multi-currency compatible regulation, allowing offshore RMB stablecoins and Hong Kong dollar stablecoins to develop in parallel. At this stage, my country has strategically built a two-tier system framework of "offshore experiment-onshore control", using the "negative list + regulatory sandbox" mechanism in the offshore market of Hong Kong, China, to allow institutions (enterprises) to test innovative projects such as RWA tokenization and cross-border payments in a controllable environment. In the context of RMB not yet achieving free convertibility, the onshore RMB stablecoin adopts the strategy of establishing a "digital firewall", isolating the offshore and onshore capital pools through a separate accounting system, and the issuing institution controls the issuance and exchange quota. The two-tier system design not only retains the space for innovation, but also ensures that the final clearing right is controlled by the central bank through the "digital RMB reserve account" mechanism.

Second, in terms of ecological construction, promote the coordinated development of scenario expansion and penetration and RMB internationalization. The essence of the competition of stablecoins is the competition of application scenarios. At present, the main application scenarios such as cryptocurrency transactions and cross-border remittances dominated by US dollar stablecoins are not in line with my country's strategic interests. The key to the expansion of RMB stablecoin scenarios and the coordinated development of RMB internationalization lies in cultivating a differentiated ecosystem. In the short term, we can rely on the trade demand along the Belt and Road to develop a supply chain financial network based on offshore RMB stablecoins. At the same time, promoting the international development of RMB-denominated RWA will not only help improve the liquidity of real-world assets, but also avoid direct impact on onshore capital account controls. In the long term, we must reshape and improve the digital RMB ecosystem with digital RMB as the core infrastructure and stablecoin as the main body of market and business innovation. The role division and functional positioning of digital RMB and RMB stablecoin are conducive to maintaining the integrity of monetary sovereignty, but also help to fully release the vitality of market innovation and promote the internationalization of RMB.

Third, in terms of technical paths, reasonably balance controllable interoperability and system architecture security. The technical core of stablecoins lies in the distributed ledger of blockchain and the automated execution capability of smart contracts, which can achieve an order of magnitude improvement in cross-border payment efficiency. However, the efficiency advantages of technically controllable interoperability are usually accompanied by systemic risks. At present, mainstream stablecoins such as USDT, USDC, and DAI rely on the public chain ecosystem such as Ethereum. Their open architecture is fundamentally different from the "centralized management + limited distribution" hybrid model of my country's digital RMB. This technical heterogeneity causes cross-chain interoperability to rely on atomic swaps or bridge protocols, which increases transaction delays and security risks. At the same time, the pseudo-anonymity of public chains may have an impact on the effectiveness of foreign exchange management. To solve the dilemma, it is necessary to build a "layered and controllable" technical system. At the basic level, we can learn from the experience of the Ensemble sandbox of the Hong Kong Monetary Authority of China, set up authorized supervision nodes in the blockchain network, and realize real-time penetrating monitoring of transaction data. At the same time, protect commercial secrets through zero-knowledge proof technology. At the application level, we can focus on developing compliance function modules of smart contracts (for example, automatically triggering large transaction reports, sensitive area payment interception and other rules), and integrate regulatory requirements into the stablecoin circulation logic through coding.

Fourth, integrate the strategic game of financial security and order in global competition and cooperation. The global expansion of stablecoins has profoundly reconstructed the international monetary power structure. The United States has incorporated stablecoins into the US dollar system through the "GENIUS Act", which has strengthened the trend of "digital dollarization". my country should respond to challenges from the perspective of maintaining national financial security and reshaping the global financial order, and conduct strategic countermeasures. First, strengthen the competition for the right to speak on rules. At present, the "Stablecoin Ordinance" of Hong Kong, China, as the world's first comprehensive regulatory framework, has been recognized and referenced by many countries for its "sufficient reserves + licensed operation" principle. In view of this, my country can promote the formation of "international standards for stablecoin supervision" through multilateral platforms such as BIS and IMF, focusing on limiting the instrumentalization of unilateral sanctions (for example, freezing wallets in specific jurisdictions). Second, improve payment infrastructure substitution. At present, the mBridge project in which the People's Bank of China participates has connected the central bank (monetary authority) systems of multiple countries (regions). On this basis, it can actively promote the establishment of a new cross-border network with digital RMB as the settlement anchor and RMB stablecoin as the payment medium to avoid the risk of financial disconnection caused by the long-arm jurisdiction of the US dollar hegemony. The third is to enhance the construction of asset pricing power. At present, global commodities, carbon credits, etc. are still denominated in US dollars. They can be bound to China's import demand (for example, iron ore and crude oil) through RMB stablecoins, and gradually form RMB pricing inertia.

Weatherly

Weatherly