A quick overview of Redstone mainnet launch activities

Redstone, the Layer2 network developed by Lattice and focusing on the full-chain gaming ecosystem, is officially launched.

JinseFinance

JinseFinance

Author: Link

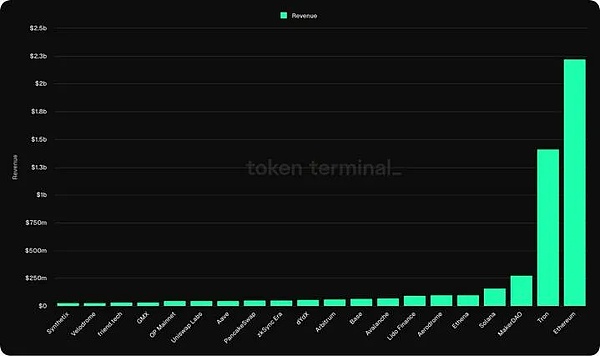

Today, we will explore the top 4 L1 and L2 by revenue and explore how much revenue these blockchains actually retain. After all, revenue generation is one of the most important indicators of whether a chain can continue to develop. Here, we define revenue as: total revenue minus token issuance.

Ethereum@Ethereum

In terms of revenue generated, Ethereum is far ahead of all other blockchains (including L1 and L2), with $2.22 billion in revenue over the past year. However, despite the impressive revenue, Ethereum recorded a net loss of $15 million.

Why? The main reason for the losses is that the issuance of new tokens has outpaced its revenue, and after a strong performance in the second half of 2023, its earnings so far this year have turned negative. This can be largely attributed to the shift of transaction activity to L2, which reduces the fees paid directly to the world computer. Therefore, despite Ethereum's large transaction volume and network activity, this migration has led to its earnings decline.

Tron @trondao

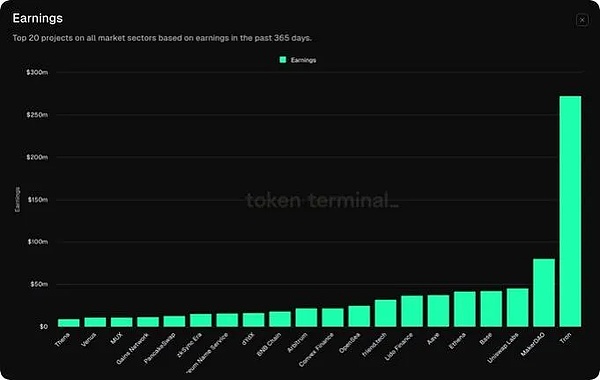

Tron ranks second in terms of overall revenue, with $1.4 billion in revenue over the past year. This success can be directly attributed to the network’s extensive stablecoin activity, which ranks second only to Ethereum among networks with the most stablecoins, thanks to heavy usage in developing economies such as Argentina, Turkey, and countries in Africa, where high inflation remains an ongoing issue. While some may call it a one-trick pony, this “one-trick pony” has generated $271 million in revenue over the past year, making it the most profitable blockchain to date.

Solana @solana

Solana also ranks high in terms of revenue, generating $157 million in revenue over the past year. Popularity as a memecoin hub, capital growth from airdrops, technical upgrades to address spam issues, and support for leading trends like AI have all contributed to its prominence and strong revenues in this cycle. However, this growth has not translated into earnings. Taking into account token issuance to stakers and operational costs, Solana has posted a net loss of $2.53 billion over the past four full quarters, completely wiping out its revenues and falling into a hole.

Avalanche @avax

Avalanche, which has its own memecoin fund, ranks fourth, generating $69 million in revenues over the past year.

Avalanche, known for its subnet scaling solution and focus on gaming, is about to launch a major upgrade called ACP-77, which will improve the experience of deploying and managing subnets, making it more affordable and thus potentially increasing revenue. With this in mind, the chain still has a long way to go, as it faced a net loss of $860.6 million over the past year due to token issuance and operating costs.

Base

Despite being less than a year old, Base @coinbase’s L2, launched alongside OPStack, has quickly become a success by generating $66.6 million in revenue since its inception. Notably, @base has managed to retain 63% of its revenue, netting $42 million in the same period.

This success can be attributed to two key factors: First, Base’s implementation of blobs through EIP-4844 has significantly reduced costs, cutting costs from $9.34 million in Q1 2024 to $699,000 in Q2 2024. Second, Base has no native token, which makes it more competitive and avoids the distribution-related fees incurred by other L2s.

Arbitrum

Arbitrum is the largest L2 by TVL, with $17.2 billion locked and generating $61.14 million in revenue over the past year.

As the hub of DeFi, leading DeFi protocols such as GMX and Pendle are developed on Arbitrum, and its SDK also provides the main infrastructure for L3s such as SankoGameCorp, Degentokenbase and XAI. Although revenue has not yet reached the level of Base, Arbitrum has achieved $21.8 million in revenue in the past year, especially in the second quarter, when its expenses dropped to only $613,000, compared with $20 million in the first quarter.

zkSync Era

As one of the leading L2s based on zero-knowledge (ZK) technology, @zksync has generated $53.3 million in revenue in the past year.

Since the June 2023 airdrop, the network’s TVL has increased significantly, with ZK technology adding approximately $850 million in value to the chain, although this amount has gradually decreased as users sell the airdropped tokens. However, the chain has remained profitable, netting $15.3 million over the past year and $17.5 million over the past four full quarters. Although zkSync ranks only eighth in the L2 rankings, its profitability makes it the third most profitable L2.

OP Mainnet

As the core of Superchain, @Optimism has generated $44.6 million in revenue over the past year through sorter fees on its mainchain and projects such as zora and Base in the network.

In the second quarter of 2024, Optimism network activity reached record levels. Average daily active addresses grew to 121.6K, up 37% month-over-month, and average daily transactions also grew to 601K, up 28% month-over-month despite the market downturn. As with other L2s, EIP-4844 contributed significantly to this growth, with lower fees increasing network activity, which in turn increased Optimism’s net profitability by more than 150%. Despite this, Optimism remains deeply in the red, having incurred a net loss of $239 million over the past year due to retroactive airdrops, incentive programs, and operating costs.

However, when you look at these numbers, remember that, just like traditional finance (TradFi), profitability is only part of the story. No one is betting trillions on NVIDIA’s current financials, but rather the narrative behind it that drives its growth.

Narrative-driven investing is often the default choice for crypto buyers who want outsized returns by taking risks, but note that there are still networks that have built substantial businesses based on today's activity. By diving deeper into the revenues and earnings of the top L1s and L2s, we can get a clearer picture of the fundamental health of these networks and their place in the competitive landscape.

Redstone, the Layer2 network developed by Lattice and focusing on the full-chain gaming ecosystem, is officially launched.

JinseFinanceDive into the transformative world of Router Nitro as it launches its mainnet, redefining blockchain interoperability and setting new standards for a connected, innovative future. Explore the features, benefits, and far-reaching impact of Router Nitro on the blockchain ecosystem.

Weiliang

WeiliangPositioned as the "1st community-owned ZK Layer 2," ZKFair leverages on Polygon's Cloud Development Kit (CDK) and Celestia DA's ZK-L2, with technical support from Lumoz RaaS.

Brian

BrianEthereum Layer 2 network Optimism changed the project’s name to OP Mainnet.

TheBlock

TheBlockSui Labs has gained attention due to its approach to DeFi and its association with Mysten Labs, a Web 3.0 infrastructure organization.

Others

Others Coinlive

Coinlive Explore the most interesting projects on Polygon and find the best plays for the Polygon narrative.

Coinlive Coinlive Ethereum PoW has revealed plans for its mainnet. It has also released information on preparing full nodes.

Beincrypto

BeincryptoAfter four years of waiting, THORChain’s new mainnet “marks the achievement of a fully functional, feature-rich protocol with a large ecosystem and strong community.”

Cointelegraph

Cointelegraph